- Home

- »

- Next Generation Technologies

- »

-

Edge Artificial Intelligence Chips Market Report, 2026-2033GVR Report cover

![Edge Artificial Intelligence Chips Market (2026 - 2033)Report]()

Edge Artificial Intelligence Chips Market (2026 - 2033)

Size, Share & Trends Analysis Report By Chipset (CPU, GPU, ASIC), By Function (Training, Inference), By Device (Consumer, Enterprise), By Region (North America, Europe, Asia Pacific, Latin America, MEA), And Segment Forecasts

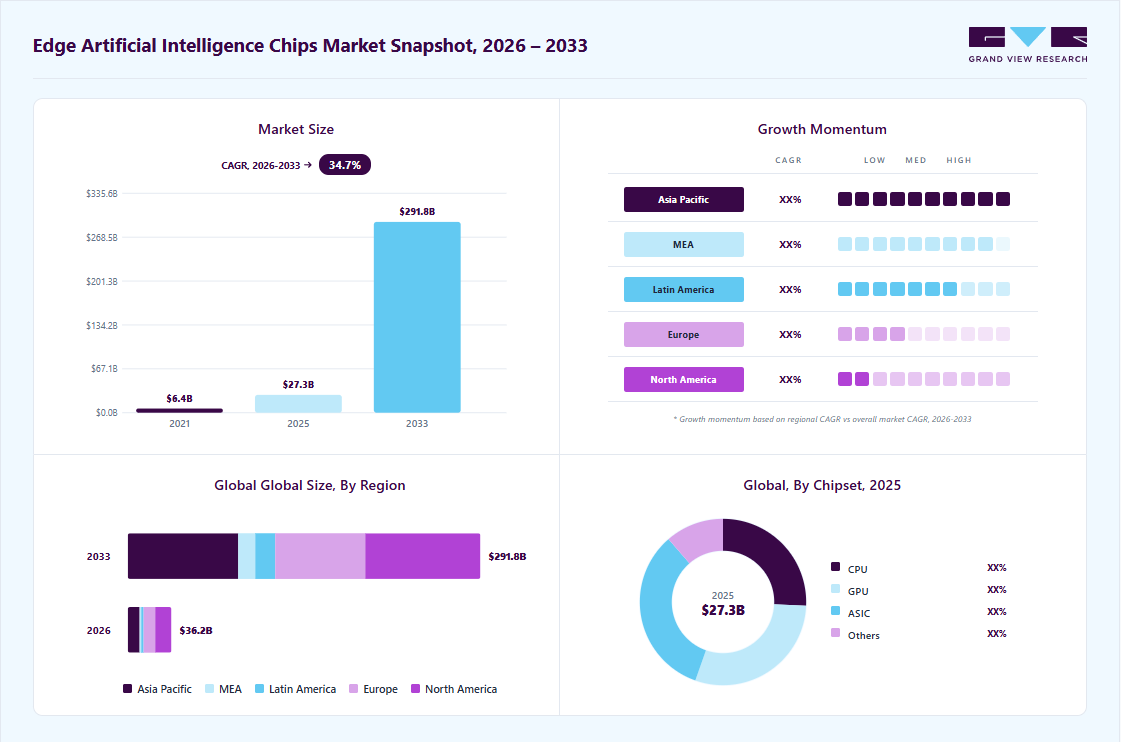

Market Size, 2025

$27.3BMarket Estimate, 2026

$36.2BMarket Forecast, 2033

$291.8BCAGR, 2026–2033

34.7%Edge Artificial Intelligence Chips Market Summary

The global edge artificial intelligence chips market size was valued at USD 27.3 billion in 2025 and is projected to grow from USD 36.2 billion in 2026 to USD 291.8 billion by 2033, at a CAGR of 34.7% from 2026 to 2033. North America dominated the global market with the largest revenue share of 37.7% in 2025. The increasing use of e-commerce platforms and social media is generating a vast amount of data.

