- Home

- »

- Next Generation Technologies

- »

-

Cloud Managed Services Market Size Report, 2026-2033GVR Report cover

![Cloud Managed Services Market (2026 - 2033)Report]()

Cloud Managed Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service Type (Business Services, Network Services), By Cloud Deployment (Public, Private), By End-user, By Verticals (BFSI, Healthcare), By Region, And Segment Forecasts

Market Size, 2025

$146.5BMarket Estimate, 2026

$160.8BMarket Forecast, 2033

$326.6BCAGR, 2026–2033

10.7%Cloud Managed Services Market Summary

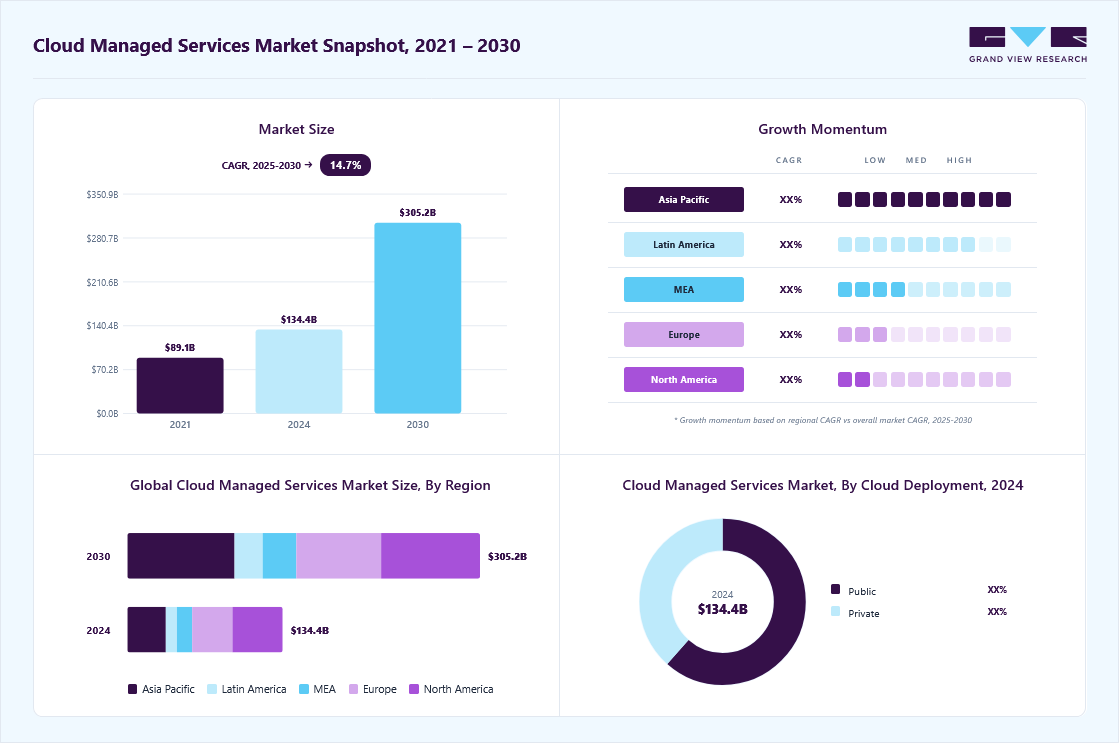

The global cloud managed services market size was valued at USD 146.5 billion in 2025 and is projected to grow from USD 160.8 billion in 2026 to USD 326.6 billion by 2033, at a CAGR of 10.7% from 2026 to 2033. The market in North America dominated with a revenue share of 41.8% in 2025. This growth is driven by increasing adoption of cloud computing, the need for cost optimization, and the rising complexity of IT environments.

Key Market Trends & Insights

- By Type: Security services segment dominated the market, with a revenue share of 27.3% in 2025.

- By Cloud Deployment: Public segment held the largest market share of 62.4% in 2025.

- By End User: Large enterprises segment held the largest revenue share in 2025.

