- Home

- »

- Plastics, Polymers & Resins

- »

-

Flexible Plastic Packaging Market Size Report, 2026-2033GVR Report cover

![Flexible Plastic Packaging Market (2026 - 2033)Report]()

Flexible Plastic Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Polyethylene, Polypropylene, Polyamide), By Product (Pouches, Rollstock, Films & Wraps, Bags), By End-use (Food, Beverages, Personal Care & Cosmetics), By Region, And Segment Forecasts

Market Size, 2025

$166.5BMarket Estimate, 2026

$173.3BMarket Forecast, 2033

$243.5BCAGR, 2026–2033

5.0%Flexible Plastic Packaging Market Summary

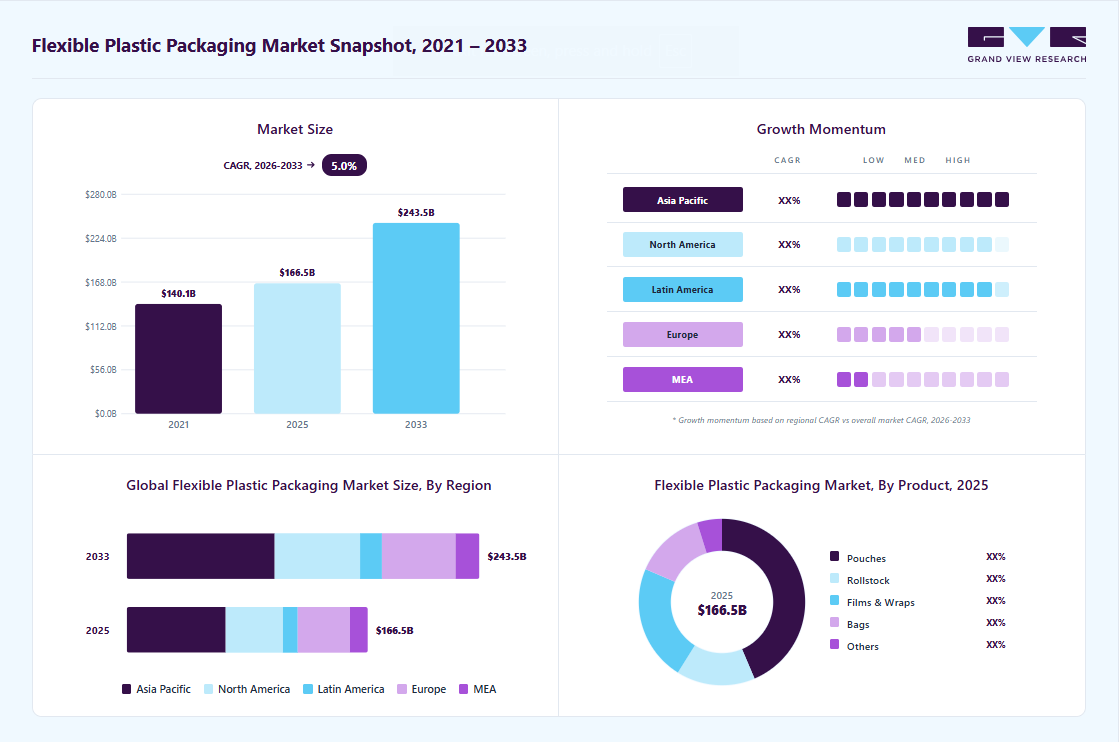

The global flexible plastic packaging market size was valued at USD 166.5 billion in 2025 and is projected to grow from USD 173.3 billion in 2026 to USD 243.5 billion by 2033, at a CAGR of 5.0% from 2026 to 2033. The Asia Pacific held the largest share of 40.0% of the global market in 2025. Rising demand for lightweight, cost-efficient, and convenient packaging in food, beverages, and pharmaceuticals is driving flexible plastic packaging adoption.

Key Market Trends & Insights

- By material: Polyethylene (PE) segment accounting for a 43.0% revenue share in 2025.

- By product: Pouches segment accounted for 43.0% of the market share in 2025.

