- Home

- »

- Network Security

- »

-

Managed Security Services Market Size Report, 2026-2033GVR Report cover

![Managed Security Services Market (2026 - 2033)Report]()

Managed Security Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Security Type (Cloud Security, Endpoint Security, Network Security, Data Security), By Enterprise Size (Large Enterprises, SMEs), By Services, By Verticals, By Region, And Segment Forecasts

Market Size, 2025

$38.0BMarket Estimate, 2026

$41.8BMarket Forecast, 2033

$86.3BCAGR, 2026–2033

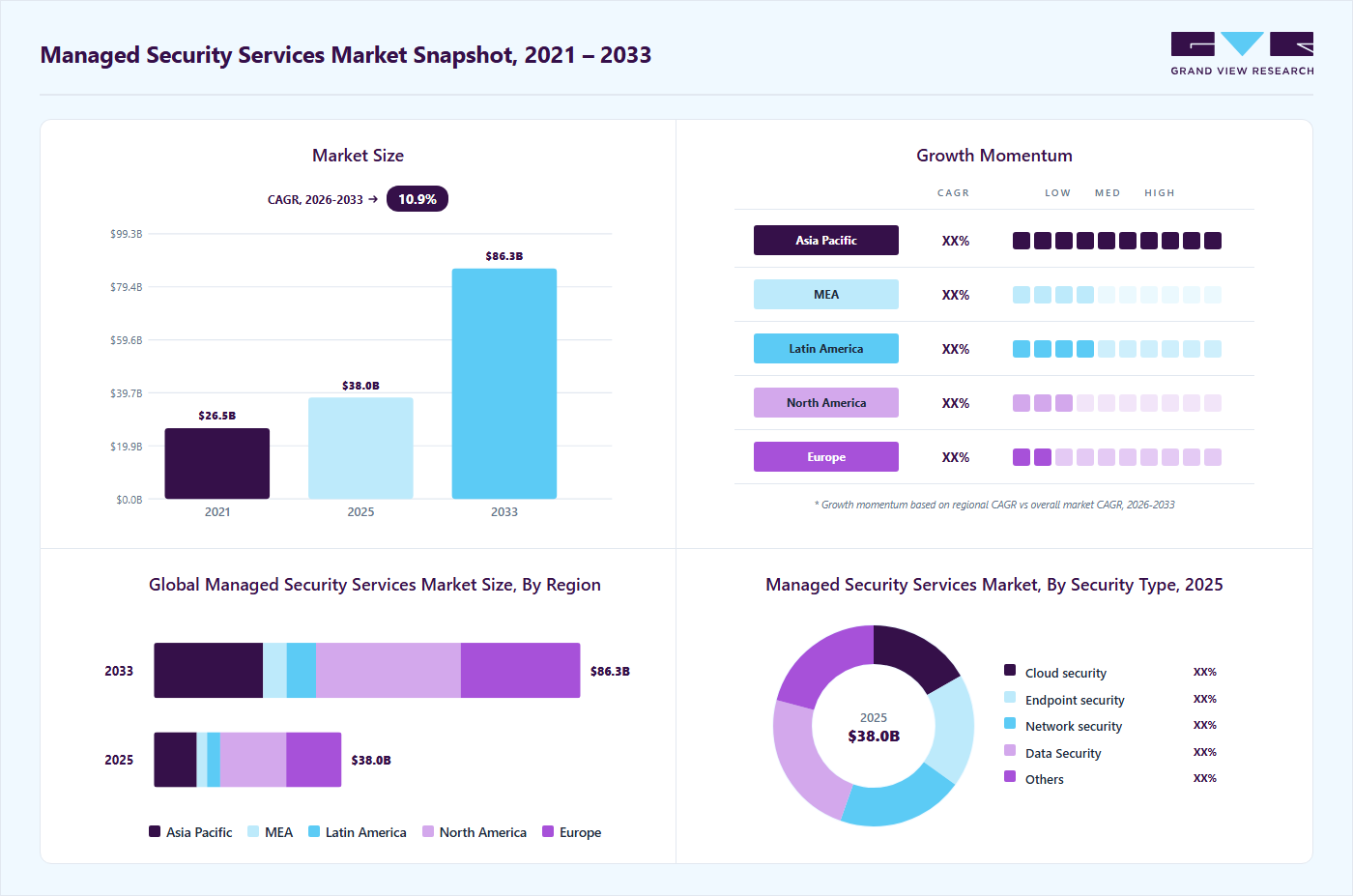

10.9%Managed Security Services Market Summary

The global managed security services market size was valued at USD 38.0 billion in 2025 and is projected to grow from USD 41.8 billion in 2026 to USD 86.3 billion by 2033, at a CAGR of 10.9% from 2026 to 2033. The market in North America dominated with a revenue share of 35.1% in 2025. The market growth is driven by the increased number of new threats, government regulations, and the proliferation of data generated by consumers.

Key Market Trends & Insights

- By security type: Data security segment held the largest market share of 23.8% in 2025.

- By services: Managed risk and compliance segment held the largest market share in 2025.

- By enterprise size: Large enterprises segment held the largest market share in 2025.

- By verticals: BFSI segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (35.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 38.0 Billion

- Estimated market size in 2026: USD 41.8 Billion

- Projected market size by 2033: USD 86.3 Billion

- CAGR (2026-2033): 10.9%

The digital movement has created a plethora of new opportunities for cyberattacks. The diversification of technology and the shortage of skilled cybersecurity laborers have created new avenues for managed security services providers. Moreover, the growing cyber threat landscape and ransomware have propelled the demand for managed security services over the forecast period. In addition, the rising adoption of cloud computing, remote working models, and increasing regulatory compliance requirements are further accelerating the Brazilian market growth.")

The managed security services capabilities include exposure assessment, detection and response, security monitoring, and operational services specific to security technology implementation and consulting. MSS providers offer a wide range of engagement models with technology-based, management-driven experiences. Managed security services have become the systematic approach to growing business requirements. Outsourcing has become prevalent and viable for many SMEs and large enterprises.

