- Home

- »

- Next Generation Technologies

- »

-

Micro-location Technology Market Size, Industry Report 2033GVR Report cover

![Micro-location Technology Market Size, Share & Trends Report]()

Micro-location Technology Market (2025 - 2033) Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Technology (Bluetooth Low Energy, Ultra-wideband, RFID), By Deployment, By Application, By End-use, By Region, And Segment Forecasts

Market Size, 2024

$33.0BMarket Estimate, 2026

$37.9BMarket Forecast, 2033

$134.0BCAGR, 2025–2033

17.1%Micro-location Technology Market Summary

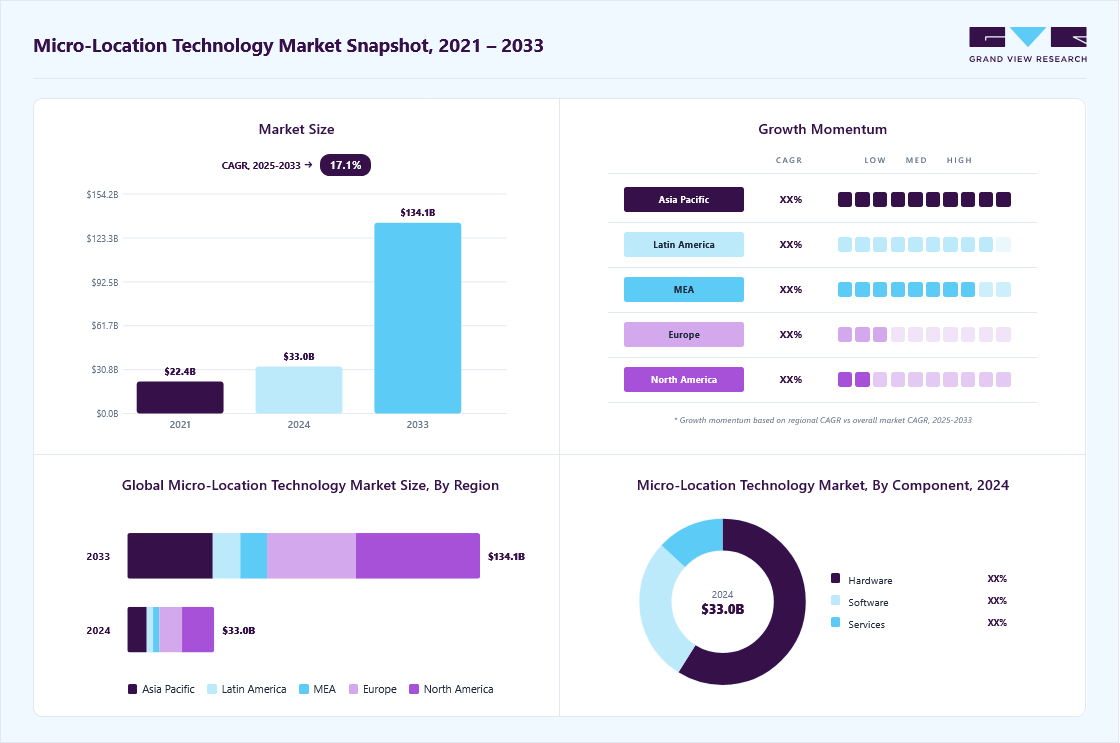

The global micro-location technology market size was estimated at USD 33.01 billion in 2024 and is projected to reach USD 134.04 billion by 2033, growing at a CAGR of 17.1% from 2025 to 2033. Key trend driving the market growth is the shift toward cloud-native, AI-driven micro-location platforms that analyze spatial data for decision automation and workflow optimization.

Key Market Trends & Insights

- North America held a 37.0% revenue share of the global micro-location technology market in 2024.

- In the U.S., the market is driven by the integration of high-precision BLE and UWB into both enterprise and consumer ecosystems.

- By component, the hardware segment held the largest revenue share of 58.8% in 2024.

