- Home

- »

- Next Generation Technologies

- »

-

Deep Tech Market Size, Share & Growth Report 2026-2033GVR Report cover

![Deep Tech Market (2026 - 2033)Report]()

Deep Tech Market (2026 - 2033)

Size, Share & Trends Analysis Report By Deployment Model (On-Premises, Cloud-Based, Hybrid), By Enterprise Size (Small and Medium Enterprises, Large Enterprises), By Technology, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$154.3BMarket Estimate, 2026

$173.7BMarket Forecast, 2033

$501.2BCAGR, 2026–2033

16.3%Deep Tech Market Summary

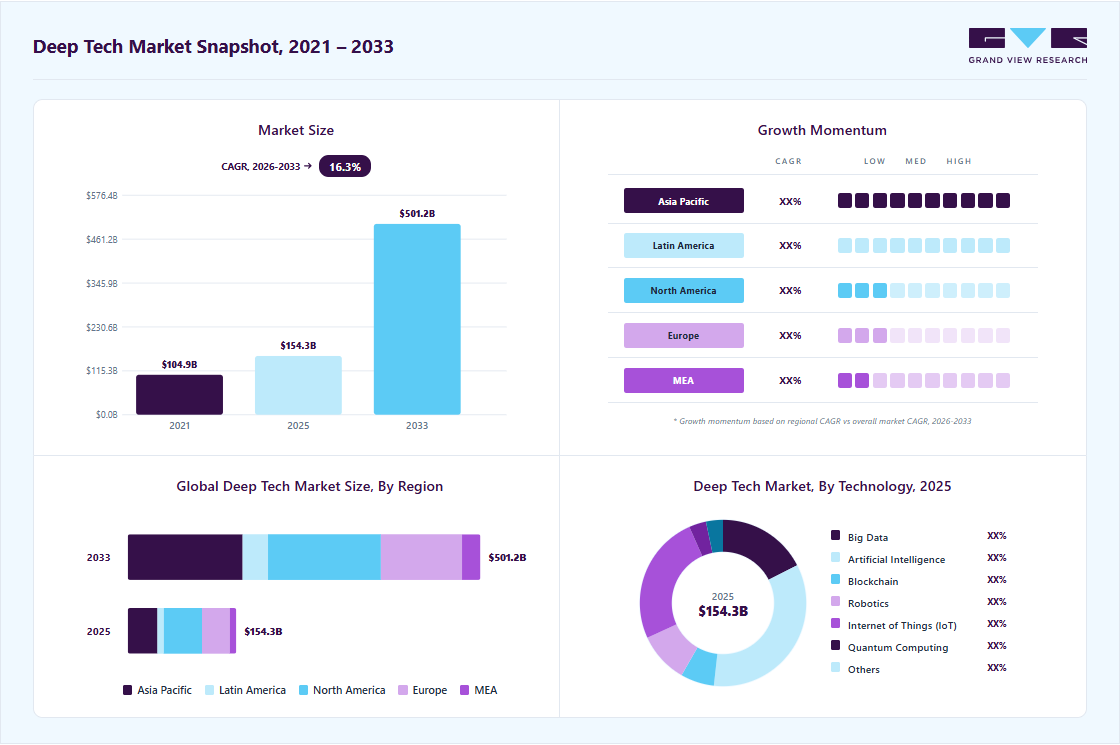

The global deep tech market size was valued at USD 154.3 billion in 2025 and is projected to grow from USD 173.7 billion in 2026 to USD 501.2 billion by 2033, at a CAGR of 16.3% from 2026 to 2033. The market in North America dominated with a revenue share of 35.2% in 2025. The market growth is driven by the increasing demand for breakthrough technologies that enable next-generation digital and physical transformation.

Key Market Trends & Insights

- By deployment model: On-premises segment led the market with the largest revenue share of 40.0% in 2025.

- By enterprise size: Small & medium enterprises segment led the market with the largest revenue share of 70.8% in 2025.

- By technology: Artificial intelligence segment led the market with the largest revenue share of 34.2% in 2025.

- By end-use: IT & telecommunication segment led the market with the largest revenue share of 28.3% in 2025.

