- Home

- »

- Advanced Interior Materials

- »

-

Packaging Machinery Market Size, Share Report, 2026-2033GVR Report cover

![Packaging Machinery Market (2026 - 2033)Report]()

Packaging Machinery Market (2026 - 2033)

Size, Share & Trends Analysis Report By Machine Type (Filling, Labelling, Form Fill & Seal, Cartoning, Wrapping, Palletizing, Bottling Line), By Application (Pharmaceuticals, Food, Beverages, Chemicals, Personal Care), By Region, And Segment Forecasts

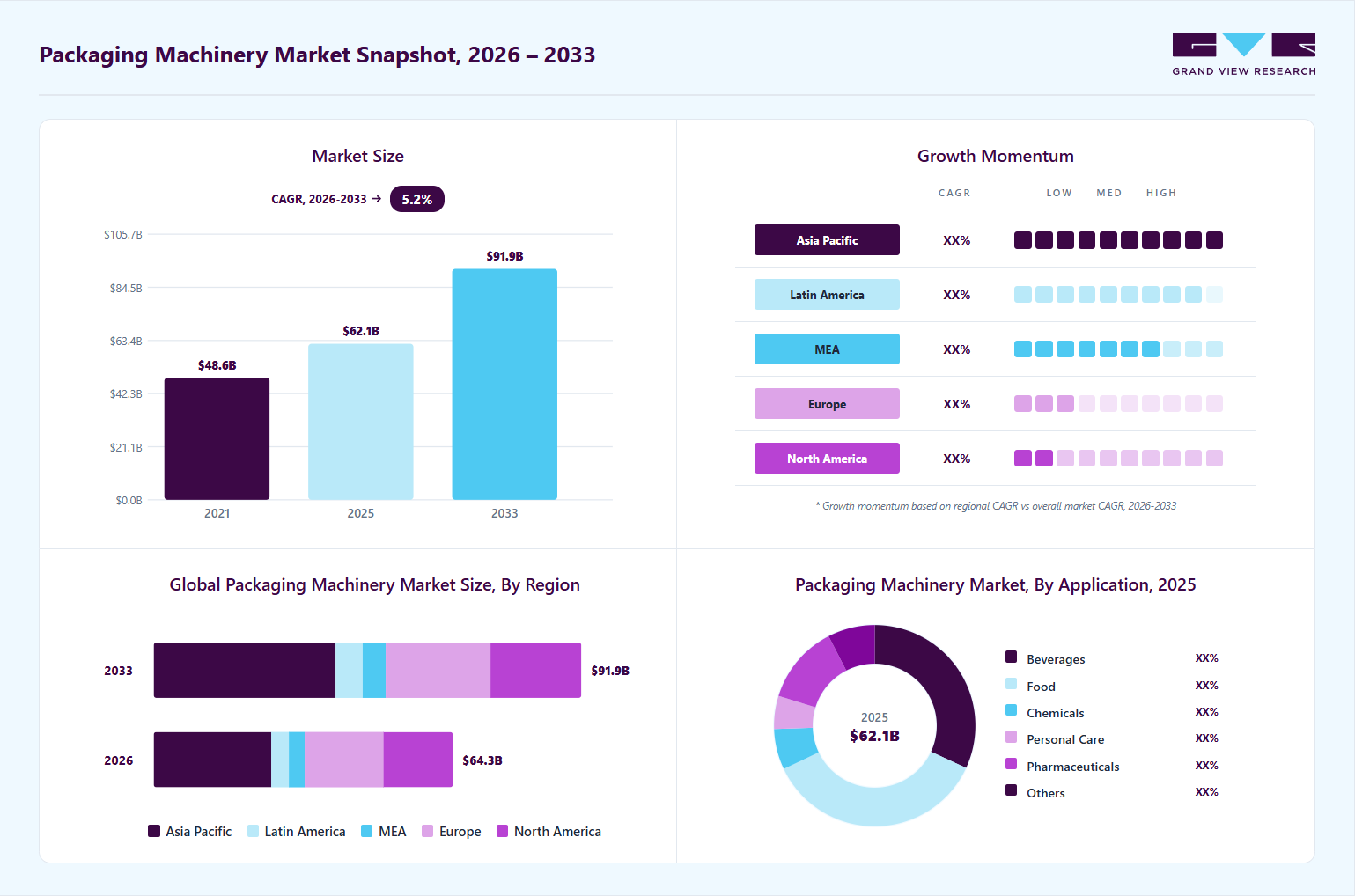

Market Size, 2025

$62.1BMarket Estimate, 2026

$64.3BMarket Forecast, 2033

$91.9BCAGR, 2026–2033

5.2%Packaging Machinery Market Summary

The global packaging machinery market size was valued at USD 62.1 billion in 2025 and is projected to grow from USD 64.3 billion in 2026 to USD 91.9 billion by 2033, at a CAGR of 5.2% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 38.8% in 2025. The market is experiencing significant growth driven by various factors, including the rising demand for packaged goods, advancements in technology, and increasing consumer preferences for convenience.