- By technology, the Bluetooth Low Energy (BLE) segment held the largest revenue share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 33.01 Billion

- 2033 Projected Market Size: USD 134.04 Billion

- CAGR (2025-2033): 17.1%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

The shift toward cloud-native, AI-driven micro-location platforms is significantly accelerating market growth by transforming raw spatial data into actionable intelligence that automates decisions and optimizes workflows across industries. These platforms enable real-time tracking of assets, people, and environmental conditions, and use AI to dynamically route resources, trigger alerts, and generate predictive insights, reducing manual intervention and improving operational efficiency. With seamless scalability and integration into enterprise systems, such platforms are especially attractive in sectors like healthcare, logistics, and manufacturing where downtime and inefficiency have high costs.The integration of high-accuracy indoor positioning systems such as Bluetooth Low Energy (BLE), Ultra-Wideband (UWB), and Radio Frequency Identification (RFID) into IoT ecosystems is a key driver for micro-location technology market growth. This integration enhances real-time visibility into the movement and status of assets, personnel, and equipment within complex facilities. In addition, these systems deliver centimeter-to-meter level precision, enabling organizations to accurately track the location, condition, and usage patterns of high-value assets, reducing the time and resources spent on manual searches and mitigating the risk of asset misplacement or theft.

")

For instance, in September 2022, Zebra Technologies announced that its MotionWorks Enterprise platform which aggregates BLE and RFID data was integrated with ServiceNow’s Hardware Asset Management solution to enhance workflow visibility across manufacturing, logistics, healthcare, and retail environments. This integration provides real‑time lifecycle, location, and movement insights, allowing organizations to trigger automated workflows, alerts, and service tickets based on spatial data. Therefore, the adoption of precise location technologies into IoT frameworks is contributing significantly in driving the market growth.

Component Insights

The hardware segment accounted for the largest revenue share of 58.8% in 2024 in the market, primarily due to the essential role of physical devices such as BLE beacons, UWB tags, RFID readers, gateways, sensors, and anchors that form the backbone of real-time location systems (RTLS). These components are critical for enabling high-accuracy spatial data capture, device-to-device communication, and environment-aware location tracking across a wide range of industries. In addition, the rising demand for edge-enabled tracking devices that can support real-time analytics and automation directly at the source is also boosting the market share. Consequently, organizations are prioritizing faster decision-making, lower latency, and reduced reliance on centralized cloud systems, driving a strong shift toward intelligent hardware capable of capturing, processing, and acting on spatial data directly at the edge. For instance, in December 2024, Dot Ai unveiled its ZiM edge-IoT bridge, designed to streamline asset management by combining support for both passive transponders and active beacons within a single device. Equipped with signal LEDs and I/O ports for environmental sensors, ZiM enables real-time data collection and localized processing at the edge, empowering businesses to track assets and optimize workflows without relying solely on back-end servers.

The software segment is expected to register a fastest growth during the forecast period, driven by its central role in transforming raw spatial data into actionable intelligence for real-time decision-making, automation, and workflow optimization. In addition, organizations are adopting micro-location technologies to streamline asset tracking, indoor navigation, and workforce management, by enabling integration of multi-sensor inputs and AI-powered vision into unified dashboards with advanced analytics and geospatial intelligence.

Moreover, the segment is further propelled by the shift toward cloud-native, edge-compatible architectures that offer scalable deployment, cross-platform interoperability, and reduced latency for distributed facility operations. For instance, in October 2024, Navbea launched hybrid RTLS software suite that integrates BLE, UWB, GPS, and AI-enabled cameras, providing a consolidated interface for real-time asset and personnel tracking, sensor interoperability, and intelligent workflow automation. This flexible and modular software reflects the growing demand for intelligent platforms that not only track but also respond to spatial dynamics. Subsequently, the above-mentioned advantages including enhanced operational efficiency, safety and seamless integration into enterprise systems is accelerating the adoption of micro-location software solutions.

Technology Insights

The Bluetooth Low Energy (BLE) segment accounted for the largest revenue share in 2024, due to its unique blend of affordability, energy efficiency, and seamless integration with existing consumer and enterprise ecosystems. BLE beacons offer reliable room-level accuracy while boasting low maintenance, extended battery life, and effortless deployment through smartphones and IoT devices. This positions BLE as the preferred technology for applications such as proximity marketing in retail, asset tracking in logistics, and patient flow monitoring in healthcare where affordability and seamless integration with existing systems are critical requirements. For instance, in January 2021, Kontakt.io announced its integration with Cisco DNA Spaces, enabling all Cisco access points to function as BLE gateways. This partnership allows organizations to onboard hundreds of thousands of BLE devices with a single click covering smart badges, asset tags, and sensors while delivering secure, two-way communication, device lifecycle management, and location-based services on an enterprise scale. Therefore, such integrations highlight that BLE are essential not only as a sensor layer but as a scalable, cloud-enabled infrastructure foundation that supports rapid adoption in large-scale commercial deployments.