IT enterprises continuously install new technologies such as cloud computing, artificial intelligence, machine learning, DevOps, and many more to sustain and maintain balance with evolving modes. As a result, outsourcing services from managed security vendors helps organizations curtail cybersecurity threats. Moreover, managed security services encapsulate various features that enable organizations to manage and protect digital assets from cyber threats. Managed security services often integrate features, such as 24/7 threat detection, rapid threat response, remote wipes, threat hunting capabilities, device encryption, and app management, to enhance security and compliance management.

This growing need for integrated, scalable, and outcome-oriented security solutions is encouraging vendors to introduce advanced, AI-driven offerings in the market. For instance, in April 2026, NWN.ai launched an AI-enabled managed security operations suite, strengthening the market. The solution integrates MDR, ransomware protection, penetration testing, and vCISO consulting into a unified platform, addressing growing complexity, alert fatigue, and fragmented tools across hybrid IT environments. This development will accelerate demand for integrated, outcome-driven managed security services. It is also expected to intensify competition as vendors focus on AI-led automation and platform-based security models. In conclusion, the market is evolving as organizations increasingly adopt integrated and outsourced security models to address rising cyber risks and operational complexity. The growing use of advanced technologies and AI-driven solutions is enhancing efficiency, threat detection, and response capabilities.

Market Dynamics

The rising frequency of cyberattacks, ransomware incidents, data breaches, and phishing campaigns is a major market driver. Organizations are adopting managed security services to strengthen threat detection, ensure continuous network monitoring, improve incident response capabilities, and protect sensitive business data from evolving cyber threats. In addition, the rising complexity of IT environments, cloud adoption, and remote work culture are further accelerating demand for outsourced cybersecurity solutions and 24/7 security operations support.

For instance, in April 2025, the FBI Internet Crime Complaint Center (IC3) reported that cybercrime-related losses in the U.S. exceeded USD 16 billion in 2024, marking a 33% increase compared to the previous year. The report highlighted a sharp rise in phishing, extortion, and personal data breach incidents, encouraging enterprises to invest in advanced managed detection and response (MDR), security information and event management (SIEM), and threat intelligence services to enhance cybersecurity resilience. Therefore, the growing need for proactive threat management, regulatory compliance, real-time monitoring, and cost-effective cybersecurity expertise is significantly driving market growth.