- By end-use: Food segment accounting for 52.0% of market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (40.0% revenue share, 2025)

- By country: The China led the Asia Pacific market in 2025.

Market Size & Forecast

- Market size in 2025: USD 166.5 Billion

- Estimated market size in 2026: USD 173.3 Billion

- Projected market size by 2033: USD 243.5 Billion

- CAGR (2026-2033): 5.0%

Its superior barrier properties, extended shelf life, and compatibility with sustainability innovations further fuel growth. The flexible plastic packaging market is driven by increasing demand for convenience-oriented packaging solutions across food, beverage, and consumer goods industries. Urbanization, changing lifestyles, and the growth of ready-to-eat and ready-to-cook products have accelerated the adoption of lightweight, resealable, and easy-to-handle Products such as pouches, sachets, and wraps. Flexible plastic packaging provides effective barrier protection against moisture and oxygen, supports extended shelf life, and ensures product integrity, making it a preferred choice for manufacturers and foodservice operators.Cost efficiency and supply chain optimization represent another major growth driver for flexible plastic packaging. Compared to rigid alternatives, flexible plastics require lower material usage, reduce transportation and storage costs, and improve overall logistics efficiency. These advantages are increasingly important amid raw material price volatility, evolving trade policies, and the growing emphasis on domestic manufacturing in the U.S. In May 2025, Oroville Flexible Packaging, a RE:CIRCLE Solutions company based in California, introduced a sustainable flexible plastics packaging and recycling system offering customized domestic manufacturing and closed-loop recycling services, demonstrating how flexible packaging solutions can enhance operational resilience while addressing sustainability and sourcing requirements.

")

Technological advancements and sustainability-focused innovation are further accelerating market growth. The industry is witnessing increased adoption of recyclable and mono-material structures, downgauging technologies, and enhanced printing and traceability solutions to support circular economy objectives and regulatory compliance. The Oroville Flexible Packaging initiative also incorporates transparent audit trails to meet rising sustainability expectations from U.S. retail and foodservice customers. Such developments reinforce flexible plastic packaging as a strategically important solution that balances performance, cost efficiency, and environmental responsibility.

Market Dynamics

The rapid growth of the pharmaceutical industry is driving significant demand for flexible plastic packaging worldwide. Rising consumer health awareness, rising pharmaceutical consumption, and the growing preference for convenient, lightweight packaging formats are driving market expansion. In addition, the increasing number of pharmaceutical manufacturing and processing facilities, particularly in emerging economies such as China and India, is creating strong demand for flexible plastic packaging products. Government support, foreign direct investment (FDI), and initiatives promoting pharmaceutical innovation and expanding production capacity are further accelerating market growth and driving advancements in flexible packaging technologies.

Moreover, the pharmaceutical sector increasingly prefers flexible plastic packaging over traditional glass packaging due to its superior functionality, safety, and cost efficiency. Flexible plastic packaging offers key advantages, including child-resistant features, tamper-proof sealing, anti-counterfeiting protection, lightweight handling, and improved product convenience. Strong pharmaceutical production growth across regions, including North America and Europe, is also positively impacting the market. Countries such as the U.S., Canada, Germany, France, Italy, and Switzerland continue to see rising pharmaceutical demand, creating substantial opportunities for flexible plastic packaging manufacturers worldwide.

Stringent government regulations regarding the use and disposal of plastic materials are expected to restrain the growth of the flexible plastic packaging market. Increasing environmental concerns related to plastic waste, pollution, and disposal have prompted regulatory authorities across regions such as North America, Europe, and the Asia Pacific to implement strict guidelines governing plastic packaging usage and waste management. Organizations such as the U.S. Environmental Protection Agency (EPA), the European Union (EU), and environmental monitoring bodies have introduced regulations to reduce plastic pollution, improve recycling practices, and limit plastic disposal into water bodies. These evolving regulatory pressures are increasing compliance costs for manufacturers and hindering the widespread adoption of flexible plastic packaging solutions.

