- Home

- »

- Advanced Interior Materials

- »

-

CO2 Separation Membrane Market Size Report, 2026-2033GVR Report cover

![CO2 Separation Membrane Market (2026 - 2033)Report]()

CO2 Separation Membrane Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Polyimide & Cellulose Acetate, Polysulfone), By Membrane (Polymeric Membranes, Inorganic Membranes), By End-use, By Region, And Segment Forecasts

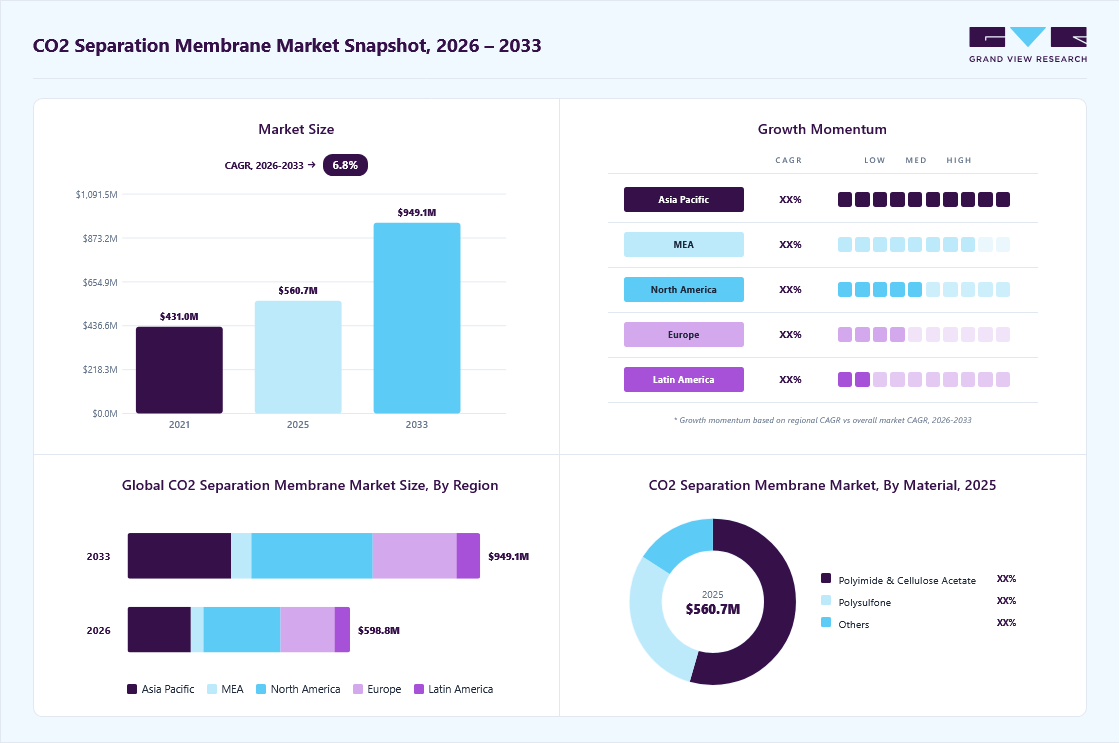

Market Size, 2025

$560.7MMarket Estimate, 2026

$598.8MMarket Forecast, 2033

$949.1MCAGR, 2026–2033

6.8%CO2 Separation Membrane Market Summary

The global CO2 separation membrane market size was valued at USD 560.7 million in 2025 and is projected to grow from USD 598.8 million in 2026 to USD 949.1 million by 2033, at a CAGR of 6.8% from 2026 to 2033. The market in North America dominated with a revenue share of 34.7% in 2025. The demand for CO2 separation membranes is rising significantly as the global push to reduce greenhouse gas emissions and achieve carbon neutrality targets.

Key Market Trends & Insights

- By membrane: Polymeric membranes segment held the largest market share of 67.2% in 2025.

- By material: Polyimide & cellulose acetate segment held the largest market share of 54.4% in 2025.

- By end use: Oil & gas segment held the largest market share of 41.5% in 2025.