Reduced control over security operations is one of the key factors restraining market growth. Organizations outsourcing cybersecurity functions to third-party managed security service providers (MSSPs) often face concerns regarding limited visibility into security processes, dependency on external vendors, delayed incident response coordination, and potential risks related to data privacy and compliance. These concerns are particularly significant among enterprises operating in highly regulated industries such as banking, healthcare, and government, where maintaining direct oversight of cybersecurity infrastructure is critical.

For instance, in November 2024, an ISACA article titled “Reassessing Risk: The Move to Third-Party Management” highlighted that 73% of leaders experienced at least one major disruption caused by a third party in recent years, emphasizing the growing concerns associated with outsourced operations and third-party risk exposure. The report further noted that organizations are reassessing external risk management strategies due to rising privacy, security, and compliance challenges linked to third-party service providers. As a result, organizations with strict internal governance and cybersecurity requirements often prefer hybrid or in-house security models, which can limit the adoption of managed security services globally.

Market Concentration & Characteristics

The managed security services industry is moderately concentrated, with the presence of several global cybersecurity companies, telecom providers, cloud service vendors, and specialized managed security service providers (MSSPs) competing across regions. The market is characterized by a high degree of innovation, driven by rapid advancements in artificial intelligence (AI), machine learning, cloud security, extended detection and response (XDR), zero-trust architecture, and security automation technologies. Vendors continuously invest in advanced threat intelligence, real-time monitoring, and automated incident response capabilities to strengthen their competitive positioning and address evolving cyber threats.

The market is witnessing a strong level of mergers, acquisitions, and strategic partnerships as companies aim to expand their cybersecurity portfolios and enhance geographic presence. In addition, stringent government regulations and data protection frameworks such as GDPR, HIPAA, PCI-DSS, and regional cybersecurity compliance mandates significantly influence market growth by increasing enterprise demand for outsourced security expertise. While certain organizations rely on in-house cybersecurity teams as a substitute for managed services, the shortage of skilled cybersecurity professionals and rising operational costs are encouraging greater adoption of MSSPs. Furthermore, the market demonstrates broad end-user concentration, with high demand originating from various sectors due to their increasing exposure to sophisticated cyberattacks and strict regulatory requirements.

Security Type Insights

The data security segment dominated the market, accounting for a 23.8% revenue share in 2025. Data security in IT firms is reaching new dimensions in managing who can access sensitive data. Enterprises can mitigate the theft risk by training employees and improving access control. In addition, the rising volume of structured and unstructured data across cloud and hybrid environments is increasing the need for robust data protection solutions. Organizations are increasingly adopting encryption, data loss prevention, and identity access management tools to strengthen security frameworks. This trend is expected to further drive the growth of the data security segment within the market.

The cloud security segment is expected to grow at the fastest CAGR during the forecast period from 2026 to 2033. Modern businesses are expected to gain momentum as enterprises continue shifting toward cloud adoption. Moreover, organizations are adopting cloud technologies to scale up with emerging technologies such as IoT, Artificial Intelligence, Machine Learning, and others by providing enhanced data storage and security measures. Moreover, the increasing demand for remote work and digital transformation initiatives is accelerating cloud-based security deployments. Organizations are leveraging cloud-native security solutions to enhance flexibility, scalability, and real-time threat monitoring. This trend is expected to significantly boost the adoption of cloud-based managed security services across industries, particularly supporting the Brazilian market growth over the forecast period.

Services Insights

The managed risk and compliance segment accounted for the largest market share in 2025. The segment's dominance can be attributed to the increasing number of cyberattacks across the globe and the stringent implementation of government regulations. The risk and compliance segment has gained traction as the organization can design strategies and implement regulations to overcome the challenges related to cyber theft. Furthermore, enterprises are increasingly focusing on continuous compliance monitoring and risk assessment to ensure adherence to evolving regulatory standards. This is driving the adoption of advanced compliance management tools and services within the market.

