- Home

- »

- Sensors & Controls

- »

-

Laser Interferometer Market Size, Share Report, 2026 - 2033GVR Report cover

![Laser Interferometer Market Size, Share & Trends Report]()

Laser Interferometer Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Type (Michelson Interferometers, Fabry-Perot Interferometers), By Technology, By Application, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$336.3MMarket Estimate, 2026

$364.3MMarket Forecast, 2033

$629.5MCAGR, 2026–2033

8.1%Laser Interferometer Market Summary

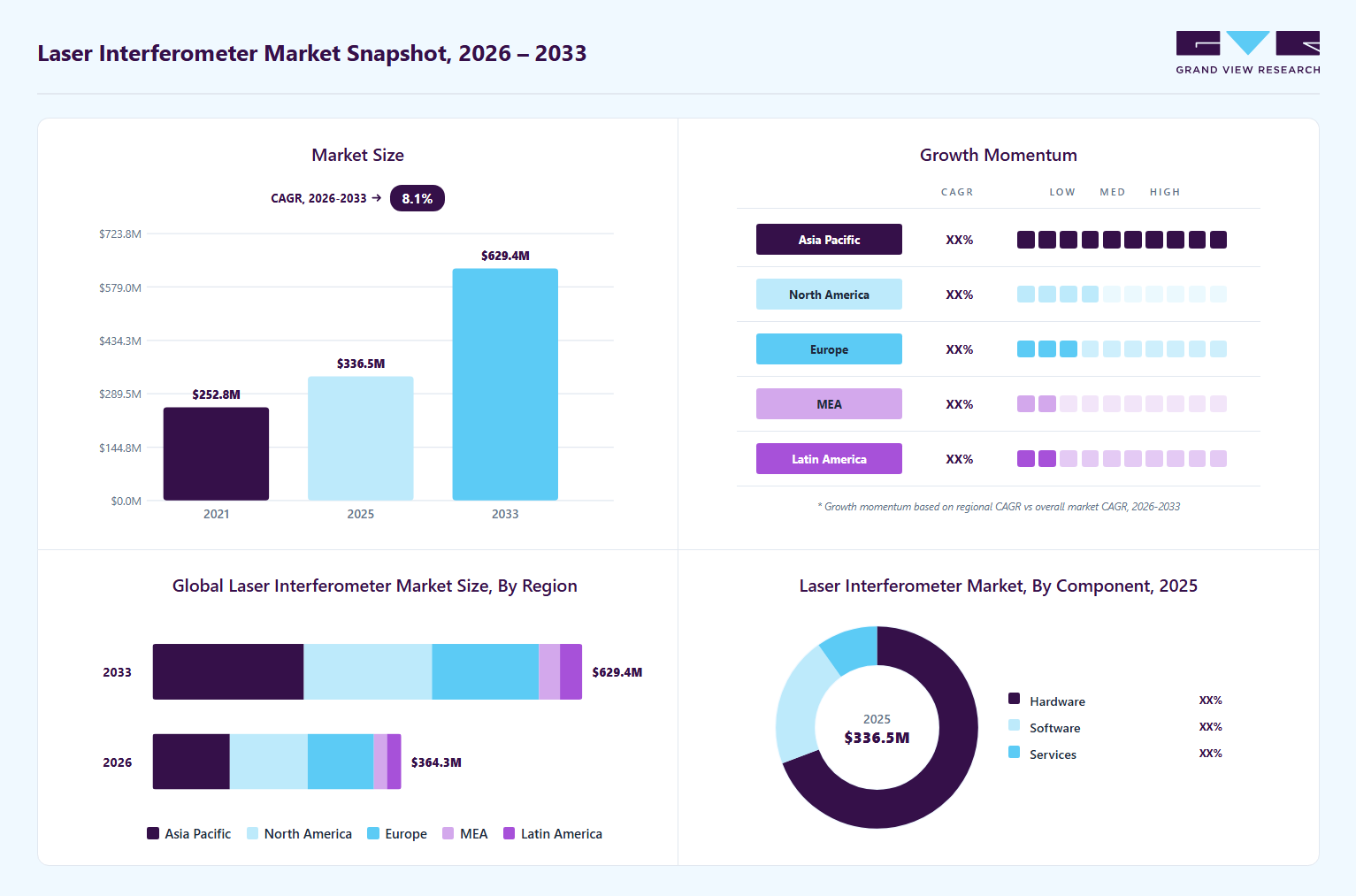

The global laser interferometer market size was valued at USD 336.3 million in 2025 and is projected to grow from USD 364.3 million in 2026 to USD 629.5 million by 2033, at a CAGR of 8.1% from 2026 to 2033. The laser interferometer market in North America accounted for the largest revenue share of 31.5% in 2025. The market growth is primarily driven by the rising demand for ultra-precise measurement solutions across semiconductor manufacturing, aerospace, automotive, and advanced industrial production.