Market Concentration & Characteristics

The flexible plastic packaging industry is characterized by high volume production, strong cost competitiveness, and continuous material innovation. Manufacturers focus on lightweight, high-performance films that offer barrier protection, durability, and seal integrity while minimizing material usage. Economies of scale play a critical role, as large production runs and optimized extrusion and converting processes help suppliers remain price competitive, particularly in food, beverage, and fast-moving consumer goods applications.

The industry is also marked by intensifying sustainability and regulatory influence. Regulatory pressure, retailer commitments, and consumer expectations are pushing manufacturers toward recyclable, mono-material, and circular packaging solutions. This has increased investment in R&D, recycling infrastructure, traceability systems, and partnerships across the value chain. At the same time, the industry must balance sustainability goals with performance, cost, and compliance requirements, making innovation and operational efficiency critical competitive differentiators.

Material Insights

The Polyethylene (PE) segment dominated the flexible plastic packaging market in 2025, accounting for over a 43.0% revenue share, due to its excellent flexibility, toughness, and moisture barrier properties, which make it suitable for a wide range of food and consumer packaging applications. Its cost effectiveness and wide availability enable large scale adoption across high volume Products. In addition, PE is highly compatible with recycling and mono material structures, aligning with sustainability and circular economy initiatives.

Polypropylene (PP) is expected to register the highest growth rate of 5.4% during the forecast period, driven by its superior heat resistance, clarity, and mechanical strength, which make it suitable for retort packaging, microwaveable formats, and high-performance food applications. Its ability to deliver downgauged, lightweight structures at competitive costs further supports adoption across food, pharmaceutical, and personal care packaging. In addition, increasing development of recyclable and mono-material PP solutions is strengthening its position amid rising sustainability and regulatory requirements.

Product Insights

The pouches segment accounted for over 43.0% of the flexible plastic packaging market in 2025 and is projected to grow at the fastest CAGR of 5.7% over the forecast period. This segment includes stand-up pouches, flat pouches, spouted pouches, and retort pouches, which are widely adopted across food, beverages, pharmaceuticals, and personal care applications. Growth is driven by demand for lightweight, resealable, and shelf-ready packaging that offers cost efficiency, extended shelf life, and strong branding potential.

Films & wraps represent a significant product segment within the flexible plastic packaging market, driven by their extensive use across food, beverage, pharmaceutical, and consumer goods applications. This segment includes stretch films, shrink films, cling films, barrier films, and overwraps, which are widely used for unit packaging, pallet wrapping, and product protection. Their ability to provide moisture and oxygen barriers while maintaining product visibility makes them especially critical in fresh food, meat, dairy, and bakery packaging.

End-use Insights

The food segment dominated the flexible plastic packaging market in 2025, accounting for over 52.0% of total market share, driven by high consumption of packaged and processed foods worldwide. Flexible plastic packaging offers effective barrier protection, extended shelf life, and convenience features such as resealability, making it well suited for fresh, frozen, and ready-to-eat food products. In addition, its cost efficiency and compatibility with high-volume food processing and distribution systems continue to support strong adoption across the global food industry.

The pharmaceutical and healthcare end use segment is expected to register a CAGR of 5.5% over the forecast period, supported by rising demand for safe, contamination-free, and regulatory-compliant packaging solutions. Flexible plastic packaging is widely used for unit dose packs, blister lidding, sachets, and medical device packaging due to its strong barrier properties and durability. Growth is further driven by increasing pharmaceutical production, expanding healthcare access, and the need for lightweight, tamper-evident, and cost-efficient Products.

Regional Insights

Asia Pacific dominated the flexible plastic packaging market in 2025, accounting for over 40.0% of global market share, and is projected to expand at the fastest CAGR of 5.3% over the forecast period. This growth is driven by rapid urbanization, rising population, and increasing consumption of packaged food and consumer goods across China, India, and Southeast Asia. In addition, expanding manufacturing capacity, cost-competitive production, and growing investments in flexible packaging technologies are further strengthening the region’s market leadership.

