- Home

- »

- Advanced Interior Materials

- »

-

Electrochemical Processing In Mining Market Report, 2025-2033GVR Report cover

![Electrochemical Processing In Mining Market (2025 - 2033)Report]()

Electrochemical Processing In Mining Market (2025 - 2033)

Size, Share & Trends Analysis Report By Process Type (Electrowinning, Electrorefining), By Metals Recovered (Base Metals, Precious Metals), By Region, And Segment Forecasts

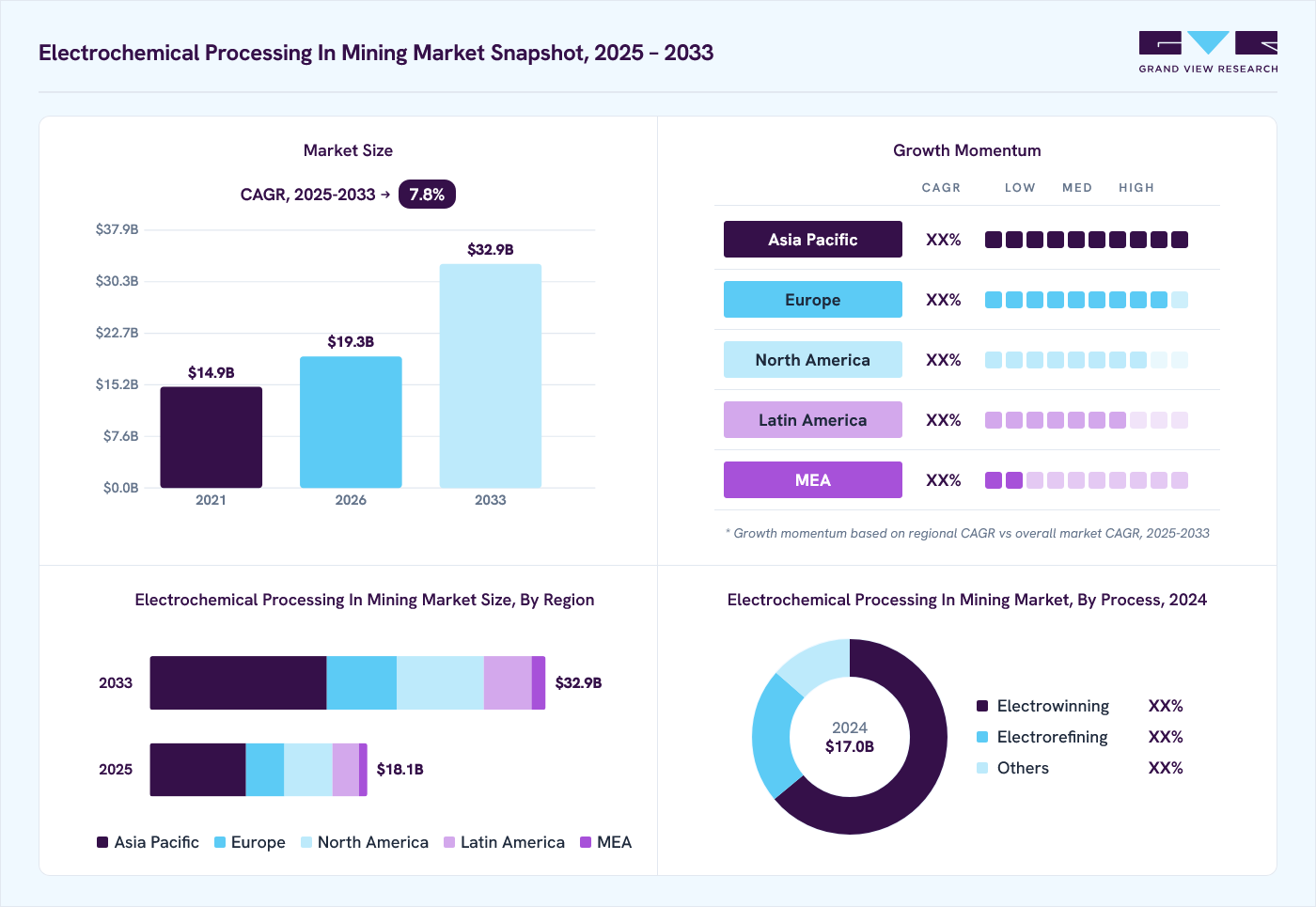

Market Size, 2024

$17.0BMarket Estimate, 2026

$19.3BMarket Forecast, 2033

$32.9BCAGR, 2025–2033

7.8%Electrochemical Processing In Mining Market Summary

The global electrochemical processing in mining market size was valued at USD 17.0 billion in 2024 and is projected to grow from USD 19.3 billion in 2026 to USD 32.9 billion by 2033, at a CAGR of 7.8% from 2025 to 2033. Asia Pacific dominated the market, accounting for a revenue share of 44.2% in 2024. The market growth is driven by the rising demand for critical minerals such as base metals, critical metals, and cobalt, coupled with the shift toward sustainable, low-emission metal extraction technologies.

Key Market Trends & Insights

- Asia Pacific dominated the electrochemical processing in mining market with a revenue share of 44.2% in 2024.

- The electrochemical processing in mining industry in Asia Pacific is expected to grow at a substantial CAGR of 7.9% from 2025 to 2033.

- By process type, the electrowinning segment dominated the market with a revenue share of over 64.0% in 2024.

- In 2024, the base metals segment held the largest market share of over 71.0% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 17.03 Billion

- 2033 Projected Market Size: USD 32.94 Billion

- CAGR (2025-2033): 7.8%

- Asia Pacific: Largest Market in 2024

Advancements in electrowinning and electrorefining, along with government initiatives to strengthen mineral security and reduce import dependency, further accelerate the adoption of electrochemical processing in mining. Sustainability and responsible mining practices are becoming central to market expansion. Companies and governments focus on energy-efficient operations, ethical sourcing, and traceable supply chains to minimize carbon footprints and align with Environmental, Social, and Governance (ESG) standards. Additionally, integrating recycled and secondary materials through circular economic initiatives reduces reliance on virgin ores and promotes resource efficiency, positioning electrochemical processing as a key enabler of sustainable metal production.")

The electrochemical processing in mining industry’s growth is further driven by technological advancements that enhance process efficiency, lower operational costs, and enable recovery from complex ore streams and waste solutions. Supportive government policies and strategic initiatives to secure critical minerals and reduce import dependency are boosting adoption across major regions, including the Asia Pacific, Latin America, and North America. As demand for critical metals grows alongside global energy transitions, electrochemical processing is emerging as a strategic, environmentally responsible, and commercially viable solution for the mining industry.