Key Market Trends & Insights

- The U.S. laser interferometer market dominated the market with a share of over 81% in 2025.

- Based on component, the hardware segment accounted for the largest revenue share of over 69% in 2025.

- Based on type, the Michelson interferometers segment holds a substantial share of over 32% in 2025.

- Based on technology, the digital / laser scanning interferometry segment is expected to grow at the highest CAGR of over 10% from 2026 to 2033.

Market Size & Forecast

- 2025 Market Size: USD 336.3 Million

- 2033 Projected Market Size: USD 629.5 Million

- CAGR (2026-2033): 8.1%

- North America: Largest market in 2025

- Asia Pacific: Fastest growing market

In addition, the increasing complexity of engineering designs and tighter tolerance requirements in high-end manufacturing are accelerating the adoption of nanometer-level accuracy tools for alignment, calibration, and quality control. The rapid expansion of the semiconductor and electronics industry is a major growth driver, with laser interferometers playing a critical role in wafer inspection, lithography alignment, and equipment calibration. Continuous advancements in chip miniaturization and growing investments in fabrication facilities are boosting the need for highly accurate metrology systems. The increasing dependency of semiconductor fabs on sub-nanometer precision control systems is driving the laser interferometer industry growth.")

Additionally, the rapid technological enhancements in laser sources, optics, and digital processing are enhancing the performance and usability of interferometer systems. The growing integration with automation platforms, AI-based analytics, and real-time monitoring capabilities is improving measurement efficiency and enabling broader industrial adoption across production and R&D environments. The continuous advancements in precision metrology technologies, enabling higher operational efficiency and reliability is significantly driving the market growth.

Furthermore, the increasing shift toward Industry 4.0 and smart manufacturing ecosystems is supporting the integration of laser interferometers into automated production lines. Demand for real-time quality monitoring, predictive maintenance, and connected factory systems is strengthening the role of precision metrology in modern industrial workflows. The widespread shift toward fully automated and digitally controlled manufacturing environments is expected to further drive the market growth in the coming years.

Moreover, expanding applications in scientific research, space exploration, and defense technologies are further contributing to market growth. Laser interferometers are widely utilized in advanced physics experiments, satellite testing, and high-precision defense systems, supported by continuous government and institutional investments in cutting-edge research programs. Overall market growth is being reinforced by increasing reliance on ultra-precise measurements in high-stakes scientific and defense missions.

Market Dynamics

The laser interferometer market is primarily driven by the growing need for ultra-precise measurement solutions across the semiconductor, aerospace, automotive, and advanced manufacturing industries. Modern production processes require extremely tight tolerances, where even nanometer-level deviations can impact product performance and yield. Laser interferometers enable highly accurate alignment, calibration, and surface measurement, making them essential in high-value production environments. This growing dependence on precision engineering is significantly strengthening market adoption.

Another key factor supporting growth is the rapid expansion of semiconductor fabrication and electronics manufacturing facilities worldwide. Advanced chip designs, miniaturization trends, and complex lithography processes demand highly stable and accurate metrology systems. Laser interferometers are widely used in wafer inspection and equipment calibration, ensuring high production efficiency and reduced error rates. Continuous investments in new fabs are further accelerating demand for these systems.

Additionally, increasing focus on quality control and productivity optimization across industrial sectors is boosting adoption. Manufacturers are prioritizing advanced measurement technologies to reduce defects, improve throughput, and maintain global competitiveness. The ability of laser interferometers to deliver high-speed, non-contact, and highly accurate measurements makes them a critical tool in modern production workflows. This widespread industrial requirement is a major driver of sustained market growth.

One of the key restraints in the laser interferometer market is the high initial investment required for system procurement and deployment. These instruments involve advanced optical components, precision lasers, and sophisticated calibration systems, making them significantly more expensive than conventional measurement tools. This high cost structure limits adoption, especially among small and medium-sized enterprises with constrained capital budgets.

