- Home

- »

- Organic Chemicals

- »

-

Organic Acids Market Size, Share & Trends Report 2026-2033GVR Report cover

![Organic Acids Market (2026 - 2033)Report]()

Organic Acids Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Acetic Acid, Citric Acid), By Source (Biomass, Synthetic), By Application (Food & Beverage, Pharmaceuticals), By Region (Asia Pacific, North America), And Segment Forecasts

Market Size, 2022

$19.1BMarket Estimate, 2026

$19.7BMarket Forecast, 2033

$25.2BCAGR, 2023–2033

3.6%Organic Acids Market Summary

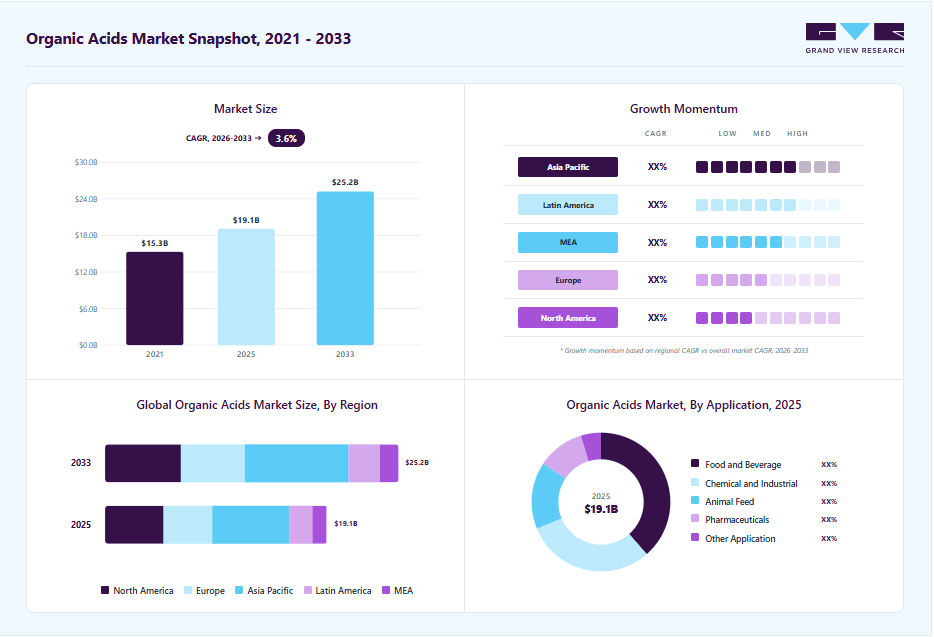

The global organic acids market size was valued at USD 19.1 billion in 2025 and is projected to grow from USD 19.7 billion in 2026 to USD 25.2 billion by 2033, at a CAGR of 3.6% from 2026 to 2033. The Asia Pacific market held the largest share of 34.6% of the global market in 2025. Growth in the organic acids market is primarily driven by the increasing use of natural additives in the food and beverage sector, where they serve as preservatives and acidity regulators.

Key Market Trends & Insights

- By product: The Acetic acid accounted for the largest share of the organic acids market in 2025.

- By source: The synthetic segment dominated the organic acids market in 2025, accounting for 57.2% of total revenue.

- By application: The food and beverage segment accounted for the largest revenue share of 38.7% in the year 2025.

Regional Highlights

- Largest regional market: Asia Pacific (34.6% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 19.1 Billion

- Estimated market size in 2026: USD 19.7 Billion

- Projected market size by 2033: USD 25.2 Billion

- CAGR (2026-2033): 3.6%

The gradual shift away from antibiotic growth promoters in animal nutrition is further boosting demand for certain organic acids. At the same time, the growing emphasis on sustainability and environmentally friendly production methods is driving the adoption of bio-based organic acids across industrial and pharmaceutical applications. The industry is constrained by volatility in key raw material prices, including agricultural feedstock and petrochemical inputs, which can impact overall production costs. Bio-based organic acids often face cost disadvantages compared to their synthetic counterparts, limiting their uptake in cost-sensitive markets. The presence of strong competition in standardized, low-differentiation products, along with the need for significant capital investment in production infrastructure, poses ongoing challenges for market participants.")

