- Home

- »

- Next Generation Technologies

- »

-

Operational Technology Market Size Report, 2026-2033GVR Report cover

![Operational Technology Market (2026 - 2033)Report]()

Operational Technology Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Functional Safety, Computer Numerical Control), By Connectivity (Wired, Wireless), By Deployment (Cloud, On-premises), By Enterprise Size, By Industry, By Region, And Segment Forecasts

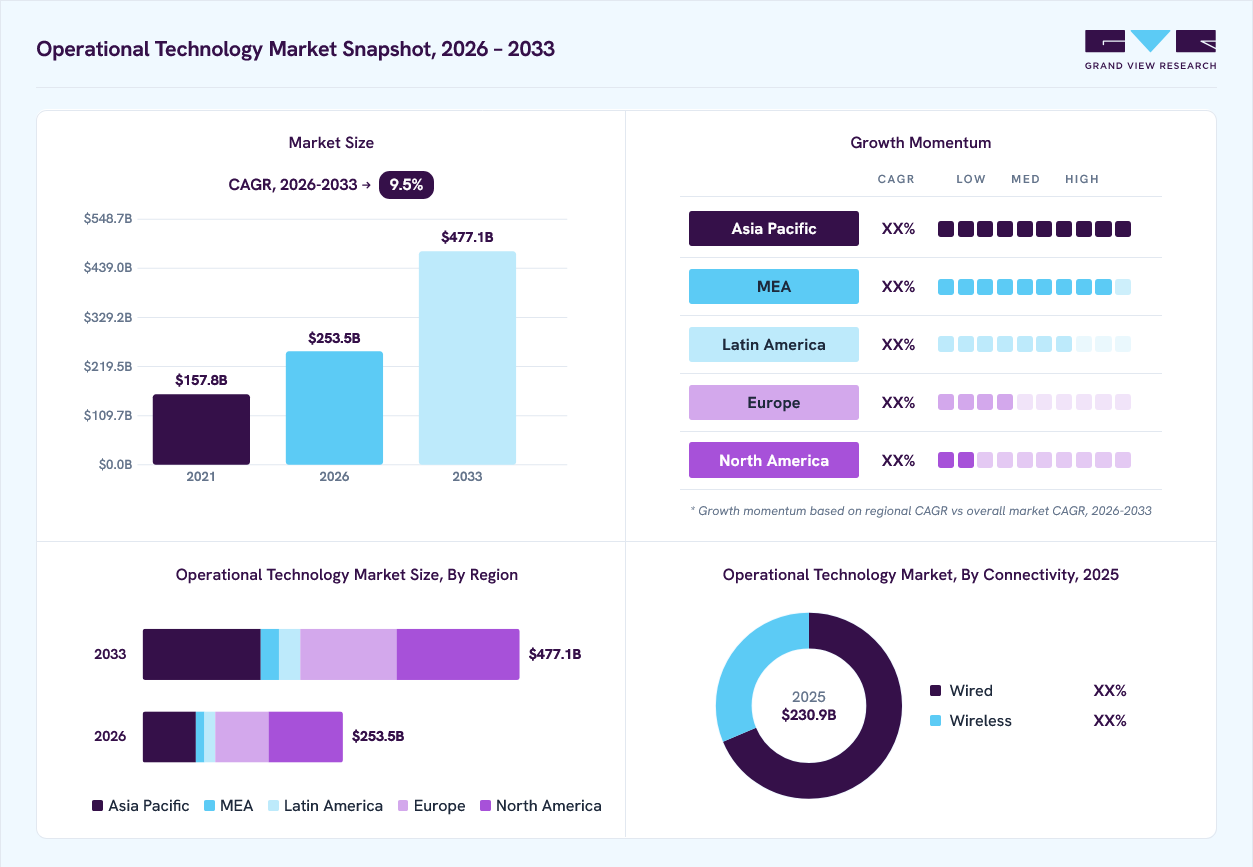

Market Size, 2025

$230.9BMarket Estimate, 2026

$253.5BMarket Forecast, 2033

$477.1BCAGR, 2026–2033

9.5%Operational Technology Market Summary

The global operational technology market size was valued at USD 230.9 billion in 2025 and is projected to grow from USD 253.5 billion in 2026 to USD 477.1 billion by 2033, at a CAGR of 9.5% from 2026 to 2033. The market in North America dominated with a revenue share of 37.7% in 2025. The market is driven by the accelerating convergence of IT and operational technology (OT) environments, increasing adoption of Industrial IoT (IIoT), smart manufacturing initiatives, AI-powered industrial automation, and rising investments in critical infrastructure modernization to enhance operational efficiency, asset visibility, predictive maintenance, and cybersecurity resilience.

Key Market Trends & Insights

- By connectivity: Wired segment held the largest market share of 68.6% in 2025.

- By enterprise size: Large enterprises segment held the largest market share of 67.7% in 2025.

- By industry: Discrete industry segment held the largest market share of 59.5% in 2025.

- By deployment: On-premises segment held the largest market share of 52.0% in 2025.

- By component: Computer numerical control (CNC) segment held the largest market share of 34.7% in 2025.