- By Verticals: BFSI segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (41.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 146.5 Billion

- Estimated market size in 2026: USD 160.8 Billion

- Projected market size by 2033: USD 326.6 Billion

- CAGR (2026-2033): 10.7%

Several key factors, including the increasing adoption of cloud computing, the need for cost optimization, and the rising complexity of IT environments, drive the growth of the cloud-managed services market. Organizations across industries are shifting to cloud-based solutions to enhance scalability, flexibility, and operational efficiency while reducing capital expenditures on IT infrastructure. Additionally, the growing reliance on digital transformation initiatives and the surge in remote work and hybrid cloud deployments have heightened the demand for managed services that ensure seamless cloud operations, security, and compliance. The rapid advancements in artificial intelligence (AI), automation, and analytics further contribute to market expansion by enabling service providers to offer more intelligent, proactive, and cost-effective solutions.")

Moreover, businesses are increasingly outsourcing cloud management to specialized providers to mitigate cybersecurity risks, address skill shortages, and focus on core competencies. As regulatory requirements and data privacy concerns become more stringent, managed service providers (MSPs) play a crucial role in ensuring compliance and risk management, further driving market growth.

The increasing adoption of cloud computing is a fundamental driver of the cloud-managed services market. Organizations across industries are transitioning from traditional on-premises infrastructure to cloud-based environments to enhance agility, scalability, and cost efficiency. Cloud computing enables businesses to access computing resources on demand, reducing the need for large capital expenditures and allowing for a more flexible operational model. As enterprises accelerate their digital transformation efforts, the reliance on managed services to optimize cloud performance and ensure seamless integration continues to grow.

The need for cost optimization is another key factor propelling the demand for cloud-managed services. Maintaining an in-house IT team to manage cloud infrastructure can be costly, requiring investments in skilled personnel, infrastructure, and ongoing maintenance. By outsourcing cloud management to specialized service providers, businesses can significantly reduce operational costs while benefiting from expert oversight. Managed services offer predictable pricing models, such as subscription-based or pay-as-you-go plans, helping organizations align IT expenses with business needs.

The rising complexity of IT environments has also expanded the cloud-managed services market. As enterprises adopt multi-cloud and hybrid cloud strategies, managing diverse cloud platforms, applications, and security protocols becomes increasingly challenging. Cloud-managed service providers (MSPs) help businesses navigate this complexity by offering end-to-end management, from cloud migration and optimization to security and compliance. This ensures seamless operations, reduced downtime, and enhanced overall performance.

Market Dynamics

The global cloud managed services market is experiencing robust growth, driven by increasing enterprise adoption of hybrid and multi-cloud environments, growing complexity of IT infrastructure management, and rising demand for cost optimization and operational efficiency. Organizations are increasingly outsourcing cloud monitoring, migration, security, governance, and performance management functions to specialized service providers to reduce internal IT burdens and accelerate digital transformation initiatives. Additionally, the integration of AI-driven automation, managed cybersecurity services, FinOps solutions, and cloud-native technologies is reshaping service offerings, enabling enterprises to improve scalability, resilience, and business agility. Growing regulatory requirements, remote workforce expansion, and the need for continuous cloud optimization are further supporting demand for cloud-managed services across industries.

The increasing sophistication of cyber threats and the growing complexity of cloud environments are driving demand for managed cloud security services, creating significant growth opportunities for cloud managed service providers. As enterprises adopt hybrid and multi-cloud architectures, they require continuous monitoring, threat detection, vulnerability management, compliance support, and incident response capabilities that often exceed internal IT resources. Consequently, organizations are increasingly partnering with managed service providers (MSPs) to secure cloud workloads, reduce risk exposure, and maintain regulatory compliance while focusing on core business operations.

For instance, in May 2026, Reinvent Telecom launched MyCloud Managed Security, a fully managed cybersecurity solution that combines Managed XDR (MXDR), vulnerability management, SIEM, SOAR, endpoint protection, compliance monitoring, and 24/7 Security Operations Center (SOC) services. The launch reflects the growing market demand for integrated managed security offerings that enable businesses to secure cloud, network, and endpoint environments without building in-house cybersecurity infrastructure.