There is considerable potential in the expansion of specialty and high-value organic acids tailored for pharmaceuticals, nutraceuticals, and premium food applications. Increasing interest in biodegradable materials is also driving demand for lactic acid in bioplastics. The advancements in fermentation technology and a growing focus on sustainable chemical solutions are expected to create new avenues for innovation and long-term market growth.

Market Dynamics

Market Drivers: Rising Demand for Processed Foods Increasing Consumption of Organic Acid Ingredients

The increasing demand for processed and convenience foods is a major driver of the organic acids market. Rapid urbanization, changing dietary habits, and busy consumer lifestyles are driving higher consumption of packaged and ready-to-eat foods worldwide. Organic acids such as citric acid, lactic acid, and acetic acid are widely used in food processing as preservatives, acidulants, flavor enhancers, and pH regulators. These ingredients help improve product shelf life, maintain food quality, and enhance taste stability during storage and transportation. As food manufacturers focus on safety, freshness, and extended shelf stability, the demand for organic acids continues to rise steadily across global food processing industries.

In addition, growing consumer demand for safe, high-quality food products is encouraging manufacturers to adopt efficient food preservation solutions. Expanding beverage production, bakery applications, dairy processing, and confectionery manufacturing are further supporting increased organic acid consumption globally, contributing significantly to long-term market growth.

The widespread availability of lower-cost synthetic alternatives constrains the organic acids market, as many manufacturers prioritize cost-efficient ingredients for large-scale industrial and food processing applications. Synthetic additives often provide comparable preservation, acidity regulation, and stabilization performance at lower production costs than certain organic acid formulations. As a result, cost-sensitive industries may prefer synthetic substitutes to maintain profitability and reduce operational expenses. This limits the adoption of organic acids, particularly in price-competitive markets where purchasing decisions are strongly influenced by production economics. The continued use of economical synthetic chemicals, therefore, restricts the full growth potential of the global organic acids market.

Market Concentration & Characteristics

The organic acids market is characterized by a mix of large multinational chemical companies and specialized bio-based producers, creating a moderately consolidated yet competitive landscape. Leading players such as Cargill, BASF, and ADM benefit from strong global supply chains, integrated operations, and broad product portfolios, allowing them to maintain cost leadership and serve diverse end-use industries. These companies leverage scale and backward integration to manage raw material volatility effectively. Firms like Corbion, Koninklijke DSM, and DuPont are strengthening their positions through innovation in bio-based and high-value organic acids, particularly in applications such as bioplastics and food preservation.

Competition is increasingly shifting from volume-based strategies toward value-added offerings, sustainability credentials, and technological advancements. Strategic partnerships, capacity expansions, and investments in green chemistry are emerging as key competitive levers across the market.

Product Insights

Acetic acid accounted for the largest share of the organic acids market in 2025, contributing 53.9% of total revenue. Its dominance is attributed to widespread usage across chemical manufacturing, food processing, and industrial applications, particularly as a key intermediate in the production of vinyl acetate monomer and other derivatives. Strong demand from multiple end-use industries continues to support its leading market position.

Lactic acid emerged as the fastest-growing product segment, with a 4.5% CAGR over the forecast period. This growth is driven by increasing demand in biodegradable plastics, food preservation, and pharmaceutical applications. The growing focus on sustainable, bio-based products is further accelerating the expansion of this segment.

Source Insights

The synthetic segment dominated the organic acids market in 2025, accounting for 57.2% of total revenue. This leadership is supported by well-established production technologies, cost efficiency, and large-scale manufacturing capabilities. Synthetic organic acids continue to be widely adopted across chemical, food, and industrial applications due to their consistent quality and reliable supply.

