- Home

- »

- Next Generation Technologies

- »

-

Container Transshipment Market Size Report, 2025-2030GVR Report cover

![Container Transshipment Market (2025 - 2030)Report]()

Container Transshipment Market (2025 - 2030)

Size, Share & Trends Analysis Report By Container Type (Standard Containers, High Cube Containers), By Container Size (40 Feet), By Service Type, By Mode of Transport, By End User Industry, By Region, And Segment Forecasts

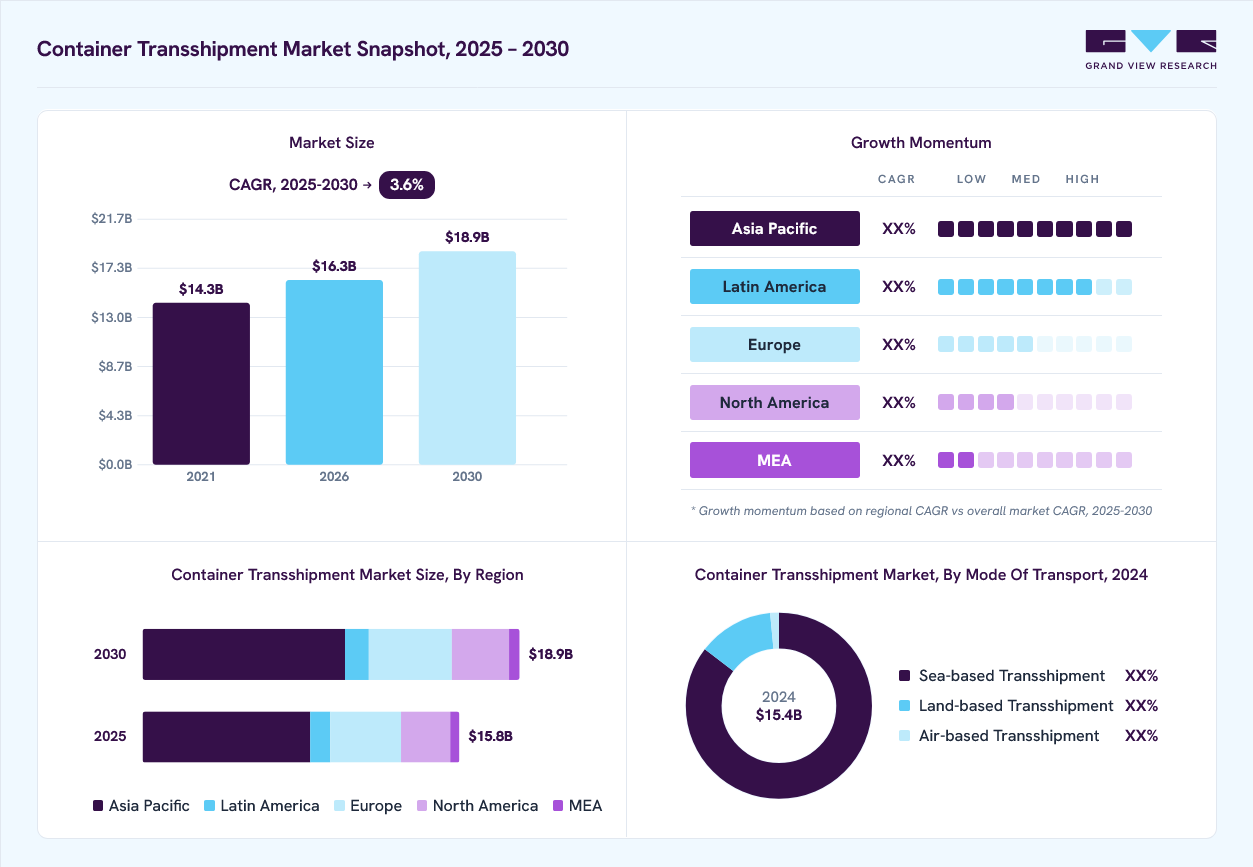

Market Size, 2024

$15.4BMarket Estimate, 2026

$16.3BMarket Forecast, 2030

$18.9BCAGR, 2025–2030

3.6%Container Transshipment Market Summary

The global container transshipment market size was valued at USD 15.4 billion in 2024 and is projected to grow from USD 16.3 billion in 2026 to USD 18.9 billion by 2030, at a CAGR of 3.6% from 2025 to 2030. Asia-Pacific dominated the market, accounting for a revenue share of 52.8% in 2024. The rise of post-Panamax and ultra-large container vessels has necessitated substantial investments in port infrastructure.

Key Market Trends & Insights

- The U.S. container transshipment market held a dominant position in 2024.

- By container type, the standard containers segment accounted for the largest revenue share of 58.4% in 2024.

- By container size, the 40-foot (FEU) segment held the largest revenue share in 2024.

- By service type, the container handling services segment dominated the market in 2024.

Market Size & Forecast

- 2024 Market Size: USD 15.4 Billion

- 2030 Projected Market Size: USD 18.9 Billion

- CAGR (2025-2030): 3.6%

- Asia Pacific: Largest market in 2024

Larger ships, which offer economies of scale, require deeper drafts and advanced crane systems to handle increased cargo volumes efficiently. For instance, ports in Asia and North America are expanding berths and upgrading equipment to remain competitive. The U.S. Bureau of Transportation Statistics highlights that cost savings from larger vessels can be offset by transshipment expenses if ports cannot service them. This has led to concentrated investments in hubs like Singapore and Rotterdam, which now feature automated terminals capable of processing over 20,000 TEUs (twenty-foot equivalent units) per vessel call. Such infrastructure improvements are critical to maintaining seamless transshipment flows amid growing global trade volumes, which boost the market growth.")

