- Home

- »

- Next Generation Technologies

- »

-

MicroLED Interconnect Market Size Report, 2026-2033GVR Report cover

![MicroLED Interconnect Market (2026 - 2033)Report]()

MicroLED Interconnect Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (GPU-to-GPU, Chip-to-Chip), By Data Rate (Less than 25 Gbps, More than 100 Gbps), By Distance (Less than 1 meter, 1- 5 meter), By Region, And Segment Forecasts

Market Size, 2025

$181.6MMarket Estimate, 2026

$225.0MMarket Forecast, 2033

$722.0MCAGR, 2026–2033

18.1%MicroLED Interconnect Market Summary

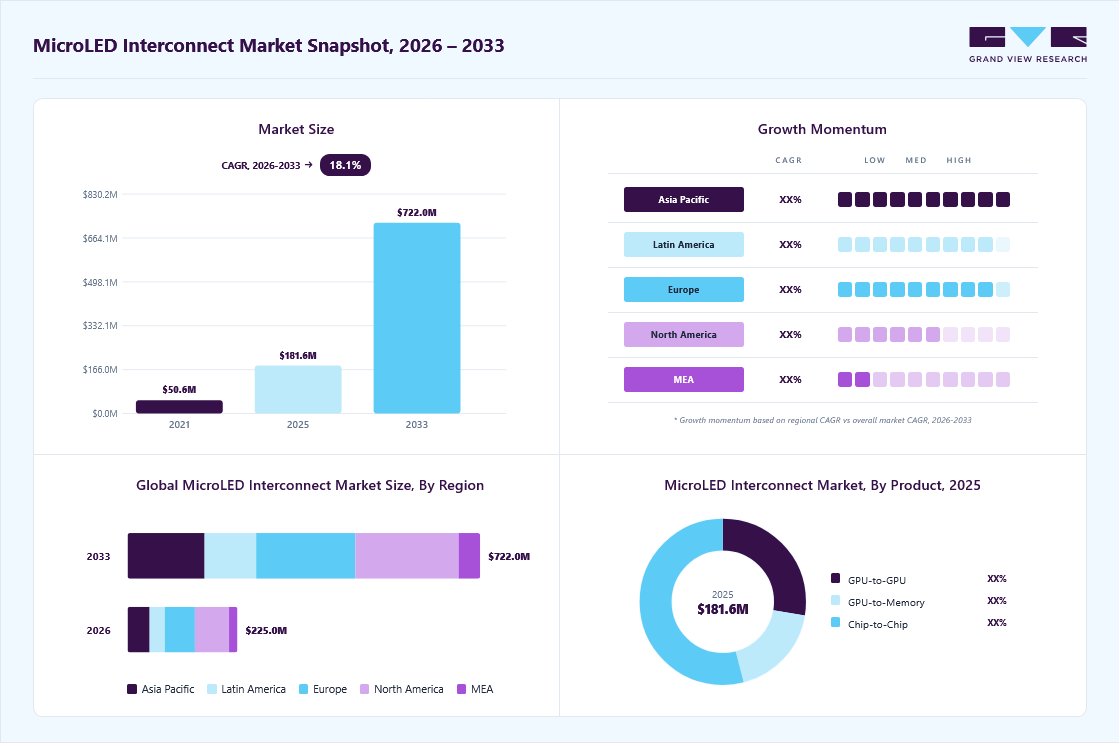

The global MicroLED interconnect market size was valued at USD 181.6 million in 2025 and is projected to grow from USD 225.0 million in 2026 to USD 722.0 million by 2033, at a CAGR of 18.1% from 2026 to 2033. The market in North America dominated with a revenue share of 31.3% in 2025. The market is driven by growing demand for high-performance and low-power data transfer solutions.

Key Market Trends & Insights

- By product: Chip-to-chip segment held the largest market share of 54.1% in 2025.

- By distance: Less than 1 meter segment held the largest market share of 47.1% in 2025.