Regional Highlights

- Largest regional market: North America (37.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 230.9 Billion

- Estimated market size in 2026: USD 253.5 Billion

- Projected market size by 2033: USD 477.1 Billion

- CAGR (2026-2033): 9.5%

The Operational Technology (OT) industry is experiencing significant growth due to its vital role in managing critical infrastructure such as power grids, water treatment plants, and manufacturing facilities. This expansion is driven by the increasing adoption of Industry 4.0, which relies on advanced technologies such as AI, big data, and IoT, necessitating real-time data collection and analysis capabilities of OT systems. Furthermore, emphasizing industrial automation to enhance efficiency and safety in manufacturing processes contributes to the market's growth.")

As industrial control systems become more complex, the demand for secure and reliable OT systems has also surged, ensuring these intricate networks' protection and proper functioning. For instance, in July 2023, Stellar Cyber introduced XDR for Operational Technology (OT) environments. This new feature enhances their Open XDR Platform, offering organizations a unified solution to detect, analyze, and respond to threats across IT and OT networks. The platform includes OT-specific threat detection rules, provides visibility into OT networks and devices, and offers response tools such as automated playbooks and manual remediation actions. This development is the key to securing interconnected IT and OT networks, safeguarding against cyberattacks in the evolving environment.

The rising adoption of digital technologies in the industrial sector is fueling the need for OT security. OT security aims to safeguard industrial control systems from unauthorized access, disruption, and potential damage. As digital technologies interconnect OT systems with IT networks and cyber threats become more sophisticated, the demand for operational technology security is on the rise. Protecting OT systems is essential to prevent cybercriminals from exploiting vulnerabilities and ensuring the continuity and safety of critical industrial processes such as manufacturing, power generation, and water treatment.

The COVID-19 pandemic had a positive impact on the OT market due to several factors. The increased demand for remote monitoring and control solutions led to an increased demand for remote monitoring and control solutions, which allow organizations to monitor and control their operational technology systems from anywhere in the world. The pandemic also raised awareness about the significance of OT security, leading to a higher demand for OT security solutions. Additionally, the acceleration of digital transformation in various industries created new opportunities for OT vendors to cater to evolving needs and requirements in the market.

The future of operational technology is characterized by agility, automation, and service-oriented delivery, with a strong emphasis on cybersecurity. Organizations are already implementing agile development methodologies, automated solutions for predictive maintenance, service-oriented architectures, and various cybersecurity measures to shape the future of operational technology . These advancements will lead to more innovative, secure, and efficient OT solutions in the coming years. As the OT systems become more complex and the threat of cyberattacks grows, the need for agility, automation, and service-oriented delivery will become more important.

Market Dynamics

The operational technology market is driven by the accelerating adoption of Industry 4.0 initiatives, increasing deployment of Industrial Internet of Things (IIoT) solutions, growing integration of IT and OT environments, and rising investments in industrial automation across manufacturing, energy, utilities, and transportation sectors. Organizations are leveraging advanced operational technology platforms, industrial control systems, edge computing, and AI-powered analytics to improve operational efficiency, asset performance, and predictive maintenance capabilities. However, cybersecurity vulnerabilities in connected industrial networks, high modernization costs associated with legacy infrastructure, and integration complexities continue to challenge market expansion. The increasing focus on critical infrastructure protection, regulatory compliance, and industrial cybersecurity is further influencing technology adoption and investment strategies. At the same time, advancements in smart manufacturing, digital twins, industrial AI, private 5G networks, and cloud-enabled OT architectures are creating significant growth opportunities across global industrial ecosystems.

The increasing convergence of Information Technology (IT) and Operational Technology (OT) environments is emerging as a key driver for the operational technology market. Industrial enterprises are integrating OT systems with cloud platforms, edge computing infrastructure, and enterprise software to enable real-time visibility across production environments. The growing deployment of Industrial Internet of Things (IIoT) devices, smart sensors, and connected industrial assets is generating vast volumes of operational data that require advanced analytics and automation capabilities. Organizations are leveraging AI-powered industrial automation, predictive maintenance, and digital twin technologies to improve operational efficiency, reduce downtime, and optimize asset performance. This trend is accelerating investments in OT platforms, industrial control systems, SCADA, distributed control systems, and industrial cybersecurity solutions across manufacturing, energy, utilities, and transportation sectors.

Furthermore, the rapid advancement of Industry 4.0 initiatives is driving enterprises to modernize legacy operational technology infrastructure and adopt intelligent factory ecosystems. Manufacturers are increasingly implementing machine learning algorithms, autonomous process controls, and edge intelligence to enhance production agility and decision-making. The integration of OT with enterprise resource planning (ERP), manufacturing execution systems (MES), and cloud-based analytics platforms is enabling seamless data exchange and process optimization. Governments and industrial organizations are also supporting digital transformation programs aimed at improving productivity, sustainability, and operational resilience. As a result, demand for advanced OT solutions continues to expand across both developed and emerging industrial economies.