Digital transformation is revolutionizing the container transshipment market through real-time tracking and data harmonization. The Federal Maritime Commission (FMC) emphasizes the need for standardized application programming interfaces (APIs) to provide stakeholders with real-time updates on container locations, estimated arrival times, and delays. For example, the proposed Maritime Transportation Data System (MTDS) aims to integrate vessel positioning data with terminal operations, enabling carriers to reroute shipments dynamically during disruptions. This level of visibility reduces idle time at ports and enhances coordination between ocean carriers and landside logistics providers. The FMC notes that harmonized data practices could reduce average shipment delays by 15-20%, directly lowering costs for U.S. importers and exporters.

Global transshipment hubs are facing intensified regulatory scrutiny to prevent illicit activities such as smuggling and trafficking. The U.S. Department of State’s Global Transshipment Seminar underscored the risks posed by unmonitored cargo transfers, particularly in high-seas zones. In response, governments are implementing stricter documentation requirements and deploying technologies like blockchain for secure record-keeping. For instance, the UAE’s Jebel Ali Port now mandates advanced cargo declarations for all transshipped containers, a measure aligned with the Proliferation Security Initiative (PSI). These regulations aim to balance trade fluidity with security, ensuring that transshipment hubs do not become nodes for unauthorized cargo diversion.

Ports worldwide are competing to become preferred transshipment hubs by enhancing connectivity and service quality, which has propelled market growth. The Canadian and U.S. rivalry over Arctic shipping routes exemplifies this trend, as thawing ice caps open new pathways for Asia-Europe trade. Similarly, Asian ports like Hong Kong and Busan are investing in hinterland rail networks to attract cargo from inland manufacturing zones. The Ontario Commercial Vehicle Survey revealed that 60% of transshipment decisions are influenced by a hub’s proximity to major highways and intermodal terminals. This geographic advantage allows hubs to serve as consolidation points, reducing overall logistics costs for shippers. Ports failing to improve their connectivity risk losing market share to rivals with superior infrastructure.

