- Home

- »

- Network Security

- »

-

Defense Cybersecurity Market Size, Industry Report, 2033GVR Report cover

![Defense Cybersecurity Market Size, Share & Trends Report]()

Defense Cybersecurity Market (2025 - 2033) Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Deployment Mode (On-premises, Cloud), By Solution, By Security Type, By End-use (Network Security), By Region, And Segment Forecasts

Market Size, 2024

$30.5BMarket Estimate, 2026

$33.3BMarket Forecast, 2033

$78.9BCAGR, 2025–2033

11.4%Defense Cybersecurity Market Summary

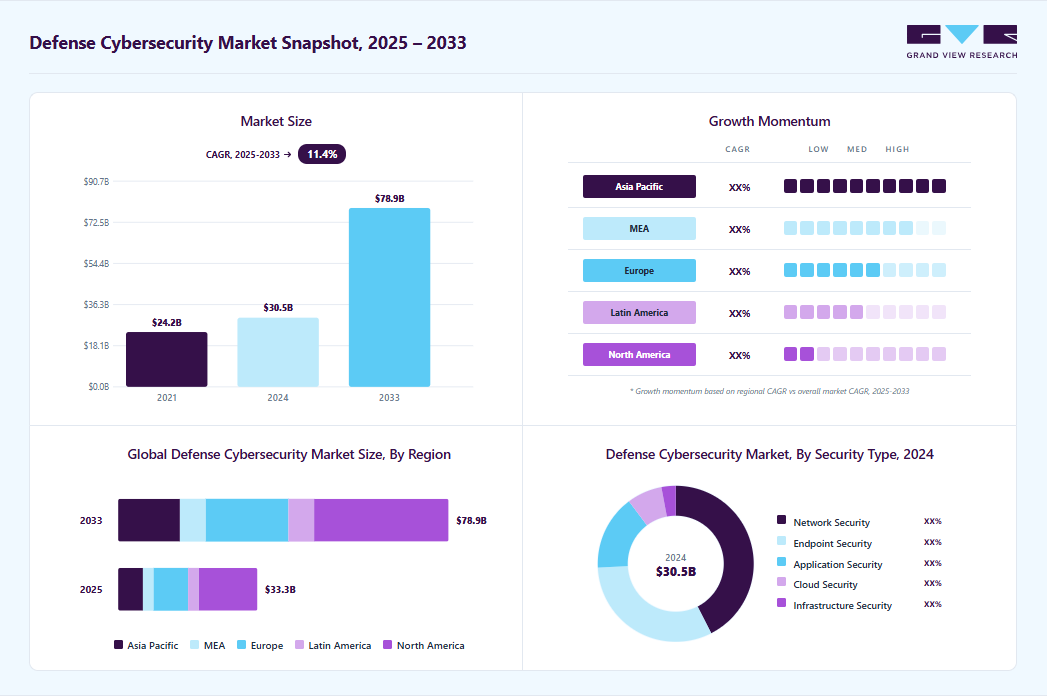

The global defense cybersecurity market size was estimated at USD 30.49 billion in 2024 and is projected to reach USD 78.85 billion by 2033, growing at a CAGR of 11.4% from 2025 to 2033. The growth is attributed to the increasingly investing in cybersecurity by nation-states, defense agencies, and the military to counter a growing wave of nation-sponsored cyberattacks, zero-day exploits, and advanced persistent threats (APTs).

Key Market Trends & Insights

- North America held a 42.17% revenue share of the global defense cybersecurity market in 2024.

- In the U.S., the market is driven by federal investments, AI integration, and evolving zero-trust mandates.

- By deployment mode, the on-premises segment held the largest revenue share of 71.87% in 2024.

- By solution, the cyber threat protection segment accounted for the largest revenue share of 37.54% in 2024.