The growth of the cloud managed services market is restrained by concerns related to vendor lock-in, data security, and reduced control over critical IT operations. Organizations often face challenges when migrating workloads between cloud environments due to proprietary technologies, integration complexities, and potential service disruptions, which can increase switching costs and limit operational flexibility. Additionally, enterprises operating in highly regulated industries remain cautious about outsourcing sensitive data and mission-critical applications, as compliance, data sovereignty, and cybersecurity risks continue to be key considerations. These concerns can slow the adoption of managed cloud services, particularly among organizations with stringent governance and security requirements.

The increasing adoption of artificial intelligence (AI), automation, and managed cybersecurity solutions presents a significant opportunity for the cloud managed services market. Enterprises are seeking intelligent cloud management platforms that can automate infrastructure monitoring, optimize cloud spending, improve workload performance, and strengthen threat detection capabilities across complex multi-cloud environments. Furthermore, the growing frequency of cyberattacks is accelerating demand for managed security services integrated within cloud offerings. As organizations continue to prioritize operational efficiency, resilience, and security, service providers offering AI-powered cloud operations, FinOps capabilities, and comprehensive managed security solutions are expected to benefit from substantial growth opportunities over the forecast period.

Analyst Perspective

The market is entering a phase where enterprise demand is shifting from standalone technology deployments toward integrated, outcome-driven digital transformation solutions that combine connectivity, cloud, cybersecurity, AI, automation, and managed services. As organizations accelerate modernization initiatives, they increasingly seek strategic partners capable of delivering end-to-end solutions rather than point products. This trend is driving market consolidation around vendors with strong ecosystem partnerships, global delivery capabilities, and the ability to manage complex multi-vendor environments across industries.

The primary competitive advantage will belong to providers that can seamlessly integrate next-generation technologies such as AI, edge computing, private networks, cloud platforms, and advanced analytics into a unified service framework. While established players benefit from scale, customer trust, and extensive infrastructure assets, emerging players are capitalizing on agility and specialized expertise. Over the long term, the ability to deliver measurable business outcomes, reduce operational complexity, and provide industry-specific solutions will be the key differentiator determining market leadership.

Service Type Insights

Based on type, the security services segment led the market with the largest revenue share of 27.3% in 2025. Security services dominate the cloud-managed services market due to the increasing frequency and sophistication of cyber threats, data breaches, and regulatory compliance requirements. As businesses migrate their critical workloads and sensitive data to the cloud, they face heightened risks related to unauthorized access, ransomware attacks, and insider threats. Cloud security services, including threat detection, identity and access management, encryption, and firewall management, help organizations safeguard their cloud environments against evolving cyber risks.

Additionally, stringent data protection regulations such as GDPR, HIPAA, and industry-specific compliance mandates require businesses to implement robust security frameworks, further driving the demand for managed security services. Many enterprises lack the in-house expertise to manage complex security protocols effectively, prompting them to rely on specialized managed service providers (MSPs) for continuous monitoring, incident response, and regulatory compliance assurance. As security remains a top priority for cloud adoption, the demand for managed security services continues to outpace other service segments.

The mobility services segment is expected to grow at a significant rate during the forecast period. Mobility services are experiencing significant growth in the cloud-managed services market, driven by the widespread adoption of remote work, mobile-first business models, and the increasing use of enterprise mobility solutions. The proliferation of smartphones, tablets, and other connected devices has transformed workplace dynamics, necessitating seamless and secure access to cloud applications from any location. Cloud-managed mobility services, including mobile device management (MDM), enterprise mobility management (EMM), and mobile application security, enable businesses to enhance productivity while maintaining stringent security controls. As organizations embrace bring-your-own-device (BYOD) policies and hybrid work environments, the need for comprehensive mobility solutions to manage access, data security, and endpoint compliance has surged.