The managed DDoS segment is expected to experience significant growth during the forecast period from 2026 to 2033. The increasing demand for specialized skills, cost-effectiveness, scalability, and the capacity to keep up with the changing threat landscape drives the development of DDoS-managed security services. In recent years, DDoS attacks have increased in frequency and complexity. Hackers are constantly inventing new methods and resources for planning effective attacks. DDoS attacks must be efficiently addressed with specialized expertise and resources. Many businesses lack the internal knowledge and skilled security staff to prevent such attacks. Managed security services companies aim to launch dedicated staff members with in-depth knowledge of DDoS mitigation, providing a higher level of security than businesses can accomplish independently.

Enterprise Size Insights

The large enterprises segment accounted for the largest market share in 2025. Large enterprises are primarily inclined towards outsourcing services. The rise in cyberattacks, which makes large firms susceptible to unexpected losses in revenue and reputation, is another crucial market factor driving market growth. Large organizations are inclined towards managed services to lower phishing attacks, the risk of data breaches, and other cyber threats. Large organizations aim to focus more on security governance and compliance as data security and privacy rules become more important. The managed security services facilitate the development of regulations and procedures to govern access to sensitive information and access while maintaining regulatory compliance.

The SMEs segment is expected to grow at the fastest CAGR during the forecast period from 2026 to 2033. SMEs have smaller budgets than larger companies, but still need data security help. Cybersecurity companies aim to offer simple, scalable solutions to cater to SMEs' IT competence levels. SMEs need more resources to monitor their systems regularly, leaving them open to intrusions outside regular business hours. Managed security providers are coping by offering round-the-clock monitoring and rapid incident response to ensure that potential security incidents are instantly identified and fixed.

Verticals Insights

The BFSI segment accounted for the largest market share in 2025. Cloud technology has become a center for BFSI firms’ future growth and innovation strategy because of the dramatic shift toward the digital platform of engagement and transactions; banks have outsourced security services catering to their requirements within the managed security service provider market. In addition, the growing volume of sensitive financial data and rising cyber threats are compelling BFSI organizations to adopt advanced managed security solutions. This is further supported by strict regulatory requirements, driving continuous investment in security monitoring and compliance services.

The manufacturing segment is expected to register significant growth during the forecast period. The integration of Industrial IoT (IIoT), automation, and connected systems has expanded the attack surface, making robust cybersecurity essential. Manufacturers are leveraging managed security services to protect critical infrastructure, production systems, and sensitive operational data. In addition, the need to ensure business continuity and prevent costly downtime is driving demand for real-time threat monitoring and rapid incident response. Managed security providers also support compliance with industry standards and regulatory requirements. As a result, the manufacturing segment is expected to experience steady growth within the market.

Regional Insights

North America accounted for the largest market share of 35.1% in 2025 in the global managed security services market. The region is expected to remain dominant due to the increased demand for outsourcing services from several tech giants. Managed service offerings to better meet individual needs and the increasing demand for cloud computing, network security, and data security are further expected to support growth in the managed security service provider market. The growing number, variety, and complexity of cyber threats targeted at expanding exposure footprint drive market demand.

U.S. Managed Security Services Market Trends

The managed security services industry in the U.S. accounted for the largest revenue share in 2025, driven by the increasing frequency and sophistication of cyberattacks across key sectors such as BFSI, healthcare, and government. The rapid adoption of cloud computing, remote work models, and advanced technologies like artificial intelligence and IoT has significantly expanded the threat landscape, prompting organizations to rely on outsourced security expertise. The presence of leading cybersecurity vendors and high awareness of digital risks further support U.S. market expansion.

Europe Managed Security Services Market Trends

The managed security services industry in Europe is anticipated to register significant growth from 2026 to 2033, driven by increasing cyber threats, strict data protection regulations, and rapid digital transformation across industries. Countries such as Germany, France, and the UK are leading adoption due to strong regulatory frameworks like the General Data Protection Regulation and rising investments in cloud and enterprise security. The growing presence of advanced manufacturing, BFSI, and IT sectors further accelerates demand for managed security services to ensure compliance and protect critical infrastructure. As a result, the European market is expected to expand steadily, supported by regulatory pressure and the need for resilient cybersecurity frameworks.

The UK managed security services market is expected to witness significant growth over the forecast period, driven by the increasing frequency of cyberattacks and the country’s strong regulatory landscape, including data protection and cybersecurity compliance requirements. The rapid adoption of cloud computing, remote working models, and digital banking services across the UK is significantly increasing demand for advanced security monitoring and threat management solutions.