- By component, the services segment accounted for the largest revenue share of 41.92% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 30.49 Billion

- 2033 Projected Market Size: USD 78.85 Billion

- CAGR (2025-2033): 11.4%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Modern defense cybersecurity strategies are shifting from perimeter-based security to layered architectures that emphasize network segmentation, threat intelligence sharing, and resilient systems architecture. For instance, agencies are integrating multi-domain security frameworks that protect traditional IT infrastructure along with operational technologies (OT), military-grade communications, and weapon systems from cyber infiltration. Consequently, as hybrid warfare and cyber espionage become standard tactics, governments are prioritizing military-specific cybersecurity standards, red-teaming exercises, and scenario-based threat modeling to enhance national cyber defense readiness.")

Additionally, governments across regions are significantly increasing defense cybersecurity budgets in response to escalating cyber conflicts and digital warfare risks. A growing trend is the formalization of cyber resilience frameworks that embed security across the entire weapon system lifecycle. Moreover, defense agencies are also aligning cybersecurity with mission assurance by mandating modular, standards-driven approaches that support continuous assessment, secure-by-design architectures, and adaptable threat mitigation. These efforts reflect a shift toward collating cybersecurity not as a compliance checkbox, but as a critical performance attribute.

For instance, in December 2024, the U.S. Department of Defense released Version 4.3 of its Cyber Resilient Weapon Systems (CRWS) Body of Practice, an updated online reference guide that helps defense programs implement cyber resilience measures across complex weapon systems. This provides revised practices, DoD-specific guidance, and improved navigation features, reinforcing the growing emphasis on scalable, threat-informed defense cybersecurity integration. In conclusion, as the threat landscape becomes more complex, the market is rapidly evolving to incorporate predictive, automated, and resilience-driven defense capabilities.

Component Insights

The services segment accounted for the largest revenue share of 41.92% in 2024, due to the increasing dependence of military agencies on outsourced expertise to safeguard critical digital infrastructure against advanced cyber threats. Additionally, as the complexity of cyber warfare increases defense organizations are relying on managed services for continuous monitoring, threat intelligence integration, system hardening, and rapid incident response. These services not only provide flexibility and scalability but also alleviate the burden on internal cyber units by offering support across diverse threat environments. For instance, in August 2024, Science Applications International Corp. (SAIC) was awarded a contract by the U.S. Navy to provide Command, Control, Communications, Computers, and Intelligence (C4I) integrated cyber support services for Naval Information Warfare Center Pacific. This includes cybersecurity engineering, vulnerability assessments, and red-teaming exercises to fortify maritime defense assets. Consequently, the surge in mission-specific, full-spectrum service engagements is propelling the growth of the services segment in the global market.

The software segment is expected to grow at the fastest CAGR of 12.1% during the forecast period, driven by the growing demand for unified, modular platforms that offer real-time threat detection, zero-trust enforcement, and AI-driven response. As defense agencies modernize their digital infrastructure, they require cybersecurity software capable of securing hybrid environments, integrating with legacy systems, and enabling rapid threat remediation without hardware dependency. Additionally, software-led defense solutions provide scalable automation, policy-based controls, and intelligent analytics that align with evolving mission needs.

Moreover, the rise in cloud adoption and remote command operations is increasing the need for software platforms that offer centralized visibility and control. For instance, in February 2022, Tata Consultancy Services (TCS) launched its Cyber Defense Suite, an integrated, cloud-native platform offering modules for threat intelligence, identity access management, vulnerability scanning, and incident response designed to secure digital transformation for enterprises and public sector clients. This reflects a shift toward software-defined cybersecurity ecosystems that are interoperable and adaptive to emerging threats, thereby driving growth in the software segment of the industry.