The growing frequency and sophistication of cyberattacks targeting industrial control systems represent a significant restraint for the operational technology market. As OT environments become increasingly connected through IIoT networks and cloud-based platforms, the attack surface for cyber threats continues to expand. Critical infrastructure operators in sectors such as energy, utilities, manufacturing, and transportation face heightened risks associated with ransomware, malware, and unauthorized network access. Many industrial facilities continue to operate legacy OT systems that were not originally designed with cybersecurity protections, creating vulnerabilities across operational networks. These security concerns often delay digital transformation initiatives and increase the complexity of OT deployment strategies.

In addition, the modernization of aging industrial infrastructure requires substantial capital investment and technical expertise, creating adoption barriers for many organizations. Legacy programmable logic controllers (PLCs), SCADA systems, and distributed control systems frequently lack interoperability with modern digital technologies. Integrating new OT solutions into existing operational environments can lead to operational disruptions, implementation challenges, and extended deployment timelines. Organizations must also comply with evolving industrial cybersecurity regulations and standards, which can increase operational costs and resource requirements. Consequently, concerns regarding cybersecurity resilience and infrastructure modernization continue to restrain market growth, particularly among small and mid-sized industrial enterprises.

The accelerating adoption of smart manufacturing and digital transformation initiatives presents a significant opportunity for the operational technology market. Industrial organizations are increasingly investing in connected factories, autonomous production systems, and intelligent operational workflows to enhance competitiveness and operational efficiency. The deployment of Industrial IoT platforms, digital twins, advanced robotics, and AI-driven analytics is enabling manufacturers to achieve higher productivity and greater process visibility. Real-time monitoring and predictive maintenance capabilities are helping enterprises reduce equipment failures, optimize maintenance schedules, and improve asset utilization rates. These advancements are creating substantial growth opportunities for OT vendors offering integrated automation, connectivity, and industrial software solutions.

Moreover, increasing investments in critical infrastructure modernization and sustainable industrial operations are expanding the scope of OT deployments worldwide. Energy utilities, transportation networks, oil and gas facilities, and smart city projects are adopting advanced operational technology systems to improve reliability, safety, and environmental performance. The emergence of edge computing, private industrial 5G networks, and cloud-native OT architectures is further enhancing industrial connectivity and data-driven decision-making. Organizations prioritize operational resilience and business continuity by implementing intelligent control systems and cybersecurity-enabled OT platforms. As industrial sectors continue to embrace digital transformation strategies, the demand for scalable, secure, and AI-enabled operational technology solutions is expected to grow significantly over the forecast period.

Market Concentration & Characteristics

The operational technology market exhibits a moderately concentrated competitive landscape, with global industrial automation leaders maintaining strong positions across manufacturing, energy, utilities, transportation, and critical infrastructure sectors. Major vendors continue to strengthen their market presence through integrated industrial control systems, supervisory control and data acquisition (SCADA) platforms, distributed control systems (DCS), and industrial cybersecurity solutions. The market is characterized by a combination of established automation providers and specialized technology companies offering niche operational intelligence and asset management capabilities. Increasing investments in digital transformation, smart factories, and connected industrial ecosystems are further intensifying competition across the value chain.

The market demonstrates a high degree of innovation, driven by advancements in Industrial Internet of Things (IIoT), edge computing, artificial intelligence, digital twins, and predictive maintenance technologies. Regulatory requirements related to critical infrastructure protection, industrial safety, and cybersecurity continue to significantly influence technology adoption and vendor strategies. Merger and acquisition activity remains robust as companies seek to expand their industrial software portfolios, automation capabilities, and OT security offerings. Furthermore, the relatively low availability of substitutes and the concentration of demand among large industrial enterprises support sustained growth and long-term investment in operational technology platforms and intelligent automation solutions.

Analyst Perspective

The Operational Technology (OT) market is experiencing strong growth, driven by increasing investments in industrial automation, smart manufacturing, and Industrial Internet of Things (IIoT) technologies across process and discrete industries. Organizations are increasingly deploying advanced operational technology solutions to enhance operational efficiency, improve asset reliability, and enable real-time monitoring of critical industrial processes. The convergence of IT and OT environments, coupled with the adoption of edge computing, industrial AI, and digital twin technologies, is accelerating digital transformation initiatives across manufacturing, energy, utilities, and transportation sectors. Additionally, growing concerns regarding industrial cybersecurity and critical infrastructure protection are encouraging enterprises to modernize legacy control systems and strengthen operational resilience. As industries continue to prioritize productivity optimization, connected operations, and data-driven decision-making, the Operational Technology market is expected to witness sustained expansion throughout the forecast period.

Component Insights

Based on component, the computer numerical control (CNC) segment led the market with the largest revenue share of 34.7% in 2025. The high share can be attributed to the surging demand for CNC machines in diverse manufacturing, automotive, and aerospace industries. CNC machines automate complex parts and product production, enhancing efficiency and productivity. The growth of the CNC segment is propelled by several key factors, including the rising need for automation in manufacturing, the increasing adoption of Industry 4.0 technologies, the growing demand for precision components, and the expansion of the automotive and aerospace sectors.