Cloud Deployment Insights

Based on cloud deployment, the public segment led the market with the largest revenue share of 62.4% in 2025. The increasing adoption of cloud-native technologies, cost-efficiency, and the need for scalable, on-demand computing resources fuels the substantial growth in public cloud in the cloud-managed services market. Enterprises leverage public cloud services to drive digital transformation, support remote work, and enhance business agility. Public cloud deployments provide businesses access to advanced technologies such as artificial intelligence (AI), big data analytics, and serverless computing without large upfront investments in infrastructure. Furthermore, the rise of multi-cloud strategies, where organizations use multiple public cloud providers to optimize performance and avoid vendor lock-in, has accelerated the adoption of public cloud services. As public cloud security capabilities continue to improve and regulatory barriers decrease, its adoption is expected to grow further across industries.

The private segment is expected to grow at a significant rate during the forecast period. The growth of private cloud in the cloud managed services market is primarily driven by its ability to provide enhanced security, control, and compliance, making it the preferred choice for enterprises operating in highly regulated industries such as finance, healthcare, and government. Organizations handling sensitive data prioritize private cloud deployments to maintain stringent data protection standards, ensure regulatory compliance, and mitigate cybersecurity risks. Private cloud environments offer greater customization, enabling businesses to tailor infrastructure, security protocols, and resource allocation to their specific needs. The growing demand for hybrid cloud models, where private cloud serves as the foundation for mission-critical workloads while integrating with public cloud services, further reinforces its leading position in the market.

End-user Insights

Based on end user, the large enterprises segment led the market with the largest revenue share of 65.7% in 2025. The dominance of large enterprises in the cloud-managed services market is primarily driven by their complex IT infrastructure, higher cloud adoption rates, and the need for advanced security and compliance solutions. Large organizations operate across multiple locations and business units, requiring robust cloud management services to ensure seamless integration, scalability, and operational efficiency. Additionally, they often deal with vast amounts of sensitive data, making security, regulatory compliance, and risk management top priorities. Cloud-managed service providers (MSPs) offer tailored solutions, including automated monitoring, AI-driven analytics, and multi-cloud management, enabling large enterprises to optimize costs, improve performance, and focus on core business functions. Furthermore, given their substantial financial resources, large enterprises are more willing to invest in comprehensive cloud management solutions, reinforcing their dominance in this segment.

The small & medium enterprise (SME) segment is expected to grow at the fastest rate during the forecast period. The increasing accessibility of cloud technologies, cost-saving benefits, and the need for operational agility drive SMEs' significant growth in the cloud-managed services market. SMEs rapidly adopt cloud solutions to reduce capital expenditures on IT infrastructure while gaining access to enterprise-grade technologies. The scalability and flexibility of cloud-managed services enable SMEs to expand their digital capabilities without the burden of managing complex IT environments. Moreover, the rise of subscription-based and pay-as-you-go pricing models makes cloud services more affordable, allowing SMEs to leverage managed services without large upfront investments. As cybersecurity threats grow and regulatory requirements become more stringent, SMEs increasingly rely on MSPs to enhance data security, ensure compliance, and maintain business continuity, further accelerating their adoption of cloud-managed services.

Verticals Insights

Based on verticals, the BFSI segment led the market with the largest revenue share of 18.6% in 2025. The BFSI sector dominates the cloud-managed services market due to its high dependence on secure, scalable, and resilient IT infrastructure. Financial institutions require advanced cloud solutions to handle vast amounts of transactional data, ensure seamless digital banking experiences, and maintain uninterrupted financial operations. The increasing adoption of cloud computing in BFSI is driven by the need for real-time data analytics, fraud detection, and enhanced cybersecurity measures. Managed cloud services enable banks and financial firms to comply with stringent regulatory requirements such as PCI-DSS, GDPR, and Basel III while ensuring data integrity and business continuity. Additionally, the rise of fintech innovations, mobile banking, and AI-driven financial services has further accelerated the adoption of cloud-managed services in this sector, solidifying its position as the leading vertical.

