- Home

- »

- Renewable Energy

- »

-

Hydrogen Generation Market Size, Share Report, 2026-2033GVR Report cover

![Hydrogen Generation Market (2026 - 2033)Report]()

Hydrogen Generation Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology (Coal Gasification, Steam Methane Reforming), By Systems (Merchant (Transportation), Captive (On-Site Consumption)), By Application, By Region, And Segment Forecasts

Market Size, 2025

$204.7BMarket Estimate, 2026

$225.0BMarket Forecast, 2033

$401.3BCAGR, 2026–2033

8.6%Hydrogen Generation Market Summary

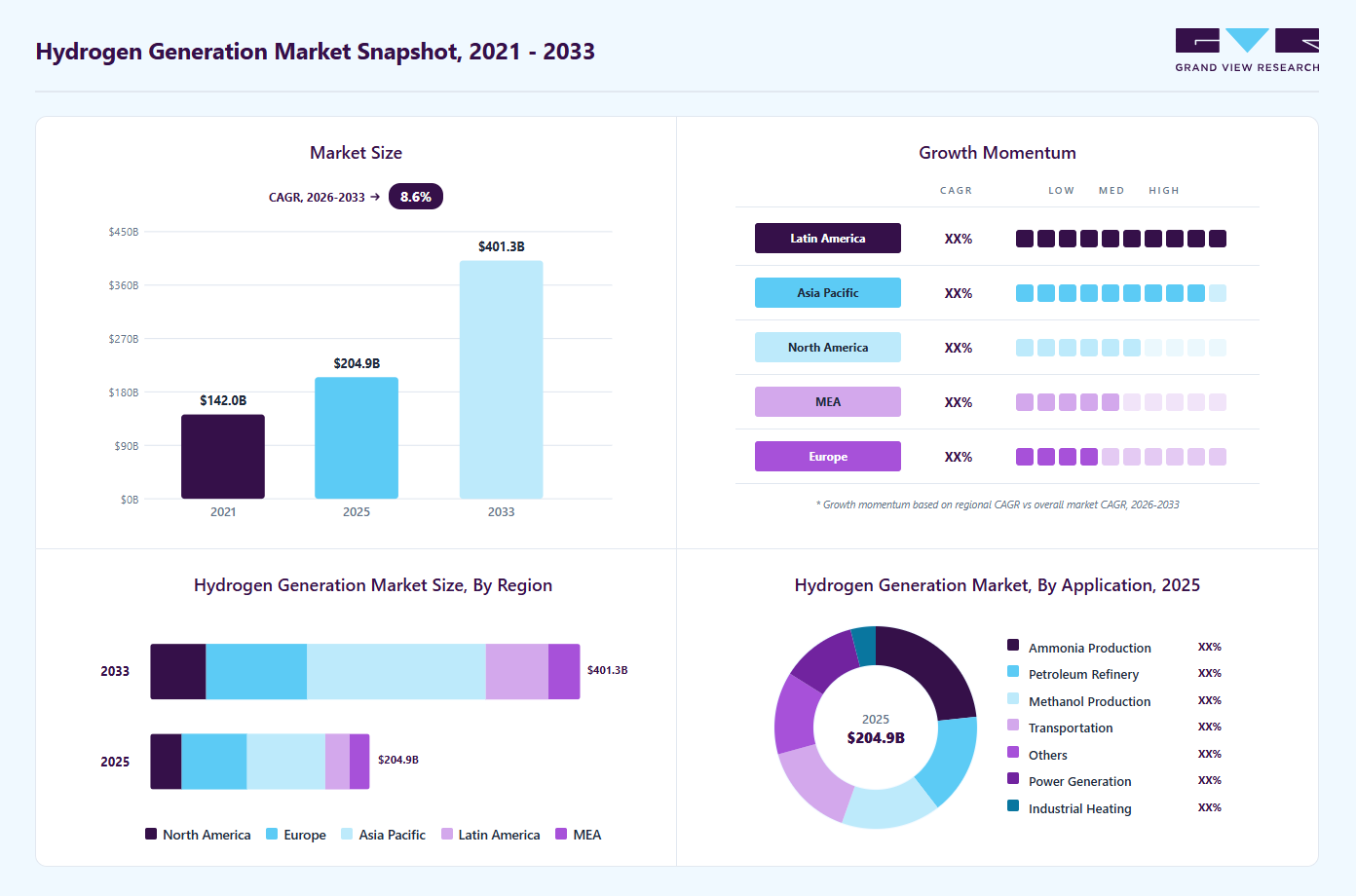

The global hydrogen generation market size was valued at USD 204.7 billion in 2025 and is projected to grow from USD 225.0 billion in 2026 to USD 401.3 billion by 2033, at a CAGR of 8.6% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 35.6% in 2025. The growth is primarily driven by the rising adoption of hydrogen as a clean and sustainable energy source across industrial, transportation, and power generation sectors.

Key Market Trends & Insights

- By systems: The captive generation segment led the market with the largest revenue share of 65.12% in 2025.

- By application: The ammonia production segment accounted for the largest market revenue share in 2025.

- By technology: The coal gasification segment accounted for the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (35.6% revenue share, 2025)

- Fastest-growing regional market: Latin America (highest CAGR, 2026-2033)

- The hydrogen generation industry in the China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 204.7 Billion

- Estimated market size in 2026: USD 225.0 Billion

- Projected market size by 2033: USD 401.3 Billion

- CAGR (2026-2033): 8.6%

Increasing government initiatives and subsidies aimed at reducing carbon emissions, coupled with growing investments in hydrogen production infrastructure, are accelerating market expansion.Technological advancements in hydrogen production methods, such as electrolysis using renewable energy, and the development of cost-effective and efficient storage and distribution solutions are further fueling market growth. In addition, the escalating demand for green hydrogen in refineries, chemical manufacturing, and fuel cell applications is creating significant opportunities.

")

Regionally, Asia-Pacific is expected to dominate due to large-scale industrial applications and substantial government support, while Europe and North America are witnessing rapid adoption of hydrogen for mobility and renewable energy integration. As industries and governments increasingly focus on decarbonization, the hydrogen generation industry is poised to witness robust growth through 2033.