The building management system segment is anticipated to grow at the fastest CAGR during the forecast period. This growth can be attributed to the increasing demand for energy-efficient and sustainable buildings, the rising popularity of smart buildings with remote-controllable BMSs, and the widespread adoption of IoT and digital technologies in the construction industry. BMSs play a crucial role in monitoring and controlling various building systems, such as HVAC, lighting, and security, leading to improved energy efficiency, reduced operating costs, and enhanced occupant comfort and safety. The surge in energy-efficient construction projects further boosts the demand for BMSs as they contribute to automating and optimizing building systems to conserve energy based on occupancy and weather conditions.

Connectivity Insights

Based on connectivity, the wired segment led the market with the largest revenue share of 68.6% in 2025. The growth is attributed to its reliability and security compared to wireless alternatives, making it indispensable for critical infrastructure applications. Its resistance to interference and hacking ensures the protection and stability of essential systems. Additionally, the scalability of wired networks allows for easy expansion to accommodate new devices and applications without compromising performance. Furthermore, wired technology's cost-effectiveness, requiring less infrastructure and simpler maintenance, is anticipated to maintain its growth trajectory in the foreseeable future.

The wireless segment is anticipated to grow at the fastest CAGR during the forecast period. The increasing demand for remote monitoring and control of industrial assets is a significant driver as businesses seek more flexible and efficient solutions. Additionally, the development of new wireless technologies, particularly 5G, with higher bandwidth and lower latency, will further fuel the expansion of wireless applications in critical areas such as Supervisory Control and Data Acquisition (SCADA), Distributed Control Systems (DCS), Human-Machine Interfaces (HMI), industrial sensors, and predictive maintenance. These advancements are expected to propel the wireless segment's prominence as businesses embrace the benefits of reliable and innovative wireless solutions.

Deployment Insights

Based on deployment, the on-premises segment led the market with the largest revenue share of 52.0% in 2025. The high market share can be attributed to organizations prioritizing on-premises solutions due to the need for greater control over their OT security systems, enabling enhanced protection and customization tailored to their specific requirements. Additionally, concerns surrounding security and privacy when storing data in the cloud fueled the demand for on-premises deployments. As many operational technology (OT) systems are not designed for internet connectivity, it adds an extra layer of difficulty for potential hackers, making on-premises solutions a favored choice for businesses seeking robust and secure operational technology solutions and thus boosting the segment's prominence.

The cloud segment is expected to grow at the fastest CAGR during the forecast period. Cloud-based solutions offer scalability and flexibility, allowing businesses to easily adjust their systems as needed without being constrained by physical location. Moreover, the rising concern for security in OT systems is addressed by cloud-based solutions, as they offer robust protection in secure data centers. Additionally, the growing adoption of IoT devices in operational technology systems fuels the demand for cloud-based solutions that efficiently manage and utilize the vast amounts of data generated, ultimately leading to enhanced operational efficiency and safety. This confluence of factors drives the adoption of cloud-based solutions in the OT market.

Enterprise Size Insights

Based on enterprise size, the large enterprises segment led the market with the largest revenue share of 67.7% in 2025. The high share can be attributed to their complex and critical OT environments and greater resources for investing in OT security and compliance. The segment's growth was fueled by the increasing convergence of OT and IT infrastructure, rising demands for OT security and compliance, and the escalating number of cyber threats targeting operational technology systems. Businesses opted for OT solutions to achieve real-time visibility into their operations, facilitating quicker problem identification and operational efficiency improvements. These solutions also empowered better decision-making by providing valuable operational data and bolstering safety and security measures, particularly in high-risk industries.

The SMEs segment is expected to grow at the fastest CAGR during the forecast period. OT solutions enable SMEs to enhance efficiency and productivity by automating tasks and processes and reducing costs. Real-time data provided by OT solutions empower better decision-making, optimizing resource utilization and maintaining a competitive edge. Additionally, SMEs benefit from improved visibility and control over operations, swiftly addressing issues and reducing risks. Enhanced customer service is another advantage, as OT solutions provide real-time data on customer interactions, facilitating quicker issue resolution and improved customer service quality.

Industry Insights

Based on industry, the discrete industry segment has a significant revenue share of 59.5% in 2025. This growth can be attributed to the segment's diverse industries, including mining & metals, oil & gas, energy & power, chemicals, pulp & paper, and pharmaceuticals, which rely heavily on operational technology. Adopting operational technology enables these industries to automate processes and gather valuable data for optimizing their operations. Moreover, the increasing adoption of automation and digitization, the pressing need to enhance operational efficiency and productivity, adherence to safety regulations, and the importance of data collection and analysis for informed decision-making is driving the segment's growth in the market.

The process industry segment is estimated to grow at the fastest CAGR during the forecast period. The segment's growth is driven by the wide array of industries encompassed within the process industry, including food and beverages, oil and gas, energy and power, chemicals, and pharmaceuticals. These industries rely heavily on operational technology to control and monitor their operations. Moreover, the adoption of operational technology in the process industry segment is further fueled by its ability to enhance resource utilization, minimize downtime, and enable data-driven decision-making. As these industries continue to expand and innovate, the demand for advanced operational technology solutions is anticipated to witness substantial growth, contributing to the overall progression of the operational technology market.