- By data rate: Less than 25 gbps segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (31.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 181.6 Million

- Estimated market size in 2026: USD 225.0 Million

- Projected market size by 2033: USD 722.0 Million

- CAGR (2026-2033): 18.1%

Applications in AI, high-performance computing, and data centers are key contributors. Companies are focusing on providing high-bandwidth interconnect technologies. This demand is accelerating innovation and adoption in the sector. The MicroLED interconnect industry is moving toward high-performance, energy-efficient solutions. Companies are focusing on developing modular and scalable architectures to support larger, more complex systems. There is a strong emphasis on ultra-high-density chip-to-chip connections for improved efficiency. Demand is rising for low-power, sustainable interconnect technologies in advanced applications. The market is increasingly adopting optical and photonic approaches to meet the needs of next-generation AI and high-performance computing. For instance, in March 2025, AvicenaTech, Corp. introduced its modular and scalable LightBundle microLED interconnect platform, offering ultra-high-density chip-to-chip connections with high energy efficiency. The platform aims to support large AI GPU clusters across multiple racks while overcoming the reach limitations of current copper interconnects.")

The expansion of optical and photonic interconnect approaches is gaining momentum to overcome reach limitations and enable high-speed communication. These technologies provide faster data transmission compared to traditional electrical interconnects, supporting the growing demands of AI and high-performance computing systems. By leveraging light-based communication, they reduce signal loss and improve energy efficiency across long distances. Optical and photonic interconnects allow for higher bandwidth and lower latency, which is essential for large-scale GPU clusters and data centers. Their modular designs make them adaptable to various system architectures, including co-packaged and pluggable solutions. These approaches are driving the development of more efficient, scalable, and high-speed computing infrastructure.

The integration of MicroLED interconnects is increasingly being adopted in AI clusters, data centers, and next-generation high-performance computing systems. These interconnects offer enhanced data transfer speeds and improved energy efficiency, which are critical for managing large-scale computations. By enabling ultra-dense chip-to-chip connections, they help overcome the limitations of traditional copper interconnects. Their modular and scalable design allows for flexible deployment across multiple racks and hardware configurations. This technology supports the growing computational demands of AI workloads and machine learning applications. It also facilitates more efficient communication between GPUs and other processing units within large clusters. Companies are investing in MicroLED interconnects to optimize system performance while reducing power consumption. Overall, these interconnects are driving the advancement of high-performance, energy-efficient computing infrastructure.

Product Insights

The chip-to-chip segment accounted for the largest market revenue share of over 54.1% in 2025, primarily due to its early adoption in experimental and prototype-level deployments. This interconnect type involves the shortest physical distances, generally within the same package or board, making it the starting point for microLED-based optical link integration. Given the compact size and directional emission of microLEDs, chip-to-chip links benefit from low power consumption, minimal signal loss, and simplified alignment requirements compared to longer-range applications. Moreover, as chiplet architectures gain momentum, the need for fine-pitch, low-latency chip-to-chip optical links is growing, further supporting the dominance of this segment in the early commercialization phase.

The GPU-to-memory segment is expected to grow at the fastest CAGR over the forecast period due to the rising demand for high-bandwidth, low-latency data transfer between compute units and memory modules in AI and high-performance computing (HPC) systems. MicroLED-based optical interconnects offer solutions by enabling energy-efficient, high-speed links that support bandwidths exceeding 100 Gbps, for near-memory and stacked-memory configurations such as HBM (High Bandwidth Memory). Furthermore, emerging memory-centric architectures and the increasing adoption of co-packaged optics in accelerator designs are creating favorable conditions for microLED adoption in this segment. As chipmakers invest in next-gen GPU-memory subsystems, the demand for compact, high-speed interconnects like microLEDs is expected to surge, driving this segment’s accelerated growth.

Data Rate Insights

The less than 25 Gbps segment accounted for the prominent market revenue share in 2025 due to the early-stage commercialization and technology readiness of microLED-based interconnects. At this stage, most microLED optical links are limited to modest modulation speeds suitable for short-reach, low-bandwidth applications such as chip-to-chip and basic board-level communication. These implementations are easier to achieve with existing microLED driver capabilities and require less complex packaging and thermal management. Moreover, the <25 Gbps range aligns well with proof-of-concept deployments, test environments, and early adoption in compact systems such as wearables, edge AI chips, and embedded systems as higher data rate µLED links (25+ Gbps) remain under development or limited to lab-scale demonstrations, the <25 Gbps segment continues to dominate current revenues.

