- Home

- »

- IT Services & Applications

- »

-

Data Security Posture Management Market Report, 2026-2033GVR Report cover

![Data Security Posture Management (DSPM) Market (2026 - 2033)Report]()

Data Security Posture Management (DSPM) Market (2026 - 2033)

Size, Share, & Trend Analysis Report By Component (Solutions, Services), By Deployment Mode, By Organization Size, By Data Type, By Application, By End User, By Region, And Segment Forecasts

Market Size, 2025

$2.2BMarket Estimate, 2026

$2.5BMarket Forecast, 2033

$6.2BCAGR, 2026–2033

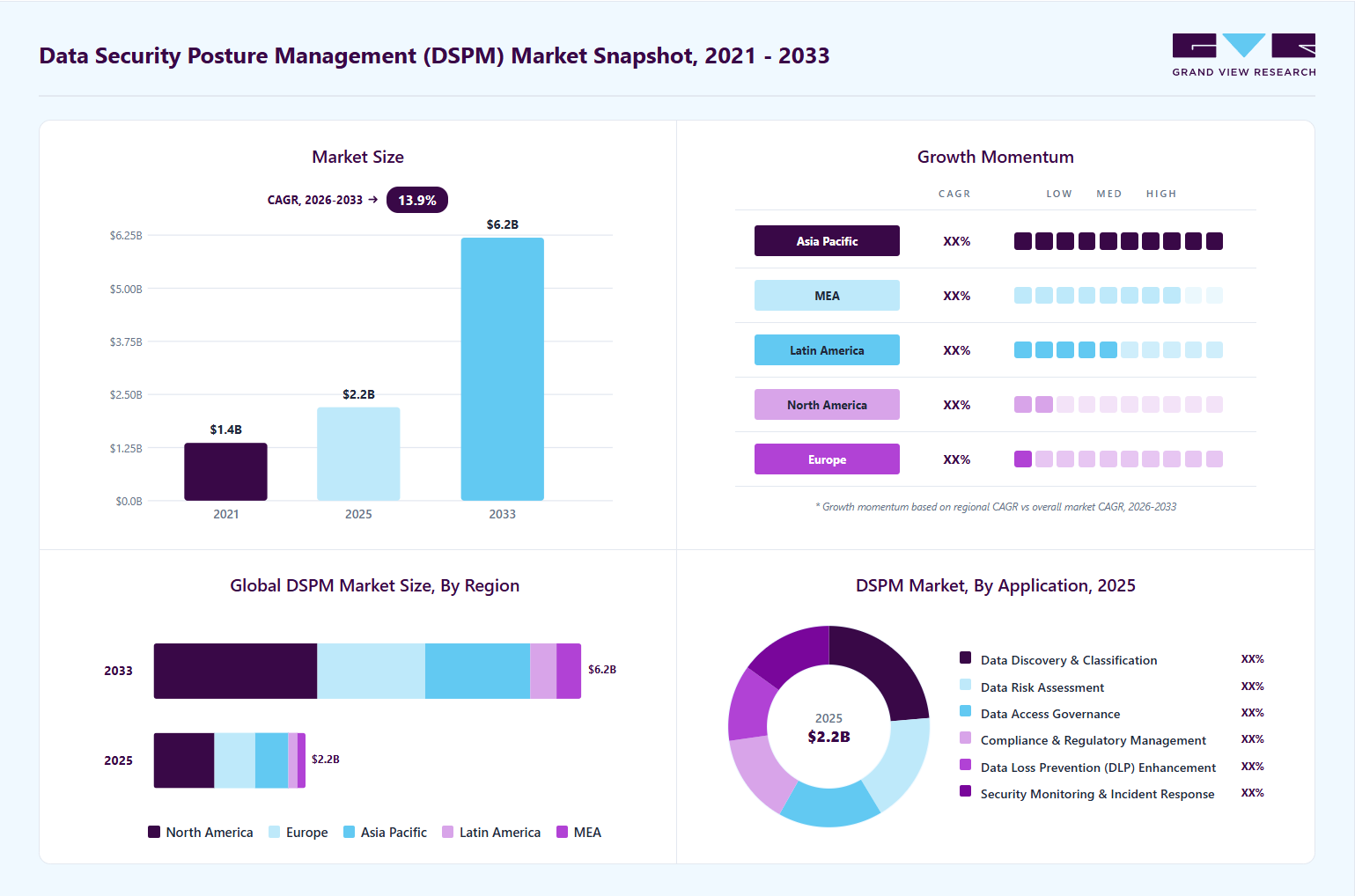

13.9%Data Security Posture Management Market Summary

The global data security posture management market size was valued at USD 2.2 billion in 2025 and is projected to grow from USD 2.5 billion in 2026 to USD 6.2 billion by 2033, at a CAGR of 13.9% from 2026 to 2033. The market in North America dominated with a revenue share of 39.8% in 2025. The market is emerging as a critical segment within the broader cybersecurity landscape, driven by the rapid expansion of cloud computing, increasing data sprawl, and rising concerns around data breaches.