The managed security services market in France is witnessing strong growth, driven by the rising sophistication of cyber threats, increasing ransomware attacks, and the growing need for continuous security monitoring across enterprises. The rapid digital transformation of organizations, coupled with expanding cloud adoption and hybrid IT environments, is further accelerating demand for outsourced security solutions. In addition, stringent data protection regulations and compliance requirements are pushing enterprises to strengthen their cybersecurity posture through managed services. The French market is also benefiting from a shortage of skilled cybersecurity professionals, prompting organizations to rely on specialized MSS providers for advanced threat detection, incident response, and security analytics capabilities.

Asia Pacific Managed Security Services Market Trends

The managed security services industry in the Asia Pacific is expected to register the fastest CAGR from 2026 to 2033. Rising adoption of cloud computing, expanding e-commerce sectors, and government-led digital initiatives are accelerating the need for advanced security solutions. In countries like India, growing startup ecosystems and digital payment platforms are increasing demand for outsourced security services, while China and Japan are focusing on strengthening data protection frameworks and critical infrastructure security.

China managed security services market is expected to witness significant growth over the forecast period, driven by rapid digital transformation, widespread adoption of cloud computing, and the expansion of industrial internet and smart manufacturing initiatives. The increasing frequency of cyberattacks and strict government regulations around data security and cybersecurity compliance, such as data localization and network security laws, are compelling enterprises to strengthen their security frameworks.

Key Managed Security Services Company Insights

Key players operating in the industry are Fortinet, Inc., IBM, Palo Alto Networks, Fujitsu, Cisco Systems, Inc., and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In April 2026, Reinvent Telecom launched MyCloud Managed Security, a fully managed cybersecurity solution enabling partners to deliver 24/7 threat protection, vulnerability management, and MXDR services. The platform supports resellers with enterprise-grade security, compliance management, and scalable recurring revenue opportunities, addressing rising demand in the market.

-

In April 2026, HENNGE launched the second phase of its campaign to support the rollout of HENNGE Endpoint & Managed Security under its cloud-based HENNGE One platform. The solution integrates EDR, MDR, and vulnerability management, enabling enterprises to adopt Zero Trust security and strengthen cyber defense within the market. This initiative will accelerate Zero Trust adoption across enterprises and increase awareness of integrated security platforms.

-

In November 2025, Cisco introduced enhanced multi-customer management capabilities within its Security Cloud Control platform, enabling managed service providers to streamline operations and deploy hybrid mesh firewall solutions efficiently. The AI-powered platform supports centralized management, reduces operational costs, and accelerates service delivery, strengthening capabilities within the market.

Key Managed Security Services Companies:

The following key companies have been profiled for this study on the managed security services market.

- AT&T

- BAE Systems, Inc.

- Cisco Systems, Inc.

- Check Point Software Technologies

- Fortinet, Inc.

- Fujitsu

- IBM

- Palo Alto Networks

- Rapid 7

- Verizon

- Wipro

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: IBM; AT&T; Verizon; Cisco Systems, Inc.; Fujitsu; Wipro; BAE Systems, Inc.

- Leveraging broad IT and telecom portfolios to offer "all-in-one" managed services that include connectivity, cloud migration, and security.

- Maintaining a massive physical network of 24/7 Security Operations Centers (SOCs) to address data residency and sovereign security requirements.

- Using high-level advisory and digital transformation services to secure long-term, multi-year managed security contracts.

- Strong experience in handling mission-critical infrastructure for the world’s largest organizations and government agencies.

- Telecom leaders (AT&T, Verizon) utilize carrier-grade visibility to identify and mitigate threats at the backbone level before they reach the client network.

- Unmatched human capital, providing thousands of on-the-ground consultants for manual remediation and complex compliance audits.

- Their massive scale can lead to a "cookie-cutter" service model that feels impersonal or slow to adapt to niche client needs.

- Internal silos often result in slower response times for deploying cutting-edge features compared to agile, product-focused competitors.

- Maintaining vast physical infrastructure often leads to higher price points, making them less competitive in the mid-market.