The Ultra-Wideband (UWB) segment is expected to grow at the fastest growth rate during the forecast period, owing to its exceptional spatial accuracy, low latency, and strong resistance to signal interference, ideal for precision-critical applications in industrial automation, logistics, healthcare, and smart infrastructure. In addition, UWB’s ability to deliver real-time, centimeter-level positioning far exceeds that of BLE or Wi-Fi, enabling use cases such as worker safety zones, autonomous vehicle navigation, and robotic coordination in dynamic environments.

Moreover, another key factor accelerating this growth is UWB’s integration into mainstream consumer and enterprise ecosystems, enhancing interoperability and broadening its application scope. For instance, in October 2021, Qorvo announced that its UWB solutions are interoperable with Apple’s U1 chip, enabling a new generation of location-aware experiences across smart home, automotive, and mobile devices. Therefore, this strategic alignment with major tech platforms highlights UWB’s expanding relevance in both industrial and consumer domains, strengthening its position for ultra-precise, real-time micro-location services.

Deployment Insights

On-premises segment accounted for the largest revenue share of 68.3% in 2024, due to its dominance in sectors where data privacy, security, and infrastructure control are paramount such as healthcare, defense, manufacturing, and critical infrastructure. Organizations in these industries require full ownership of location data and prefer local server-based deployments to ensure compliance with regulatory standards, reduce external dependencies, and enable real-time processing without internet connectivity. In addition, on-premises systems offer greater customization and integration flexibility with existing enterprise resource planning (ERP), asset management, and facility control systems, ideal for legacy-heavy environments. Moreover, the need for low-latency location intelligence in critical operations, such as patient tracking in hospitals or machine-level monitoring in industrial plants, further drives adoption. Subsequently, the aforementioned factors are contributing significantly substantially in accelerating the micro-location technology market size.

The cloud-based segment is predicted to witness the highest CAGR from 2025 to 2033 owing to the growing demand for scalable, cost-efficient, and remotely accessible micro-location solutions that support real-time spatial analytics and seamless system updates. These platforms eliminate heavy upfront infrastructure costs, ideal for SMEs and multi-site enterprises that require consistent location intelligence across facilities. In addition, cloud deployments integrate swiftly with AI, IoT, and enterprise IT systems enabling dynamic geofencing, workflow-triggered alerts, and unified data dashboards.

For instance, in September 2024, Crowdkeep partnered with Veea to deliver a hybrid edge-cloud solution for construction, healthcare, logistics, and education sectors. Their integrated platform combines real-time data captured at the edge with cloud-based management, enabling enterprises to optimize operations and enhance safety through intelligent spatial orchestration. Consequently, these advancements highlight the growing preference for cloud-based micro-location deployments as organizations prioritize operational flexibility, centralized visibility, and rapid scalability to support evolving business and infrastructure needs.

Application Insights

The asset tracking & management segment accounted for the largest revenue share in 2024, reflecting the need for real-time asset visibility across industries such as healthcare, logistics, manufacturing, and retail. Micro-location technologies such as BLE, UWB, RFID, and GPS enable organizations to precisely monitor high-value equipment, tools, and inventory, reducing time spent searching, minimizing theft or misplacement, and maximizing resource utilization. This demand is further strengthened by integration with systems such as ERP, CMMS, and IoT platforms, facilitating predictive maintenance, lifecycle management, and compliance tracking. For example, in July 2024, Samsara launched its Asset Tag, an enterprise-grade BLE tracker designed to monitor high-value tools and equipment. Integrated with the Samsara Network, this asset tag delivers real-time location tracking, significantly reducing downtime and costs associated with asset misplacement. This new solution underscores the tangible operational and financial benefits driving organizations to invest in micro-location asset tracking systems.