Regional Highlights

- Largest regional market: North America (35.2% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 154.3 billion

- Estimated market size in 2026: USD 173.7 billion

- Projected market size by 2033: USD 501.2 billion

- CAGR (2026-2033): 16.3%

Rapid advancements in artificial intelligence (AI), edge computing, and high-performance semiconductors are enabling wider enterprise adoption, further accelerating the growth of the deep tech industry.The increasing adoption of next-generation deep technologies, such as generative AI platforms, edge AI processors, autonomous robotics systems, and digital twin-based simulation environments, is expected to enhance operational intelligence, accelerate decision-making, and deliver high-impact productivity gains. The growing emphasis on smart manufacturing, autonomous mobility ecosystems, and AI-enabled enterprise infrastructure, along with rising demand for predictive maintenance, intelligent automation, and real-time optimization, is accelerating enterprise investments in advanced deep tech solutions, thereby contributing to the sustained expansion of the deep tech industry.

")

The growing deployment of advanced semiconductor technologies, including AI accelerators, neuromorphic chips, photonic computing, and high-efficiency power electronics, is expected to improve computing performance, reduce energy consumption, and support scalable AI workloads. The increasing focus on data center modernization, high-performance computing (HPC), and edge-to-cloud connectivity, combined with demand for low-latency processing in industrial IoT, smart cities, and defense-grade systems, is driving technology upgrades and fueling market growth.

In addition, growing integration of robotics, automation, and intelligent sensing technologies, such as LiDAR, computer vision, sensor fusion, and autonomous navigation software, is expected to improve precision, safety, and scalability across complex operational environments. The expanding demand for warehouse automation, last-mile delivery robotics, autonomous mining equipment, and smart inspection drones, along with increasing investments in AI-powered motion planning and real-time control systems, is strengthening the adoption of deep tech solutions across industrial sectors.

Moreover, the adoption of clean energy and climate deep-tech solutions, such as next-generation battery chemistries, hydrogen production systems, carbon capture technologies, and smart grid optimization platforms, is expected to improve energy efficiency and accelerate decarbonization. The growing focus on net-zero targets, renewable integration, and sustainable industrial operations, combined with increasing deployment of AI-driven energy forecasting, grid digital twins, and predictive asset management, is driving large-scale investments and expanding the deep tech industry.

Deployment Model Insights

The on-premises segment led the market with the largest revenue share of 40.0% in 2025, driven by the strong demand for greater data control, low-latency processing, and regulatory compliance. On-premises deep-tech deployments remain highly preferred for mission-critical AI workloads, robotics and automation systems, and high-volume big-data processing. The growing need for confidential model training, sensitive customer data protection, and internal governance of AI pipelines continues to support the sustained dominance of on-premises deep tech solutions in large-scale enterprise deployments.

The cloud-based segment is expected to register at the fastest CAGR of 19.0% from 2026 to 2033. This growth is attributed to the rapid expansion of AI-as-a-service platforms, scalable big data analytics, and IoT-enabled real-time intelligence applications across multiple industries. Enterprises are increasingly shifting toward cloud-based deep tech models due to benefits such as elastic computing, faster deployment cycles, and access to advanced GPU and accelerator-based compute environments. The growing adoption of generative AI, cloud-native robotics simulation, and edge-to-cloud integration frameworks, along with improvements in cloud security and distributed data processing, is accelerating the cloud-based segment in the deep tech industry.

Enterprise Size Insights

The small & medium enterprise segment accounted for the largest market revenue share in 2025, driven by the rising adoption of cost-efficient deep tech solutions across industries such as retail, IT services, logistics, and small-scale manufacturing. SMEs are increasingly deploying cloud-based AI, big data analytics, IoT monitoring platforms, and automation tools. The growing availability of subscription-based deep tech platforms, low-code AI development tools, and scalable SaaS deployment models is enabling SMEs to adopt advanced technologies. These factors reflect the continued focus on high-volume adoption of affordable deep tech solutions, thereby sustaining the strong position of SMEs in the deep tech industry.

The large enterprise segment is expected to witness at the fastest CAGR from 2026 to 2033. This growth is primarily driven by the expanding deployment of deep tech across enterprise-scale AI transformation programs, autonomous robotics automation, digital twin infrastructure, and advanced cybersecurity. The increasing emphasis on AI governance, regulatory compliance, secure hybrid cloud architectures, and the integration of high-performance computing (HPC) is further fueling adoption. These developments are accelerating enterprise-wide deep tech deployments, thereby contributing to the strong long-term growth of the large enterprise segment in the deep tech industry.