Operational complexity also restricts wider market penetration. Laser interferometers require controlled environments with minimal vibration, stable temperature, and clean operating conditions to ensure accurate measurements. Setting up such environments adds additional infrastructure costs and increases overall system dependency. The need for skilled technicians further raises operational expenses, making it challenging for companies without specialized expertise.

Furthermore, maintenance and calibration requirements add to long-term ownership costs. Regular system tuning is essential to maintain accuracy, which can lead to downtime and additional service expenditures. These combined factors make adoption less feasible for cost-sensitive industries, thereby slowing down overall market expansion despite strong demand potential.

A major opportunity for the laser interferometer market lies in the rapid growth of Industry 4.0 and digital manufacturing ecosystems. The increasing adoption of smart factories is driving demand for real-time, automated, and highly accurate measurement systems. Laser interferometers integrated with IoT platforms and industrial automation systems enable continuous monitoring and process optimization, making them highly valuable in modern production environments.

The rise of digital twins and data-driven manufacturing is further expanding the application scope. Companies are increasingly using virtual models of physical systems to simulate, analyze, and optimize production processes. Laser interferometers provide the high-precision data required to build and maintain these digital models, enabling improved decision-making and predictive maintenance. This is opening new use cases across multiple industries.

Additionally, growing investments in advanced manufacturing across emerging economies present strong expansion potential. Countries are focusing on upgrading industrial infrastructure and improving production efficiency, which is increasing demand for precision metrology solutions. With the global rise in automation levels, laser interferometers are expected to become an integral part of connected manufacturing ecosystems, creating significant long-term growth opportunities.

Market Concentration & Characteristics

The global laser interferometer market is moderately concentrated, with a small group of established precision metrology and optical instrumentation companies dominating high-end applications in semiconductor manufacturing, aerospace, defense, and advanced research. Leading players maintain strong positions through advanced product portfolios, proprietary optical technologies, high-precision engineering capabilities, and long-standing relationships with industrial and research institutions.

Furthermore, the market is characterized by a high degree of innovation with continuous technological advancements in laser stability, interferometric measurement accuracy, vibration compensation, and digital signal processing. Strategic collaborations among metrology firms, semiconductor manufacturers, and research organizations are also driving product development and expanding applications.

The market exhibits moderate substitution risk, primarily from alternative metrology technologies, such as coordinate measuring machines (CMMs), laser trackers, and structured-light scanning systems. Regulatory and standardization influences are significant, particularly in the aerospace, defense, and semiconductor industries, where strict calibration standards and quality certifications govern adoption. End-user concentration is relatively high, with strong demand from semiconductor fabs, precision engineering industries, and research laboratories, while adoption in mid-sized manufacturing sectors is gradually increasing due to automation and cost-efficiency improvements.

Component Insights

The hardware segment accounted for the largest market share, over 69% in 2025, owing to strong demand for high-precision optical components, including lasers, beam splitters, mirrors, detectors, and vibration isolation systems, used in industrial metrology and scientific applications. Additionally, the segmental growth is driven by the increasing deployment of interferometer-based measurement systems across semiconductor fabrication, aerospace alignment, and precision manufacturing, where ultra-high accuracy and real-time measurement capabilities are essential for process control and quality assurance.

The software segment is expected to register the highest CAGR of over 11% from 2026 to 2033, driven by the rising adoption of advanced data processing platforms, real-time signal analysis tools, and AI-enabled error correction systems that improve measurement accuracy. Additionally, the increasing automation in metrology workflows, growing use of digital twin technologies, and the demand for advanced visualization solutions that simplify the interpretation of complex interference data are the significant factors driving segmental growth.

Type Insights

The Michelson Interferometers segment accounted for the largest market share in 2025. This growth can be attributed to their widespread application in optical testing, surface profiling, and precision displacement measurement. Their dominance is further supported by a simple optical design, high measurement reliability, cost efficiency, and broad usage across laboratories, industrial inspection systems, and scientific research environments requiring accurate wave interference analysis, thereby driving segmental growth in the coming years.

The Fabry-Perot interferometers are expected to register the fastest CAGR from 2026 to 2033, owing to increasing demand for high-resolution spectral analysis and wavelength-specific measurement applications. The segmental growth is further supported by expanding use in fiber-optic communication systems, laser stabilization technologies, and photonics research, where extremely fine spectral resolution and high sensitivity are required. The rising demand for high-precision optical instrumentation in emerging photonics, spectroscopy, and laser-based communication applications is expected to further drive the segmental growth in the coming years.