Environmental sustainability is increasingly prioritized through operational optimizations rather than standalone initiatives. The FMC’s 2022 Annual Report highlights how route optimization and reduced anchorage times-enabled by digital tools-lower fuel consumption and emissions. For example, the Port of Los Angeles reduced diesel particulate matter by 85% over a decade by streamlining truck turnaround times and promoting shore power for docked vessels. While direct regulatory mandates for emissions are still emerging, the integration of efficiency measures into transshipment workflows demonstrates a proactive approach to sustainability. These practices not only align with global climate goals but also enhance cost competitiveness for logistics providers.

Container Type Insights

The standard containers segment accounted for the largest revenue share of 58.4% in 2024. Standard containers remain the backbone of global shipping and transshipment due to their universal standardization and widespread infrastructure compatibility. Ports, vessels, and intermodal transport systems are primarily designed to handle these containers efficiently. Their versatility allows for a broad range of cargo, from manufactured goods to raw materials. Although newer container types emerge, the entrenched global supply chain investments in standard containers keep their demand stable. Additionally, ongoing initiatives to improve container tracking and handling efficiency continue to strengthen their role in the market.

The high cube containers segment is projected to grow at the fastest CAGR over the forecast period. High Cube containers, with an extra foot of height compared to standard containers, are gaining momentum as shippers look to maximize cargo volume without increasing shipping costs significantly. This container type is especially beneficial for lightweight but bulky goods such as apparel, furniture, and many e-commerce items, where volume rather than weight is the constraint. The rise in e-commerce and the need for greater supply chain efficiency push ports and carriers to accommodate high-cube containers more frequently. Their adoption also correlates with growing demand in industries seeking to reduce the total number of shipments by optimizing container space.

Container Size Insights

The 40-foot (FEU) segment held the largest revenue share in 2024. The 40-foot container leads the market due to its efficiency in cargo volume and handling. It offers the best cost-to-capacity ratio, making it ideal for large international shipments. Mega container vessels (ULCVs) and transshipment hubs are designed to optimize the loading and unloading of FEUs, supporting economies of scale that reduce shipping costs per container. Furthermore, many supply chains have standardized their logistics around FEUs to streamline operations and inventory management. Investments in infrastructure such as cranes, yard space, and stacking equipment are often tailored for 40-foot containers, reinforcing their dominant position.

The 20-foot (TEU) segment is expected to grow at a significant CAGR during the forecast period. While smaller in size, the 20-foot container remains critical for transporting heavy, dense cargo like machinery, metals, and chemicals that require less volume but more weight capacity. They also play a strategic role in feeder services that connect smaller ports or inland facilities to major transshipment hubs. The TEU size offers flexibility in regions where port infrastructure or transport conditions limit the handling of larger containers. Despite the dominance of FEUs, TEUs’ importance persists in specialized sectors and geographic markets, contributing to a balanced container size portfolio within the transshipment industry.

Service Type Insights

The container handling services segment dominated the market in 2024. As the foundational pillar of transshipment operations, container handling services encompass activities like loading, unloading, stacking, and moving containers within port facilities. Technological advancements, including automation, AI-driven container cranes, and remote-controlled vehicles, are significantly improving handling speed and accuracy, reducing turnaround time, and minimizing human error. These innovations are especially critical in mega-ports facing congestion challenges. The drive towards smart ports integrating IoT and real-time data analytics further enhances operational efficiency and responsiveness in container handling.

The logistics & forwarding services segment is projected to grow at the fastest CAGR over the forecast period. This segment is evolving beyond traditional freight forwarding to become a comprehensive logistics management solution. Increasingly, clients demand seamless, end-to-end visibility, efficient route planning, and flexible delivery options. Digital platforms offering real-time tracking, predictive analytics, and multi-modal transport coordination are becoming standard. The surge in e-commerce and globalized supply chains intensifies the need for agile logistics providers who can integrate sea, land, and air transport modes efficiently. This service type's growth reflects the broader trend of supply chain digitization and the move toward customer-centric, data-driven logistics.