Technology Insights

The artificial intelligence segment accounted for the largest market revenue share in 2025, driven by its strong ability to deliver automation at scale, predictive decision-making, real-time analytics, and intelligent customer engagement, enabling organizations to improve productivity and reduce operational costs. The increasing deployment of generative AI models, AI-powered cybersecurity, intelligent process automation (IPA), and AI-driven recommendation and personalization engines is further strengthening demand. These factors reflect the continued focus on scalable and high-impact deep tech adoption, thereby sustaining the leadership of the artificial intelligence segment in the deep tech industry.

The internet of things (IoT) segment is expected to witness at the fastest CAGR from 2026 to 2033. This growth is primarily driven by the growing need for real-time connected intelligence, predictive maintenance, and smart city infrastructure. The increasing rollout of 5G connectivity, edge computing integration, and low-power sensor networks is enabling faster data capture and low-latency analytics, accelerating IoT adoption across mission-critical deep tech applications. These developments are expected to accelerate IoT deployment, thereby driving strong long-term expansion of the segment in the deep tech industry.

End Use Insights

The IT & telecommunication segment accounted for the largest market revenue share in 2025, driven by the rapid expansion of 5G infrastructure, cloud-native network modernization, and rising demand for AI-enabled network automation. The growing adoption of software-defined networking (SDN), network function virtualization (NFV), and AI-powered cybersecurity frameworks, along with increasing investments in hyperscale data centers, is further strengthening demand, thereby sustaining the leadership of the IT & telecommunication segment in the deep tech industry.

The agriculture segment is expected to register at the fastest CAGR from 2026 to 2033. This growth is primarily driven by the rising adoption of precision farming technologies, AI-based crop monitoring, and IoT-enabled smart irrigation systems. The growing emphasis on sustainable farming practices, real-time farm asset monitoring, and data-driven decision-making, supported by improving rural connectivity and falling sensor costs, is accelerating adoption, thereby supporting strong growth of the segment in the deep tech industry.

Regional Insights

North America dominated the global deep tech market with the largest revenue share of 35.2% in 2025, fueled by the region’s strong lottery retail infrastructure, high consumer participation in draw-based jackpot games, and the rapid expansion of regulated online lottery platforms. The widespread presence of state/provincial lottery operators, strong government-backed credibility, and high disposable income levels continue to support consistent ticket sales. The growing integration of digital payment systems, loyalty programs, and mobile-based lottery applications is improving accessibility, thereby strengthening long-term lottery industry growth in the region.

U.S. Deep Tech Market Trends

The deep tech market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by the dominance of multi-state jackpot lotteries, strong state-level revenue generation models, and the high frequency of scratch-off and draw-based lottery participation. The country benefits from a highly developed retail distribution network across convenience stores, supermarkets, and gas stations, which sustains strong offline ticket sales. The increasing legalization of online lottery sales across multiple states, combined with the rising adoption of digital wallets, is accelerating consumer participation, thereby supporting the continued growth of the lottery industry in the country.

Europe Deep Tech Market Trends

The deep tech market in Europe is expected to grow at a significant CAGR of 14.8% from 2026 to 2033. In Europe, the market is driven by strong government-regulated lottery frameworks, high consumer trust in national lottery systems, and the growing shift toward digital lottery platforms. The region’s emphasis on responsible gambling policies, secure payment infrastructure, and strict licensing requirements is strengthening market stability. The rising adoption of mobile lottery apps, cross-border jackpot interest, and expanding digital engagement strategies are increasing lottery participation, thereby supporting steady market expansion across Europe.

The UK deep tech market held a significant share in Europe in 2025. This expansion is supported by strong consumer loyalty toward national lottery products, the expansion of digital lottery ticket sales, and increasing demand for instant win and scratchcard-style formats. The country's highly mature online payment ecosystem and widespread smartphone usage enable higher engagement through mobile platforms. The growing interest in cause-based lottery participation, strong marketing campaigns, and the increasing integration of subscription-based lottery models are driving long-term growth in the lottery market.