Key Market Trends & Insights

- By machine type: Filling machine type segment led the market and accounted for a revenue share of 19.7% in 2025.

- By application: Food application segment led the market and accounted for a share of 36.0% in 2024.

Regional Highlights

- Largest regional market: Asia Pacific (38.8% revenue share, 2025)

- By country: The packaging machinery market in China held the largest share in the Asia Pacific region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 62.1 Billion

- Estimated Market Size in 2026: USD 64.3 Billion

- Projected Market Size by 2033: USD 91.9 Billion

- CAGR (2026-2033): 5.2%

As e-commerce continues to expand, manufacturers are investing in automated and flexible packaging solutions to enhance production efficiency and reduce labor costs. Additionally, the growing emphasis on sustainability is pushing companies to adopt eco-friendly packaging materials and machinery that minimize waste.")

Increasing demand for packaging machinery can be attributed to the need for differentiating products in the retail space. Consumers are demanding greater product diversity and a wider range of products. The pandemic has had a significant impact on people's lifestyles and purchasing habits. Following the lockdown, people panicked buying increased the demand for packaged food products. Customers' preferences for healthy and natural foods prompted packaged food companies to diversify their product lines. As a result, the demand for packaged food products, such as intermediary food items, ready-to eat food, and frozen foods, increased during the lockdown period. During the initial phases of the lockdown, consumers stocked up on ready-to-eat and ready-to-cook products.

Market Dynamics

The packaging machinery market is shaped by strong demand from food, beverage, pharmaceutical, and e-commerce industries, increasing automation adoption, and the need for higher production efficiency. Market growth is supported by technological advancements such as robotics, smart sensors, and Industrial Internet of Things (IIoT)-enabled equipment, while opportunities are emerging from the shift toward sustainable and recyclable packaging materials. However, high capital investment requirements, long equipment replacement cycles, and integration complexities continue to restrain adoption. Regulatory requirements related to food safety, product traceability, labeling, and environmental sustainability are influencing equipment design and investment decisions, while competition among machinery manufacturers is driving innovation, customization capabilities, and the development of more flexible, energy-efficient packaging solutions.

The increasing consumption of packaged food and beverages is a primary driver of the packaging machinery market. Rapid urbanization, changing lifestyles, higher disposable incomes, and growing preference for convenience foods have led manufacturers to expand production capacities and improve packaging efficiency. Demand for ready-to-eat meals, snacks, dairy products, bottled beverages, and frozen foods has intensified the need for high-speed filling, sealing, labeling, wrapping, and palletizing equipment. Additionally, growing emphasis on food safety, shelf-life extension, and attractive packaging designs is encouraging food and beverage producers to invest in advanced packaging machinery that enhances productivity while ensuring consistent product quality.

Long replacement cycles of packaging equipment act as a significant restraint on market growth, as packaging machinery is designed for durability and can remain operational for many years with regular maintenance and upgrades. Many manufacturers prefer refurbishing, retrofitting, or upgrading existing systems rather than investing in entirely new equipment due to the substantial capital costs involved. This limits the frequency of new machinery purchases, particularly among established food, beverage, and industrial manufacturers with mature production facilities. Consequently, demand is often tied to capacity expansion projects, technological obsolescence, or regulatory changes rather than routine equipment replacement.

The increasing focus on sustainability presents a major growth opportunity for the packaging machinery market. Governments, brand owners, and consumers are placing greater emphasis on reducing packaging waste, improving recyclability, and minimizing environmental impact. This transition is driving demand for machinery capable of processing recyclable, biodegradable, compostable, and lightweight packaging materials while maintaining production efficiency and product protection. Packaging equipment manufacturers are responding by developing flexible systems that can handle a wider range of sustainable materials and package formats, enabling customers to meet evolving environmental regulations and corporate sustainability goals without compromising operational performance.