Key Market Trends & Insights

- By chipset: ASIC segment dominated the market with a revenue share of 33.2% in 2025.

- By function: Inference segment held the largest market share of 86.5% in 2025.

- By device: Consumer devices segment has a significant revenue share of 65.3% in 2025.

Regional Highlights

- Largest regional market: North America (37.7% revenue share, 2025)

- Fastest growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The edge artificial intelligence chips market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market size in 2025: USD 27.3 Billion

- Estimated market size in 2026: USD 36.2 Billion

- Projected market size by 2033: USD 291.8 Billion

- CAGR (2026-2033): 34.7%

The market is gaining significant momentum driven by the rapid expansion of edge computing, AI inference, computer vision, 5G connectivity, and smart devices, as organizations increasingly deploy advanced chipsets to enable faster data processing, improved operational intelligence, and enhanced autonomous decision-making at the network edge.Artificial intelligence chips are addressing this need by enabling quicker processing. A major trend in chip technology is the implementation of edge-based AI, which involves running AI processes on a device instead of a remote server. This approach offers faster speed and better privacy. The growing interest in Internet of Things (IoT) devices is a key factor driving tech companies to invest in developing high-speed processors.

")

Edge artificial intelligence chips eliminate or reduce the need to transmit bulk data to data centers or cloud stations. Thus, these chips offer numerous benefits for speed, usability, and data privacy & security by locally enabling processor-intensive machine learning computations. However, for some applications, not all machine learning-related tasks have to occur locally, and transmitting data by a remote AI array for processing is preferred. For instance, data center usage is preferred for applications involving data in large volumes, such as online video streaming.

The AI-related application technologies for edge computing are intelligent robots, autonomous vehicles, and smart hardware. Artificial intelligence-supported edge computing technology is multifaceted as it runs through the algorithm mechanism, application, processor type, and computing technology. The primary applications that run over edge AI are related to image/video, sound and speech, natural language processing, device control, and high-volume computing.

Market Dynamics

The edge artificial intelligence chips market is expanding rapidly, supported by the increasing deployment of edge analytics, distributed computing, and intelligent endpoints across multiple industries. Rising demand for on-device intelligence, data localization, and autonomous processing is strengthening market adoption. However, challenges related to advanced node fabrication, chip verification, and silicon development costs continue to limit scalability for some participants. At the same time, emerging investments in network virtualization, connected ecosystems, and digital transformation initiatives are creating new growth avenues. Ongoing innovations in semiconductor technologies and AI hardware optimization are expected to support sustained market development.

The growing implementation of edge analytics solutions across industrial and commercial environments is a key driver supporting market growth. Enterprises are increasingly deploying intelligent endpoints to process information closer to data sources and improve operational responsiveness. The demand for on-device intelligence is rising as organizations seek faster execution of AI workloads without relying on centralized cloud platforms. This trend is encouraging investments in specialized chip architectures designed to deliver higher computational efficiency. Consequently, manufacturers are expanding their portfolios to address the growing need for localized AI processing capabilities.

The expansion of distributed computing environments is further accelerating demand for advanced edge AI chips. Businesses are integrating sensor fusion technologies and embedded AI systems to enhance automation, monitoring, and predictive decision-making functions. Growing utilization of industrial IoT platforms is creating additional requirements for low-power and high-performance semiconductor solutions. Furthermore, increasing deployment of machine vision applications across manufacturing and logistics sectors is supporting chipset adoption. These developments are expected to reinforce long-term demand for edge AI hardware across diverse end-use industries.

The edge artificial intelligence chips market faces challenges associated with advanced node fabrication and increasingly sophisticated design requirements. Developing high-performance processors requires substantial investment in electronic design automation (EDA) tools, engineering expertise, and testing infrastructure. The growing complexity of chip verification processes often extends product development timelines and increases commercialization risks. Additionally, maintaining performance efficiency while reducing power consumption remains a critical challenge for manufacturers. These factors can limit the pace of innovation and market entry for emerging companies.