The government segment is expected to grow at a significant rate during the forecast period due to the increasing focus on digital transformation, e-governance, and data-driven decision-making. Governments worldwide are modernizing their IT infrastructure to enhance public service delivery, improve operational efficiency, and ensure data security. Cloud-managed services enable public sector organizations to scale IT resources efficiently, reduce operational costs, and enhance disaster recovery capabilities. Furthermore, the growing emphasis on cybersecurity and compliance with national data protection regulations drives government agencies to adopt managed cloud solutions for secure data storage and access. The expansion of smart city initiatives, digital identity programs, and AI-driven governance further propels the demand for cloud-managed services, making it one of the fastest-growing verticals in the market.

Regional Insights

North America dominated the global zero-trust security market with the largest revenue share of 41.8% in 2025. In North America, the cloud managed services industry is characterized by rapid digital transformation across industries, with a strong focus on hybrid and multi-cloud environments. Companies increasingly adopt cloud solutions for enhanced scalability, security, and cost-efficiency. The rise of edge computing, AI-driven automation, and increased regulatory requirements, particularly data privacy and security, also drive regional growth.

U.S. Cloud Managed Services Market Trends

The cloud managed services market in the U.S. held the largest share in the North America region in 2025. In the U.S., the cloud managed services market is witnessing significant growth due to widespread cloud adoption in the healthcare, finance, and telecom sectors. The need for enhanced cybersecurity, compliance with regulations like HIPAA, and the adoption of AI and machine learning are key trends fueling this market.

Europe Cloud Managed Services Market Trends

The cloud managed services industry in Europe is expected to grow significantly at a CAGR of over 17% from 2026 to 2033. In Europe, the cloud managed services industry is evolving due to a mix of regulatory pressures, particularly around GDPR and the increasing adoption of cloud-native technologies. European businesses focus on cloud solutions to improve efficiency, reduce costs, and meet compliance requirements while integrating artificial intelligence and machine learning into cloud services.

The U.K. cloud managed services industry is expected to grow rapidly in the coming years. In the U.K., there is a growing demand for cloud services in sectors like finance and public services. Companies are moving towards cloud-based solutions for enhanced security, improved business agility, and regulatory compliance, especially following Brexit, which has heightened data residency concerns.

The cloud managed services industry in Germany held a substantial market share in 2025. In Germany, cloud managed services industry is expanding rapidly, driven by the country's strong manufacturing sector and a growing focus on Industry 4.0. German companies are adopting cloud solutions to support digitalization, automation, and innovation in manufacturing, while compliance with GDPR remains a top priority.

Asia Pacific Cloud Managed Services Market Trends

The cloud managed services industry in Asia Pacific is expected to grow significantly at a CAGR of over 21% from 2026 to 2033. In the Asia Pacific region, the cloud managed services industry is growing rapidly as businesses in countries like China, Japan, and India embrace digital transformation. The demand for cloud solutions is driven by the rise of IoT, smart cities, and the need for scalable and flexible IT infrastructure to support fast-growing economies and industries.

China cloud managed services market held a substantial share in 2025. In China, the cloud managed services market is expanding rapidly due to the government's push for digital infrastructure development, the rise of e-commerce, and large-scale cloud adoption by both state-owned and private enterprises. The focus on cybersecurity and data localization regulations also plays a crucial role.

The cloud managed services market in Japan held a substantial share in 2025. In Japan, the cloud managed services industry is growing as manufacturing, automotive, and retail companies seek to modernize their IT infrastructure. Adopting cloud-based services, along with integrating AI and automation, enables businesses to enhance operational efficiency and innovation.

India cloud managed services market is expanding rapidly. In India, the cloud managed services industry is witnessing a significant growth driven by the increasing digitalization of enterprises, a large IT services outsourcing sector, and the rise of startups. The growing demand for cloud adoption among SMEs and government initiatives promoting digital infrastructure further accelerates the market's expansion.