Mode of Transport Insights

The sea-based transshipment segment dominated the market in 2024. Sea-based transshipment continues to dominate global trade due to the cost-effectiveness of maritime transport for large volumes and long distances. The rise of ultra-large container vessels (ULCVs), capable of carrying upwards of 20,000 TEUs, reinforces the central role of sea transport. Ports worldwide are investing in deeper berths, longer quays, and advanced handling equipment to accommodate these massive vessels efficiently. Furthermore, shipping alliances optimize vessel routes to leverage transshipment hubs, which act as critical nodes connecting regional and global trade flows.

The land-based transshipment segment is projected to grow at a significant CAGR over the forecast period. Growing investments in inland dry ports, rail corridors, and intermodal hubs, particularly in Asia and Europe, are driving the expansion of land-based transshipment. This mode helps alleviate congestion at major seaports, shorten delivery times to inland markets, and improve the overall resilience of supply chains. Governments are supporting this trend through infrastructure development and trade facilitation policies. Additionally, land-based transshipment is critical for last-mile connectivity, linking ports with final destinations through multimodal logistics solutions.

End User Industry Insights

The retail and e-commerce segment dominated the market in 2024 and is projected to grow at the fastest CAGR over the forecast period. The retail and e-commerce sectors are the most dynamic drivers of container transshipment growth. The exponential growth in online shopping worldwide demands faster, more flexible logistics solutions, pushing ports and logistics providers to adapt their operations. Transshipment hubs are increasingly designed to support omnichannel distribution strategies, with a focus on reducing transit times and offering value-added services like packaging and returns management. The global reach of e-commerce also necessitates efficient cross-border transshipment networks capable of handling diverse product categories with varying delivery urgency.

The consumer electronics segment is projected to grow at a significant CAGR over the forecast period. The consumer electronics industry relies heavily on efficient transshipment due to the high value, rapid innovation cycles, and time sensitivity of its products. Delays in shipping can lead to significant losses, making real-time tracking, secure handling, and quick processing essential. The growth in electronics manufacturing in Asia, coupled with demand in North America and Europe, generates complex supply chains that depend on optimized transshipment hubs. Temperature-controlled logistics and special handling for sensitive components further drive investment in specialized transshipment infrastructure and services.

Regional Insights

The North America container transshipment market accounted for a 15.6% share of the overall market in 2024. The container transshipment market in North America is characterized by steady growth, primarily driven by increasing trade activities and focused investments in modernizing port infrastructure. Key ports in the region are adopting advanced automation and digital tracking technologies to improve operational efficiency and reduce congestion. Canadian ports, in particular, are playing a significant role in facilitating trade flows between North America and Asia-Pacific markets, while also prioritizing sustainability initiatives to lower environmental impact.

U.S. Container Transshipment Market Trends

The U.S. container transshipment market held a dominant position in 2024. In the U.S., the container transshipment market continues to expand, supported by significant governmental funding aimed at upgrading port facilities and embracing cutting-edge automation technologies. Prominent ports on the West Coast are enhancing container handling processes through the integration of smart systems to accelerate throughput and minimize delays. This technological evolution helps maintain competitiveness on a global scale and addresses rising demands from increasing international trade volumes.

Europe Container Transshipment Market Trends

The Europe container transshipment market was identified as a lucrative region in 2024. Europe’s container transshipment sector benefits from well-developed port infrastructure and strong hinterland connectivity. Major hubs like Rotterdam and Antwerp remain crucial to global shipping networks, supported by robust cold chain logistics to serve perishable goods markets. European ports are increasingly adopting environmentally friendly operations and shore power technologies to meet stringent EU regulations. Furthermore, digital transformation initiatives across ports enhance transparency and operational efficiency, positioning the region as a key player in sustainable maritime logistics.