Rising silicon development costs continue to create financial pressures across the semiconductor value chain. Companies must allocate significant resources toward wafer processing, packaging technologies, and manufacturing optimization initiatives. Dependence on advanced fabrication facilities can also increase exposure to supply-side constraints and production bottlenecks. Moreover, evolving AI workloads require continuous architectural upgrades, adding further complexity to product development strategies. As a result, cost-intensive development cycles remain a key restraint for market participants.

The increasing adoption of network virtualization technologies is creating substantial growth opportunities for edge AI chip providers. Organizations are investing in intelligent infrastructure capable of supporting real-time data processing across highly connected environments. Growing deployment of private 5G networks is enabling faster communication between devices and enhancing the effectiveness of AI-enabled applications. This shift is generating demand for advanced processors optimized for low-latency and high-throughput operations. Consequently, semiconductor vendors are focusing on developing solutions tailored to next-generation connectivity requirements.

The emergence of connected ecosystems across automotive, healthcare, retail, and industrial sectors is further expanding market potential. Businesses are leveraging digital transformation initiatives to improve operational visibility, resource utilization, and customer engagement. Increasing integration of autonomous systems, smart surveillance platforms, and predictive maintenance solutions is creating new application areas for edge AI hardware. Furthermore, advancements in neuromorphic computing and AI acceleration engines are opening opportunities for enhanced performance and energy efficiency. These trends are expected to support sustained investment and innovation throughout the edge artificial intelligence chips market.

Market Concentration & Characteristics

The Edge Artificial Intelligence Chips Market demonstrates a moderately concentrated and technology-driven competitive landscape, supported by the presence of semiconductor manufacturers, AI accelerator providers, processor developers, and edge computing solution vendors. Market participants compete by offering advanced chip architectures capable of delivering low-latency processing, high computational efficiency, and real-time AI inference at the network edge. The increasing adoption of edge computing, machine learning, computer vision, and IoT-enabled devices is expanding the competitive environment and driving continuous product innovation. As enterprises accelerate investments in intelligent automation and connected infrastructure, companies are strengthening their semiconductor portfolios to enhance market competitiveness.

The market is characterized by rapid advancements in AI accelerators, neural processing units (NPUs), application-specific integrated circuits (ASICs), and energy-efficient processing technologies, creating substantial opportunities for differentiation. Companies are focusing on developing high-performance edge AI solutions that support autonomous systems, predictive analytics, and next-generation smart devices across diverse industries. Strategic investments in semiconductor research, advanced packaging technologies, and AI optimization capabilities are shaping competitive dynamics and accelerating technological development. Furthermore, the growing demand for localized intelligence, enhanced data privacy, and real-time decision-making across automotive, healthcare, industrial automation, and consumer electronics sectors continues to support sustained market expansion and innovation.

Analyst Perspective

The edge artificial intelligence chips market is witnessing strong growth driven by the increasing adoption of edge computing, AI inference, computer vision, and real-time data processing across connected devices and intelligent systems. Rising demand for low-latency computing, AI accelerators, and energy-efficient semiconductor architectures is encouraging continuous innovation in chipset design and performance optimization. The expansion of 5G networks, Internet of Things (IoT) ecosystems, and autonomous technologies is further accelerating the deployment of edge AI solutions across diverse industries. Market participants are investing in advanced neural processing units (NPUs), application-specific integrated circuits (ASICs), and embedded AI technologies to address evolving enterprise and consumer requirements. As organizations increasingly prioritize localized intelligence, enhanced data privacy, and operational efficiency, the market is expected to experience sustained growth and technological advancement throughout the forecast period.

Chipset Insights

Based on chipset, the ASIC segment led the market with the largest revenue share of 33.2% in 2025. CPU chipsets have long been the cornerstone of general-purpose computing, offering a versatile and well-established architecture. Their ability to handle a wide range of tasks, including sequential and parallel processing, and their widespread availability and compatibility with existing software ecosystems make them an attractive choice for many edge AI applications. In addition, continuous advancements in CPU technology, such as increased core counts and improved performance per watt, have further solidified their position in the market.