Key Cloud Managed Services Company Insights

Key players operating in the cloud managed services market include IBM Corporation, Cisco Systems, Inc., Telefonaktiebolaget LM Ericsson, Verizon, Accenture, NTT DATA Corporation, Huawei Technologies Co., Ltd., Fujitsu, CHINA HUAXIN, CenturyLink, and Trianz. The companies focus on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In April 2024, IBM and HashiCorp Inc., a prominent company specializing in multi-cloud infrastructure automation, announced a definitive agreement under which IBM acquired HashiCorp for USD 35 per share in cash, reflecting an enterprise value of USD 6.4 billion. HashiCorp's portfolio of products offers comprehensive security lifecycle management and infrastructure lifecycle management solutions, empowering enterprises to automate their hybrid and multi-cloud environments. This acquisition is a further testament to IBM's ongoing commitment and investment in hybrid cloud and artificial intelligence (AI), the two most transformative technologies for its clients.

-

In April 2024, Fujitsu Limited and Oracle announced a collaboration to provide sovereign cloud and AI capabilities to meet the digital sovereignty needs of Japanese businesses and the public sector. Through Oracle Alloy, Fujitsu will enhance its hybrid IT offerings under Fujitsu Uvance, supporting customers in growing their businesses and addressing societal challenges. This partnership will enable Fujitsu to operate Oracle Alloy independently within its data centers in Japan, granting the company greater control over its operations.

Key Cloud Managed Services Companies:

The following key companies have been profiled for this study on the cloud managed services market.

-

Accenture

-

CenturyLink

-

CHINA HUAXIN

-

Cisco Systems, Inc.

-

Fujitsu

-

Huawei Technologies Co., Ltd.

-

IBM Corporation

-

NTT DATA Corporation

-

Telefonaktiebolaget LM Ericsson

-

Trianz

-

Verizon

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Mature Players (IBM Corporation, Cisco Systems, Inc., Telefonaktiebolaget LM Ericsson, Verizon, Accenture, NTT DATA Corporation, Huawei Technologies Co., Ltd., Fujitsu, CenturyLink)

- Expand end-to-end digital transformation, cloud, network, cybersecurity, and managed services portfolios through strategic partnerships and ecosystem development.

- Invest heavily in AI, automation, 5G, edge computing, and industry-specific solutions to strengthen enterprise customer retention and recurring service revenues.

- Strong global brand recognition, extensive customer base, and large-scale delivery capabilities across multiple regions.

- Significant R&D investments, established partner ecosystems, and comprehensive technology portfolios enable integrated solutions.

- High operational and workforce costs associated with maintaining global delivery networks and compliance requirements.

- Longer innovation and decision-making cycles compared to niche or specialized competitors reduce agility in addressing emerging market opportunities.

Emerging Players (CHINA HUAXIN, Trianz)

- Focus on specialized digital transformation, cloud modernization, analytics, and consulting services targeting specific industries and enterprise requirements.

- Expand through strategic alliances, innovation-led service offerings, and customer-centric engagement models to gain market share.

- Greater organizational agility and faster deployment of emerging technologies and customized solutions.

- Ability to address niche customer requirements with flexible service models and competitive pricing structures.

- More limited geographic reach, brand recognition, and customer penetration compared to established multinational competitors.

- Lower financial resources and ecosystem influence, which can constrain large-scale project execution and global expansion initiatives.

Cloud Managed Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 146.5 billion

Estimated market size in 2026

USD 160.8 billion

Projected market size by 2033

USD 326.6 billion

Growth rate

CAGR of 10.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share analysis, competitive landscape, growth factors, and trends

Segments covered

Type, cloud deployment, end user, verticals, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

IBM Corporation, Cisco Systems, Inc., Telefonaktiebolaget LM Ericsson, Verizon, Accenture, NTT DATA Corporation, Huawei Technologies Co., Ltd., Fujitsu, CHINA HUAXIN, CenturyLink, Trianz

Customization scope

Free report customization (equivalent to up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud Managed Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cloud managed services market report based on service type, cloud deployment, end-user, verticals, and region.

-

Service Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Business Services

-

Network Services

-

Security Services

-

Data Center Services

-

Mobility Services

-

-

Cloud Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Public

-

Private

-

-

End-user Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small and Medium Enterprises (SMEs)

-

-

Verticals Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

Retail & Consumer Goods

-

Telecom & ITES

-

Manufacturing & Automotive

-

Government

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

U.K.