Key Market Trends & Insights

- By component: Solutions segment held the largest market share of 81.3% in 2025.

- By deployment mode: Cloud-based segment held the largest market share in 2025.

- By organization size: Large enterprises segment held the largest market share in 2025.

- By data type: Unstructured data segment held the largest market share in 2025.

- By application: Data discovery & classification segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (39.8% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 2.2 Billion

- Estimated market size in 2026: USD 2.5 Billion

- Projected market size by 2033: USD 6.2 Billion

- CAGR (2026-2033): 13.9%

DSPM solutions focus on continuously discovering, classifying, and securing sensitive data across cloud, on-premises, and hybrid environments.Another major driver is the sharp rise in data breaches and misconfiguration-related security incidents. A significant proportion of breaches today occur not due to perimeter failures but due to excessive permissions, unsecured data stores, or unknown data exposure in cloud environments. DSPM tools offer organizations proactively identify such risks by continuously scanning and classifying sensitive data, thereby reducing the attack surface. This shift from reactive security to proactive data-centric protection is becoming a critical enterprise priority.

")

Regulatory compliance requirements are also playing a major role in accelerating market growth. Regulations such as GDPR, HIPAA, and other regional data protection laws are forcing organizations to maintain strict control over sensitive information. DSPM solutions simplify compliance by providing automated data discovery, classification, and reporting capabilities, enabling organizations to demonstrate governance and reduce audit complexities. As regulatory scrutiny continues to increase globally, demand for DSPM is expected to strengthen further.

In addition, the growing adoption of zero-trust security frameworks is reinforcing the importance of DSPM in modern cybersecurity architectures. Since zero trust assumes that no user or system should be inherently trusted, organizations require deep visibility into data access patterns and permissions. DSPM complements this approach by ensuring that only authorized users can access sensitive data and that any anomalous behavior is quickly detected. Combined with increasing awareness of data-centric security strategies, these trends are positioning DSPM as a foundational layer in enterprise cybersecurity transformation.

Market Dynamics

The rapid expansion of cloud computing, hybrid IT environments, and digital transformation initiatives is increasing organizational exposure to data security risks, thereby driving the demand for Data Security Posture Management (DSPM) solutions. Enterprises are generating and storing large volumes of sensitive data across multiple platforms, making it difficult to maintain visibility, enforce consistent security policies, and identify misconfigurations or unauthorized access. This growing complexity is pushing organizations to adopt DSPM tools to continuously monitor data assets, assess security posture, and reduce the risk of data breaches.

For instance, according to IBM’s 2024 Cost of a Data Breach Report, the global average cost of a data breach reached USD 4.88 million, the highest recorded to date, driven largely by breaches involving cloud environments and compromised sensitive data. The report also highlighted that organizations with high levels of security automation and visibility experienced significantly lower breach costs, reinforcing the importance of proactive data security posture monitoring. Therefore, the increasing need for unified data visibility, regulatory compliance, risk reduction, and continuous security assessment across complex IT ecosystems is strongly contributing to the growth of the data security posture management market.

Alert fatigue and potential misclassification of security events are significant restraints for the growth of the Data Security Posture Management (DSPM) market. DSPM solutions continuously monitor cloud and on-premises environments to identify sensitive data exposure, misconfigurations, and access risks; however, they often generate a high volume of alerts, many of which can be false positives or low-priority notifications. This overwhelming stream of alerts can desensitize security teams, reduce operational efficiency, and increase the likelihood of critical risks being overlooked or misclassified, thereby weakening the overall effectiveness of DSPM tools.

For instance, cybersecurity research highlights that excessive alert generation and poorly tuned detection systems contribute to alert fatigue, where security teams become overwhelmed by continuous notifications and may ignore or deprioritize important warnings, increasing the risk of missed threats and delayed response times. As a result, concerns around alert fatigue, misclassification of risks, and reduced trust in automated DSPM outputs can slow down adoption, particularly among enterprises that require highly accurate, low-noise security intelligence.