Technology Insights

The heterodyne interferometry segment accounted for the largest market share in 2025, owing to its ability to deliver highly precise phase shift, vibration, and displacement measurements with strong resistance to environmental noise. Its adoption is reinforced by increasing usage in aerospace testing, nanotechnology research, and precision manufacturing applications that require sub-nanometer accuracy and stable performance. The segmental growth is further supported by increasing demand for highly stable and ultra-precise measurement technologies across advanced industrial and scientific applications.

The digital/laser-scanning interferometry segment is expected to register the fastest CAGR from 2026 to 2033, driven by rising demand for automated, high-speed, full-field surface measurement systems. Growth is supported by advancements in digital imaging sensors, integration with machine vision platforms, and increasing requirements for non-contact inspection methods in semiconductor inspection, biomedical imaging, and advanced materials analysis. The segmental growth is further accelerated by growing adoption of automated optical inspection technologies and increasing demand for high-speed, non-contact surface characterization solutions.

Application Insights

The precision engineering & metrology segment accounted for the largest market share in 2025, driven by the extensive use of interferometers for calibration, dimensional inspection, and quality assurance. The segmental growth is further supported by the rising demand for ultra-high precision measurement in advanced manufacturing processes, increasing automation in industrial inspection systems, and stringent quality standards across aerospace, automotive, and industrial equipment production.

The semiconductor inspection & lithography segment is expected to post the highest CAGR from 2026 to 2033, driven by relentless scaling of patterning requirements, the growing complexity of multi-patterning, and the need for nanometer-scale overlay and wafer‑flatness control. Growing investments in advanced packaging, chiplet integration, and sub‑3nm node development are increasing demand for inline interferometric inspection tools and specialized optics, accelerating segment growth.

End Use Insights

The semiconductor and electronics segment accounted for the largest market share in 2025, fueled by the rising need for ultra-precise measurement, alignment, and inspection tools in advanced chip fabrication and electronic component manufacturing. The segmental growth is further supported by the increasing complexity of semiconductor nodes, the expansion of wafer-scale production, and the growing adoption of laser interferometers for lithography, defect detection, and nanometer-level surface characterization. Overall, the segment continues to dominate, owing to its critical role in ensuring accuracy and optimizing yield in high-end electronics manufacturing.

The healthcare & life sciences segment is expected to register a significant CAGR from 2026 to 2033, driven by increasing use of laser interferometry in high-resolution biomedical imaging, ophthalmic diagnostics, and cellular-level research. The segmental expansion is further supported by rising demand for non-invasive diagnostic techniques, advancements in optical coherence tomography, and growing application of optical measurement tools in pharmaceutical development and life sciences research. Moreover, the growing adoption of advanced optical technologies for improved diagnostic accuracy is expected to further drive segmental growth in the coming years.

Regional Insights

North America dominated the laser interferometer market with a share of 31.5% in 2025, driven by strong demand from aerospace & defense, semiconductor manufacturing, and advanced research institutions, where ultra-precise measurement is critical. High R&D investments, rapid adoption of Industry 4.0, and the presence of leading technology and metrology companies further accelerate market growth. Additionally, increasing use of laser interferometers in space exploration programs, nanotechnology, and high-end manufacturing quality control supports sustained regional expansion.

U.S. Laser Interferometer Market Trends

The U.S. laser interferometer industry dominated the market with a share of over 81% in 2025, driven by large-scale semiconductor fabrication, defense modernization programs, and robust aerospace engineering activities that require extreme-precision metrology tools. Strong federal funding for scientific research and widespread adoption of automation in manufacturing also contribute to demand. The presence of major players and continuous innovation in laser-based measurement technologies further strengthen market growth.

Europe Laser Interferometer Market Trends

The Europe laser interferometer industry is expected to grow at a CAGR of over 7% from 2026 to 2033, driven by advanced industrial manufacturing, automotive engineering, and strong emphasis on precision engineering standards. Growth is supported by extensive adoption in aerospace hubs, scientific research facilities, and metrology institutes. Additionally, strict quality regulations and sustainability-focused manufacturing practices encourage the adoption of high-accuracy measurement systems, such as laser interferometers.