China Flexible Plastic Packaging Market Trends

Chinarepresents the largest country market within the Asia Pacific flexible plastic packaging industry, driven by its vast consumer base and strong food and consumer goods manufacturing ecosystem. High demand for packaged foods, ready-to-eat meals, and e-commerce-friendly Products is accelerating the adoption of flexible plastic packaging across the country. In addition, large-scale domestic production capabilities, ongoing investments in advanced film technologies, and a growing focus on recyclable and mono-material packaging solutions continue to support China’s market dominance.

North America Flexible Plastic Packaging Market Trends

North Americarepresents a mature yet steadily growing market for flexible plastic packaging, supported by strong demand from the food, beverage, pharmaceutical, and healthcare sectors. The region benefits from advanced packaging technologies, high adoption of convenience-oriented formats such as pouches and films, and a well-established retail and foodservice infrastructure. In addition, increasing investments in sustainable, recyclable, and domestically manufactured flexible packaging solutions are reinforcing market stability and long-term growth across the U.S. and Canada.

The U.S. represents the largest market for flexible plastic packaging in North America, driven by high consumption of packaged foods, beverages, and pharmaceutical products. Strong demand for convenience-focused formats such as pouches, films, and wraps, along with advanced packaging and converting capabilities, continues to support market growth. In addition, increasing emphasis on recyclable, mono-material structures, domestic manufacturing, and circular economy initiatives is shaping innovation and investment across the U.S. flexible plastic packaging industry.

Europe Flexible Plastic Packaging Market Trends

Europe represents a well-established and sustainability-driven market for flexible plastic packaging, supported by strong demand from the food, beverage, and pharmaceutical industries. The region is characterized by strict regulatory frameworks, including circular economy and packaging waste directives, which are accelerating the adoption of recyclable, mono-material, and downgauged flexible packaging solutions. In addition, advanced packaging technologies, high consumer awareness, and strong presence of multinational brand owners continue to shape innovation and steady market growth across Western and Northern Europe.

Key Flexible Packaging Company Insights

The competitive environment of the flexible plastic packaging market is highly fragmented and intensely competitive, characterized by the presence of large multinational converters alongside numerous regional and local players. Global leaders compete on scale, diversified product portfolios, advanced barrier materials, and strong relationships with FMCG, food, and pharmaceutical companies, while regional players often differentiate through cost competitiveness, customization, and faster turnaround times.

Competition is increasingly shifting from price alone to innovation-driven factors such as lightweighting, high-barrier and multilayer films, recyclability, mono-material structures, and compliance with evolving sustainability regulations. Strategic moves such as capacity expansions, mergers & acquisitions, partnerships with brand owners, and investments in recycling-compatible technologies are common as companies seek to strengthen market share and geographic reach. Overall, the market rewards players that can balance cost efficiency, performance, and sustainability, making innovation and regulatory adaptability key competitive differentiators.

-

In April 2025, Amcor plc completed its all-stock acquisition of Berry Global Inc, creating a global packaging leader with around 400 facilities, 75,000 employees, and operations in 140 countries. The merger, valued at approximately USD 13.0 billion, enhances Amcor's portfolio with expanded material science and innovation capabilities, positioning it to deliver more consistent growth and improved margins.

-

In April 2025, TOPPAN Inc. completed its acquisition of Sonoco Products Company’s Thermoformed & Flexibles Packaging (TFP) business for approximately USD 1.8 billion, marking a significant expansion of TOPPAN’s global packaging operations and its commitment to sustainable packaging solutions. This acquisition aligns with TOPPAN’s strategy to drive innovation in sustainable packaging and streamline its global operations, further strengthening its market position and ability to deliver advanced packaging solutions worldwide.

Key Flexible Plastic Packaging Companies:

The following key companies have been profiled for this study on the flexible plastic packaging market.

- Amcor plc

- Sealed Air

- Huhtamaki

- ProAmpac

- TOPPAN Inc.

- Constantia Flexibles

- Cosmo Films

- Uflex Limited

- Jindal Films

- CarePac

- Winpak LTD.

- FLAIR Flexible Packaging Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Amcor plc; Sealed Air; Huhtamaki; TOPPAN Inc.; Constantia Flexibles

- Regional expansion through acquisitions and sustainability-focused investments; strong engagement in R&D and recyclable flexible packaging development.