Regional Insights

North America dominated the operational technology market with the largest revenue share of 37.7% in 2025. The region boasts a well-developed industrial base, particularly in automotive manufacturing. This existing infrastructure provides a foundation for the adoption of new operational technology solutions. For instance, in November 2024, Rockwell Automation, Inc. announced the integration of NVIDIA Omniverse APIs into its Emulate3D software. This strategic move aims to improve factory operations by leveraging AI and physics-based simulation technology.

U.S. Operational Technology Market Trends

The Operational technology market in the U.S. held the largest share in the North America region in 2025. Reshoring efforts in the U.S. are driving the need for investments in modern operational technology solutions to enhance manufacturing efficiency. Simultaneously, the evolving energy sector, driven by the increased use of renewables and grid modernization, requires advanced operational technology solutions to manage and optimize complex energy systems effectively.

Europe Operational Technology Market Trends

The Europe operational technology market is expected to witness significant growth over the forecast period. The increasing emphasis on sustainability and energy transition in Europe, with a growing focus on renewable energy and energy efficiency, is propelling the demand for advanced operational technology solutions. This trend particularly drives the development of operational technology solutions dedicated to grid management and optimization. Moreover, the European Union (EU) has implemented specific regulations, such as the NIS Directive and the Cybersecurity Act, to address cybersecurity concerns in critical infrastructure.

Asia Pacific Operational Technology Market Trends

The Asia Pacific operational technology industry is anticipated to register the highest CAGR over the forecast period. The active adoption of industry 4.0 principles, merging IT and operational technology systems, is promoting increased automation and improved resource utilization across various industries. Moreover, the region's focus on energy transition and sustainability is driving the demand for advanced operational technology solutions, especially in effective grid management, seamless integration of renewable energy sources, and real-time monitoring for optimized energy usage.

China operational technology market dominated the regional market in 2024. The growing awareness of cybersecurity threats in critical infrastructure further propels the adoption of robust operational technology security solutions, safeguarding against cyberattacks and ensuring the safe and reliable operation of industrial processes in China. As industries in China increasingly integrate IoT devices and solutions into their operations, there is a parallel surge in the demand for operational technology to manage and optimize these interconnected systems. For instance, in 2024, China's rapid industrial internet growth spurred huge demand for operational technology cybersecurity solutions, as noted by Kaspersky, highlighting the increasing awareness of cybersecurity threats in critical infrastructure.

Key Operational Technology Company Insights

Some key companies in the operational technology industry are ABB, Emerson Electric Co., IBM Corporation, and Honeywell International Inc.

-

ABB is a global technology company that specializes in electrification, robotics, automation, and motion technologies. In the realm of OT, ABB focuses on enhancing cybersecurity for industrial infrastructure through partnerships such as the one with Nozomi Networks, which integrates advanced OT and IoT security solutions to support digital transformation and operational resiliency in energy and process industries.

-

Honeywell International Inc. is a prominent player in the industrial automation sector, offering a range of Operational Technology solutions. Its OT cybersecurity portfolio includes advanced software-enabled solutions such as Honeywell Forge Cybersecurity+, which provides continuous monitoring and real-time threat detection to protect industrial control systems and assets. Honeywell's industrial automation technologies are used in various settings, including factories and refineries, to manage complex processes and ensure consistent results.

Key Operational Technology Companies

The following key companies have been profiled for this study on the operational technology market.

-

Emerson Electric Co.

-

General Electric

-

Hitachi, Ltd.

-

IMB Corporation

-

Honeywell International Inc.

-

OMRON Corporation

-

Rockwell Automation

-

Siemens.

-

Schneider Electric

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Mature Players (ABB Ltd., Siemens AG, Schneider Electric SE, Honeywell International Inc., Emerson Electric Co., Rockwell Automation)

- Mature players emphasize industrial digitalization, connected operations, intelligent process optimization, asset performance management, and critical infrastructure modernization.

- Their strategies focus on expanding software-driven automation capabilities, strengthening operational visibility, and enhancing industrial productivity through integrated technology ecosystems.

- Their competitive strength is supported by extensive installed equipment bases, comprehensive industrial portfolios, long-standing customer relationships, and global engineering expertise.

- Strong service capabilities, broad geographic reach, and deep domain knowledge enable these companies to support complex operational environments across multiple industries.

- These organizations may face challenges associated with maintaining legacy product portfolios, lengthy procurement cycles, and high deployment complexity within large-scale industrial projects.

- Additionally, evolving cybersecurity requirements and increasing competition from software-centric providers can create operational and strategic pressures.

Emerging Players (Hitachi, Ltd., IBM Corporation, OMRON Corporation, General Electric (GE Vernova))

- Emerging players are focusing on industrial intelligence, data-driven operations, predictive asset monitoring, edge-enabled architectures, and advanced analytics platforms.

- Their market approach prioritizes innovation, operational insights, and technology differentiation to address evolving industrial performance requirements.

- Their competitive advantage stems from specialized expertise in analytics, industrial software, intelligent monitoring systems, and next-generation operational technologies.

- Flexible solution architectures, strong innovation capabilities, and targeted industry offerings allow them to address specific customer challenges with greater precision.