Deployment Mode Insights

The on-premises segment accounted for the largest revenue share of 71.87% in 2024, primarily due to the increasing need for high-assurance and physically controlled environments within military and defense agencies. Defense organizations continue to favor on-premises deployments because they enable full sovereignty over sensitive data, granular control of security configurations, and compliance with stringent national defense regulations and frameworks such as CMMC, NIST 800-171, and ISO/IEC 27001. Additionally, on-prem infrastructures minimize latency and ensure uninterrupted performance in contested environments, a critical requirement during combat operations or cyber disruption scenarios. Moreover, legacy defense systems, air-gapped environments, and weapon platforms are often not cloud-compatible, necessitating localized cybersecurity architectures. Also, the increasing threat of nation-state attacks and the need for secure enclaves further reinforce the value of hardened, internally managed cybersecurity solutions. Consequently, on-premises deployment remains the dominant mode due to its supreme alignment with operational security, resilience, and regulatory expectations in defense ecosystems.

The cloud segment is expected to grow at a CAGR of 12.6% over the forecast period, driven by the rising need for scalable and secure infrastructure capable of supporting real-time defense operations. Defense agencies are adopting cloud-based cybersecurity platforms that offer centralized visibility, automated compliance, threat intelligence integration, and AI-powered response delivering faster deployment, mission adaptability, and reduced maintenance overhead. Additionally, the shift toward hybrid warfare, edge connectivity, and digital battlefield coordination is pushing defense institutions to invest in sovereign, air-gapped, and zero-trust cloud architectures that can secure both classified and non-classified workloads.

For instance, in June 2025, Oracle launched a first-of-its-kind global defense ecosystem built on its secure cloud infrastructure, designed to support national security innovation by delivering AI, cybersecurity, and data integration capabilities across defense supply chains, battlefield systems, and allied operations. This reflects a growing trend in which cloud-native platforms are being tailored for defense-specific requirements, thereby driving the rapid expansion of the cloud segment in the industry.

Solution Insights

The cyber threat protection segment accounted for the largest revenue share of 37.54% in 2024, propelled by the critical need for proactive defense against sophisticated, persistent cyber threats targeting military infrastructure and weapon systems. Defense agencies are prioritizing advanced protective measures such as intrusion prevention systems, next-generation firewalls, malware sandboxing, endpoint detection and response (EDR), and integrated threat intelligence to detect and neutralize threats. Additionally, in response to cyberattacks involving zero-day vulnerabilities, lateral movement techniques, and coordinated threats across space-based systems, organizations are adopting multi-layered security architectures to strengthen their cyber defense posture.

For instance, in December 2024, the U.S. Space Force awarded an approximately USD 34.5 million contract to ASIRTek Federal Services to provide “Delta 6 defensive cybersecurity operations,” a specialized program focused on protection, detection, and response for space weapon systems, highlighting the military’s reliance on dedicated cyber threat protection solutions.Consequently, the increasing complexity of cyber threats and the strategic imperative to protect defense assets are accelerating the growth of cyber threat protection as the key solution in the global industry.

The Identity and Access Management (IAM) segment is predicted to witness the fastest CAGR of 12.2% in the upcoming years, driven by the growing emphasis on zero-trust security models, insider threat mitigation, and secure access. As military agencies digitize command systems and extend collaborations to allied forces and contractors, there is a critical need for robust IAM solutions that manage user privileges dynamically, enforce least‑privilege principles, and continuously verify identities. Moreover, IAM platforms integrate multi-factor authentication (MFA), biometric controls, and behavioral analytics offering both enhanced security and audit readiness. Additionally, rising credential-based attacks and insider risks have made IAM a key strategic investment. For instance, in July 2023, Accenture Federal Services secured a USD 94 million contract with the U.S. Army to modernize its Identity, Credential, and Access Management (ICAM) systems, deploying identity governance, privileged access management, and MFA across over 1,500 applications. In conclusion, the strategic importance of IAM in enforcing secure, role-based access, supporting zero-trust implementation, and mitigating identity-driven threats is projected to drive its growth in the industry.