The deep tech market in Germany is rapidly expanding, driven by strong participation in state-regulated lotteries and rising demand for secure, transparent lottery operations. Germany’s strong regulatory environment and high consumer preference for legitimate, government-backed lottery systems continue to support market stability. The growing shift toward mobile ticket purchasing, digital result tracking, and app-based lottery engagement, combined with increasing interest in high-value jackpot formats, is accelerating participation, reinforcing Germany’s position as a key growth market in the deep tech industry.

Asia-Pacific Deep Tech Market Trends

The deep tech market in Asia-Pacific is expected to register the fastest CAGR of 19.0% from 2026 to 2033, driven by rapid smartphone penetration, rising internet accessibility, and the expansion of government-supported lottery programs across emerging economies. The region’s large population base, rising disposable incomes, and growing adoption of digital payments are enabling faster growth in both online and offline lottery participation. The increasing popularity of sports-linked lottery formats, expanding retail distribution networks, and rising demand for jackpot-driven games are positioning the Asia Pacific region as a high-growth region for the lottery industry.

The Japan deep tech market is gaining momentum, driven by strong demand for draw-based lottery games, high consumer trust in regulated lottery systems, and the increasing shift toward digital engagement through official online platforms. Japan’s mature payments ecosystem and strong retail presence through convenience stores continue to support stable offline lottery sales. The rising adoption of mobile-friendly ticket purchasing, improved digital user experiences, and growing consumer interest in high-value jackpot opportunities are further strengthening the long-term expansion of the country's lottery market.

The deep tech market in China is witnessing robust expansion, fueled by the country’s large-scale lottery participation base, the growing popularity of sports lottery formats, and strong demand for government-authorized lottery programs. China’s rapid adoption of mobile payments and digital consumer ecosystems is accelerating the shift toward online engagement. The increasing national interest in sports events, rising disposable incomes, and the growing emphasis on secure lottery distribution are driving widespread adoption, thereby supporting the strong growth of the lottery market in China.

Key Deep Tech Company Insights

Some of the key players operating in the market are NVIDIA Corporation and Microsoft Corporation, among others.

-

NVIDIA Corporation is a global company in advanced computing and AI acceleration technologies, specializing in high-performance GPUs, AI supercomputing platforms, and edge AI hardware that enable large-scale deep learning, robotics, autonomous systems, and real-time industrial intelligence. With extensive innovation in AI infrastructure, accelerated computing, and AI software ecosystems such as CUDA and enterprise AI stacks, the company drives deep tech adoption across hyperscale data centers, automotive autonomy, and smart manufacturing, reinforcing its position as a core enabler in the deep tech industry.

-

Microsoft Corporation is a global technology company in deep tech innovation, specializing in cloud-scale AI, advanced enterprise computing, and next-generation digital infrastructure through its Azure platform. The company enables deep-tech commercialization through foundation AI models, AI co-pilots, and scalable cloud AI services that support enterprise automation, predictive analytics, cybersecurity modernization, and intelligent operations. Microsoft continues to accelerate deep tech adoption across industries, strengthening its leadership in the field.

Anthropic PBC and Covariant are some of the emerging participants in the deep tech industry.

-

Anthropic PBC is a fast-growing deep tech company specializing in advanced generative AI and large language model development, focused on delivering high-performance, safety-aligned AI systems for enterprise and mission-critical use cases. The company’s rapid innovation in foundation model training, responsible AI alignment methods, and scalable AI deployment is enabling organizations to adopt next-generation deep tech capabilities across customer service automation, knowledge workflows, and intelligent decision support. With strong momentum in enterprise AI adoption and model innovation, Anthropic is emerging as a high-impact player in the deep tech industry.

-

Covariant is an emerging deep tech company specializing in AI-powered robotics and autonomous manipulation systems that enable intelligent automation in warehouses and industrial environments. The company integrates deep learning, computer vision, and robotics control software to deliver adaptive robotic picking and material handling solutions that improve speed, accuracy, and operational efficiency. With the growing demand for robotics-led supply chain modernization and scalable automation, Covariant is strengthening its presence as an emerging innovator in the deep tech industry.

Key Deep Tech Companies:

The following key companies have been profiled for this study on the deep tech market.

- Anthropic PBC

- Databricks

- Alphabet Inc. (Google DeepMind)

- NVIDIA Corporation

- International Business Machines Corporation

- Microsoft Corporation

- Amazon Web Services, Inc.