Drivers, Opportunities & Restraints

The hydrogen generation industry is driven by the growing demand for clean energy and global initiatives aimed at reducing carbon emissions. Hydrogen adoption is increasing across the industrial, power, and mobility sectors, driven by technological advancements in electrolysis, fuel cells, and carbon capture, which enhance production efficiency and energy security.

Green hydrogen production from renewable sources presents strong growth potential. Expanding applications in fuel cell vehicles, public transport, and shipping, along with investments in storage, pipelines, and refuelling infrastructure, create new market avenues. Emerging regions like the Asia-Pacific and the Middle East offer high expansion potential.

High production costs, particularly for green hydrogen, and limited storage and transport infrastructure restrict market growth. Technical inefficiencies, inconsistent regulations, and competition from other renewable energy sources also pose challenges to adoption.

Technology Insights

The coal gasification segment led the market with the largest revenue share of 65.74% in 2025 and is expected to grow at the fastest CAGR during the forecast period. Coal gasification, which uses coal as a raw material for producing hydrogen, has been in practice for nearly two centuries; moreover, it is also recognized as a mature technology for hydrogen generation.

The U.S. has a huge domestic resource in coal. The use of coal to generate hydrogen for the transportation sector is expected to help America reduce its dependency on imported petroleum products. This growth is driven by increasing industrial demand, favorable government policies promoting cleaner energy alternatives, and ongoing technological advancements that enhance the efficiency and cost-effectiveness of coal gasification processes.

Systems Insights

The captive generation segment led the market with the largest revenue share of 65.12% in 2025 and is also expected to register at the fastest CAGR of 1.4% during the forecast period. Captive hydrogen generation refers to the on-site production of hydrogen, where it is generated and consumed at the same facility, thereby eliminating the need for external transport or distribution infrastructure.

This approach is increasingly adopted in industries such as refining, chemicals, and steel, where hydrogen demand is continuous and integration with existing operations enhances efficiency. With the rising interest in decarbonizing industrial processes and enhancing energy security, the captive generation segment is expected to grow steadily and maintain a strong position throughout the forecast period.