ASIC chipset is expected to register the fastest CAGR of 47.2% during the forecast period due to its exceptional performance and efficiency. The surge in demand for AI applications in different sectors, such as autonomous vehicles, healthcare, and smart cities, creates a need for custom hardware to provide real-time insights at the edge. ASICs, designed for AI tasks, provide better computing power, lower latency, and reduced energy usage compared to CPUs designed for general use. ASICs are the favored option for edge AI deployments due to their various benefits, leading to their rapid expansion in the edge AI chips market.

Device Insights

Based on device, the consumer devices segment has a significant revenue share of 65.3% in 2025, which is primarily attributed to the widespread adoption of AI-powered devices in everyday life. Consumer electronics such as smartphones, smart speakers, and laptops increasingly incorporate AI features, such as natural language processing, image recognition, and personalized recommendations, to improve user experiences. The rise in popularity of these gadgets, along with the incorporation of AI capabilities, has led to a surge in the requirement for edge AI chips capable of effectively managing the computing needs of consumer applications. The increase in demand has strengthened the segment position in the market.

The enterprise devices segment is projected to grow at the fastest CAGR over the forecast period. The rising adoption of AI in business applications fuels the need for specific edge AI chips that can provide immediate insights and enhance operational efficiency. Moreover, the increasing focus on data privacy and security motivates businesses to implement AI solutions at the edge, minimizing the requirement to send confidential information to the cloud. The rise in cost-effective and powerful edge AI hardware is fueling the rapid growth of the enterprise devices segment.

Function Insights

Based on function, inference segment led the market with the largest revenue share of 86.5% in 2025, due to the increasing demand for instant decision-making and data analysis at the edge. With the growth of AI technology in industries, there is a significant demand for chips capable of processing and analyzing data locally without relying on cloud-based systems. Inference functions involve trained AI models to make predictions or classifications based on new data, which is essential for enabling these edge AI applications. The growing complexity and variety of AI models and the strict latency needs of edge applications are fueling the need for high-performance inference chips, strengthening their dominance in the market.

The training function is expected to register the fastest CAGR during the forecast period. The increasing complexity and size of AI models, along with the growing emphasis on on-device learning and privacy, drive the need for edge devices capable of locally training AI models. Furthermore, progress in hardware technologies, such as dedicated neural processing units (NPUs), allows more effective and affordable training on edge devices. As edge AI applications continue to evolve and become more sophisticated, the demand for training capabilities at the edge is expected to surge, propelling the growth of this segment.

Regional Insights

North America dominated the Edge Artificial Intelligence Chips market with the largest revenue share of 37.7% in 2025. The region boasts a strong presence of leading technology companies and research institutions, driving innovation and development in AI technologies. In addition, the high adoption of AI-driven devices and applications in the automotive, healthcare, and manufacturing industries has created a significant demand for edge AI chips. Furthermore, the favorable regulatory environment and substantial investments in AI research and development have further contributed to the edge AI chips market growth.

U.S. Edge Artificial Intelligence Chips Market Trends

The Edge Artificial Intelligence Chips market in the U.S. held the largest share in the North America region in 2025, due to the country's robust environment for AI development and innovation and the presence of top technology companies and research institutions. These businesses have made substantial investments in research and development, resulting in progress in edge AI chip technology and structure. Moreover, the crucial growth of the market has been driven by the U.S. government's strong support for AI projects, which includes financial support for research and development.

Europe Edge Artificial Intelligence Chips Market Trends

Europe edge artificial intelligence chips market was identified as a lucrative region in 2023. The increasing adoption of AI technologies across various industries and a focus on data privacy and security have driven the demand for edge AI solutions. In addition, leading technology companies and research institutions in countries such as Germany, France, and the UK have fostered innovation and development in this field. Moreover, government initiatives and investments in AI research and infrastructure have further contributed to the region's growth potential in the edge AI chips market.