The 50-100 Gbps segment is anticipated to grow at the fastest CAGR during the forecast period due to its alignment with the evolving performance demands of AI, machine learning, and high-performance computing (HPC) workloads. As data-intensive applications increasingly require ultra-fast communication between processing units, microLEDs are emerging as a promising solution capable of delivering high-speed, short-reach optical interconnects within this bandwidth range. Ongoing R&D advancements have demonstrated microLED modulation speeds exceeding 10 GHz, and multi-channel implementations are making 50-100 Gbps transmission rates increasingly viable for chip-to-chip, GPU-to-GPU, and GPU-to-memory links.

Distance Insights

The less than 1 meter segment dominated the market in 2025, due to its suitability for compact designs and high-density applications. It enables minimal signal loss, ensuring reliable and stable connections. Short-distance interconnects are essential for chip-to-chip and module-to-module communication. This range supports efficient power usage while maintaining high performance. Manufacturers increasingly favor it for advanced electronic systems. Overall, it reflects the industry’s focus on optimizing speed, energy efficiency, and integration in constrained spaces.

The more than 5-meter category is showing strong growth in this market. Demand for longer products is increasing due to industrial and commercial applications that require extended coverage. Manufacturers are focusing on improving quality and durability to meet these requirements. Customers are preferring longer options for efficiency and reduced installation time. This trend is expected to continue as infrastructure and large-scale projects expand. The more than 5-meter segment is becoming a key driver of market development.

Regional Insights

North America microLED interconnect industry dominated the global market with a revenue share of over 31.3% in 2025 due to the strong presence of leading semiconductor and AI infrastructure companies and they actively investing in advanced packaging and high-speed interconnect technologies. Funding for R&D from both private and public institutions, including DARPA and NSF, has accelerated the development of microLED modulation, integration, and packaging techniques. Moreover, North American universities and labs are at the forefront of prototyping microLED optical interconnects for chip-to-chip and GPU-to-memory communication.

U.S. MicroLED Interconnect Market Trends

The U.S. microLED interconnect industry is poised for significant growth in 2025 due to a combination of strong government investments and R&D activity. Under the CHIPS and Science Act, the U.S. government is offering substantial grants and tax credits to support domestic microdisplay fabs, which have accelerated investment in fabrication infrastructure across states such as Arizona, Texas, and New York. This public support is complemented by rising interest from FAANG companies and defense agencies in AR/VR and HUD microLED applications driven by the need for ultra-bright, power-efficient near-eye displays.

Europe MicroLED Interconnect Market Trends

Europe’s microLED interconnect industry is set to witness strong growth in the forecast period, fueled by the region’s robust innovation ecosystem in automotive, aerospace, and industrial applications. European governments and institutions, such as the European Innovation Council, are providing substantial funding and mentorship to microLED startups and scale-ups, accelerating technology development and commercialization. With the semiconductor value chain strengthening, microLED manufacturing capabilities, including mass transfer, wafer bonding, and co-packaged optics, are scaling up, reducing costs, and boosting yield.

Asia Pacific MicroLED Interconnect Market Trends

The microLED interconnect industry in the Asia Pacific region is anticipated to register the fastest CAGR over the forecast period. In the APAC region, China, South Korea, Japan, Taiwan, and India together form a semiconductor and display supply chain, marked by mass manufacturing capacity and aggressive innovation in optical interconnects. Governments across these countries are investing heavily, often at a national scale, in next-gen semiconductor fabs, optics R&D, and packaging infrastructure, accelerating commercial readiness and yield optimization for microLED devices.

Key MicroLED Interconnect Company Insights

Some key companies in the microLED Interconnect industry are Aledia; ASE; Ayar Labs, Inc.; AvicenaTech, Corp. Google LLC and others. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Aledia is advancing microLED interconnect technology through its 3D nanowire microLED solutions, enhancing efficiency and pixel density. The company has scaled production with a large fabrication facility in Grenoble. Its FlexiNOVA platform supports diverse devices with flexible chip formats and power options. Ongoing R&D and commercialization are strengthening Aledia’s position in the microLED ecosystem.

-

ASE is developing microLED interconnect solutions to support high-performance display and computing applications. The company focuses on scalable manufacturing techniques and efficient chip-to-chip integration. Its advanced packaging technologies enhance signal transmission and energy efficiency. ASE continues to invest in R&D to expand its microLED interconnect capabilities and market presence.