Market Concentration & Characteristics

The Data Security Posture Management (DSPM) market is moderately concentrated, with a small group of leading cybersecurity and data security vendors accounting for a significant share of enterprise deployments. Established players such as Microsoft, Wiz, Varonis, BigID, Cyera, and Palo Alto Networks dominate the market due to their strong capabilities in cloud data discovery, sensitive data classification, and AI-driven risk visibility across complex multi-cloud environments. At the same time, the market remains highly competitive and fast-evolving, as emerging DSPM-native vendors continue to innovate in automated data discovery, contextual risk prioritization, and real-time exposure management.

The market is strongly innovation-driven, with increasing emphasis on AI and machine learning-powered data classification and continuous monitoring of sensitive data across structured and unstructured sources. Mergers and acquisitions are also shaping the competitive landscape, as larger cybersecurity and cloud security platforms acquire niche DSPM startups to enhance their data security capabilities and strengthen integrated security suites such as CNAPP and data governance platforms. Regulatory compliance requirements, including GDPR, HIPAA, and other data protection mandates, further reinforce demand, particularly in highly regulated industries such as BFSI, healthcare, and IT & telecom. The market is further characterized by high enterprise concentration, with adoption primarily driven by large organizations managing large-scale, distributed, and sensitive data environments where data visibility and risk reduction are mission-critical priorities.

Component Insights

The solutions segment dominated the data security posture management market, accounting for 81.3% of revenue share in 2025, primarily driven by the rising need for comprehensive, automated platforms that can continuously discover, classify, and secure sensitive data across complex and distributed IT environments. Organizations are increasingly prioritizing DSPM solutions as they shift toward cloud-first and hybrid architectures, where data visibility gaps and misconfigurations pose significant security risks. This growing reliance on integrated solutions over standalone tools is further fueled by the need to manage escalating data volumes, strengthen real-time risk detection, and reduce manual intervention in security operations. Moreover, demand for DSPM solutions is reinforced by the increasing frequency of data breaches and the growing importance of proactive, data-centric security strategies that go beyond traditional perimeter-based defenses.

For instance, in March 2026, Lifebit launched a Security Posture Management capability for Trusted Research Environments, enhancing governance and continuous monitoring of sensitive research data, highlighting how solution-based approaches are being embedded into specialized ecosystems to strengthen data protection and compliance. Overall, the dominance of the solutions segment reflects the market’s clear shift toward unified, scalable, and intelligence-driven platforms that enable organizations to secure data effectively in increasingly complex digital environments.

The services segment is anticipated to grow at a significant CAGR during the forecast period, driven by the increasing complexity of data environments and the rising need for expert-led implementation, optimization, and continuous management of Data Security Posture Management (DSPM) solutions. As organizations adopt DSPM platforms, many require specialized services to effectively integrate these tools with existing cloud infrastructures, configure data classification policies, and ensure alignment with internal security frameworks and regulatory requirements. In addition, the shortage of in-house cybersecurity expertise is further pushing enterprises to rely on managed and professional services for ongoing monitoring, risk assessment, and compliance support. This demand is also strengthened by the growing frequency of data breaches and the need for continuous tuning of security controls to address evolving threats. As a result, service providers are becoming critical enablers in helping organizations maximize the value of DSPM deployments while ensuring sustained data protection and governance effectiveness.

Deployment Mode Insights

The cloud-based segment dominated the data security posture management industry, capturing the largest revenue share in 2025, driven by the rapid adoption of cloud-first strategies and the need for scalable, real-time visibility across increasingly complex multi-cloud environments. As organizations continue migrating sensitive workloads to public and hybrid clouds, cloud-based DSPM solutions are preferred for their ability to continuously discover, classify, and secure data while enabling centralized governance and faster risk detection. The rising incidence of cloud misconfigurations, data exposure risks, and growing reliance on SaaS applications further strengthens demand for cloud-native security approaches. Additionally, the shift toward Zero Trust architectures is accelerating adoption, as cloud-based DSPM tools support continuous monitoring and dynamic access control across distributed systems. For instance, in March 2025, Cloudflare introduced Security Posture Management capabilities to provide unified visibility and risk management across data, applications, and cloud environments, reflecting the industry’s move toward integrated cloud security platforms. Overall, the segment’s dominance highlights the transition toward agile, automated, and cloud-centric data protection strategies.