The proximity marketing segment is expected to register the fastest growth over the forecast period, driven by the surge in demand for context-aware customer engagement through real-time, location-triggered interactions. Retailers, airports, hotels, and event venues are deploying BLE beacons, NFC tags, and geofencing to deliver personalized offers, targeted notifications, and content prompts that align with shoppers' exact in-store or on-site locations, enhancing dwell time, boosting conversion rates, and strengthening omnichannel loyalty. For instance, in April 2022, Oriient partnered with Google Cloud to integrate its AI-powered, sensor-free indoor positioning technology into the Google Cloud Marketplace, giving retailers access to features like product locators, optimized shopping routes, foot-traffic analytics, and location-based promotions. Consequently, these developments highlight the application of micro‑location data to create immersive, context-rich experiences that add measurable value to customer engagement strategies.

End-use Insights

The retail segment accounted for the largest revenue share in 2024, driven by the increasing adoption of micro-location technologies to enhance customer experience, operational efficiency, and omnichannel integration. Retailers are deploying BLE beacons, RFID, and AI-driven indoor positioning to enable real-time foot traffic analysis, smart shelf monitoring, queue management, and location-based promotions, helping them personalize in-store experiences, increase conversion rates, and optimize layout strategies. In addition, with growing competition from e-commerce, brick-and-mortar retailers are leveraging micro-location data to bridge the digital-physical gap, delivering dynamic, app-based guidance and offers tailored to individual shopping behavior. This shift is also enabling seamless integration with loyalty programs, mobile wallets, and interactive displays, creating a unified, data-rich customer journey. Moreover, the adoption of edge-enabled location services allows retailers to respond to shopper movement in real time, improving responsiveness and in-store engagement. In conclusion, the above-mentioned factors are contributing remarkably in driving the growth of retail sector in the global micro-location technology market.

The healthcare segment is expected to register the fastest growth during the forecast period, driven by the growing need for real-time visibility, patient and staff safety, and operational efficiency within hospitals and medical facilities. Micro‑location technologies such as BLE, RFID, and UWB are being widely adopted to support critical applications such as asset tracking for life‑saving equipment, patient and staff monitoring, infant and wander protection, and infection control through contact tracing. These systems enable healthcare providers to locate resources instantly, reduce equipment loss, minimize wait times, and automate workflows leading to safer, more economical patient care. For instance, in March 2025, CenTrak introduced a plug-and-play BLE platform that can integrate with its existing RTLS suite offering hospitals flexible deployment options across BLE-only, multi-mode, and clinical-grade locating networks. This addition supports applications such as staff duress alerts, infant protection zones, hand hygiene compliance, and asset tracking via a unified, interoperable interface enabling healthcare facilities to scale up or refine their systems without replacing existing investments

Regional Insights

North America accounted for the largest market share of 37.0% in 2024 in the global micro-location technology market, driven by strong institutional demand across healthcare, retail, and industrial sectors, as well as the region’s advanced IT infrastructure and early adoption of location-based technologies. The U.S. healthcare system is rapidly deploying BLE and RFID-based RTLS solutions for patient tracking, asset management, and hygiene compliance, while major retailers such as Walmart and Target are investing in AI-powered proximity marketing and indoor analytics platforms to enhance in-store experiences. In addition, the widespread rollout of 5G and edge computing across logistics and manufacturing hubs is accelerating the deployment of high-accuracy UWB and hybrid positioning systems for asset visibility and workforce safety. Supportive government initiatives promoting smart infrastructure and workplace safety standards, coupled with strong vendor presence including Cisco, Zebra Technologies, and CenTrak are strengthening North America’s leadership in the micro-location technology market.

U.S. Micro-location Technology Market Trends

The U.S. micro-location technology market is witnessing rapid advancement driven by the integration of high-precision BLE and UWB into both enterprise and consumer ecosystems. In 2025, Google enhanced the indoor tracking capabilities of its Pixel Watch 3 by introducing Bluetooth 6.0 Channel Sounding via Wear OS 5.1, enabling centimeter-level accuracy without dedicated UWB hardware-an innovation set to accelerate BLE-based consumer adoption. Simultaneously, Google rebranded its “Find My Device” app to “Find Hub” and introduced UWB support for directional and distance-aware tracking, expanding its smart tracker ecosystem to compete with Apple and Samsung. On the enterprise front, U.S.-based companies such as Cisco, Zebra Technologies, and Aruba are embedding RTLS into network infrastructure across hospitals, warehouses, and retail chains to enable precise asset tracking, staff safety alerts, and intelligent space utilization. These developments, combined with 5G rollout and strong investment in smart infrastructure, are making the U.S. a global leader in commercializing micro-location solutions across both consumer and industrial domains.