Drivers, Opportunities & Restraints

The increasing demand for critical metals, such as base metals, propels the adoption of electrochemical processing methods. These metals are essential for renewable energy technologies, electric vehicles, and electronics. For instance, China's investment in advanced electrowinning technologies has significantly boosted its base metals production efficiency, aligning with its green energy initiatives. Electrochemical methods like electrowinning and electrorefining offer high-purity outputs and reduced environmental impact compared to traditional pyrometallurgical processes, making them crucial for meeting the growing demand in these sectors.

Advancements in electrochemical technologies present opportunities for enhanced metal recovery from complex ores and waste streams. A notable example is the development of electrodialysis processes for efficient water treatment in mining operations, which not only recovers valuable metals but also addresses environmental concerns. These innovations enable the mining industry to process lower-grade ore and recycle materials, reducing waste and improving resource efficiency. Integrating renewable energy sources with electrochemical processes further enhances sustainability and operational cost-effectiveness.

High capital investment and operational costs associated with electrochemical processing technologies can hinder adoption, especially in regions with limited financial resources. For example, smaller mining operations in developing countries may struggle to implement such advanced technologies due to budget constraints. Additionally, the complexity of integrating these systems into existing infrastructure and the need for specialized workforce training can further impede widespread adoption. Overcoming these challenges requires targeted investments, government support, and capacity-building initiatives.

Process Type Insights

By process type, electrowinning dominated the market with a revenue share of over 64.0% in 2024. Electrowinning and electrorefining remain dominant in the global electrochemical processing market due to their large-scale efficiency in extracting and purifying metals. Other processes, such as electrodialysis and electrocoagulation, are increasingly adopted for wastewater treatment, selective recovery, and complex or low-grade ores processing. These methods enable mining operations to improve yield, maintain consistent product quality, and minimize environmental impact, forming the backbone of modern and sustainable extraction practices.