Security Type Insights

The network security segment accounted for the largest share of 42.47% in 2024, driven by its foundational role in safeguarding critical communication and data networks across military domains. Defense operations rely on robust network gateways like next-generation firewalls, intrusion detection/prevention systems (IDPS), encrypted comms, and micro-segmentation to block lateral movement and DDoS attacks. Moreover, with networks spanning air, sea, land, space, and cyber domains, the attack surface has grown significantly, necessitating AI-enabled network monitoring and zero-trust segmentation to detect and neutralize threats in real time. These capabilities are essential for preserving operational continuity in contested and hybrid warfare environments. For instance, in July 2024, the U.S. Defense Information Systems Agency (DISA) awarded Leidos a USD 823 million task order to manage and secure the DoDNet infrastructure, serving up to 370,000 users across 14 defense agencies. This contract emphasizes network resilience and cybersecurity through virtual desktop delivery and enhanced network operations.In conclusion, the rising complexity and interdependence of defense communication infrastructures are reinforcing network security as a strategic priority, solidifying its position within the market.

The cloud security segment is expected to grow at the highest CAGR of 13.1% during the forecast period, driven by defense agencies’ rapid transition toward cloud-native architectures that deliver scalable and secure protection for critical workloads. As military operations extend across hybrid environments, the demand for cloud-based defenses like secure access, cloud workload protection platforms, and AI-powered threat detection continues to surge. These solutions offer centralized visibility, automated compliance, and real-time policy enforcement, which are essential for safeguarding sensitive systems against misconfiguration exploits and account hijacking. Furthermore, compliance mandates such as FedRAMP, CMMC, and zero-trust frameworks also focus on the need for advanced cloud security tooling. For instance, in March 2025, Oracle secured a deal to deliver an “air‑gapped” isolated cloud environment and AI-driven cybersecurity capabilities to Singapore’s armed forces, highlighting the operational importance and trust in sovereign cloud security solutions. In summary, as defense ecosystems modernize toward distributed and data-centric deployments, the demand for cloud security is expected to increase.

End-use Insights

The land forces segment accounted for the largest revenue share of 45.63% in 2024, reflecting the extensive digital transformation and networked operations within ground military units. Army formations rely on interlinked command-and-control hubs, armored and unmanned ground vehicles, mobile edge computing platforms, and sensor networks, which demand robust cybersecurity defenses to counter electronic warfare, cyber-physical incursions, and data-driven threats. For instance, in August 2024, Sealing Technologies was awarded a USD 9.59 million contract by the U.S. Army to deliver its Deployable Defensive Cyber Operations System, Modular Version 2 (DDS‑Mv2), providing portable cyber-defense capabilities for frontline Cyber Protection Teams. In conclusion, the digitization of land-based systems, the evolving threat spectrum, and the operational necessity for on-site cyber protection are contributing significantly to spurring the growth of the global land forces segment.

The Naval Forces segment is expected to grow at the highest CAGR of 12.3% during the forecast period, driven by the increasing digitization of maritime defense operations and the strategic imperative to secure multi-domain naval systems from advanced cyber threats. As modern naval fleets become more reliant on interconnected platforms, including surface vessels, submarines, autonomous systems, and maritime command centers the need for robust cybersecurity frameworks that ensure resilient communications, operational continuity, and asset integrity has intensified. Naval forces are investing in secure communication networks, zero-trust architectures, and cyber-hardened platforms to defend against espionage, GPS spoofing, signal jamming, and cyber-physical intrusions. For instance, in February 2025, Airbus was awarded a USD 503.22 million (€480 million) contract to design, deploy, and maintain a next-generation communication network for the French Air and Naval forces, which integrates enhanced cybersecurity and cryptographic capabilities tailored to meet national sovereignty and resilience standards. Therefore, this initiative reflects a shift among global naval commands toward building cyber-resilient maritime infrastructure, thus positioning naval forces as the fastest-growing segment within the market.