- Oracle Corporation

- Siemens AG

- Qualcomm Technologies, Inc.

- SAP SE

- Covariant.

Recent Developments

-

In February 2026, Anthropic PBC secured a USD 30 billion Series G funding round, marking one of the largest funding events in the AI space and underscoring strong investor confidence in enterprise AI platform development, advanced AI models, and cloud-scale deep tech deployments. This capital influx is expected to accelerate the development of frontier AI research, expand computing infrastructure, and enterprise AI products, further strengthening Anthropic’s role in shaping next-generation deep tech applications.

-

In January 2026, NVIDIA Corporation launched its next-generation AI platform called the Rubin platform, comprising six new chips optimized for high-performance computing workloads and advanced reasoning models, representing a significant architectural leap for AI supercomputing and agentic AI deployment across industrial, scientific, and enterprise deep tech applications. The launch of the Rubin platform signals accelerated innovation in AI infrastructure, enabling deeper integration of AI into complex automation and next-generation AI systems across sectors in the deep tech industry.

-

In October 2025, Oracle announced the upcoming OCI Zettascale10 cloud supercomputer project, designed to connect up to 800,000 GPUs across multiple data centers to deliver massive AI compute performance capable of supporting large-scale generative AI and simulation workloads. This positions Oracle as a strategic provider of next-generation AI infrastructure that can underpin deep tech innovation across AI research, scientific computing, and enterprise automation.

Deep Tech Market Report Scope

Report Attribute

Details

Market size in 2025

USD 154.3 Billion

Estimated market size in 2026

USD 173.7 Billion

Projected market size by 2033

USD 501.2 Billion

Growth rate

CAGR of 16.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report Product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Deployment model, enterprise size, technology, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Anthropic PBC; Databricks; Alphabet Inc. (Google DeepMind); NVIDIA Corporation; International Business Machines Corporation; Microsoft Corporation; Amazon Web Services, Inc.; Oracle Corporation; Siemens AG; Qualcomm Technologies, Inc.; SAP SE; Covariant.

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Deep Tech Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technology trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global deep tech market report based on deployment model, enterprise size, technology, end use, and region:

-

Deployment Model Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premises

-

Cloud-Based

-

Hybrid

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small and Medium Enterprises

-

Large Enterprises

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Big Data

-

Artificial Intelligence

-

Blockchain

-

Robotics

-

Internet of Things (IoT)

-

Quantum Computing

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT & Telecommunication

-

Automotive

-

Healthcare

-

Agriculture

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Frequently Asked Questions About This Report

North America dominated with a 35.2% revenue share in 2025.

The on-premises segment accounted for the largest market share of 40% in 2025, driven by the strong demand for greater data control, low-latency processing, and regulatory compliance. On-premises deep tech deployments remain highly preferred for mission-critical AI workloads, robotics automation systems, and high-volume big data processing. The growing need for confidential model training, sensitive customer data protection, and internal governance of AI pipelines continues to support the sustained dominance of on-premises deep tech solutions in large-scale enterprise deployments.

Some key players operating in the deep tech market include Anthropic PBC, Databricks, Alphabet Inc. (Google DeepMind), NVIDIA Corporation, International Business Machines Corporation, Microsoft Corporation, Amazon Web Services, Inc., Oracle Corporation, Siemens AG, Qualcomm Technologies, Inc., SAP SE, Covariant.

The key factors driving the deep tech include the increasing demand for breakthrough technologies that enable next-generation digital and physical transformation. Rapid advancements in artificial intelligence (AI), edge computing, and high-performance semiconductors are enabling wider enterprise adoption, further accelerating the growth of the deep tech industry.

Small & medium enterprises segment led with the largest revenue share of 70.8% in 2025, while large enterprises is the fastest-growing segment

Artificial intelligence segment aheld the largest revenue share in 2025, while internet of things (IoT) is the fastest-growing segment

IT & telecommunication segment held the largest share in 2025, while agriculture is the fastest-growing segment

The global deep tech market size was estimated at USD 154.3 billion in 2025 and is expected to reach USD 173.7 billion in 2026.

The global deep tech market is expected to grow at a compound annual growth rate (CAGR) of 16.3% from 2026 to 2033 to reach USD 501.2 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.