The market is experiencing steady growth driven by the increasing demand for critical minerals across sectors such as renewable energy, electric mobility, and advanced manufacturing. Electrochemical processing is prioritized for its ability to enhance resource efficiency, ensure supply stability, and reduce reliance on traditional extraction methods. Technological innovations and energy-efficient and sustainable practices improve process performance and environmental compliance, making electrochemical methods a strategic solution for long-term industrial resilience and resource security.

Metals Recovered Insights

In 2024, the base metals segment held the largest share, over 71.0% of electrochemical processing in mining revenue. The global electrochemical processing industry’s growth continues to be driven by the strong demand for base metals, which remain the most significant contributor due to their extensive use in industrial and infrastructure applications. Electrochemical processes-particularly electrowinning and electrorefining-enable efficient extraction and the production of high-purity metals, meeting the stringent quality requirements of various industrial sectors. Ongoing advancements in process efficiency and energy optimization enhance metal recovery rates, supporting a consistent supply and long-term market growth.

Precious metals represent another key segment experiencing steady expansion, fueled by their diverse industrial applications and growing use in alloy manufacturing. Electrochemical processing of precious metals offers notable advantages compared to conventional methods, including high yield, reduced energy consumption, and improved environmental compliance. Furthermore, innovations that enable recovery from lower-grade ores and secondary resources reflect an increasing focus on resource efficiency and sustainable production practices.

Critical and emerging metals are also gaining prominence, driven primarily by the rapid expansion of the electric vehicle and renewable energy sectors. Electrochemical techniques facilitate the selective recovery and purification of these metals, making them essential for applications such as battery production and advanced manufacturing. The market is witnessing a strategic shift toward high-demand, high-value metals, underpinned by technological innovation, sustainability goals, and the growing need for secure and efficient global metal supply chains.

Regional Insights

Asia Pacific dominated the electrochemical processing in mining market with a revenue share of 44.2% in 2024. Asia Pacific continues to lead the global electrochemical processing market, fueled by rapid industrialization, increasing energy transition demands, and strong government support for strategic mineral reserves. Nations including China, India, and South Korea actively invest in electrochemical processing infrastructure to secure domestic supplies of lithium, cobalt, critical metals, and rare earth elements. These measures strengthen supply chain security and promote sustainable extraction and processing practices in line with growing regional and global environmental standards.

North America Electrochemical Processing In Mining Market Trends

The North America electrochemical processing industry is experiencing significant growth, driven by the increasing demand for critical minerals essential for defense, clean energy, and high-tech industries. Governments invest in domestic processing capabilities to reduce reliance on foreign suppliers and enhance supply chain resilience. For instance, the U.S. Department of Defense has allocated USD 20 million to establish a cobalt refinery in Ontario, Canada, to secure a stable supply chain for cobalt, a crucial material for electric vehicle batteries, electronics, and military hardware.

States like Oklahoma are positioning themselves as critical mineral processing hubs in the United States. The state hosts facilities for lithium refining, battery recycling, rare earth magnet production, and electronic waste recycling. These initiatives are part of a broader strategy to support battery and EV supply chains and reduce dependence on foreign sources.

Europe Electrochemical Processing In Mining Market Trends

Europe is accelerating the development of electrochemical processing capabilities to support its green energy transition and reduce dependence on external sources for critical minerals. The European Union has launched 47 strategic projects across 13 countries focused on extracting, processing, and recycling essential metals like aluminium, base metals, critical metals, lithium, and rare earth elements. These initiatives aim to enhance regional resource self-sufficiency, foster sustainable practices, and strengthen the competitiveness of Europe’s clean energy, defense, and high-tech industries.

Key Electrochemical Processing In Mining Company Insights

Some of the key players operating in the market include Albemarle Corporation, Ganfeng Lithium, and Tianqi Lithium.

-

Albemarle Corporation, established in 1994 and headquartered in Charlotte, North Carolina, USA, is a leading producer of lithium and other specialty chemicals, focusing on electrochemical processing for battery materials. The company operates primary lithium extraction and refining projects in Chile, the USA, and Australia, supporting the growing demand for electric vehicles, energy storage systems, and renewable technologies. Albemarle emphasizes sustainability, advanced processing methods, and partnerships with local communities to ensure efficient resource utilization and long-term supply security.

-

Ganfeng Lithium, established in 2000 and headquartered in Xinyu, China, specializes in lithium production, electrochemical processing, and battery material supply. The company’s key projects, including operations in Argentina, Australia, and China, aim to provide high-purity lithium for electric vehicles, energy storage, and clean energy solutions. Ganfeng Lithium invests in research and development, environmental sustainability, and technological innovation to improve efficiency, reduce environmental impact, and secure a reliable global lithium supply.