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

U.A.E

-

Saudi Arabia

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Type

Revenue Capture Definition

Business Services

Revenue is generated through managed cloud consulting, migration, governance, compliance management, cloud cost optimization (FinOps), disaster recovery planning, and application lifecycle management services. Providers typically capture revenue through recurring subscription contracts, project-based engagements, and long-term managed service agreements.

Network Services

Revenue is earned through managed WAN, SD-WAN, network monitoring, connectivity management, traffic optimization, and cloud networking services. Recurring monthly service fees, network-as-a-service (NaaS) models, and usage-based billing represent the primary revenue streams.

Security Services

Revenue is captured through managed security operations, cloud security monitoring, threat detection, SIEM, SOAR, vulnerability management, identity and access management (IAM), compliance management, and incident response services. Revenue is primarily subscription-based and supported by premium cybersecurity service contracts.

Data Center Services

Revenue is generated through cloud infrastructure management, server monitoring, backup and recovery, storage management, workload optimization, and hybrid cloud administration services. Revenue is typically derived from managed infrastructure contracts, capacity-based pricing, and recurring service subscriptions.

Mobility Services

Revenue is earned through mobile device management (MDM), enterprise mobility management (EMM), endpoint management, application management, and support services for remote and hybrid workforces. Providers generate revenue through per-device, per-user, or enterprise-wide subscription models.

Segment - Cloud Deployment

Revenue Capture Definition

Public

Revenue is generated through the management of public cloud environments hosted on platforms such as AWS, Microsoft Azure, and Google Cloud. Managed service providers capture revenue through cloud monitoring, optimization, migration, security, governance, and support services, typically under recurring subscription or consumption-based pricing models.

Private

Revenue is earned through management of dedicated private cloud infrastructure, including on-premises and hosted environments. Revenue streams include infrastructure management, compliance support, security monitoring, maintenance, and customization services delivered through long-term service agreements and managed contracts.

Segment - End User

Revenue Capture Definition

Large Enterprises

As the largest revenue-generating segment, revenue is captured through enterprise-wide managed cloud contracts covering infrastructure management, security, networking, migration, governance, and application management across multi-cloud and hybrid cloud environments. Long-term managed service agreements and premium support offerings contribute significantly to revenue generation.

Small and Medium Enterprises (SMEs)

Revenue is generated through scalable cloud management solutions designed to provide enterprise-grade cloud capabilities without significant in-house IT investments. Subscription-based managed services, bundled security offerings, and outsourced cloud administration represent the primary revenue sources within this segment.

Segment - Verticals

Revenue Capture Definition

BFSI

Revenue is earned through managed cloud services supporting core banking systems, digital payments, regulatory compliance, cybersecurity, disaster recovery, and data management. Financial institutions typically engage providers through high-value, compliance-intensive service contracts.

Healthcare

Revenue is generated through management of cloud-based electronic health records (EHRs), telehealth platforms, clinical applications, patient data storage, and healthcare cybersecurity solutions. Regulatory compliance and secure data management services form key revenue streams.

Retail & Consumer Goods

Revenue is captured through cloud management services supporting e-commerce platforms, customer analytics, inventory management, omnichannel operations, and digital customer engagement systems. Revenue is often linked to application management, scalability, and cloud optimization services.

Telecom & ITES

Revenue is generated through management of large-scale cloud infrastructure, network operations, customer service platforms, collaboration tools, and digital service delivery environments. Continuous cloud optimization and infrastructure modernization initiatives drive recurring revenue opportunities.

Manufacturing & Automotive

Revenue is earned through cloud services supporting smart manufacturing, industrial IoT platforms, predictive maintenance, supply chain management, and connected vehicle ecosystems. Providers generate revenue through infrastructure management, analytics support, and operational technology (OT) integration services.

Government

Revenue is captured through management of government cloud infrastructure, citizen service platforms, digital transformation initiatives, cybersecurity services, and regulatory compliance programs. Long-term public-sector contracts and sovereign cloud deployments represent major revenue contributors.