Emerging Players: Palo Alto Networks; Fortinet, Inc.; Check Point Software; Rapid7

- Aggressively moving clients toward consolidated platforms that combine networking and security into a single, cloud-delivered stack.

- Investing heavily in "Autonomous SOC" technology to replace manual log-checking with machine-speed threat hunting and response.

- Building API-first ecosystems that allow for rapid deployment and interoperability with diverse third-party cloud environments.

- Consistently leading in technical benchmarks for threat detection, particularly in cloud native and Zero Trust architectures.

- Ability to ship updates and respond to emerging threats (like Generative AI attacks) significantly faster than infrastructure-heavy giants.

- Leveraging automation to provide premium security outcomes with fewer billable human hours, appealing to high-growth enterprises.

- Their "platforms" are often designed to work best within their own software stack, making multi-vendor management difficult for clients.

- Lack the workforce to manage a client’s entire non-security IT infrastructure.

- While they have elite researchers, they often lack the "boots on the ground" volume required for massive, manual international remediation projects.

Managed Security Services Market Report Scope

Report Attribute

Details

Market size in 2025

USD 38.0 billion

Estimated market size in 2026

USD 41.8 billion

Projected market size by 2033

USD 86.3 billion

Growth rate

CAGR of 10.9% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Security type, services, enterprise size, verticals, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

AT&T; BAE Systems, Inc.; Cisco Systems, Inc.; Check Point Software Technologies; Fortinet, Inc.; Fujitsu; IBM; Palo Alto Networks; Rapid 7; Verizon; Wipro

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Managed Security Services Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global managed security services market report based on security type, services, enterprise size, verticals, and region:

-

Security Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud security

-

Endpoint security

-

Network security

-

Data Security

-

Others

-

-

Services Outlook (Revenue, USD Billion, 2021 - 2033)

-

Managed SIEM

-

Managed UTM

-

Managed IDPS

-

Managed DLP

-

-

Managed DDoS

-

Managed XDR

-

Managed IAM

-

Managed Risk and Compliance

-

Infrastructure Protection

-

Others

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

Verticals Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

Manufacturing

-

IT& Telecom

-

Retail

-

Defense/Government

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

The market entry and competitive assessment for a cloud security vendor

Analysis of regional cybersecurity spending and managed services adoption trends

Competitive benchmarking of regional and global MSSPs

Identified regional growth opportunities

Supported go-to-market and partnership strategies

Industry-specific managed security services demand analysis for the BFSI and healthcare sectors

Assessment of cybersecurity challenges and compliance requirements in the BFSI and healthcare industries

Analysis of demand for data protection, threat detection, and regulatory compliance services

Identified sector-specific growth opportunities

Highlighted key security investment priorities among end users

Regional managed detection and response (MDR) adoption study for enterprise clients

Evaluation of MDR adoption trends across North America, Europe, and the Asia Pacific

Analysis of key deployment preferences, pricing models, and threat monitoring requirements

Identified high-potential regional markets for MDR services

Provided insights into customer preferences and evolving threat management needs

Frequently Asked Questions About This Report

The global managed security services market size was valued at USD 38.0 billion in 2025 and is estimated at USD 41.8 billion for 2026.

The global managed security services market is expected to grow at a CAGR of 10.9% from 2026 to 2033, reaching USD 86.3 billion by 2033.

North America dominated with a 35.1% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include AT&T; BAE Systems, Inc.; Cisco Systems, Inc.; Check Point Software Technologies; Fortinet, Inc.; Fujitsu; IBM; Palo Alto Networks; Rapid 7; Verizon; Wipro

Key factors that are driving the managed security services market growth include elements of digital business such as cloud computing, mobile computing, BYOD and Internet of Things (IoT) are gaining popularity across the world.

The data security segment led with a 23.8% revenue share in 2025, while the cloud security segment is the fastest-growing.

The managed risk and compliance segment held the largest revenue share in 2025, while the managed DDoS segment is the fastest-growing.

The large enterprises segment held the largest revenue share in 2025, while the SMEs segment is the fastest-growing.

The BFSI segment held the largest revenue share in 2025, while the manufacturing segment is the fastest-growing.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.