- Limited penetration across certain industrial segments, smaller automation hardware portfolios, and dependence on strategic partnerships may constrain market expansion.

- Furthermore, competition from established automation leaders and the need for continuous technology investments can affect long-term scalability and market positioning.

Recent Developments

-

In March 2025, Fortinet introduced substantial updates to its OT Security Platform, enhancing the protection of critical infrastructure from emerging cyber threats. These advancements, announced at the Gartner Digital Workplace Summit in Singapore, provide advanced visibility, segmentation, and secure connectivity solutions tailored for industries such as transportation, energy, and manufacturing.

-

In March 2025, TXOne Networks introduced Version 3.2 of its Stellar solution, significantly enhancing its capabilities in operational technology environments. This update expands Stellar's functionality from endpoint protection to comprehensive detection and response, facilitating more effective threat hunting and detection.

-

In March 2025, Armis, a company specializing in cyber exposure management and security, completed the acquisition of OTORIO, an expert in OT and Cyber-Physical Systems (CPS) security. This strategic move aims to strengthen Armis' capabilities in OT and CPS by incorporating OTORIO's Titan platform into Armis' Centrix cloud-based cyber exposure management platform.

Operational Technology Market Report Scope

Report Attribute

Details

Market size in 2025

USD 230.9 billion

Estimated market size in 2026

USD 253.5 billion

Projected market size by 2033

USD 477.1 billion

Growth rate

CAGR of 9.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, connectivity, deployment, enterprise size, industry, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; Saudi Arabia; South Africa; UAE

Key companies profiled

ABB.; Emerson Electric Co.; General Electric; Hitachi, Ltd.; IMB Corporation; Honeywell International Inc.; OMRON Corporation; Rockwell Automation; Siemens; Schneider Electric

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Operational Technology Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global operational technology market report based on component, connectivity, deployment, enterprise size, industry, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Supervisory Control and Data Acquisition (SCADA)

-

Programmable Logic Controller (PLC)

-

Remote Terminal Units (RTU)

-

Human-Machine Interface (HMI)

-

Others

-

-

Distributed Control System (DCS)

-

Manufacturing Execution System Market

-

Functional Safety

-

Building Management System

-

Plant Asset Management (PAM)

-

Variable Frequency Drives (VFD)

-

Computer Numerical Control (CNC)

-

Others

-

-

Connectivity Outlook (Revenue, USD Billion, 2021 - 2033)

-

Wired

-

Wireless

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-premises

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

SMEs

-

Large Enterprises

-

-

Industry Outlook (Revenue, USD Billion, 2021 - 2033)

-

Process Industry

-

Oil & Gas

-

Chemicals

-

Pulp & Paper

-

Pharmaceuticals

-

Mining & Metals

-

Energy & Power

-

Others

-

-

Discrete Industry

-

Automotive

-

Semiconductor & Electronics

-

Aerospace & Defense

-

Heavy Manufacturing

-

Others

-

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

KSA

-

-

Research Methodology

The operational technology market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each operational technology segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Component

Revenue capture definition

Supervisory Control and Data Acquisition (SCADA)

The Supervisory Control and Data Acquisition (SCADA) segment comprises software and hardware solutions that enable centralized monitoring, control, and data acquisition from industrial assets and remote operations. These systems support real-time process visibility, operational management, and performance optimization across critical infrastructure and industrial environments.

Distributed Control System (DCS)

This segment includes integrated control platforms designed to manage complex industrial processes through distributed controllers deployed across production facilities. DCS solutions facilitate continuous process automation, improve operational stability, and enhance plant-wide efficiency in process-intensive industries.

Manufacturing Execution System Market

The Manufacturing Execution System (MES) segment encompasses software platforms that connect shop-floor operations with enterprise-level planning systems. These solutions provide production tracking, workflow coordination, quality management, and performance analytics to improve manufacturing productivity.

Functional Safety

This Functional Safety segment consists of technologies and systems designed to minimize operational risks and ensure safe functioning of industrial processes. The category includes safety controllers, emergency shutdown systems, and safety instrumentation that help organizations comply with industry regulations and standards.

Building Management System

Building Management System solutions enable centralized supervision and automation of building infrastructure, including HVAC, lighting, security, and energy management systems. These platforms support improved resource utilization, occupant comfort, and operational efficiency across commercial and industrial facilities.

Plant Asset Management (PAM)

Plant Asset Management (PAM) comprises software and analytical tools used to monitor, maintain, and optimize the performance of industrial assets throughout their lifecycle. The solutions assist organizations in reducing downtime, extending equipment longevity, and improving maintenance planning.

Variable Frequency Drives (VFD)

The Variable Frequency Drives (VFD) segment includes motor control devices that regulate speed and torque by adjusting electrical frequency and voltage supplied to motors. These solutions enhance energy efficiency, process control, and equipment reliability in industrial applications.

Computer Numerical Control (CNC)

Computer Numerical Control (CNC) systems automate machining and manufacturing operations through programmable instructions and precision control mechanisms. The technology supports high-accuracy production, reduced manual intervention, and improved manufacturing consistency.