Germany container transshipment market is anchored by its major ports, notably Hamburg, which continues to be a vital gateway for European trade. The market is experiencing advancements through the deployment of automated cranes and digital terminal management systems that optimize container handling. German ports are also aligning closely with EU climate goals by incorporating sustainable practices, making them resilient and efficient even amid global shipping challenges.

The UK container transshipment market has faced some challenges due to geopolitical factors such as Brexit and disruptions in global shipping routes. These have led to increased operational costs and complexities for exporters and importers. Nevertheless, UK ports continue to maintain their importance in global trade networks. The government is supporting infrastructure upgrades and initiatives to enhance port resilience, ensuring that the sector can adapt to evolving trade environments.

Asia Pacific Container Transshipment Market Trends

The Asia-Pacific container transshipment market is experiencing rapid growth, driven by booming intra-regional trade and rapid growth in e-commerce. Leading ports across China, Singapore, Japan, and India are investing heavily in expanding capacity and adopting automation to keep pace with demand. The region is also focusing on sustainable port operations and smart supply chain management solutions, making it a dynamic hub for international maritime logistics.

China container transshipment market remains at the forefront with some of the world’s busiest ports. The country’s ports continue to enhance their capacity and efficiency by investing in automation and digital infrastructure. Strategic development of port clusters and deep-water facilities has positioned China as a global leader in container throughput. These advancements support China’s ambitions to maintain its dominance in maritime trade networks.

India container transshipment market is evolving rapidly, with a clear focus on expanding domestic port capacity to reduce reliance on foreign transshipment hubs. The government’s initiatives aim to modernize ports and improve connectivity, addressing congestion issues at existing facilities. New port developments are strategically planned to support the country’s growing trade volumes and strengthen its position in regional maritime logistics.

Key Container Transshipment Company Insights

Some major players in the container transshipment market include MSC Mediterranean Shipping, A.P. Moller - Maersk, CMA CGM Group, PSA Singapore, among others. These companies have strategically positioned terminals across key transshipment hubs, allowing them to manage large volumes of cargo efficiently and offer seamless connectivity across international trade routes. Their strong integration of shipping and logistics services, coupled with technological innovation in real-time tracking and smart terminal operations, further enhances operational efficiency and customer reliability. Additionally, their ability to form strategic alliances and adapt to evolving regulatory and environmental standards has cemented their influence in shaping the global container transshipment landscape.

-

DP World has established itself as a leading force in the container transshipment market through its expansive network of marine terminals strategically located across multiple continents. The company is known for its significant investment in smart port technologies, automation, and digital supply chain solutions, which enhance operational efficiency and throughput capacity. DP World's integrated logistics capabilities, including inland transportation and trade facilitation services, allow for streamlined cargo movement and improved connectivity between origin and destination markets. Its proactive approach to sustainable port operations and commitment to innovation ensure resilience and adaptability in a rapidly evolving maritime industry.

-

MSC Mediterranean Shipping has emerged as one of the most influential players in the container transshipment market by leveraging its massive fleet size and comprehensive global coverage. The company operates through major transshipment hubs, optimizing cargo flow across international trade lanes with high-frequency services and reliable schedules. MSC’s vertical integration strategy, which includes terminal operations and inland logistics, provides end-to-end visibility and efficiency across the supply chain. Its continuous investment in digital solutions and eco-efficient vessels underscores its leadership in delivering high-capacity, cost-effective, and environmentally conscious shipping and transshipment services.

Key Container Transshipment Companies:

The following are the leading companies in the container transshipment market. These companies collectively hold the largest market share and dictate industry trends.

- MSC Mediterranean Shipping

- A.P. Moller - Maersk

- CMA CGM Group

- PSA Singapore

- DP World

- COSCO Shipping

- APM Terminals

- EUROGATE

- Hamburger Hafen und Logistik

- Hutchison Ajman International Terminals Limited - F.Z.E.