Others

This segment includes education, energy & utilities, media & entertainment, transportation, logistics, and other industries. Revenue is derived from managed cloud infrastructure, security, networking, application management, and digital transformation services tailored to sector-specific requirements.

Estimation Model

Layer

Question

Analysis

Cloud Workload Addressable Layer

Who can potentially use cloud-managed services?

Identify the total universe of organizations operating cloud environments, including large enterprises, SMEs, government agencies, financial institutions, healthcare providers, telecom operators, retailers, and manufacturing companies utilizing public, private, or hybrid cloud infrastructure. This establishes the potential customer base requiring ongoing cloud management, monitoring, optimization, and support services.

Serviceable Cloud Infrastructure Layer

Which cloud environments are accessible to managed service providers?

Apply factors such as cloud adoption rates, managed services penetration, multi-cloud and hybrid cloud deployment maturity, regulatory readiness, and availability of third-party managed service ecosystems to determine the serviceable market. This layer excludes organizations that manage cloud operations entirely in-house or have limited cloud adoption.

Managed Services Adoption Layer

Who actively purchases cloud-managed services?

Apply cloud complexity levels, cybersecurity requirements, skills shortages, operational expenditure preferences, digital transformation initiatives, and workload migration trends to convert serviceable organizations into active users of cloud-managed services. This includes services such as cloud monitoring, infrastructure management, security management, migration support, backup and disaster recovery, governance, and performance optimization.

Monetization Layer

How much revenue is generated?

Assess revenue generation by analyzing enterprise spending on cloud infrastructure management, managed security services, cloud operations, FinOps, monitoring and observability, compliance management, backup and disaster recovery, application management, and professional support contracts. Revenue is captured through recurring subscription agreements, managed service contracts, consumption-based pricing models, and outcome-based service engagements.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Enterprise Digital Transformation Adoption Analysis

Conducted a focused assessment of enterprise adoption trends across cloud migration, network modernization, AI integration, cybersecurity, automation, and managed services deployments across key industries.

Help stakeholders identify high-growth technology investment areas, understand evolving customer priorities, and assess future demand drivers.

Industry-Specific Use Case Assessment

Analyzed deployment trends and demand patterns across BFSI, healthcare, manufacturing, government, retail, and telecommunications sectors, highlighting key operational and business use cases.

Supports go-to-market planning by identifying industry-specific growth opportunities and customer investment priorities.

Regional Market Opportunity Assessment

Delivered a detailed regional analysis covering market demand, technology adoption, regulatory environment, infrastructure readiness, and investment activity across key geographic markets.

Enables informed expansion strategies by identifying high-growth regions, emerging demand clusters, and competitive intensity across target markets.

Frequently Asked Questions About This Report

The global cloud managed services market size was estimated at USD 146.5 billion in 2025 and is expected to reach USD 160.8 billion in 2026.

The global cloud managed services market is expected to grow at a compound annual growth rate of 10.7% from 2026 to 2033 to reach USD 326.6 billion by 2033.

By type, the security services segment led with a 27.3% revenue share in 2025, while the mobility services segment is the fastest-growing segment.

Some of the key players in the global cloud managed services market include the International Business Machines Corporation, Cisco Systems, Inc., Telefonaktiebolaget LM Ericsson, Verizon, Accenture, NTT DATA Corporation, Huawei Technologies Co., Ltd., Fujitsu, CHINA HUAXIN, CenturyLink, and Trianz.

Several key factors, including the increasing adoption of cloud computing, the need for cost optimization, and the rising complexity of IT environments, drive the growth of the cloud-managed services market. Organizations across industries are shifting to cloud-based solutions to enhance scalability, flexibility, and operational efficiency while reducing capital expenditures on IT infrastructure.

North America dominated with 41.8% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The public segment led with a 62.4% revenue share in 2025, while private segment is the fastest-growing segment.

The large enterprises segment led with a 65.7% revenue share in 2025, while the SMEs segment is the fastest-growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.