Others

This segment covers additional operational technology solutions that support industrial automation, monitoring, control, and optimization functions not classified under the primary categories. It includes emerging technologies and specialized applications tailored to specific operational requirements.

Segment - Supervisory Control and Data Acquisition (SCADA)

Revenue capture definition

Programmable Logic Controller (PLC)

The Programmable Logic Controller (PLC) segment consists of industrial computing devices used to automate machinery and process operations through predefined logic and control functions. These controllers enable reliable execution of production tasks in demanding industrial environments.

Remote Terminal Units (RTU)

This segment includes field-based electronic devices that collect operational data from equipment and transmit information to centralized monitoring systems. RTUs facilitates remote asset management and communication across geographically dispersed industrial networks.

Human-Machine Interface (HMI)

The Human-Machine Interface (HMI) segment comprises visualization and interaction platforms that allow operators to monitor and control industrial processes. These solutions provide graphical displays, operational alerts, and process insights to improve decision-making and productivity.

Others

This SCADA-related segment encompasses supporting technologies and components that contribute to industrial monitoring and controlling architectures. It includes communication gateways, data historians, protocol converters, and other specialized devices.

Segment - Connectivity

Revenue capture definition

Wired

The Wired connectivity segment includes communication technologies that transmit data through physical cabling infrastructure such as Ethernet, fiber optics, and industrial fieldbus networks. These solutions offer high reliability, low latency, and secure communication for mission-critical industrial operations.

Wireless

Wireless connectivity solutions enable data transmission between industrial devices without the need for physical network connections. The segment includes Wi-Fi, cellular, industrial wireless protocols, and private network technologies that support flexible and scalable deployments.

Segment - Deployment

Revenue capture definition

Cloud

The Cloud segment comprises operational technology solutions delivered through remote computing infrastructure and host platforms. These deployments provide scalable processing capabilities, centralized data access, and advanced analytics without extensive on-site hardware investments.

On-premises

This On-premises segment includes software and control systems installed and operated within an organization's own facilities and infrastructure. Such deployments offer greater control over data management, system customization, and cybersecurity requirements.

Segment - Enterprise Size

Revenue capture definition

SME

The SME segment represents small and medium-sized enterprises that deploy operational technology solutions to improve production efficiency, process automation, and asset utilization. Adoption is often driven by cost-effective technologies that support business growth and operational modernization.

Large Enterprises

Large Enterprises utilize comprehensive operational technology ecosystems across multiple facilities, production sites, and business units. These organizations typically invest in advanced automation, digital transformation, and industrial intelligence platforms to optimize large-scale operations.

Segment - Industry

Revenue capture definition

Process Industry

The Process Industry segment includes sectors where products are manufactured through continuous, batch, or sequential processing operations. Operational technology solutions support process control, production optimization, safety management, and regulatory compliance within these environments.

Discrete Industry

This Discrete Industry segment comprises sectors that manufacture distinct products through assembly, fabrication, or machining processes. The technologies enable production automation, quality assurance, workflow coordination, and operational efficiency improvements.

Segment - Process Industry

Revenue capture definition

Oil & Gas

The Oil & Gas segment encompasses exploration, production, refining, transportation, and distribution activities that rely on advanced monitoring and control systems. Operational technology solutions help improve safety, operational reliability, and asset performance across the value chain.

Chemicals

Chemicals organizations utilize operational technology platforms to manage complex production processes, maintain product quality, and ensure safe plant operations. These solutions support process optimization, regulatory compliance, and resource efficiency initiatives.

Pulp & Paper

The Pulp & Paper segment includes facilities involved in pulp processing, paper manufacturing, and packaging material production. Operational technology systems assist in controlling production parameters, minimizing waste, and improving operational consistency.

Pharmaceuticals

Pharmaceutical manufacturers deploy operational technology solutions to support precision production, quality assurance, and regulatory compliance requirements. These systems enable process monitoring, batch control, and manufacturing traceability across production facilities.

Mining & Metals

Mining & Metals operations leverage operational technology to monitor extraction activities, processing equipment, and material handling systems. The technologies improve productivity, workforce safety, and operational visibility across mining and metallurgical processes.

Energy & Power

The Energy & Power segment includes electricity generation, transmission, distribution, and renewable energy operations supported by advanced control and monitoring platforms. Operational technology solutions enhance grid reliability, asset utilization, and infrastructure performance.

Others

This category covers additional process-oriented industries that utilize operational technology to automate workflows, monitor operations, and improve production efficiency. The segment includes sectors with specialized process control and asset management requirements.

Segment - Discrete Industry

Revenue capture definition

Automotive

The Automotive segment utilizes operational technology to automate assembly lines, monitor production performance, and enhance manufacturing quality. These solutions support efficient vehicle production, process standardization, and operational flexibility.

Semiconductor & Electronics

Semiconductor & Electronics manufacturers employ advanced automation and process control technologies to achieve high precision and production consistency. Operational technology platforms help optimize fabrication processes, equipment performance, and product quality.