The biomass segment emerged as the fastest-growing source, with a 3.8% CAGR. This growth is driven by increasing demand for sustainable and bio-based products, along with rising regulatory and consumer pressure to reduce environmental impact. Advancements in fermentation technologies and growing investments in green chemistry are further accelerating the adoption of biomass-derived organic acids.

Application Insights

The food and beverage segment accounted for the largest revenue share of 38.7% in the year 2025. This dominance is supported by the widespread use of organic acids as preservatives, acidulants, and flavor enhancers across processed foods and beverages. Growing consumer preference for clean-label, naturally derived ingredients, along with the expansion of packaged and convenience food consumption, is driving strong demand in this segment. Manufacturers are increasingly incorporating organic acids to enhance shelf life while meeting evolving regulatory and quality standards.

The animal feed segment is expected to grow at a CAGR of 3.7%. This growth is largely attributed to the growing shift away from antibiotic growth promoters and the rising adoption of organic acids as effective alternatives to improve gut health and feed efficiency. Expanding livestock production, particularly in developing regions, and the need for higher productivity and disease prevention are further accelerating demand. As a result, feed applications are becoming a key growth engine within the overall organic acids market.

Regional Insights

Asia Pacific led the organic acids market, accounting for 34.6% of global share in 2025, driven by strong industrialization, expanding food processing sectors, and rising demand for animal nutrition. The region benefits from cost-effective production, abundant raw material availability, and a well-established manufacturing base. Rapid urbanization and increasing consumption of packaged foods further support market expansion, while growing investments in bio-based production are strengthening long-term growth prospects.

China Organic Acids Market Trends

China was represented as the largest contributor within Asia Pacific, supported by its dominant manufacturing capacity and export-oriented production of organic acids such as citric and acetic acid. The country benefits from economies of scale, low production costs, and strong domestic demand across food, feed, and chemical industries. The government support for industrial growth and increasing focus on sustainable production are shaping the competitive landscape.

North America Organic Acids Market Trends

North America held a 26.3% share of the global market in 2025, characterized by advanced production technologies and strong demand for high-value and specialty organic acids. The region’s growth is supported by increasing adoption of bio-based chemicals, stringent regulatory standards, and well-established food and pharmaceutical industries. Innovation and sustainability initiatives remain key drivers, with companies focusing on premium and application-specific solutions.

The U.S. organic acids market dominated the North American market, driven by robust demand across food and beverage, pharmaceuticals, and industrial applications. The presence of major global players, coupled with strong R&D capabilities, supports continuous innovation. The growing emphasis on clean-label products and sustainable manufacturing practices is accelerating the shift toward bio-based organic acids.

Europe Organic Acids Market Trends

Europe was accounted for 22.1% of the organic acids market in 2025, supported by strict environmental regulations and a strong focus on sustainability. The region is witnessing increased demand for bio-based and specialty organic acids, particularly in food, pharmaceuticals, and industrial applications. Regulatory frameworks promoting green chemistry and reduced carbon emissions are encouraging innovation and adoption of eco-friendly production processes.

The Germany organic acids market is a key market within Europe, driven by its advanced chemical industry and strong emphasis on technological innovation. The country benefits from a well-developed industrial base and high demand for specialty chemicals, including organic acids used in pharmaceuticals, food processing, and industrial applications. Sustainability initiatives and investments in bio-based production further enhance market growth.

Middle East & Africa Organic Acids Market Trends

The Middle East and Africa market is gradually growing, driven by increasing demand from the food processing and animal feed industries. Growth is supported by rising population, urbanization, and improving economic conditions in select countries. Although the region remains relatively underdeveloped compared to others, ongoing investments in industrial diversification and food security initiatives are expected to create future growth opportunities.