Application Insights

The ammonia production segment led the market with the largest revenue share of 23% in 2025. This segment is expected to maintain its lead throughout the forecast period. Ammonia’s potential as a carbon-free fuel, hydrogen carrier, and energy storage medium represents an opportunity for renewable hydrogen technologies to be deployed on an even greater scale. Hydrogen is typically produced on-site at ammonia plants from a fossil fuel feedstock. A common feedstock is natural gas, which is used to fuel a steam methane reforming (SMR) unit. Coal can also be used to produce ammonia via a partial oxidation (POX) process.

The transportation segment is anticipated to witness at the fastest CAGR over the forecast period. This accelerated expansion is primarily driven by the increasing adoption of alternative fuel vehicles, growing investments in clean mobility infrastructure, and supportive government policies aimed at reducing carbon emissions and dependence on conventional fossil fuels.

Regional Insights

The hydrogen generation market in North America is growing steadily, driven by strong demand from oil refining and industrial applications, as well as increasing policy support for clean energy. The United States dominates the region due to its established hydrogen infrastructure, while investments in green and blue hydrogen are accelerating under decarbonization initiatives and hydrogen hub programs.

U.S. Hydrogen Generation Market Trends

The hydrogen generation market in the U.S. is anticipated to grow at a significant CAGR over the forecast period. The U.S.-based market players like Praxair Inc. and Air Liquide are looking to expand their operations in other countries with increasing demand for hydrogen as part of their strategic growth plans.

Asia Pacific Hydrogen Generation Market Trends

Asia Pacific dominated the global hydrogen generation market with the largest revenue share of 35.6% in 2025. This leadership position is supported by rapid industrialization, the expansion of the refining and chemical sectors, strong government initiatives promoting the adoption of clean energy, and significant investments in hydrogen infrastructure across key economies, including China, Japan, South Korea, and India.

Latin America Hydrogen Generation Market Trends

The hydrogen generation market in Latin America is projected to register at the fastest CAGR of 12.5% over the forecast period, driven by increasing investments in infrastructure and industrial development, rising energy demand, and growing adoption of advanced technologies across key end-use sectors. Supportive government initiatives, expanding manufacturing activities, and improving economic stability in major economies are further contributing to accelerated market expansion in the region.

Europe Hydrogen Generation Market Trends

The hydrogen generation market in Europe is anticipated to grow rapidly over the forecast period, driven by the development and deployment of fuel cell systems in Europe, which are increasing due to projects announced by the European Commission through organizations such as the Fuel Cells and Hydrogen Joint Undertaking (FCH JU). These projects have been announced with the objective of increasing the adoption of fuel cell vehicles in Europe, and this will aid in the development of supportive hydrogen infrastructure for fuel cell vehicles in major European countries.

Middle East & Africa Hydrogen Generation Market Trends

The hydrogen generation market in the Middle East & Africa is gradually expanding, supported by strong refining and ammonia demand, as well as growing investments in green and blue hydrogen. Abundant renewable resources and government-led initiatives in countries such as Saudi Arabia and the UAE are positioning the region as a future hub for hydrogen production and export.

Key Hydrogen GenerationCompany Insights

Some of the key players operating in the global hydrogen generation industry include Air Liquide International S.A. and Linde plc, among others.

-

Air Liquide International S.A. is one of the world’s leading industrial gas and hydrogen producers, headquartered in France, with operations across Europe, North America, Asia-Pacific, the Middle East, and Latin America. Founded in 1902, Air Liquide has a strong presence across the entire hydrogen value chain, including large-scale hydrogen production, purification, storage, and distribution. The company is a major supplier of hydrogen for refining, chemical processing, electronics, and mobility applications. Air Liquide is also a key player in low-carbon and green hydrogen, leveraging technologies such as electrolysis, carbon capture, and renewable integration.

-

Linde plc is a global industrial gas and engineering company headquartered in the United Kingdom, with a significant operational footprint in North America, Europe, and Asia-Pacific. Linde is one of the world's largest hydrogen producers, supplying hydrogen for refinery operations, ammonia production, chemicals, and emerging clean energy applications. The company possesses deep expertise in hydrogen generation technologies, including steam methane reforming, autothermal reforming, and water electrolysis, as well as advanced hydrogen liquefaction and storage solutions.