The Germany laser interferometer industry is expected to grow significantly in the coming years, fueled by its world-leading industrial automation, automotive manufacturing, and precision engineering sectors. The strong presence of machine tool manufacturers and metrology equipment suppliers drives consistent demand for high-accuracy measurement systems. Additionally, Industry 4.0 initiatives and focus on smart factories significantly boost the adoption of laser interferometers in production and calibration processes.

The UK laser interferometer industry is witnessing rapid expansion, driven by strong research capabilities in optics, photonics, and physics, particularly at universities and national laboratories. Demand is further driven by aerospace, R&D defense, and precision engineering industries. Government-backed innovation programs and collaborations between academia and industry also support the adoption of advanced interferometric measurement technologies.

Asia Pacific Laser Interferometer Market Trends

The Asia Pacific laser interferometer industry is expected to grow at the fastest CAGR of over 10% from 2026 to 2033, owing to expanding semiconductor production, electronics manufacturing, and industrial automation. Increasing investments in smart manufacturing, infrastructure development, and R&D centers across emerging economies are driving adoption. Rising demand for precision quality control in high-volume manufacturing industries further accelerates market expansion.

The China laser interferometer industry is being accelerated by massive semiconductor expansion, strong government support for advanced manufacturing, and rapid industrial automation. The country’s growing aerospace, defense, and electronics sectors are increasing demand for high-precision measurement systems. Additionally, investments in domestic metrology capabilities and reduction of reliance on imported technologies further fuel market growth.

The Japan laser interferometer industry is expanding steadily, supported by its leadership in precision engineering, robotics, and semiconductor manufacturing. High demand from automotive, electronics, and nanotechnology industries drives adoption of laser interferometers for ultra-precise measurement and calibration. Strong focus on innovation, miniaturization, and quality control further reinforces market growth across advanced manufacturing sectors.

Key Laser Interferometer Company Insights

Some of the key players operating in the market include Renishaw PLC and Carl Zeiss AG, among others.

-

Renishaw plc provides advanced precision measurement and calibration solutions and specializes in laser interferometer systems used for machine tool calibration, semiconductor manufacturing, coordinate measuring machines (CMMs), and industrial metrology applications. The company focuses on delivering high-accuracy measurement systems that support precision engineering, automation, and quality control across global manufacturing industries.

-

Carl Zeiss AG provides high-end optical and metrology solutions and specializes in laser interferometry-based measurement systems for semiconductor manufacturing, optical inspection, industrial quality assurance, and scientific research. The company is known for its advanced precision optics technologies and integrated metrology platforms used in high-tech manufacturing and research environments.

SmarAct GmbH and 4D Technology Corporation are some of the emerging market participants in the laser interferometer market.

-

SmarAct GmbH provides high-precision motion control and metrology solutions and specializes in compact laser interferometry systems for nano positioning, semiconductor manufacturing, photonics, and nanotechnology applications. The company focuses on miniaturized, high-accuracy measurement technologies designed for advanced research and industrial automation environments.

-

4D Technology Corporation provides optical metrology and surface measurement solutions and specializes in dynamic laser interferometry systems for aerospace testing, semiconductor inspection, optics manufacturing, and precision surface analysis. The company focuses on vibration-insensitive and high-speed interferometry technologies for advanced industrial and research applications.

Key Laser Interferometer Companies:

The following key companies have been profiled for this study on the laser interferometer market

-

Renishaw plc

-

Keysight Technologies

-

Carl Zeiss AG (ZEISS Group)

-

Zygo Corporation (AMETEK)

-

Bruker Corporation

-

Mahr GmbH

-

Thorlabs, Inc.

-

SIOS Meßtechnik GmbH

-

4D Technology Corporation

-

SmarAct GmbH

Recent Developments

-

In April 2026, Zygo Corporation demonstrated advanced 3D optical metrology solutions at Optatec 2026, showcasing its latest interferometry-based systems for high-precision industrial and optical manufacturing applications.

-

In February 2026, Renishaw plc expanded its laser interferometer-based machine calibration and metrology portfolio, with a focus on improving precision motion system measurement and industrial machine performance optimization using its XL-80 laser interferometer system and related calibration solutions.