The on-premises segment is expected to grow at a significant CAGR during the forecast period, driven by continued demand for stronger data control, security sovereignty, and strict regulatory compliance in highly regulated industries. Despite increasing cloud adoption, many organizations still prefer on-premises deployments to maintain full ownership of sensitive data, minimize external exposure risks, and comply with data residency and governance requirements. This growth is further supported by enterprises operating legacy IT environments and hybrid infrastructures, where gradual modernization necessitates continued reliance on on-premises security systems. In addition, rising concerns around data privacy, AI-driven data exposure risks, and complex cross-environment data flows are reinforcing the need for secure on-premises controls within broader DSPM strategies. For instance, in February 2026, Cyberhaven launched its Unified AI & Data Security Platform with DSPM capabilities to secure sensitive data across endpoints, SaaS, cloud, and on-premises environments, highlighting the continued importance of on-premises security within modern hybrid architectures. Consequently, the segment’s growth reflects the sustained relevance of on-premises deployments within balanced, enterprise-wide data security strategies.

Organization Size Insights

The large enterprises segment dominated the data security posture management market, accounting for the largest revenue share in 2025, primarily due to their extensive and complex data environments that span across multi-cloud, SaaS, and on-premises infrastructures. These organizations handle vast volumes of sensitive data, making continuous monitoring, classification, and risk management essential to mitigate exposure to breaches, misconfigurations, and unauthorized access. In addition, large enterprises typically operate under strict regulatory requirements and have higher cybersecurity budgets, enabling faster adoption of advanced DSPM solutions to strengthen data governance and compliance across global operations. The increasing use of AI, analytics, and digital transformation initiatives further expands their data footprint, intensifying the need for robust, centralized security posture management. For instance, in March 2026, Cohesity expanded its data security portfolio with Cyera’s DSPM capabilities to enhance cyber resilience by delivering deeper data visibility and protection across hybrid enterprise environments. Subsequently, this dominance reflects the critical need of large enterprises for scalable and unified data-centric security solutions.

The Small & Medium Enterprises (SMEs) segment is expected to grow at the fastest CAGR form 2026 to 2033, owing to the increasing accessibility of cloud-based Data Security Posture Management (DSPM) solutions that offer cost-effective, scalable, and easy-to-deploy security capabilities. As SMEs accelerate their digital transformation and adopt cloud, SaaS, and remote working models, their exposure to data security risks such as misconfigurations, unauthorized access, and data leaks has significantly increased, creating strong demand for advanced data protection tools. Additionally, the availability of subscription-based pricing models and managed security services is enabling SMEs to adopt DSPM solutions without requiring large upfront investments or extensive in-house cybersecurity expertise. Growing awareness of data privacy regulations and rising cyberattacks targeting smaller organizations are further pushing SMEs to invest in proactive data security measures. In conclusion, this segment’s rapid growth reflects the democratization of enterprise-grade security capabilities, making DSPM increasingly essential for organizations of all sizes.

Data Type Insights

The unstructured data segment dominated the market with the largest revenue share in 2025, driven by the explosive growth of emails, documents, images, logs, multimedia files, and AI-generated content across enterprise environments. As organizations increasingly rely on cloud platforms, SaaS applications, and generative AI tools, unstructured data has become the most widely distributed and least governed data type, significantly increasing the need for advanced visibility, classification, and security controls. This has made DSPM solutions particularly critical in identifying hidden sensitive information, reducing exposure risks, and improving overall data governance across complex infrastructures. For instance, in March 2026, Commvault expanded its enterprise resilience capabilities to include structured and AI data with real-time governance controls, highlighting the growing industry focus on securing diverse and unstructured data types across modern digital ecosystems.

The semi-structured data segment is expected to grow at a significant CAGR over the forecast period, driven by the rapid expansion of modern application architectures that generate data in formats such as JSON, XML, logs, and event streams across cloud-native and API-driven environments. As organizations increasingly adopt SaaS platforms, microservices, and IoT-enabled systems, semi-structured data has become a critical bridge between structured databases and unstructured content, requiring advanced security and governance controls. The growing need for real-time analytics, API security, and cloud data integration is further accelerating demand for DSPM solutions capable of discovering and classifying semi-structured datasets across distributed environments. Furthermore, rising concerns around data leakage through APIs and misconfigured cloud storage are pushing enterprises to strengthen visibility over this data type. For instance, in July 2025, Concentric AI expanded its data security capabilities through the acquisition of Swift Security and Acante to enhance automated data discovery and protection across complex data environments, highlighting the increasing focus on securing semi-structured data in modern DSPM strategies.