The edge artificial intelligence chips market in UK is expected to grow rapidly in the coming years due to the growing utilization of Internet of Things (IoT) devices in different sectors such as smart homes, factories, healthcare, and transportation, which is creating a large amount of data that needs to be processed quickly and on-site. The increasing need for autonomous systems, such as self-driving cars and drones, necessitates high-performance edge AI chips for instant decision-making and object detection.

Asia Pacific Edge Artificial Intelligence Chips Market Trends

Asia Pacific edge artificial intelligence chips market is anticipated to grow with the fastest CAGR over the forecast period. The growing population, increasing digitalization, and economic growth drive a surge in demand for AI-driven applications. Furthermore, support from governments and funding for AI research and infrastructure, especially in countries such as China and India, create a conducive setting for advancing edge AI technologies. In addition, the strong manufacturing capabilities and cost benefits make it an appealing location for AI chip production and deployment, further enhancing its potential for robust growth.

China edge artificial intelligence chips market held a substantial market share in 2023 owing to the country's significant investments in AI research and development and prioritizing domestic technology independence, which has driven the expansion of AI chip production and utilization. Moreover, the increasing Chinese market for AI-driven applications, especially in surveillance, smart cities, and industrial automation sectors, has generated a high need for edge AI chips. Moreover, government support, policies, and strategies to encourage AI innovation and growth have also played a role in solidifying China's growth in this industry.

Key Edge Artificial Intelligence Chips Company Insights

Some key companies in the edge artificial intelligence chips market include Advanced Micro Devices, Inc., Alphabet Inc., Intel Corporation, Qualcomm Technologies, Inc., Apple Inc., Mythic, and others. Organizations focus on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions and partnerships with other major companies.

-

Advanced Micro Devices, Inc. is a semiconductor company that designs, manufactures, and sells microprocessors, graphics processing units (GPUs), and other computing technologies. The company has a significant presence in the edge AI chip market, offering products well-suited for this segment's unique requirements.

-

Intel Corporation is a global leader in semiconductors and is renowned for its x86 processors. While mainly known for traditional computing, Intel has also played an active role in the AI chip market. The company created various AI-optimized processors and accelerators to meet AI applications' complex computational needs.

Key Edge Artificial Intelligence Chips Companies

The following key companies have been profiled for this study on the edge artificial intelligence chips market.

-

Advanced Micro Devices, Inc.

-

Alphabet Inc.

-

Intel Corporation

-

Qualcomm Technologies, Inc.

-

Apple Inc.

-

Mythic

-

Arm Limited

-

Samsung

-

NVIDIA Corporation

-

Huawei Technologies Co., Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., Advanced Micro Devices, Inc. (AMD), Samsung Electronics Co., Ltd.

- Mature players focus on expanding AI accelerators, edge AI platforms, graphics processing units (GPUs), neural processing units (NPUs), and high-performance inference processors to strengthen their market presence. They are increasing investments in advanced semiconductor design, edge computing ecosystems, and strategic partnerships to support large-scale AI deployments.

- Their competitive advantage is derived from strong global distribution networks, extensive semiconductor expertise, broad product portfolios, established customer relationships, and substantial R&D investments. Their ability to deliver scalable and high-performance AI processing solutions further reinforces market leadership.

- These companies may encounter challenges related to rising fabrication costs, supply chain complexities, technology transition requirements, and regulatory pressures affecting semiconductor operations.

Emerging Players: Mythic, Arm Limited, Huawei Technologies Co., Ltd., Alphabet Inc., Apple Inc.

- Emerging players focus on advancing edge inference technologies, low-power AI chipsets, on-device intelligence, custom silicon architectures, and application-specific AI processors to capitalize on evolving market opportunities. They emphasize innovation-driven product development and targeted deployment across high-growth edge AI applications.