Regional Insights

North America defense cybersecurity market accounted for the largest share of 42.17% in 2024, driven by strong federal cybersecurity initiatives, sustained military modernization programs, and growing public-private defense collaborations. Additionally, the U.S. Department of Defense (DoD) continues to lead in cyber readiness through frameworks like Zero Trust Architecture (ZTA), the Cybersecurity Maturity Model Certification (CMMC), and investments in cyber talent pipelines across the defense industrial base. Moreover, Canada’s defense agencies are increasing their investments in cyber-resilient command-and-control systems, as well as bilateral cybersecurity initiatives with the U.S. under NORAD and NATO-led operations. Consequently, the region’s strong cybersecurity procurement pipeline, combined with early adoption of modular and autonomous cyber defense technologies, continues to reinforce North America’s leadership in the market.

U.S. Defense Cybersecurity Market Trends

The defense cybersecurity market in the U.S. is experiencing growth, driven by federal investments, AI integration, and evolving zero-trust mandates. With over USD 30 billion allocated for cybersecurity in FY2025, the Department of Defense (DoD) is focusing on improving its digital infrastructure through AI-enabled threat detection, secure supply chains, and real-time cyber operations. Major initiatives such as the rollout of the Cybersecurity Maturity Model Certification (CMMC) 2.0 and DISA’s Thunderdome program are reinforcing zero-trust architectures across defense networks. Additionally, public-private collaboration is also increasing, which emphasizes joint threat intelligence sharing and incident response. Furthermore, legislative momentum is building around supply chain resilience and critical infrastructure protection, with growing support from both Congress and federal agencies. In conclusion, the U.S. is shaping the global defense cybersecurity landscape through a combination of policy enforcement, technological innovation, and ecosystem-wide coordination.

Europe Defense Cybersecurity MarketTrends

The defense cybersecurity market in Europe is anticipated to register considerable growth from 2025 to 2033.The growth is attributed to the strong focus on cyber resilience and digital sovereignty. Additionally, a key strategic development is the “Readiness 2030” initiative, which allocates up to €800 billion, including €150 billion in defense-focused loans to enhance military readiness, with a strong emphasis on strengthening cyber resilience, fortifying command-and-control infrastructure, and advancing digital interoperability across EU member states. Additionally, NATO’s commitment to allocate 1.5% of GDP toward cybersecurity and hybrid threat mitigation (within its broader 5% defense budget requirement) is accelerating R&D funding, tech procurement, and procurement frameworks for advanced cyber tools in European countries.

The U.K. defense cybersecurity market is undergoing a strategic transformation driven by a surge in hybrid threats, regulatory reinforcement, and rapid capability development. Additionally, the government is revising legislation to address "grey‑zone" cyber risks such as sabotage of undersea infrastructure and disinformation campaigns updating century-old laws to include modern cyber dimensions.Moreover, the Strategic Defence Review is propelling significant investment in cyber and electromagnetic warfare capabilities, including the establishment of a dedicated Cyber & Electromagnetic Command and a £1 billion “Digital Targeting Web” to integrate cyber operations into frontline decision-making processes. To address these threats MoD launched a fast-track cyber recruitment pipeline, accelerating the training of cyber specialists from weeks to months to supply talent to the National Cyber Force and frontline operations.

The defense cybersecurity market in Germany is undergoing transformation, driven by strategic alliances and targeted investments in cyber capabilities. A key development is the elevation of the Cyber and Information Domain Service (CIDS) to a full military branch, reflecting Germany’s commitment to embedding cyber operations into national defense strategy. Additionally, Germany is also expanding international collaboration, through a cyber partnership with Israel aimed at establishing a joint research center under the “Cyber Dome” initiative to enhance resilience against supply chain and information warfare threats. Consequently, these developments highlight Germany’s push toward a sovereign and alliance-integrated cyber defense ecosystem.