Application Insights

The data discovery & classification segment dominated the market, accounting for the largest revenue share in 2025, primarily driven by the increasing need for organizations to gain full visibility into where sensitive data resides and how it is being used across complex cloud, SaaS, and hybrid environments. As enterprises continue to experience rapid data growth and rising exposure risks from misconfigurations, shadow data, and unauthorized access, automated discovery and classification capabilities have become the foundational layer of DSPM solutions. These capabilities enable organizations to identify, categorize, and prioritize sensitive data such as PII, financial records, and intellectual property, which is essential for effective risk management and compliance enforcement. In addition, the growing adoption of AI and data-intensive applications has further amplified the importance of accurate data classification to prevent data leakage and ensure secure AI usage across enterprise ecosystems. For instance, in April 2025, Kyndryl and Microsoft collaborated to enhance data security and risk management using Microsoft Purview, focusing on automated data discovery and classification to help organizations secure and govern sensitive information across hybrid environments. Consequently, the dominance of this segment reflects the critical role of discovery and classification as the starting point for building a strong and proactive data security posture.

The security monitoring & incident response segment is expected to grow at a significant CAGR during the forecast period, driven by the increasing need for real-time visibility, rapid threat detection, and automated response capabilities in complex cloud and hybrid environments. As organizations face a rising volume of sophisticated cyberattacks and data exposure incidents, DSPM solutions are increasingly integrating continuous monitoring and incident response features to quickly identify risky data access patterns, misconfigurations, and potential breaches. The growing shortage of skilled cybersecurity professionals and the need to reduce response times are also accelerating the adoption of AI-driven and automated incident response mechanisms. Additionally, enterprises are prioritizing proactive security operations that can not only detect but also contain and remediate threats across distributed data ecosystems. For instance, in April 2026, Semperis expanded its identity-driven cyber resilience capabilities with enhancements to Purple Knight, enabling improved security assessments and posture visibility for complex environments, including government and hybrid infrastructures, highlighting the industry’s focus on strengthening monitoring and incident response capabilities.

End User Insights

The BFSI segment dominated the data security posture management market in 2025, driven by the sector’s high concentration of sensitive financial data, stringent regulatory requirements, and increasing exposure to sophisticated cyber threats. Banks, financial institutions, and insurance providers manage vast volumes of personally identifiable information (PII), transaction records, and payment data, making them prime targets for data breaches and fraud. As a result, BFSI organizations are rapidly adopting DSPM solutions to gain continuous visibility into data assets, enforce strict access controls, and ensure compliance with evolving regulations such as GDPR, PCI DSS, and other regional financial governance frameworks. Moreover, the sector’s ongoing digital transformation, including the shift to cloud-based banking, mobile payments, and fintech integrations, has further expanded the data attack surface, reinforcing the need for advanced data-centric security controls. Overall, the dominance of BFSI reflects its critical need for robust, proactive, and compliance-driven data security posture management to safeguard highly sensitive financial ecosystems.

The retail & e-commerce segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by the rapid expansion of digital commerce platforms and the increasing need to secure large volumes of customer, payment, and behavioral data generated across online channels. As retailers adopt AI-driven personalization, cloud-based storefronts, and omnichannel strategies, the exposure of sensitive structured, semi-structured, and unstructured data is increasing significantly, thereby accelerating the demand for advanced DSPM solutions. Rising concerns around data breaches, fraud, and stringent consumer data protection regulations are further compelling e-commerce organizations to strengthen their data security posture through continuous discovery, classification, and monitoring capabilities.

In addition, the integration of technologies such as AI analytics, OCR, and image-based processing in retail operations is expanding the data attack surface, making robust security frameworks even more critical. For instance, in February 2024, Symmetry Systems enhanced its DSPM capabilities by introducing OCR and image analysis features to improve the detection and protection of sensitive data within complex retail and e-commerce environments. Thus, the segment’s strong growth outlook reflects the increasing prioritization of data-centric security in the rapidly evolving digital retail ecosystem.