- Their strength comes from specialized technological capabilities, innovative processor architectures, strong software-hardware integration, and the ability to address niche AI workloads with optimized performance and efficiency.

- Limited market penetration in certain regions, lower manufacturing scale, geopolitical constraints, and dependence on ecosystem partnerships may restrict expansion relative to established semiconductor leaders.

Recent Developments

-

In June 2024, Intel revealed innovative technologies and structures expected to greatly speed up the AI environment in various areas such as the data center, cloud, network, edge, and PC. With increased processing capabilities, cutting-edge energy efficiency, and a reduced total cost of ownership (TCO), customers can now take full advantage of the AI system opportunity.

-

In June 2024, Advanced Micro Devices, Inc. announced the launch of the latest AMD Ryzen AI 300 Series processors, presenting a Neural Processing Unit (NPU) for upcoming AI PCs and next-generation AMD Ryzen 9000 Series processors for desktop computers. These processors will enhance performance for content creators, gamers, and prosumers.

Edge Artificial Intelligence Chips Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 27.3 billion

Estimated market size in 2026

USD 36.2 billion

Projected market size by 2033

USD 291.8 billion

Growth rate

CAGR of 34.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Chipset, function, device, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

Advanced Micro Devices, Inc.; Alphabet Inc.; Intel Corporation; Qualcomm Technologies, Inc.; Apple Inc.; Mythic; Arm Limited; Samsung; NVIDIA Corporation; Huawei Technologies Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Edge Artificial Intelligence Chips Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global edge artificial intelligence chips market report based on chipset, function, device, and region.

-

Chipset Outlook (Revenue, USD Million, 2021 - 2033)

-

CPU

-

GPU

-

ASIC

-

Others

-

-

Function Outlook (Revenue, USD Million, 2021 - 2033)

-

Training

-

Inference

-

-

Device Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer Devices

-

Enterprise Devices

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Chipset

Revenue capture definition

CPU

The CPU segment comprises central processing units that execute general-purpose computing tasks, system control functions, and AI workloads within edge devices. Revenue is generated from the sale of processors integrated into consumer electronics, industrial equipment, automotive systems, and enterprise edge computing platforms.

GPU

This GPU segment includes graphics processing units designed to accelerate parallel computing, machine learning algorithms, and AI inference operations at the edge. Revenue capture covers GPU chip sales deployed in autonomous systems, intelligent cameras, robotics, and high-performance edge computing applications.

ASIC

The ASIC segment consists of application-specific integrated circuits developed to perform dedicated AI functions with enhanced efficiency and lower power consumption. Revenue is derived from custom and purpose-built AI chips utilized in edge inference, computer vision, and specialized intelligent processing environments.

Others

Others segment includes FPGAs, NPUs, VPUs, and other specialized processors designed for edge artificial intelligence applications. Revenue includes sales of alternative AI acceleration technologies deployed across diverse edge computing and intelligent device ecosystems.

Segment - Function

Revenue capture definition

Training

The Training segment includes chipsets utilized for developing, optimizing, and refining artificial intelligence and machine learning models before deployment. Revenue is generated from processors supporting data-intensive training workloads across enterprise, cloud-edge, research, and industrial environments.

Inference

This Inference segment comprises chipsets that execute trained AI models and generate real-time outputs directly on edge devices. Revenue capture includes processors deployed in applications requiring low-latency decision-making, predictive analytics, computer vision, and intelligent automation.

Segment - Device

Revenue capture definition

Consumer Devices

The consumer devices segment covers edge AI chips integrated into smartphones, wearables, smart home devices, personal electronics, and entertainment systems. Revenue is generated from semiconductor sales that enable on-device intelligence, voice recognition, image processing, and personalized user experiences.

Enterprise Devices

Enterprise devices includes edge AI chipsets deployed within industrial machinery, healthcare equipment, telecommunications infrastructure, connected vehicles, surveillance systems, and enterprise-grade hardware. Revenue capture encompasses processor sales supporting business-critical applications, operational automation, and real-time data analytics across commercial environments.