Europe Micro-location Technology Market Trends

Micro-location technology market in Europe is anticipated to register considerable growth from 2025 to 2033, driven by rising investments in smart infrastructure, strict regulatory emphasis on operational transparency, and rapid digitalization across sectors. Countries like Germany, the UK, and France are leading adoption, with hospitals deploying BLE- and RFID-based RTLS to enhance patient safety and asset utilization, while retailers leverage proximity marketing and indoor navigation tools to enrich in-store customer journeys. For instance, Infsoft GmbH launched a modular BLE and UWB platform tailored for European logistics and healthcare sectors, integrating real-time asset tracking with GDPR-compliant data management tools. In addition, the region’s push toward Industry 5.0 and worker safety is accelerating the adoption of UWB-enabled positioning systems in smart factories, especially in Central and Northern Europe. Consequently, these targeted, regulation-aligned deployments are making Europe a key growth engine for high-accuracy, privacy-conscious micro-location solutions.

The UK micro-location technology market is poised for robust growth from 2025 to 2033, driven by increasing adoption across logistics, manufacturing, and healthcare sectors that demand high-accuracy indoor positioning for operational efficiency and safety. In logistics and warehousing, micro-location solutions are being deployed to enable real-time inventory tracking, automated asset management, and worker location monitoring, especially within high-density fulfillment centers. In addition, the manufacturing sector is integrating UWB and BLE-based systems into smart factories to optimize equipment utilization, enable predictive maintenance, and support safe human-machine interactions. Moreover, government initiatives supporting smart building innovation and digital twin infrastructure are accelerating demand for micro-location systems that provide granular spatial data and analytics within commercial and public spaces in the UK.

The Germany micro-location technology industry is undergoing rapid transformation from 2025 to 2033, with several distinct, region-specific trends shaping its trajectory. A major driver is the emergence of hybrid BLE/UWB beacons, such as the infsoft Locator Beacon developed in Ingolstadt, which enables enterprises to achieve high-precision tracking (within 30 cm) while maintaining low installation complexity and long battery life, ideal for industries like automotive, pharmaceuticals, and building management. In addition, Germany's strong position in industrial automation and logistics is further supported by increasing adoption of UWB-based RTLS systems in manufacturing plants and warehouses, paired with AI-enhanced asset flow analytics to optimize efficiency and safety.

Asia Pacific Micro-location Technology Market Trends

Asia Pacific is expected to register the fastest CAGR of 18.2% from 2025 to 2033 in the micro-location technology market, fueled by large-scale smart infrastructure development. In addition, the region is witnessing strong demand from logistics hubs, mega-retail environments, and healthcare networks, where real-time location tracking is being integrated to optimize asset utilization, patient flow, and workforce productivity. Moreover, government-led digitization programs such as India’s Digital Health Mission and China’s Smart Hospital Blueprint are accelerating healthcare RTLS deployment, while Southeast Asia’s growing e-commerce and retail ecosystems are driving the uptake of proximity marketing and indoor navigation technologies. These sector-specific drivers, combined with cost-effective technology rollout and growing vendor ecosystems, are positioning Asia Pacific as the fastest-growing region in the global micro-location technology landscape.

Japan's micro-location technology industry is on a strong upward trajectory from 2025 to 2033, driven by rapid integration that demand precise indoor positioning and automation. In manufacturing, UWB-enabled RTLS platforms are being widely adopted within advanced assembly lines to facilitate real-time tool tracking, predictive maintenance, and safety protocols that support the country's push toward Industry 5.0 and autonomous production. Healthcare institutions are increasingly implementing BLE- and RFID-based patient and equipment tracking systems to streamline hospital workflows, enhance patient care, and reinforce hygiene monitoring in compliance with Japan's stringent safety standards.

China’s micro-location technology industry held a substantial share in 2024, driven by digital infrastructure expansion, national smart city programs, and large-scale industrial automation. The country is witnessing widespread adoption of BLE and RFID technologies across urban hospitals and elderly care facilities for patient tracking, asset management, and infection control as part of its Smart Hospital initiatives. In addition, under the "Made in China 2025" strategy, manufacturing zones are integrating micro-location systems for predictive maintenance and safety monitoring in smart factories.