Regional Highlights

- Largest regional market: North America (34.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 560.7 Million

- Estimated market size in 2026: USD 598.8 Million

- Projected market size by 2033: USD 949.1 Million

- CAGR (2026-2033): 6.8%

Industries such as power generation, oil & gas, and chemicals are increasingly adopting carbon capture solutions to comply with environmental mandates. Membrane-based separation is gaining preference over conventional methods due to its lower energy consumption and operational efficiency. The growing adoption of carbon capture, utilization, and storage (CCUS) technologies is further boosting demand across industrial sectors. Additionally, increasing investments in clean energy infrastructure and sustainable industrial processes are accelerating market expansion. The need to purify natural gas and remove CO2 impurities is also a key contributor to demand.Key drivers include stringent environmental regulations, rising carbon pricing mechanisms, and industrial decarbonization goals. The oil & gas sector remains a major demand generator due to its reliance on CO2 removal for natural gas processing and enhanced oil recovery. Rapid growth in hydrogen production and biogas upgrading is also driving the adoption of membrane technologies. Technological advancements in polymeric and inorganic membranes are improving efficiency, selectivity, and durability, making them more commercially viable. Additionally, increasing demand for renewable natural gas (RNG) and cleaner fuels is supporting membrane integration in energy systems. Industrial applications such as petrochemicals, cement, and power plants are expanding use cases.

")

The market is witnessing rapid innovation in membrane materials, including mixed-matrix membranes, nano-engineered membranes, and advanced polymeric structures. These innovations enhance permeability, selectivity, and resistance to harsh operating conditions. The integration of nanotechnology is improving gas separation efficiency and reducing fouling issues. There is also a trend toward developing cost-effective manufacturing processes to enable large-scale deployment. Hybrid membranes combining polymeric and inorganic materials are gaining traction for improved performance. Additionally, the increasing use of membranes in emerging applications such as biogas upgrading and hydrogen purification is expanding the market scope.

Market Concentration & Characteristics

The CO2 separation membrane market is moderately consolidated, with a mix of established global players and emerging technology providers. Large companies dominate due to strong R&D capabilities, advanced manufacturing technologies, and established industrial partnerships. However, the market is also witnessing the entry of innovative startups focusing on advanced materials and nanotechnology-based membranes. Strategic collaborations, technology licensing, and capacity expansions are common competitive strategies. The presence of both multinational corporations and niche technology providers creates a competitive yet evolving landscape. Increasing demand for sustainable solutions is attracting new entrants, gradually intensifying competition.

Conventional alternatives to CO2 separation membranes include amine-based absorption, cryogenic separation, and pressure swing adsorption. These conventional methods are widely used but often involve higher energy consumption and operational complexity. While membranes offer advantages such as modularity and lower energy requirements, their adoption can be limited by performance constraints under certain conditions. However, ongoing advancements are narrowing this gap, reducing the threat of substitutes over time. Hybrid systems combining membranes with conventional technologies are also emerging as a solution. Despite competition, membranes are increasingly preferred for their efficiency and environmental benefits.

Material Insights

The polyimide & cellulose acetate segment held the largest revenue share of 54.4% in 2025, due to their widespread commercial adoption and proven performance in CO₂ separation applications. These materials offer a strong balance between permeability, selectivity, and cost-effectiveness, making them ideal for large-scale industrial use. Cellulose acetate membranes are particularly dominant in natural gas sweetening, while polyimide membranes provide higher thermal and chemical stability. Their established manufacturing processes and reliability have made them the preferred choice across the oil & gas and chemical industries. Besides, their compatibility with existing infrastructure supports continued dominance in the market.

The polysulfone segment is expected to grow at a CAGR of 7.7% over the forecast period, owing to its superior mechanical strength, thermal resistance, and durability under harsh operating conditions. These membranes are increasingly being explored for advanced gas separation applications where stability and longevity are critical. Polysulfone also serves as a key base material in the development of composite and asymmetric membranes. Rising demand for high-performance membranes in emerging applications, such as hydrogen purification and industrial carbon capture, is driving its growth. Continuous R&D efforts to enhance its selectivity and permeability are further driving adoption.

Membrane Insights

The polymeric membranes segment held the largest revenue share of 67.2% in 2025, due to their cost efficiency, ease of fabrication, and scalability. These membranes are widely used across industries such as oil & gas, chemicals, and power generation for CO₂ removal and gas purification. Their flexibility in material selection, including polyimide, cellulose acetate, and polysulfone, enables customization to meet application requirements. Established commercial deployment and lower operational costs compared to alternative technologies have strengthened their market position. Furthermore, ongoing improvements in polymer chemistry continue to enhance their performance and expand their application scope.

The hybrid/mixed-matrix membranes segment is expected to grow at a CAGR of 9.0% over the forecast period, driven by their ability to combine the advantages of polymeric and inorganic materials. These membranes offer enhanced selectivity, permeability, and resistance to plasticization compared to conventional polymeric membranes. The incorporation of nanomaterials, such as metal-organic frameworks (MOFs) and zeolites, significantly improves separation efficiency. Increasing demand for high-performance solutions in carbon capture and hydrogen purification is accelerating their adoption. Although still in the commercialization phase, advancements in material science and manufacturing techniques are expected to drive large-scale deployment in the coming years.