Regional Insights

The data security posture management market in North America dominated the global market with the largest revenue share in 2025, driven by early and widespread adoption of advanced cybersecurity technologies and strong presence of leading DSPM vendors in the region. Enterprises across the United States and Canada are increasingly prioritizing data-centric security strategies due to the rising frequency of sophisticated cyberattacks, cloud misconfigurations, and large-scale data breaches. The rapid adoption of multi-cloud and hybrid cloud environments, combined with extensive use of SaaS applications, has significantly expanded the data attack surface, accelerating demand for continuous data discovery, classification, and monitoring solutions. Additionally, strict regulatory frameworks such as CCPA and sector-specific compliance requirements in BFSI and healthcare are pushing organizations to invest heavily in DSPM platforms. The strong presence of technology giants and high cybersecurity spending further reinforces North America’s leadership in the global DSPM market.

U.S. Data Security Posture Management (DSPM) Market Trends

The data security posture management industry in the U.S. is expected to grow significantly at a CAGR from 2025 to 2033, driven by the rapid expansion of cloud-first enterprise strategies and the increasing complexity of managing sensitive data across hybrid and multi-cloud environments. U.S. organizations are facing a rising number of sophisticated cyberattacks, data breaches, and misconfiguration risks, which are accelerating the adoption of advanced DSPM solutions for continuous data discovery, classification, and risk mitigation. Additionally, strong regulatory pressures such as CCPA and evolving federal data protection initiatives are compelling enterprises to strengthen data governance and compliance capabilities. The widespread adoption of AI, SaaS platforms, and digital transformation initiatives is further increasing data volumes and exposure risks, reinforcing the need for proactive, data-centric security frameworks across U.S. enterprises.

Europe Data Security Posture Management (DSPM) Market Trends

The European data security posture management industry is anticipated to register considerable growth from 2026 to 2033, driven primarily by the region’s stringent data protection regulations, such as GDPR, which continue to compel organizations to strengthen data governance, visibility, and compliance capabilities. Enterprises across Europe are increasingly adopting DSPM solutions to address growing concerns around data sovereignty, cross-border data transfers, and sensitive data exposure in complex cloud and hybrid environments. The rapid digitalization of industries such as BFSI, healthcare, and government services is further expanding data volumes and security risks, accelerating the need for continuous data discovery and classification. Additionally, the rising adoption of multi-cloud strategies and SaaS applications is increasing the complexity of data environments, pushing organizations to implement advanced posture management tools to ensure regulatory compliance and reduce breach risks across distributed systems.

The UK data security posture management market is expected to grow significantly in the forecast period, driven by increasing regulatory enforcement around data protection, particularly under the UK GDPR framework and evolving national cybersecurity policies. Organizations across the UK are rapidly adopting DSPM solutions to gain better visibility and control over sensitive data spread across cloud, SaaS, and hybrid environments. The rising frequency of cyberattacks targeting financial institutions, healthcare providers, and government agencies is further accelerating demand for advanced data-centric security solutions. Additionally, the strong digital transformation initiatives across UK enterprises, along with growing adoption of multi-cloud strategies, are increasing data complexity and exposure risks, thereby boosting the need for continuous data discovery, classification, and risk monitoring capabilities.

Data security posture management market in Germany is expected to grow significantly in the forecast period, driven by the country’s strong industrial base and rapid adoption of cloud and hybrid infrastructures across sectors such as manufacturing, automotive, BFSI, and healthcare. Increasing cyber threats targeting critical infrastructure, along with Germany’s strict regulatory environment under GDPR and the EU’s NIS2 directive, is compelling enterprises to adopt advanced DSPM solutions for continuous data visibility, classification, and risk mitigation. Additionally, the growing complexity of multi-cloud environments and rising concerns around data sovereignty and compliance are further accelerating demand for data-centric security frameworks. Enterprises are also prioritizing automated tools to reduce misconfigurations and strengthen real-time governance across distributed data ecosystems. Overall, Germany’s market growth reflects a strong shift toward proactive, compliance-driven, and cloud-integrated data security strategies.

Asia Pacific Data Security Posture Management (DSPM) Market Trends

The Asia Pacific held a significant share of the global market in 2025, driven by rapid digital transformation across emerging economies and widespread adoption of cloud computing, SaaS platforms, and AI-driven applications. Countries such as China, India, Japan, and South Korea are witnessing exponential growth in data generation, which is increasing the need for advanced data security and governance solutions. The expansion of e-commerce, fintech, and telecom sectors across the region is further intensifying data exposure risks, prompting organizations to adopt DSPM solutions for continuous data discovery, classification, and monitoring. Additionally, rising cybersecurity threats, coupled with strengthening data protection regulations in several Asia Pacific countries, are encouraging enterprises to invest in proactive, data-centric security frameworks.