Latin America Organic Acids Market Trends

Latin America represented a developing market for organic acids, supported by growth in the food and beverage and animal feed sectors. Increasing livestock production and rising demand for processed foods are key growth drivers. While the region faces challenges related to economic volatility and infrastructure limitations, improving industrial capabilities and expanding agricultural activities are expected to support steady market expansion.

Key Organic Acids Market Company Insights

BASF is a leading participant in the organic acids market, leveraging its strong global presence, integrated value chain, and advanced chemical manufacturing capabilities. The company benefits from its “Verbund” production model, which enhances operational efficiency by optimizing resource utilization and reducing production costs. BASF’s broad portfolio of organic acids, particularly acetic acid and its derivatives, is widely used across industries such as chemicals, food processing, pharmaceuticals, and coatings, enabling the company to maintain a diversified revenue base. From a strategic perspective, BASF focuses on innovation, sustainability, and process optimization to strengthen its competitive position.

Key Organic Acids Companies:

The following key companies have been profiled for this study on the organic acids market.

- Cargill, Incorporated

- BASF

- DuPont

- Henan Jindan lactic acid Technology Co., Ltd..

- ADM

- Eastman Chemical Company

- Corbion

- dsm-firmenich

- Tate & Lyle

- Polynt S.p.A.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: BASF, Cargill, Incorporated, DuPont, ADM, Corbion, DSM-Firmenich, and Eastman Chemical Company.

- Major companies emphasize large-scale fermentation technologies and integrated raw material sourcing to maintain consistent organic acid production efficiency across food, pharmaceutical, and industrial applications globally.

- They also expand bio-based product portfolios and strengthen partnerships with food processors and animal nutrition manufacturers to increase long-term commercial demand worldwide.

- Leading manufacturers benefit from advanced biotechnology expertise, extensive global distribution networks, and diversified organic acid portfolios supporting multiple end-use industries efficiently and consistently.

- Their strong research capabilities and established customer relationships help maintain product quality, regulatory compliance, and competitive positioning across international organic acids markets globally.

- Major players face high dependence on agricultural feedstocks, making production costs vulnerable to fluctuations in corn, sugar, molasses, and starch raw material prices.

- They also encounter pricing pressure from low-cost synthetic substitutes and regional manufacturers offering competitively priced organic acid products in developing industrial markets.

Emerging Players: Henan Jindan Lactic Acid Technology Co., Ltd., Tate & Lyle, and Polynt S.p.A.

- Emerging companies focus on specialized organic acid production, targeting niche applications in biodegradable plastics, food preservation, and regional pharmaceutical manufacturing industries globally.

- They also prioritize regional expansion, flexible production capabilities, and customized formulations to strengthen customer relationships and penetrate price-sensitive developing markets effectively.

- These players benefit from cost-efficient regional manufacturing operations and faster adaptation to changing customer requirements within food, feed, and industrial application sectors globally.

- Their focused product specialization and growing investments in fermentation technologies support competitive differentiation in selected organic acid market segments worldwide.

- Emerging companies often face limited global distribution reach and lower financial capacity compared to multinational manufacturers dominating large-volume organic acid supply contracts internationally.

- They also experience challenges in scaling production capacities and maintaining consistent regulatory compliance across multiple countries and industrial application standards globally.

Recent Developments

-

BASF implemented a price increase of 250 euro per metric ton for formic acid across Europe, effective immediately or as per existing contracts. The move reflects rising production costs and sustained demand from applications such as animal feed preservation, silage treatment, and industrial processing, indicating tightening supply conditions and a firm pricing environment in the regional market.

-

DuPont introduced AmberLite FPA57, an advanced anion exchange resin designed to enhance efficiency in organic acid purification. The product improves processing capacity, extends operational cycles, and minimizes fouling, enabling manufacturers of lactic and citric acids to achieve higher productivity and cost optimization while supporting consistent product quality across key end-use industries.