End Use Insights

The oil & gas segment held the largest revenue market share of 41.5% in 2025, due to the extensive use of CO₂ separation membranes in natural gas processing and enhanced oil recovery. Removing CO₂ from natural gas streams is essential to meet pipeline and liquefaction specifications, making membranes a critical component in gas treatment facilities. Their low energy consumption, modular design, and operational efficiency make them ideal for remote and offshore applications. Increasing exploration and production activities, particularly in unconventional gas reserves, further support demand. The sector’s continuous need for cost-effective and reliable gas separation solutions ensures its dominant position.

The power generation segment is expected to grow at a CAGR of 7.7% over the forecast period, driven by increasing adoption of carbon capture technologies to reduce emissions from fossil fuel-based plants. CO₂ separation membranes are gaining traction as an energy-efficient alternative to conventional capture methods in power plants. Growing regulatory pressure and carbon reduction targets are pushing utilities to integrate membrane-based systems. In addition, the transition toward cleaner energy and the development of gas-fired and hydrogen-based power plants are creating new opportunities. Advancements in membrane performance and integration with CCUS systems are further accelerating adoption in this segment.

Regional Insights

The North America CO2 separation membranes industry dominated the global market, accounting for the largest revenue share of 34.7% in 2025, due to stringent environmental regulations and advanced industrial infrastructure. The U.S. leads in carbon capture capacity and technological innovation in membrane systems. Strong presence of key market players and government funding for clean energy projects drive growth. The oil & gas sector remains a major end-user, particularly in natural gas processing. Increasing adoption of CCUS technologies further supports market expansion. The region continues to lead in large-scale deployment of membrane-based solutions.

U.S. CO2 Separation Membrane Market Trends

The CO2 separation membranes industry in the U.S. is driven by strong regulatory frameworks and investments in carbon capture technologies. Government incentives and tax credits for CCUS projects are encouraging adoption. The presence of advanced R&D facilities and key companies accelerates innovation. Growing demand for hydrogen and cleaner fuels is boosting membrane applications. Industrial sectors such as power generation and petrochemicals are key contributors. The U.S. remains a hub for technological advancements in this market.

Asia Pacific CO2 Separation Membrane Market Trends

The CO2 separation membranes industry in the Asia Pacific is emerging as a high-growth region due to rapid industrialization, increasing energy demand, and rising environmental concerns. Countries like China and India are investing heavily in carbon capture and clean energy technologies. Expansion of the petrochemical and power generation industries is driving demand for CO2 separation membranes. Government initiatives focusing on emission reduction and sustainable development are supporting adoption. The region’s strong manufacturing base and availability of raw materials further enhance market growth. Increasing investments in hydrogen and biogas projects are also contributing to demand.

The China CO2 separation membranes industry is a key contributor due to its large industrial base and strong focus on reducing carbon emissions. The country is investing heavily in CCUS technologies and renewable energy infrastructure. Growing demand for natural gas purification and hydrogen production is boosting membrane adoption. Government policies supporting carbon neutrality by 2060 are accelerating technological deployment. Domestic manufacturers are also focusing on developing cost-effective membrane solutions. Increasing industrial emissions and regulatory pressure are key drivers in the Chinese market.

Europe CO2 Separation Membrane Market Trends

The CO2 separation membranes industry in Europe is a mature market driven by strict environmental regulations and sustainability goals. The region’s commitment to carbon neutrality is accelerating the adoption of CO2 separation technologies. Investments in renewable energy and the hydrogen economy are key growth drivers. Countries like Germany, France, and the UK are focusing on CCUS deployment. Strong regulatory frameworks and government support enhance market growth. The region is also a leader in innovation and sustainable technologies.

The Germany CO2 separation membranes industry plays a crucial role due to its strong industrial base and focus on energy transition. The country is investing heavily in hydrogen production and carbon capture technologies. Strict emission norms and sustainability targets are driving the adoption of membrane solutions. Industrial sectors such as chemicals and manufacturing are key end-users. Government policies supporting clean energy transition further boost demand. Germany remains a key innovation hub in Europe.

Central & South America CO2 Separation Membrane Market Trends

The CO2 separation membranes industry in Central and South America is witnessing gradual growth driven by increasing industrialization and energy demand. Countries like Brazil are investing in natural gas and biogas upgrading projects. Government initiatives supporting renewable energy are boosting the adoption of membranes. The oil & gas sector remains a key contributor in the region. However, limited infrastructure and investment constraints may slow growth. Despite challenges, the region shows promising potential.