-

In January 2026, Thorlabs, Inc. announced a strategic partnership with Xanadu Quantum Technologies to develop customized optical fiber components used in photonic quantum computing systems. The collaboration focuses on improving phase and polarization stability and reducing optical loss, critical parameters closely linked to high-precision laser interferometry and optical measurement systems.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Renishaw PLC; Carl Ziess AG; Zygo Corporation

- Focus on continuous improvement of high-precision hardware and integrated software solutions.

- Maintain strong partnerships with semiconductor, aerospace, and research customers for stable demand.

- Strong technological expertise in high-accuracy measurement systems.

- Established global distribution and service networks that support reliability, calibration services, and long-term customer trust.

- Slower innovation cycles compared to agile entrants, leading to delayed adoption of newer digital and AI-enabled measurement technologies.

- High product and maintenance costs that limit penetration in price-sensitive or emerging market segments.

Emerging Players: SmarAct GmbH; 4D Technology Corporation; Thorlabs, Inc.

- Emphasis on developing cost-effective, modular, and software-driven interferometer solutions targeting new industrial and research applications.

- Aggressive adoption of digital technologies and compact system design to differentiate offerings.

- Greater agility in innovation cycles, allowing faster integration of emerging technologies.

- Ability to target niche or underserved applications with customized solutions and flexible pricing models.

- Limited brand recognition and weaker global service infrastructure compared to established competitors.

- Constraints in scaling high-end precision manufacturing.

Laser Interferometer Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 336.3 million

Market size value in 2026

USD 364.3 million

Revenue forecast in 2033

USD 629.5 million

Growth rate

CAGR of 8.1% from 2026 to 2033

Base year of estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million/ Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, type, technology, application, end use, region

Regional scope

North America Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Renishaw plc; Keysight Technologies; Carl Zeiss AG; Zygo Corporation; Bruker Corporation; Mahr GmbH; Thorlabs, Inc.; SIOS Meßtechnik GmbH; 4D Technology Corporation; SmarAct GmbH

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Laser Interferometer Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global laser interferometer market report based on component, type, technology, application, end use, and region.

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Michelson Interferometers

-

Fabry-Perot Interferometers

-

Fizeau Interferometers

-

Mach-Zehnder Interferometers

-

Others

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Homodyne Interferometry

-

Heterodyne Interferometry

-

Fiber Optic Interferometry

-

Digital / Laser Scanning Interferometry

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Precision Engineering & Metrology

-

Semiconductor Inspection & Lithography

-

Surface Topology

-

Biomedical & Healthcare Imaging

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Semiconductor and Electronics

-

Aerospace and Defense

-

Automotive

-

Industrial Manufacturing

-

Healthcare and Life Sciences

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Objective

Custom Research Modules Delivered

Strategic Value / Business Impact

Product Positioning & Competitive Intelligence

Regional demand sizing & forecasting across industrial and research markets

Customer segmentation across aerospace, semiconductor, and manufacturing sectors

Competitive benchmarking across precision metrology players

Regulatory & distribution channel assessment (standards, compliance, OEM/distributor networks)

High-growth opportunities in nanometrology, semiconductors, and ultra-precision manufacturing

Go-to-market strategy across regions and industrial verticals

Investment priorities & risk analysis in R&D and supply chain

Expansion planning into emerging advanced manufacturing markets

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline and patent review

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

The global laser interferometer market size was valued at USD 336.3 million in 2025 and is projected to reach USD 364.3 million in 2026.

The global laser interferometer market is projected to reach USD 629.5 million by 2033, growing at a compound annual growth rate (CAGR) of 8.1% from 2026 to 2033.

The hardware segment accounted for the largest market share, over 69% in 2025, owing to strong demand for high-precision optical components, including lasers, beam splitters, mirrors, detectors, and vibration isolation systems, used in industrial metrology and scientific applications.

Key players operating in the market include Renishaw plc, Keysight Technologies, Carl Zeiss AG, Zygo Corporation, Bruker Corporation, Mahr GmbH, Thorlabs, Inc., SIOS Meßtechnik GmbH, 4D Technology Corporation, and SmarAct GmbH

The market growth is primarily driven by the rising demand for ultra-precise measurement solutions across semiconductor manufacturing, aerospace, automotive, and advanced industrial production, the increasing complexity of engineering designs and tighter tolerance requirements in high-end manufacturing, and the rapid expansion of the semiconductor and electronics industry.

About the Author(s)

Sensors & Controls Research Team

Semiconductors & Electronics · Sensors & ControlsThis report was authored by the sensors & controls research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the sensors & controls segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.