Aerospace & Defense

The Aerospace & Defense segment relies on operational technology solutions to support precision manufacturing, quality assurance, and mission-critical production environments. These systems enable operational control, traceability, and compliance with stringent industry standards.

Heavy Manufacturing

Heavy Manufacturing organizations deploy operational technology platforms to manage large-scale production equipment, industrial machinery, and complex manufacturing workflows. The solutions improve operational efficiency, asset utilization, and process reliability.

Others

This segment includes additional discrete manufacturing industries that utilize automation, monitoring, and industrial control technologies to enhance production operations. The category encompasses specialized manufacturing applications not covered within the primary industry classifications.

Estimation Model

Layer Name

Key Questions

Description

Industrial Operations & Automation Demand Layer

Which industries generate demand for operational technology solutions?

Identify industries with significant automation, process control, and operational monitoring requirements, including manufacturing, oil & gas, energy & power, chemicals, pharmaceuticals, mining & metals, automotive, aerospace & defense, transportation, and utilities. This layer establishes the total addressable demand base for operational technology solutions across organizations seeking enhanced productivity, operational efficiency, asset reliability, and industrial process optimization.

Industrial Digitalization & Infrastructure Modernization Layer

Who invests in operational technology infrastructure and modernization initiatives?

Apply adoption rates of industrial automation systems, Industrial Internet of Things (IIoT) platforms, industrial networking solutions, edge computing infrastructure, SCADA systems, distributed control systems (DCS), programmable logic controllers (PLCs), and cybersecurity technologies. This layer estimates the transition from conventional industrial environments to connected, intelligent, and data-driven operational ecosystems.

Advanced Operational Technology Deployment Layer

Who deploys advanced operational technology platforms and applications?

Apply penetration levels of smart manufacturing solutions, predictive maintenance platforms, digital twins, industrial AI, plant asset management systems, manufacturing execution systems (MES), building management systems (BMS), and industrial analytics applications. This layer captures the adoption of advanced operational technology capabilities across process industries, discrete manufacturing environments, and critical infrastructure operations.

Operational Technology Value Realization Layer

How much value is generated through operational technology adoption?

Estimate market revenue by multiplying active operational technology deployments by average spending on industrial automation hardware, software platforms, connectivity infrastructure, cloud services, cybersecurity solutions, integration services, maintenance contracts, and consulting engagements. This layer captures the total operational technology market revenue generated through the deployment, operation, modernization, and optimization of industrial control and automation systems.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Industrial Automation & Digital Transformation Assessment

Performed a comprehensive analysis of Operational Technology market trends, including industrial automation, Industrial Internet of Things (IIoT), smart manufacturing, edge computing, digital twins, predictive maintenance, industrial networking, and industrial cybersecurity adoption across major end-use industries.

This assessment enables stakeholders to identify high-growth technology segments, evaluate industrial modernization trends, prioritize automation investments, and strengthen competitive positioning within the evolving Operational Technology ecosystem.

Industry-Specific Operational Technology Deployment Analysis

Assessed demand for Operational Technology solutions across manufacturing, oil & gas, energy & power, chemicals, pharmaceuticals, mining & metals, automotive, aerospace & defense, and utilities sectors, including process automation, asset monitoring, production optimization, industrial control systems, and intelligent operations management applications.

Provides strategic insights into industry-specific digital transformation initiatives, operational technology deployment requirements, and long-term revenue opportunities, supporting market expansion planning and targeted business growth strategies.

Smart Manufacturing, Industrial Intelligence & Asset Optimization Opportunity Assessment

Evaluated adoption trends for SCADA systems, distributed control systems (DCS), manufacturing execution systems (MES), plant asset management (PAM), industrial AI, connected assets, real-time analytics, and next-generation operational technology platforms across global markets.

Supports investment and product development strategies by identifying emerging automation opportunities, accelerating digital transformation roadmaps, enhancing operational efficiency initiatives, and enabling data-driven decision-making across high-growth segments of the Operational Technology market.

Frequently Asked Questions About This Report

North America dominated the market in 2025, accounting for over 37.0% share of the global revenue. The region's prominent position in the operational technology market is attributable to its thriving industrial sectors, including manufacturing, energy, and transportation.

Some key players operating in the operational technology market include ABB; Emerson Electric Co.; Fortinet, Inc.; Forcepoint; General Electric; Honeywell International Inc.; Huawei Technologies Co., Ltd.; IBM Corporation; Rockwell Automation; Schneider Electric.

Key factors driving the operational technology market growth include the growing demand for real-time data analysis and predictive maintenance and the surging adoption of cloud-based OT solutions.

The computer numerical control (CNC) segment led with over 34.0% revenue share in 2025, while the building management system segment is the fastest-growing.

The wired segment led with over 68.0% revenue share in 2025, while the wireless segment is the fastest-growing.

The on-premises segment led with a 52.0% revenue share in 2025, while the cloud segment is the fastest-growing.

Asia Pacific is the fastest-growing region over the forecast period.

The global operational technology market size was valued at USD 230.9 billion in 2025 and is estimated at USD 253.5 billion for 2026.

The global operational technology market is expected to grow at a CAGR of 9.5% from 2026 to 2033, reaching USD 477.1 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.