Middle East & Africa CO2 Separation Membrane Market Trends

The CO2 separation membranes industry in the Middle East & Africa region is driven by the strong presence of the oil & gas industry. CO2 separation membranes are widely used in natural gas processing and enhanced oil recovery. Increasing focus on sustainability and emission reduction is supporting market growth. Governments are investing in carbon capture technologies to diversify energy portfolios. The region’s abundant hydrocarbon resources create steady demand. However, adoption is still at a developing stage compared to mature markets.

Key CO2 Separation Membrane Company Insights

Some of the key players operating in the market include Evonik and Membrane Technology and Research, Inc.

-

Evonik is a leading player in the CO2 separation membranes market, known for its high-performance SEPURAN polymer-based membranes used in gas separation and purification. The company focuses on applications such as natural gas processing, biogas upgrading, and hydrogen purification, offering high selectivity and efficiency.

-

Membrane Technology and Research (MTR) is a prominent innovator in advanced gas separation membranes, particularly recognized for its work in mixed-matrix and polymeric membranes for CO2 capture. The company focuses on developing high-efficiency membrane modules for applications such as carbon capture, hydrogen recovery, and natural gas treatment.

GENERON and FUJIFILM are some of the emerging market participants in the CO2 separation membranes market.

-

GENERON specializes in membrane-based gas separation systems, particularly for CO2 removal from natural gas and industrial streams. The company offers customized membrane solutions with high CO2/CH₄ selectivity, enabling efficient gas sweetening, biogas upgrading, and enhanced oil recovery applications.

-

FUJIFILM is an emerging player in the gas separation membranes market through its advanced material science capabilities and membrane technologies. The company develops high-performance membranes for industrial gas separation, leveraging its expertise in chemical processing and film technologies.

Key CO2 Separation Membrane Companies:

The following key companies have been profiled for this study on the CO2 separation membrane market.

- Evonik

- Membrane Technology and Research, Inc.

- UBE Corporation

- Honeywell International Inc.

- Toray Industries, Inc.

- BORSIG GmbH

- FUJIFILM

- GENERON

- Air Liquide

- Air Products and Chemicals, Inc.

Recent Developments

-

In September 2024, Evonik launched its SEPURAN Green G5X 11 membrane, designed for high-efficiency biogas upgrading and CO2 removal. This product focuses on improving sustainability and enabling the production of renewable natural gas (RNG), thereby strengthening Evonik’s position in carbon capture and gas separation applications.

-

In December 2024, Toray announced the development of a pilot production line for all-carbon CO2 separation membranes at its Shiga plant. The facility aims to enable large-scale manufacturing and commercialization of next-generation high-performance membranes.

CO2 Separation Membrane Market Report Scope

Report Attribute

Details

Market size in 2025

USD 560.7 million

Estimated market size in 2026

USD 598.8 million

Projected market size by 2033

USD 949.1 million

Growth rate

CAGR of 6.8% from 2026 to 2033

Base year for estimation

2025

Actual estimates/Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, membrane, end use, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; Japan; India

Key companies profiled

Evonik; Membrane Technology and Research, Inc.; UBE Corporation; Honeywell International Inc.; Toray Industries, Inc.; BORSIG GmbH; FUJIFILM; GENERON; Air Liquide; Air Products and Chemicals, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global CO2 Separation Membrane Market Report Segmentation

This report forecasts revenue growth at regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global CO2 separation membrane market report on the basis of material, membrane, end use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Polyimide & Cellulose Acetate

-

Polysulfone

-

Others

-

-

Membrane Outlook (Revenue, USD Million, 2021 - 2033)

-

Polymeric Membranes

-

Inorganic Membranes

-

Hybrid / Mixed-Matrix Membranes

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Oil & Gas

-

Power Generation

-

Industrial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

-

Central & South America

-

Middle East & Africa

-

Frequently Asked Questions About This Report

North America dominated with a 34.7% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The polyimide & cellulose acetate segment led with a 54.4% revenue share in 2025.

The oil & gas segment dominated the market and accounted for the largest revenue share of 41.5% in 2025.

The global CO2 separation membrane market size was valued at USD 560.7 million in 2025 and is estimated at USD 598.8 million for 2026.

The polymeric membranes segment accounted for the highest revenue share of 67.2% in 2025, driven by their cost efficiency, ease of fabrication, and scalability.

Key players include Evonik; Membrane Technology and Research, Inc.; UBE Corporation; Honeywell International Inc.; Toray Industries, Inc.; BORSIG GmbH; FUJIFILM; GENERON; Air Liquide; Air Products and Chemicals, Inc.

Stringent carbon emission regulations and the rising adoption of carbon capture, utilization, and storage (CCUS) technologies are the key factors driving the CO₂ separation membranes market.

The global CO2 separation membranes market is expected to grow at a CAGR of 6.8% from 2026 to 2033, reaching USD 949.1 million by 2033.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.