-

Tianqi Lithium, established in 1995 and headquartered in Chengdu, China, is a major lithium producer focused on electrochemical extraction and refining technologies. The company’s projects include the Greenbushes lithium mine in Australia and lithium hydroxide plants in China, catering to the growing global demand for EV batteries and renewable energy storage. Tianqi Lithium emphasizes responsible mining, advanced processing technologies, and collaboration with industrial partners to enhance resource efficiency and ensure sustainable supply chains.

Key Electrochemical Processing In Mining Companies:

The following are the leading companies in the electrochemical processing in mining market. These companies collectively hold the largest market share and dictate industry trends.

- Albemarle Corporation

- Freeport-McMoRan Inc.

- Ganfeng Lithium

- Glencore Plc

- Hydroleap

- Ma’aden (Saudi Arabian Mining Company)

- Rio Tinto Group

- Southern Base Metals Corporation

- Tianqi Lithium

- Yasa ET (Shanghai) Co., Ltd.

Recent Developments

-

Rio Tinto Group announced in August 2025 a USD 6.7 billion acquisition of Arcadium Lithium, expanding its lithium production portfolio to support global EV and renewable energy supply chains. The acquisition includes lithium brine and spodumene projects, enhancing Rio Tinto’s capacity for sustainable lithium extraction and electrochemical processing while advancing environmental and community stewardship initiatives.

-

Albemarle Corporation inaugurated a new lithium hydroxide plant in Nevada, USA, in July 2025, increasing domestic lithium refining capacity to meet the growing demand for electric vehicle batteries. The facility integrates advanced electrochemical processing technologies to optimize lithium purity, reduce energy consumption, and support environmentally responsible production practices.

-

Ganfeng Lithium signed a strategic partnership in September 2025 with a European battery manufacturer to supply high-purity lithium hydroxide sourced through electrochemical processing. This collaboration aims to secure a stable lithium supply for EV production and energy storage projects while promoting sustainable mining and resource efficiency.

Electrochemical Processing In Mining Report Scope

Report Attribute

Details

Market size in 2024

USD 17.0 billion

Estimated Market size in 2026

USD 19.3 billion

Projected Market size by 2033

USD 32.9 billion

Growth rate

CAGR of 7.8% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Process type, metals recovered, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK.; Italy; China; India; Japan; South Korea; Brazil; South Africa

Key companies profiled

Albemarle Corporation; Freeport-McMoRan Inc.; Ganfeng Lithium; Glencore Plc; Hydroleap; Ma’aden; Rio Tinto Group; Southern Base Metals Corporation; Tianqi Lithium; Yasa ET Co., Ltd.

Market Definition

The electrochemical processing in mining market represents the value of metals recovered through processes like electrowinning, electrorefining, and recovery from tailings, mine water, or batteries.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Electrochemical Processing In Mining Market Report Segmentation

This report forecasts the global, country, and regional revenue growth and analyzes the latest trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global electrochemical processing in mining market report by process type, metals recovered, and region:

-

Process Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Electrowinning

-

Electrorefining

-

Others

-

-

Metals Recovered Outlook (Revenue, USD Million, 2021 - 2033)

-

Base Metals

-

Precious Metals

-

Critical Metals

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

The global electrochemical processing in mining market size was estimated at USD 17.03 billion in 2024 and is expected to reach USD 18.10 billion in 2025.

The global electrochemical processing in mining market is expected to grow at a compound annual growth rate of 7.8% from 2025 to 2033, reaching USD 32.94 billion by 2033.

By process type, electrowinning dominated the market with a revenue share of over 64.0% in 2024.

Some of the key vendors in the global electrochemical processing in mining market are Albemarle Corporation, Freeport-McMoRan Inc., Ganfeng Lithium, Glencore Plc, Hydroleap, Ma’aden, Rio Tinto Group, Southern Base Metals Corporation, Tianqi Lithium, and Yasa ET Co., Ltd.

Increasing supply chain risks, geopolitical uncertainties, and the rising demand for critical minerals crucial to defense, clean energy, and high-tech sectors mainly drive the global electrochemical processing in mining market. Governments are more frequently creating reserves to decrease import reliance and improve resource security.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.