Analyst Perspective

The packaging machinery market is being shaped by the convergence of automation, sustainability, and changing consumer purchasing patterns. As manufacturers face increasing pressure to improve productivity, reduce operational costs, and enhance packaging flexibility, investments in advanced filling, labeling, cartoning, palletizing, and form-fill-seal systems continue to accelerate. The growing complexity of product portfolios, shorter production runs, and the expansion of e-commerce channels are driving demand for highly adaptable and digitally integrated packaging equipment. In addition, the transition toward sustainable packaging materials is creating opportunities for machinery upgrades and new equipment installations capable of handling recyclable and lightweight packaging formats. Looking ahead, market growth is expected to be supported by continued automation investments in developed economies and expanding manufacturing capacity across emerging markets, positioning technologically advanced equipment providers to benefit from long-term industry modernization trends.

Drivers, Opportunities & Restraints

The packaging machinery market is driven by the increasing demand for convenience and ready-to-eat foods, as consumers seek quick and easy meal solutions. The rise of e-commerce further fuels this demand, necessitating efficient and protective packaging to ensure product integrity during transport. Additionally, advancements in automation and smart technologies enhance production efficiency and reduce operational costs, making packaging processes faster and more reliable. The growing emphasis on sustainability also pushes manufacturers to adopt eco-friendly packaging solutions, creating a favorable environment for the development of innovative machinery.

Despite its growth potential, the market faces challenges such as high initial investment costs associated with advanced technologies. Smaller companies may find it difficult to afford these investments, hindering their competitiveness. Additionally, the complexity of integrating new machinery with existing systems can disrupt production, while a shortage of skilled labor to operate and maintain sophisticated equipment further complicates matters. Regulatory compliance concerning food safety and environmental impact also adds to operational costs and may slow the adoption of new technologies.

The market presents significant opportunities, particularly in emerging economies where rising consumer demand for packaged goods is driving growth. Technological innovations, such as smart packaging and automation, allow manufacturers to improve efficiency and product traceability, catering to evolving consumer preferences. Moreover, the trend toward personalized packaging creates opportunities for differentiation, enabling brands to enhance their identity and engage consumers. As companies seek to meet these demands, the market for flexible and adaptable packaging machinery is expected to expand, offering substantial growth prospects.

Machine Type Insights

Based on machine type, the filling segment led the market with the largest revenue share of 19.7% in 2025. Filling machines are classified into semi-automatic and automatic filling machines. While semiautomatic filling machines require minimal human intervention, automatic filling machines cover the processes of filling, packing, and cardboard casing by integrating other packaging machines. Reducing manual labor and saving time on the packaging would result in increased productivity. Furthermore, using a filling machine allows for a predetermined quantity of filling, consistent quality, and efficient operation.

Form-Fill-Seal (FFS) machines are packaging machines that fill and seal a package on the same machine. These are highly sophisticated machines with control networks and computer interfaces. Many businesses prefer to use FFS systems because they provide additional advantages such as versatility and speed.

Application Insights

Based on application, the food segment led the market with the largest revenue share of 36.0% in 2025. Food end-use industry is the largest consumer group in the packaging machinery market. Increasing demand for ready-to-eat, convenience food items is anticipated to favor the growth of the market. Apart from this, there has been a trend toward the consumption of healthy and organic food products which require a special type of packaging to maintain the authenticity and richness of the food products which is projected to further augmented the demand for packaging machinery. Additionally, consumers also look for easy-to-use and attractive packaging, which has forced food manufacturers to develop artistic packaging to gain a competitive advantage which in turn has driven the demand for packaging machinery.

Packaging machinery is used in a variety of beverage applications such as beer, bottled water, soda pop, boxes of drink pouches, drink mixes, sparkling fruit coolers, sport drinks wine, and fruit juice. Liquid fillers, capping machines, and labeling machines are some of the packaging machinery used in beverage industry. Tetra Laval, Krones AG, Coesia Group, and others are major manufacturers of packaging machinery.

Regional Insights

North America region accounted for 23.8% of the global market share in 2024. Increasing demand for processed food & beverages, growing immigration, and technological advancement in packaging equipment are some of the key factors responsible for driving the market growth. The growth is also driven by factors such as rapid urbanization, rising spending power, high household income, industrialization, and shifting consumer food preferences.

U.S. Packaging Machinery Market Trends

The packaging machinery market in the U.S. is expected to grow at a CAGR of 4.1% from 2025 to 2030. The U.S. market is robust with its growth being propelled by a rising demand for automated solutions in industries such as food and beverage, pharmaceuticals, and cosmetics. Innovation in packaging technologies, including smart machinery and sustainable materials, is helping manufacturers enhance efficiency and meet evolving consumer expectations.