Data security posture management market in Japan is expected to grow significantly during the forecast period, driven by the country’s increasing focus on strengthening cybersecurity resilience across critical industries such as BFSI, manufacturing, healthcare, and technology. As Japanese enterprises accelerate digital transformation and expand their adoption of cloud and hybrid infrastructures, the complexity of managing sensitive data is rising, creating strong demand for advanced DSPM solutions. Additionally, growing concerns around ransomware attacks, data breaches, and supply chain vulnerabilities are pushing organizations to adopt proactive, data-centric security frameworks. Japan’s stringent data protection and privacy regulations, along with increasing enterprise investment in AI and automation technologies, are further supporting the adoption of continuous data discovery, classification, and risk monitoring capabilities across the market.

The data security posture management market in China held a substantial revenue share in 2025, supported by rapid digitalization across industries and large-scale adoption of cloud computing, AI, and big data technologies. The country’s massive data generation from sectors such as e-commerce, fintech, manufacturing, and telecommunications has significantly increased the need for advanced data security solutions to manage visibility, classification, and risk across complex environments. Furthermore, rising concerns over cyberattacks, data leakage, and regulatory compliance under evolving data protection laws such as the Personal Information Protection Law (PIPL) are encouraging enterprises to adopt DSPM solutions. The expansion of domestic cloud service providers and increasing enterprise focus on data sovereignty and localized data governance are further strengthening market demand. Overall, China’s strong digital ecosystem and regulatory momentum continue to support sustained growth in the DSPM market.

Key Data Security Posture Management (DSPM) Company Insights

Key players operating in the data security posture management industry are BigID, Cyera, Fortanix, Google Cloud, and IBM, and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

Key Data Security Posture Management Companies:

The following key companies have been profiled for this study on the data security posture management market.

- BigID

- Cyera

- Fortanix

- Google Cloud

- IBM

- Microsoft

- Orca Security

- Palo Alto Networks

- Rubrik

- Securiti

- Sentra

- Symmetry Systems

- Varonis

- Wiz

- Zscaler

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Microsoft; Google Cloud (incl. Wiz); IBM; Palo Alto Networks; Zscaler; Varonis; BigID

- Bundling DSPM into larger CNAPP or XDR suites to provide a "single pane of glass" across cloud, identity, and data.

- Rapidly acquiring innovative startups to add advanced data discovery capabilities to their cloud ecosystems instantly.

- Using massive regulatory research teams to automatically map data discovered to hundreds of global jurisdictions (GDPR, CCPA, etc.) out of the box.

- Seamless deployment for customers already using Azure, GCP, or Palo Alto’s Prisma, removing the need for new vendor onboarding.

- The financial and technical backing to scan petabytes of data across the world’s largest enterprise environments without performance degradation.

- Leveraging global signal intelligence to correlate "data at rest" risks with real-time "data in motion" attack patterns.

- Integrated platforms can be "heavy," requiring significant configuration and training compared to nimble, specialized tools.

- Large firms may take longer to release specific, bleeding-edge features (like AI-model data lineage) than specialized startups.

- Their broad focus can sometimes lead to less "depth" in data classification accuracy compared to firms that only do data security.

Emerging Players: Cyera; Securiti; Orca Security; Rubrik; Sentra; Symmetry Systems; Fortanix

- Using advanced large language models to understand data context more deeply than traditional regex-based scanners.

- Moving beyond simple visibility into active "Data Detection and Response" (DDR) and automated remediation.

- Focusing on the "toxic combination" of sensitive data and excessive permissions, often partnering with IGA (Identity Governance) firms.

- Specialized algorithms provide much lower false-positive rates in data classification, which is critical for trust in automated security.

- Most offer "agentless" architectures that can connect to cloud environments in minutes, providing immediate value via "dark data" discovery.

- Able to pivot quickly to secure new technologies, such as protecting the training data used in corporate Generative AI initiatives.

- They often lack the broader infrastructure security (like a firewall or network monitoring) that enterprises want to consolidate.

- High-growth startups are often targets for acquisition, leading to potential roadmap uncertainty for long-term customers.

- Smaller teams may struggle to provide the 24/7 on-the-ground global support that "Mature Players" guarantee.

Recent Developments

-

In September 2025, Varonis acquired SlashNext, an AI-native email security firm, to integrate top-tier phishing and social engineering detection into its Data Security Platform. This bolsters data security posture management (DSPM) by extending threat detection from inboxes across email and collaboration tools to data risks, halting breaches before data compromise.