Key Micro-location Technology Company Insights

Key players operating in the Micro-Location Technology Industry Apple Inc., Google LLC, Cisco Systems, Inc., Aruba Networks, Inc. and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In June 2025, Cisco’s unveiled secure network architecture is designed to support AI and IoT initiatives, including micro-location technologies, by providing unified management, enhanced security, and high-performance networking tailored for real-time data and device connectivity in workplaces. This architecture enables more reliable and scalable micro-location deployments across campus, branches, and industrial environments, facilitating precise tracking and automation critical to the micro-location technology market.

-

In March 2025, Zebra Technologies unveiled advanced solutions that leverage micro-location technologies such as RFID and AI-powered automation to enhance asset visibility, streamline workflows, and improve inventory management across retail, warehousing, and supply chain operations. These innovations, including enhanced scanning and tracking devices, support precise real-time location tracking and intelligent automation, reinforcing Zebra’s leadership in the micro-location technology market by enabling smarter, more efficient frontline operations.

-

In January 2021, Kontakt.io’s partnered with Cisco DNA Spaces to expand scalable BLE IoT services, enabling seamless device management and enhanced indoor location solutions, thereby strengthening Cisco’s leadership and accelerating adoption in the micro-location technology market across industries.

Key Micro-location Technology Companies:

The following are the leading companies in the micro-location technology market. These companies collectively hold the largest market share and dictate industry trends.

- Apple Inc.

- Google LLC

- Cisco Systems, Inc.

- Aruba Networks, Inc.

- Zebra Technologies Corporation

- Estimote, Inc.

- Here Technologies

- Qualcomm Technologies, Inc.

- Ubisense Group PLC

- Mist Systems (Juniper Networks)

- Kontakt.io

- Humatics Corporation

- Ruckus Networks, Inc.

- CenTrak, Inc.

- Siemens AG

Micro-location Technology Market Report Scope

Report Attribute

Details

Market size in 2025

USD 37.87 billion

Revenue forecast in 2033

USD 134.04 billion

Growth rate

CAGR of 17.1% from 2025 to 2033

Actual data

2021 - 2024

Forecast period

2025 - 2033

Quantitative units

Revenue in USD billion, and CAGR from 2025 to 2033

Report Application

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, technology, deployment, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Apple Inc.; Google LLC; Cisco Systems, Inc.; Aruba Networks, Inc.; Zebra Technologies Corporation; Estimote, Inc.; Here Technologies; Qualcomm Technologies, Inc.; Ubisense Group PLC; Mist Systems (Juniper Networks); Kontakt.io; Humatics Corporation; Ruckus Networks, Inc.; CenTrak, Inc.; Siemens AG

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Micro-location Technology Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global micro-location technology market report based on component, technology, deployment, application, end-use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

Managed Services

-

Professional Services

-

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

Bluetooth Low Energy (BLE)

-

Ultra-Wideband (UWB)

-

Wi-Fi

-

RFID

-

Near Field Communication (NFC)

-

ZigBee

-

Magnetic Positioning

-

Infrared

-

Others

-

-

Deployment Mode Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premise

-

Cloud-Based

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Asset Tracking & Management

-

Proximity Marketing

-

Indoor Navigation

-

Workflow Optimization

-

Emergency & Security Management

-

People Tracking

-

Augmented Reality & Gaming

-

Others

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Education

-

Healthcare

-

Retail

-

Government and Public Sector

-

Sports & Entertainment

-

Manufacturing

-

Travel & Hospitality

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global micro-location technology market size was estimated at USD 33.01 billion in 2024 and is expected to reach USD 37.87 billion in 2025.

The global micro-location technology market is expected to grow at a compound annual growth rate of 17.1% from 2025 to 2033 to reach USD 134.04 billion by 2033.

The retail segment accounted for the largest revenue share of 23.02% in 2024, driven by the increasing adoption of micro-location technologies to enhance customer experience, operational efficiency, and omnichannel integration.

Some key players operating in the market include Apple Inc., Google LLC, Cisco Systems, Inc., Aruba Networks, Inc., Zebra Technologies Corporation, Estimote, Inc., Here Technologies, Qualcomm Technologies, Inc., Ubisense Group PLC, Mist Systems (Juniper Networks), Kontakt.io, Humatics Corporation, Ruckus Networks, Inc., CenTrak, Inc., Siemens AG and Others.

Factors such as the shift toward cloud-native, AI-driven micro-location platforms that analyze spatial data for decision automation and workflow optimization plays a key role in accelerating the micro-location technology market.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.