Asia Pacific Defense Cybersecurity Market Trends

The defense cybersecurity market in Asia Pacific is expected to register the fastest CAGR of 12.1% from 2025 to 2033, driven by escalating regional tensions, digital modernization of armed forces, and a surge in cyberattacks targeting defense infrastructure. Countries such as China, India, Japan, and South Korea are investing in indigenous cyber capabilities, zero-trust frameworks, and sovereign cloud infrastructure to safeguard sensitive military assets. Moreover, the rise of AI-enabled surveillance, drone warfare, and cross-border digital threats is prompting defense ministries across the region to prioritize real-time cyber threat detection. Additionally, the increasing focus on Indo-Pacific security cooperation, evident through multilateral defense exercises and cyber-focused pacts like the Quad Cybersecurity Partnership, is accelerating collaborative efforts to bolster regional cyber resilience. Therefore, strong government initiatives and the expansion of dual-use technologies are contributing notably to positioning Asia Pacific as the fastest-growing region in the global defense cybersecurity market.

Japan defense cybersecurity market is undergoing a strategic overhaul marked by policy innovation, organizational modernization, and enhanced international cooperation. A crucial development is Japan’s enactment of the Active Cyberdefence Law, which grants the government and Self‑Defense Forces new capabilities such as monitoring cross-border IP traffic, mandating breach reporting for critical infrastructure, and executing preemptive cyber operations to proactively counter escalating digital threats.Additionally, NEC has inaugurated a dedicated cybersecurity center in Kawasaki, leveraging generative AI for real‑time threat detection and intelligence-sharing, with plans to establish a global network of such hubs.Furthermore, Tokyo is strengthening its cyber alliances by engaging in NATO-led exercises and advancing joint initiatives focused on AI-drone integration and cyber interoperability, aligning with its broader “USADEN” strategy, which aims to unify capabilities across cyber, space, and electromagnetic warfare domains. Consequently, these factors are contributing substantially to bolstering the growth of the Japanese market.

The defense cybersecurity market in China is undergoing significant strategic expansion, driven by the People’s Liberation Army’s commitment to establishing a dedicated cyberspace warfare force and deepening civil-military cybersecurity integration. In April 2024, the PLA formally launched its Cyberspace Force, separating cyber operations from its Strategic Support Force to strengthen national cyber sovereignty, real-time threat response, and offensive-defensive cyber capabilities. Additionally, China is investing in national cyber ranges, requiring real-time incident reporting by telecoms, and building AI-rich cyber-innovation hubs under the military‑civil fusion policy, reflecting a coordinated approach to dual-use technological advancement.

India defense cybersecurity market is advancing rapidly through both structural reforms and targeted investments in technology and talent. A central trend is the elevation of the Defence Cyber Agency (DCyA), India’s tri-service cyber command that has become fully operational, enhancing integrated cyber capabilities across the Army, Navy, and Air Force. Also, the Defence Ministry has begun deploying "Maya OS", an indigenous Linux-based operating system fortified with the “Chakravyuh” endpoint defense suite, signaling a broader move toward software sovereignty and secure supply chains. Furthermore, the government’s emphasis on long-term resilience is evident through policy and academia-led capacity-building efforts such as the USI-CyberPeace Center of Excellence, which advances public-private partnerships in cyber defense. Subsequently, these factors are contributing substantially to spurring the growth of the Indian market.

Key Defense Cybersecurity Companies Insights

Key players operating in the defense cybersecurity market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Defense Cybersecurity Companies:

The following are the leading companies in the defense cybersecurity market. These companies collectively hold the largest market share and dictate industry trends.

- BAE Systems plc

- CACI International Inc.

- General Dynamics Corporation

- IBM Corporation

- Leidos Holdings Inc.

- Lockheed Martin Corporation

- L3Harris Technologies Inc.

- Northrop Grumman Corporation

- Palantir Technologies Inc.

- Nicopods ehf.

- QinetiQ Group plc

- Raytheon Technologies Corporation

- SAIC Inc.

- Thales S.A.

- Airbus Defence and Space

- Booz Allen Hamilton Holding Corp.