Key Hydrogen Generation Companies:

The following are the leading companies in the global hydrogen generation market. These companies collectively hold the largest market share and dictate industry trends.

- Air Liquide International S.A.

- Air Products and Chemicals, Inc.

- Cummins Inc. (Hydrogenics)

- INOX Air Products Ltd.

- Iwatani Corporation

- Linde plc

- Matheson Tri-Gas, Inc.

- Messer Group GmbH

- Nel ASA (NEL Hydrogen)

- Taiyo Nippon Sanso Corporation

Recent Developments

-

In September 2025, Air Products and Chemicals, Inc. advanced its hydrogen generation footprint by progressing construction milestones at its NEOM Green Hydrogen Project in Saudi Arabia, one of the world’s largest green hydrogen facilities. The project integrates large-scale renewable power generation with electrolysis-based hydrogen production to supply green ammonia for global export markets. Air Products is responsible for the engineering, procurement, and long-term operation of the hydrogen production and export infrastructure.

Hydrogen Generation Market Report Scope

Report Attribute

Details

Market Definition

The hydrogen generation market size represents the global revenue generated from the production of hydrogen using technologies such as steam methane reforming and water electrolysis for industrial, energy, and transportation applications.

Market size in 2025

USD 204.7 billion

Estimated market size in 2026

USD 225.0 billion

Projected market size by 2033

USD 401.3 billion

Growth rate

CAGR of 8.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, Volume in Million Metric Tons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Technology, systems, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Spain; Italy; China; India; Japan; South Korea; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Air Liquide International S.A.; Linde plc; Air Products and Chemicals, Inc.; Messer Group GmbH; INOX Air Products Ltd.; Iwatani Corporation; Matheson Tri-Gas, Inc.; Taiyo Nippon Sanso Corporation; Nel ASA (NEL Hydrogen); Cummins Inc. (Hydrogenics)

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Hydrogen Generation Market Report Segmentation

This report forecasts volume and revenue growth at global, regional, and country levels and provides an analysis of latest industry trends in each of sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global hydrogen generation market report based on technology, application, system, and region:

-

Technology Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033)

-

Coal Gasification

-

Steam Methane Reforming

-

Others

-

-

Systems Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033

-

Merchant (Transportation)

-

Captive (On-Site Consumption)

-

-

Application Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033)

-

Methanol Production

-

Ammonia Production

-

Petroleum Refinery

-

Transportation

-

Power Generation

-

Industrial Heating

-

Others

-

-

Regional Outlook (Volume, Million Metric Tons; Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Some of the key vendors operating in the global hydrogen generation market include Air Liquide International S.A., Linde plc, Air Products and Chemicals, Inc., Cummins Inc. (Hydrogenics), Nel ASA, Bloom Energy Corporation, Messer Group GmbH, INOX Air Products Ltd., Iwatani Corporation, and Taiyo Nippon Sanso Corporation, among others.

The hydrogen generation market is primarily driven by the accelerating global shift toward clean and low-carbon energy systems, supported by stringent emission regulations and government incentives promoting hydrogen adoption. Rising demand from refining, chemicals, and emerging mobility and power generation applications, along with advancements in electrolysis and carbon capture technologies, are further strengthening market growth by improving efficiency, scalability, and cost competitiveness.

Captive generation held the largest revenue share 65.1% in 2025.

Coal gasification held the largest share (over 65.7%) in 2025.

Asia Pacific dominated with a 35.6% revenue share in 2025.

The global hydrogen generation market size was estimated at USD 204.7 billion in 2025 and is expected to reach USD 225.0 billion in 2026.

The global hydrogen generation market is expected to grow at a compound annual growth rate of 8.6% from 2026 to 2033 to reach USD 401.3 billion by 2033.

Ammonia production held the largest revenue share of approximately 23% in 2025.

About the Author(s)

Renewable Energy Research Team

Energy & Power · Renewable EnergyThis report was authored by the renewable energy research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the renewable energy segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.