Estimation Model

Layer Name

Key Questions

Description

AI-Enabled Device Adoption Layer

Who creates demand for Edge Artificial Intelligence Chips?

Identify enterprises, consumers, industrial operators, automotive manufacturers, healthcare providers, and technology companies deploying AI-enabled devices. This layer establishes the demand base by assessing the adoption of smart devices, connected systems, intelligent sensors, and edge computing applications across key industries.

Semiconductor Infrastructure & Edge Computing Investment Layer

Who invests in edge AI processing infrastructure?

Apply investment rates in semiconductor technologies, edge computing platforms, AI accelerators, data processing infrastructure, and intelligent hardware ecosystems. This layer measures spending that supports localized AI computation, real-time analytics, and low-latency processing capabilities.

Edge AI Chip Deployment Layer

Who deploys Edge Artificial Intelligence Chips solutions?

Apply penetration rates of CPUs, GPUs, ASICs, NPUs, machine vision processors, autonomous systems, and AI-enabled edge devices. This layer captures the deployment of chipsets that enable AI inference, computer vision, predictive analytics, and intelligent automation at the network edge.

Edge Artificial Intelligence Chips Market Revenue Realization Layer

How much revenue is generated through Edge Artificial Intelligence Chips adoption?

Estimate market revenue by combining chipset deployments with spending on semiconductor components, AI processors, hardware integration, software optimization, support services, and platform enhancements. This layer captures total revenue generated from the commercialization and expansion of edge AI chip technologies across end-use industries.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Edge Artificial Intelligence Chips Technology Adoption & Growth Assessment

Performed an in-depth assessment of adoption trends related to edge computing, AI inference, Internet of Things (IoT), 5G connectivity, machine learning, and AI accelerators across major industry verticals.

Helps stakeholders identify emerging growth areas, evaluate technology adoption trends, optimize investment strategies, and strengthen competitive positioning within the Edge Artificial Intelligence Chips market.

Industry-Specific Edge Artificial Intelligence Chips Deployment Analysis

Analyzed the deployment of Edge AI chip solutions across automotive, healthcare, consumer electronics, industrial automation, telecommunications, retail, and other end-use industries, including intelligent automation and real-time analytics applications.

Provides actionable insights into industry-specific demand patterns, deployment requirements, market opportunities, and long-term growth prospects to support strategic business planning.

AI Acceleration, Intelligent Edge Computing & Semiconductor Innovation Opportunity Assessment

Evaluated growth opportunities associated with AI accelerators, embedded AI, computer vision, neuromorphic computing, low-power processors, and advanced edge intelligence technologies across global markets.

Supports innovation planning, product development strategies, technology differentiation initiatives, and expansion into high-growth application segments within the Edge Artificial Intelligence Chips ecosystem.

Frequently Asked Questions About This Report

The global edge AI chips market size was estimated at USD 27.3 billion in 2025 and is expected to reach USD 36.2 billion in 2026.

Asia Pacific is the fastest-growing region over the forecast period.

Consumer devices segment has a significant revenue share of 65.3% in 2025.

The global edge AI chips market is expected to grow at a compound annual growth rate of 34.7% from 2026 to 2033 to reach USD 291.8 billion by 2033.

North America dominated the edge AI chips market with a share of 37.7% in 2025. The region boasts a strong presence of leading technology companies and research institutions, driving innovation and development in AI technologies.

ASIC segment dominated the market with a revenue share of 33.2% in 2025.

Inference segment held the largest market share of 86.5% in 2025.

Some key players operating in the edge AI chips market include Advanced Micro Devices, Inc.; Alphabet Inc.; Intel Corporation; Qualcomm Technologies, Inc.; Apple Inc.; Mythic; Arm Limited; Samsung; NVIDIA Corporation; Huawei Technologies Co., Ltd.

The market is gaining significant momentum driven by the rapid expansion of edge computing, AI inference, computer vision, 5G connectivity, and smart devices,

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.