Recent Developments

-

In May 2025, Leidos acquired Kudu Dynamics for approximately USD 300 million to enhance its AI-enabled offensive cyber and electromagnetic spectrum capabilities, accelerating its ability to deliver advanced automated targeting and scalable cyber solutions for defense, intelligence, and homeland security customers. This strategic move aligns with Leidos’ NorthStar 2030 growth plan, reinforcing its position in the defense cybersecurity market by rapidly advancing next-generation cyber warfighting technologies.

-

In April 2025,Leidos was awarded a USD 390 million contract by the NSA to deliver advanced signals intelligence (SIGINT) capabilities, engineering, analysis, and reporting tools over a potential five-year period. This contract strengthens Leidos' role in the defense cybersecurity market by enhancing NSA's SIGINT infrastructure with resilient communications and integrated cyber, radar, and sensor technologies critical for information superiority in military and intelligence operations.

-

In January 2025, BAE Systems secured a £285 million contract under the RECODE program to modernize and support the Royal Navy’s combat management systems, shared infrastructure, and warship networks across 20 vessels, enhancing cybersecurity, system availability, and operational agility through integrated DevSecOps principles.

-

In January 2025, Leidos secured a USD 120 million contract from the U.S. Department of Defense to provide advanced cybersecurity and cryptographic key management services, reinforcing its leadership in safeguarding national security communications.

Defense Cybersecurity Market Report Scope

Report Attribute

Details

Market size in 2025

USD 33.25 billion

Revenue forecast in 2033

USD 78.85 billion

Growth rate

CAGR of 11.4% from 2025 to 2033

Actual data

2021 - 2024

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report scope

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment mode, solution, security type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

BAE Systems plc; CACI International Inc.; General Dynamics Corporation; IBM Corporation; Leidos Holdings Inc.; Lockheed Martin Corporation; L3Harris Technologies Inc.; Northrop Grumman Corporation; Palantir Technologies Inc.; QinetiQ Group plc; Raytheon Technologies Corporation; SAIC Inc.; Thales S.A.; Airbus Defence and Space; Booz Allen Hamilton Holding Corp.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Defense Cybersecurity Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global defense cybersecurity market report based on component, deployment mode, solution, security type, end-use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Deployment Mode Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premises

-

Cloud

-

-

Solution Outlook (Revenue, USD Billion, 2021 - 2033)

-

Threat Evaluation and Vulnerability Management

-

Identity and Access Management (IAM)

-

Content/Data Security

-

Managed Security Solutions

-

Risk and Compliance Management

-

Cyber Threat Protection

-

-

Security Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Network Security

-

Endpoint Security

-

Application Security

-

Cloud Security

-

Infrastructure Security

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Land Forces

-

Naval Forces

-

Air Forces

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global defense cybersecurity market size was estimated at USD 30.49 billion in 2024 and is expected to reach USD 33.25 billion in 2025.

The global defense cybersecurity market is expected to grow at a compound annual growth rate of 11.4% from 2025 to 2033 to reach USD 78.85 billion by 2033.

The cyber threat protection segment accounted for the largest revenue share of 37.54% in 2024 by solution, propelled by the critical need for proactive defense against sophisticated, persistent cyber threats targeting military infrastructure and weapon systems.

Some key players operating in the defense cyber security market include BAE Systems plc, CACI International Inc., General Dynamics Corporation, IBM Corporation, Leidos Holdings Inc., Lockheed Martin Corporation, L3Harris Technologies Inc., Northrop Grumman Corporation, Palantir Technologies Inc., QinetiQ Group plc, Raytheon Technologies Corporation, SAIC Inc., Thales S.A., Airbus Defence and Space, Booz Allen Hamilton Holding Corp. and Others.

Factors such as the increasing invest in cybersecurity by nation-states, defense agencies, and military to counter a growing wave of nation-sponsored cyberattacks, zero-day exploits, and advanced persistent threats (APTs) plays a key role in accelerating the defense cyber security market.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.