-

Mitsubishi Gas Chemical entered into a joint research agreement with Veritas In Silico to develop nucleic acid-based therapeutics and establish scalable manufacturing methods using QbD principles. The collaboration underscores the company’s strategic focus on expanding into high-value pharmaceutical applications, where organic acid derivatives play a critical role in enabling advanced drug development and production processes.

Organic Acids Market Report Scope

Report Attribute

Details

Market size in 2025

USD 19.1 billion

Estimated market size in 2026

USD 19.7 billion

Projected market size by 2033

USD 25.2 billion

Growth rate

CAGR of 3.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Application, product, source, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

Cargill, Incorporated; BASF; DuPont; Henan Jindan lactic acid Technology Co.,Ltd; ADM; Eastman Chemical Company; Corbion; dsm-firmenich; Tate & Lyle; Polynt S.p.A.

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Organic Acids Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global organic acids market report based on application, product, source, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

Acetic Acid

-

Citric Acid

-

Formic Acid

-

Lactic Acid

-

Propionic Acid

-

Malic Acid

-

Other Products

-

-

Source Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

Biomass

-

Synthetic

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

Food and Beverage

-

Animal Feed

-

Chemical and Industrial

-

Pharmaceuticals

-

Other End Uses

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Billion; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Trade Assessment

Detailed historical import-export analysis of organic acids under relevant HS codes, covering trade volume, trade revenue, key exporting and importing countries, regional shipment flows, and supply-demand dynamics across major global organic acid markets.

Support sourcing strategy development and supply chain optimization through enhanced visibility into international trade dependencies, pricing movements, and country-level organic acid trade patterns.

Competitive Benchmarking

Comparative evaluation of organic acid manufacturers based on production capacity, fermentation technology capabilities, product portfolio strength, global distribution networks, raw material integration, sustainability initiatives, and strategic expansion activities.

Assist supplier assessment and competitive intelligence activities through a deeper understanding of manufacturer positioning, operational strengths, and technological competitiveness within the global organic acids market.

Opportunity Assessment

Assessment of emerging opportunities associated with rising processed food demand, bio-based chemical adoption, biodegradable plastics development, animal nutrition expansion, and increasing pharmaceutical and personal care applications globally.

Help identify future revenue streams and high-growth application areas through enhanced insights into evolving consumer preferences, sustainability trends, and industrial demand for organic acid products worldwide.

Frequently Asked Questions About This Report

Food and beverage segment led with a 38.7% revenue share in 2025.

Acetic acid segment held the highest market share of 3.05% in 2025. while lactic acid is the fastest-growing segment.

Synthetic segment held the highest market share of 57.2% in 2025, while biomass is the fastest-growing segment.

Key factors include rising demand for natural and safe preservatives in the food and beverage industry, along with increasing use in animal feed as an alternative to antibiotics. Additionally, growing preference for bio-based and sustainable chemicals, coupled with expanding applications in pharmaceuticals and industrial sectors, is further supporting market growth.

The global organic acids market was valued at USD 19.1 billion in 2025 and is projected to reach around USD 19.7 billion in 2026.

The global organic acids market is anticipated to grow at a compound annual growth rate (CAGR) of about 3.6% from 2026 to 2033, reaching an estimated value of USD 25.2 billion by 2033.

Asia Pacific emerged as the leading regional market, accounting for a 34.6% revenue share in 2025.

Key players operating in the market include Cargill, Incorporated; BASF SE; DuPont de Nemours, Inc.; Henan Jindan Lactic Acid Technology Co., Ltd.; Archer-Daniels-Midland Company (ADM); Eastman Chemical Company; Corbion N.V.; dsm-firmenich; Tate & Lyle PLC; and Polynt S.p.A. These companies focus on innovation, large-scale production, and strategic collaborations to strengthen their market position.

About the Author(s)

Organic Chemicals Research Team

Bulk Chemicals · Organic ChemicalsThis report was authored by the organic chemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the organic chemicals segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.