- Expansion in emerging economies and development of fiber-based and recyclable flexible packaging solutions.

- Extensive global manufacturing footprint; diversified product portfolio; strong sustainability positioning and financial strength.

- Strong technological capabilities; established relationships with food and healthcare companies.

- High operational complexity; exposure to raw material price volatility.

- Limited flexibility in highly customized small-volume orders.

Emerging Players: ProAmpac; Cosmo Films

- Focus on specialty films, labeling, and sustainable film innovations.

- Customer-centric packaging customization and short-run flexible packaging production.

- Strong responsiveness to small and medium-sized customer requirements.

- Strong customization capabilities and innovation-focused portfolio.

- Limited diversification outside film manufacturing.

- Limited international presence and production scale.

Flexible Plastic Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 166.5 billion

Estimated market size in 2026

USD 173.3 billion

Projected market size by 2033

USD 243.5 billion

Growth rate

CAGR of 5.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, product, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; UAE ; South Africa

Key companies profiled

Amcor plc; Sealed Air; Huhtamaki; ProAmpac; TOPPAN Inc.; Constantia Flexibles; Cosmo Films; Uflex Limited; Jindal Films; CarePac; Winpak LTD.; FLAIR Flexible Packaging Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Flexible Plastic Packaging Market Report Segmentation

This report forecasts revenue growth at the regional, and country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global flexible plastic packaging market report on the basis of material, product, end-use, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Polyamide (PA)

-

Polyvinyl Chloride (PVC)

-

Polystyrene (PS)

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Pouches

-

Rollstock

-

Films & Wraps

-

Bags

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Food

-

Beverages

-

Pharmaceutical & Healthcare

-

Personal Care & Cosmetics

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed analysis of the global flexible plastic packaging market across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, including country-level demand assessment, food & beverage consumption trends, pharmaceutical packaging demand, sustainability initiatives, plastic waste regulations, recycling infrastructure, and regional growth outlook.

Identify high-growth regional markets and investment opportunities. Support region-specific expansion strategies and sales prioritization. Enable understanding of regional consumption patterns, sustainability adoption, regulatory landscape, and competitive intensity.

Competitive Benchmarking

Comparative assessment of key flexible plastic packaging manufacturers based on product portfolio, packaging formats, film technologies, sustainability initiatives, regional presence, production capabilities, strategic partnerships, innovation capabilities, and recent developments.

Support competitor tracking and positioning analysis. Identify market leaders, emerging players, and product differentiation opportunities. Enable informed partnership, acquisition, and competitive strategy development.

Pricing Analysis

Assessment of flexible plastic packaging pricing trends across films, pouches, wraps, bags, and high-barrier packaging formats, including analysis of polymer raw material costs, packaging design complexity, regional pricing variations, production costs, and competitor pricing structures.

Identify key pricing drivers and cost optimization opportunities. Support competitive pricing strategy development and procurement planning. Enable benchmarking against regional and global flexible plastic packaging manufacturers.

Frequently Asked Questions About This Report

Key factors that are driving the market growth include surging demand for flexible plastics in pharmaceutical packaging, owing to increasing health awareness among consumers and the burgeoning popularity of convenient packaging.

Pouches held the largest revenue share 43.0% in 2025.

The polyethylene (PE) segment led with a 43.0% revenue share in 2025.

Food held the largest share (over 52.0%) in 2025.

The global flexible plastic packaging market is expected to grow at a compound annual growth rate of 5.0% from 2026 to 2033 and reach USD 243.5 billion by 2033.

The global flexible plastic packaging market size was estimated at USD 166.5 billion in 2025 and is expected to reach USD 173.3 billion in 2026.

Asia Pacific dominated with a 40.0% revenue share in 2025.

Some key players operating in the flexible plastic packaging market include Amcor plc; Sealed Air; Huhtamaki; ProAmpac; TOPPAN Inc.; Constantia Flexibles; Cosmo Films; Uflex Limited; Jindal Films; CarePac; Winpak LTD.; and FLAIR Flexible Packaging Corporation

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.