Key MicroLED Interconnect Companies:

The following key companies have been profiled for this study on the microLED interconnect market.

- ALLOS Semiconductors GmbH

- Aledia

- ASE

- Ayar Labs, Inc.

- Intel Corporation

- Micledi

- AvicenaTech, Corp

- Plessey Semiconductors Ltd

- Taiwan Semiconductor Manufacturing Company Limited

- VueReal

Recent Developments

-

In May 2025, Taiwan Semiconductor Manufacturing Company Limited partnered with Avicena to manufacture microLED-based interconnects aimed at replacing traditional electrical links with low-cost, energy-efficient optical connections for high-performance GPU communication. Avicena’s LightBundle platform uses hundreds of blue microLEDs and imaging fibers to transmit data, offering a modular, laser-free alternative that reduces complexity, power consumption, and cost compared to traditional optical chiplets.

-

In May 2025, AvicenaTech Corp raised USD 65 million in Series B funding, bringing its total to USD 120 million, to expand its team and ramp up production of its first product. The company’s LightBundle solution enables scalable, low-power optical chiplet interconnects for GPU-to-memory and die-to-die communication. It uses GaN microLED arrays integrated onto CMOS chips, paired with multi-fiber cables and silicon detectors, offering a reliable and cost-effective alternative to laser-based interconnects.

-

In March 2025, AvicenaTech launched its LightBundle interconnect platform. This scalable, modular solution extends die-to-die (D2D) communication beyond 10 meters with sub-pJ/bit energy efficiency, enabling>1 Tbps/mm shoreline density. The platform uses transceiver chiplets with integrated microLED and photodetector (PD) arrays, connected via multi-core fiber bundles, and supports standard D2D interfaces such as UCIe and BOW. LightBundle is compatible with CPO, OBO, AOC, and other packaging formats, and unlike silicon photonics, it can be integrated into a wide range of IC processes from different foundries.

MicroLED Interconnect Market Report Scope

Report Attribute

Details

Market size in 2025

USD 181.6 million

Estimated market size in 2026

USD 225.0 million

Projected market size by 2033

USD 722.0 million

Growth rate

CAGR of 18.1% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, data rate, distance, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Aledia; ASE; Ayar Labs, Inc.; AvicenaTech, Corp; Micledi; VueReal; Plessey Semiconductors Ltd; Intel Corporation; ALLOS Semiconductors GmbH; Taiwan Semiconductor Manufacturing Company Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global MicroLED Interconnect Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global microLED interconnect market report based on product, data rate, distance and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

GPU-to-GPU

-

GPU-to-Memory

-

Chip-to-Chip

-

-

Data Rate Outlook (Revenue, USD Million, 2021 - 2033)

-

Less than 25 GBPS

-

25 - 50 GBPS

-

50 - 100 Gbps

-

More than 100 Gbps

-

-

Distance Outlook (Revenue, USD Million, 2021 - 2033)

-

Less than 1 meter

-

1 - 5 meter

-

More than 5 meter

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

KSA

-

South Africa

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The chip-to-chip segment led with a 54.1% revenue share in 2025, while GPU-to-memory is the fastest-growing product.

The less than 25 gbps segment held the largest revenue share in 2025, while 50-100 gbps is the fastest-growing data rate.

Less than 1 meter segment held the largest share (over 47.0%) in 2025.

Key players include Aledia; ASE; Ayar Labs, Inc.; AvicenaTech, Corp; Micledi; VueReal; Plessey Semiconductors Ltd; Intel Corporation; ALLOS Semiconductors GmbH; Taiwan Semiconductor Manufacturing Company Limited.

Key factors that are driving the market growth include the increasing demand for high-performance, low-power, and high-bandwidth data transfer solutions in various applications primarily drives the market. This includes sectors like high-performance computing, AI, and data centers.

The global microLED interconnect market size was valued at USD 181.6 million in 2025 and is estimated at USD 225.0 million for 2026.

The global microLED interconnect market is expected to grow at a CAGR of 18.1% from 2026 to 2033, reaching USD 722.0 million by 2033.

North America dominated the microLED interconnect market with a share of 31.3% in 2025. This is driven by strong R&D investments, the presence of leading semiconductor companies, and growing demand for advanced display and high-performance electronic technologies.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.