-

In April 2025, Cyera launched Omni DLP, an AI-native solution that integrates its DSPM platform with real-time DLP from the Trail Security acquisition to enhance data security posture management. It reduces false positives by over 95%, provides adaptive protection for data at rest, in motion, and in use, and addresses AI-era risks like data exfiltration in dynamic environments.

-

In February 2025, Zscaler unveiled Asset Exposure Management (AEM), a CAASM solution built on its Data Fabric for Security that aggregates data from hundreds of sources to create accurate asset inventories, detect coverage gaps, and automate risk mitigation. In relation to data security posture management (DSPM), it enhances cyber risk reduction by providing foundational asset visibility and integrating with Zscaler's broader exposure management for better data protection in hybrid environments.

Data Security Posture Management (DSPM) Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.2 billion

Estimated market size in 2026

USD 2.5 billion

Projected market size by 2033

USD 6.2 billion

Growth rate

CAGR of 13.9% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment mode, organization size, data type, application, end user, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

BigID; Cyera; Fortanix; Google Cloud; IBM; Microsoft; Orca Security; Palo Alto Networks; Rubrik; Securiti; Sentra; Symmetry Systems; Varonis; Wiz; Zscaler

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Security Posture Management (DSPM) Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data security posture management market report based on component, deployment mode, organization size, data type, application, end-user, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solutions

-

Services

-

-

Deployment Mode Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud-Based

-

Public Cloud

-

Private Cloud

-

-

On-Premises

-

-

Organization Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small & Medium Enterprises (SMEs)

-

-

Data Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Structured Data

-

Semi-Structured Data

-

Unstructured Data

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Data Discovery & Classification

-

Data Risk Assessment

-

Data Access Governance

-

Compliance & Regulatory Management

-

Data Loss Prevention (DLP) Enhancement

-

Security Monitoring & Incident Response

-

-

End User Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare & Life Sciences

-

IT & Telecom

-

Retail & E-commerce

-

Government & Public Sector

-

Manufacturing

-

Media & Entertainment

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

- Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customization

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

DSPM market opportunity assessment for a cybersecurity solution provider

Assessment of DSPM demand across key regions (North America, Europe, APAC)

Analysis of adoption trends across cloud, multi-cloud, and SaaS environments

Identified high-growth DSPM adoption segments (BFSI, healthcare, tech)

Supported product positioning within the cloud security and data governance ecosystem

Customized segmentation analysis for DSPM by deployment and enterprise type

Conducted segmentation of the DSPM market by deployment (cloud vs hybrid) and enterprise size

Evaluated adoption across SMEs and large enterprises

Identified enterprise-heavy adoption patterns in large organizations

Highlighted convergence trends with broader cloud security platforms

DSPM digital risk & compliance and market entry assessment for a security vendor

Analysis of regulatory drivers (GDPR, HIPAA, data sovereignty laws) across regions

Evaluation of enterprise requirements for sensitive data discovery, AI governance, and cloud visibility

Identified high-potential regions for DSPM expansion

Supported GTM and partnership strategy with cloud security ecosystems

Frequently Asked Questions About This Report

The global data security posture management market size was valued at USD 2.2 billion in 2025 and is estimated at USD 2.5 billion for 2026.

The global data security posture management market is expected to grow at a CAGR of 13.9% from 2026 to 2033, reaching USD 6.2 billion by 2033.

North America dominated with a 39.8% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include BigID; Cyera; Fortanix; Google Cloud; IBM; Microsoft; Orca Security; Palo Alto Networks; Rubrik; Securiti; Sentra; Symmetry Systems; Varonis; Wiz; Zscaler

Factors such as rising data security risks and increasing cloud adoption are driving market growth and growing need for real-time visibility and control over structured and unstructured data across platforms play a key role in accelerating the Data Security Posture Management (DSPM) market.

The solutions segment led with a 81.3% revenue share in 2025, while the services segment is the fastest-growing.

The cloud-based segment held the largest revenue share in 2025, while the on-premises segment is the fastest-growing.

The large enterprises segment held the largest revenue share in 2025, while the small & medium enterprises segment is the fastest-growing.

The unstructured data segment held the largest revenue share in 2025, while the semi-structured data segment is the fastest-growing.

About the Author(s)

IT Services & Applications Research Team

Technology · IT Services & ApplicationsThis report was authored by the it services & applications research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the it services & applications segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.