Recent Developments

-

In December 2024, DP World Cochin introduced new ship-to-shore (STS) cranes and electric Rubber-Tyred Gantry (e-RTGs) cranes at its International Container Transshipment Terminal (ICTT) in Cochin, India. These advancements boosted the terminal’s capacity to approximately 1.4 million TEUs per year, positioning it as one of the largest terminals in South and East India. The electrified equipment, supported by an upgraded power infrastructure from 3 MVA to 5 MVA, ensures reliable operations during peak demand and reduces the carbon footprint, aligning with sustainability goals. The terminal handled 840,564 TEUs in 2024, a 17% increase from the previous year, and managed its largest-ever single vessel exchange of 6,157 TEUs with the MSC Aurora.

-

In November 2024, MSC Mediterranean Shipping acquired a 51% stake in MVN Logistics, a Milan-based provider of multi-modal freight forwarding, warehousing, and distribution services, expecting to close 2024 with a turnover of 100 million euros. This strategic acquisition enhances MSC’s logistics capabilities by integrating MVN’s established network, strengthening its position in the global container transshipment market. The move supports MSC’s broader strategy to expand its land-based logistics portfolio, improving end-to-end supply chain solutions for transshipment operations.

Container Transshipment Market Report Scope

Report Attribute

Details

Market size in 2024

USD 15.4 billion

Estimated market size in 2026

USD 16.3 billion

Projected market size by 2030

USD 18.9 billion

Growth rate

CAGR of 3.6% from 2025 to 2030

Base year for estimation

2024

Historical data

2018 - 2023

Forecast period

2025 - 2030

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2030

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Container type, container size, service type, mode of transport, end user industry, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

MSC Mediterranean Shipping; A.P. Moller - Maersk; CMA CGM Group; PSA Singapore; DP World; COSCO Shipping; APM Terminals; EUROGATE; Hamburger Hafen und Logistik; Hutchison Ajman International Terminals Limited - F.Z.E.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Container Transshipment Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global container transshipment market report based on container type, container size, service type, mode of transport, end use industry, and region:

-

Container Type Outlook (Revenue, USD Billion, 2018 - 2030)

-

Standard Containers

-

High Cube Containers

-

Refrigerated Containers

-

Open Top Containers

-

Flat Rack Containers

-

-

Container Size Outlook (Revenue, USD Billion, 2018 - 2030)

-

40-foot (FEU)

-

20-foot (TEU)

-

Others

-

-

Service Type Outlook (Revenue, USD Billion, 2018 - 2030)

-

Container Handling Services

-

Logistics & Forwarding Services

-

Warehousing & Storage

-

Customs Clearance & Documentation

-

-

Mode of Transport Outlook (Revenue, USD Billion, 2018 - 2030)

-

Sea-based Transshipment

-

Land-based Transshipment

-

Air-based Transshipment

-

-

End User Industry Outlook (Revenue, USD Billion, 2018 - 2030)

-

Retail and E-commerce

-

Automotive

-

Consumer Electronics

-

Agriculture and Food

-

Pharmaceuticals

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global container transshipment market size was valued at USD 15.4 billion in 2024 and is estimated at USD 16.3 billion for 2026.

The global container transshipment market is expected to grow at a CAGR of 3.6% from 2025 to 2030, reaching USD 18.9 billion by 2030.

Asia-Pacific (APAC) held the largest market share of 52.8% in 2024. This is due to the booming intra-regional trade and rapid growth in e-commerce. Leading ports across China, Singapore, Japan, and India are investing heavily in expanding capacity and adopting automation to keep pace with demand.

Some of the players in the container transshipment market are MSC Mediterranean Shipping, A.P. Moller - Maersk, CMA CGM Group, PSA Singapore, DP World, COSCO Shipping, APM Terminals, EUROGATE, Hamburger Hafen und Logistik, and Hutchison Ajman International Terminals Limited - F.Z.E.

The key driving trend in the container transshipment market is the increasing investment in port automation and digitalization, aimed at enhancing operational efficiency, reducing turnaround times, and accommodating growing global trade volumes.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.