The packaging machinery market in Canada is expected to grow at a CAGR of 4.0% from 2025 to 2030. Canada is experiencing steady growth, fueled by the country's expanding food processing and e-commerce sectors. The focus on sustainable packaging practices is prompting manufacturers to invest in eco-friendly machinery and solutions that comply with stringent environmental regulations.

The Mexico packaging machinery market is expected to grow at a CAGR of 4.6% from 2025 to 2030. Mexico's packaging machinery market is on the rise, supported by a strong manufacturing base and increasing foreign investments in the automotive and food sectors. As demand for flexible and cost-effective packaging solutions grows, local manufacturers are adopting advanced technologies to enhance production capabilities and competitiveness.

Europe Packaging Machinery Trends

The packaging machinery market in Europe held a share of about 26.9% in 2024. The Europe market for packaging machinery is characterized by a strong emphasis on sustainability and regulatory compliance, driving the adoption of eco-friendly packaging solutions. Additionally, advancements in automation and smart technologies are enhancing operational efficiency, catering to the increasing demand for customizable and innovative packaging across various industries.

The Germany packaging machinery market held 23.5% share in the Europemarket in 2024. Germany is home to numerous large manufacturers of packaging machinery. The region is expanding, which can be attributed to the rising demand for German packaging machines from emerging and developing countries. Moreover, the market growth is likely to be driven by global trends such as rising demand for adaptable, highly productive, and efficient packaging equipment to meet changing consumer demands.

The packaging machinery market in the UK held 13.4% share of the Europe market in 2024. The UK market is benefiting from a surge in demand for flexible packaging solutions driven by consumer preferences for convenience and sustainability. Furthermore, the ongoing trend of digitalization in manufacturing is fostering innovation, enabling companies to streamline operations and improve product traceability.

Asia Pacific Packaging Machinery Market Trends

Asia Pacific dominated the packaging machinery market with the largest revenue share of 38.8% in 2025. Rapid population growth and rising consumer purchasing power are likely to fuel the demand for packaged goods, which is anticipated to facilitate regional market growth. Launching production facilities by significant regional players is expected to increase the e-commerce industry, which is anticipated to promote the regional market. North America is primarily driven by the highly established food & beverage industry in the U.S. and Canada. The presence of various multinational food processing and manufacturing companies results in an increased demand for packaging machinery. Technological progress in packaging equipment is also one of the leading factors driving the region’s growth.

The packaging machinery market in China held the largest share in the Asia Pacific region in 2025. The China packaging machinery market is experiencing rapid growth, driven by increasing demand in various sectors such as food and beverage, pharmaceuticals, and cosmetics. Technological advancements and the push for automation are enhancing production efficiency and expanding the market's potential, positioning China as a global leader in packaging machinery manufacturing.

The packaging machinery market in India held 19.6% share in the Asia Pacific region in 2024. The India packaging machinery market is expanding significantly due to the booming e-commerce sector and rising demand for packaged consumer goods. With a focus on sustainability and innovation, manufacturers are investing in advanced technologies to meet the diverse needs of industries such as food processing, pharmaceuticals, and personal care products.

Middle East & Africa Packaging Machinery Market Trends

The packaging machinery market in Middle East & Africa is witnessing steady demand owing to the increased internet penetration, rise of social media influences and demand for organic products, which is expected to drive the cosmetic industry. The growing opportunities in the cosmetics industry both in the Middle East and Africa region are expected to boost the demand for cosmetic packaging such as bottles and vials which, in turn, is expected to boost the regional market growth.

Saudi Arabia packaging machinery market held 36.6% share in the Middle East & Africa region in 2024. The personal care industry's contribution to the country’s economy is growing at an exponential rate. Furthermore, the demand for organic or natural, halal products, as well as innovative and eco-friendly packaging designs, is growing in the country. Moreover, poor water quality, harsh climatic conditions, and a greater emphasis on personal well-being are driving the demand for sophisticated personal care routines and treatments. This, in turn, is expected to increase the demand for packaging machinery.

Latin America Packaging Machinery Trends

The packaging machinery market in Latin America accounted for a market share of 5.8% in 2024. Food & beverage industry in Latin America has experienced tremendous expansion in recent years as a result of industrial sector investments. Rapid urbanization in nations such as Argentina, Brazil, and Chile greatly contributes to the expansion of food & beverage industry. The rising demand for novel flavors and cuisines in food & beverage industry is expected to have a beneficial effect on the market expansion.

Brazil packaging machinery market held 37.4% share in Central & South America in 2024. The Brazil market is expanding due to a resurgence in the food and beverage sector, driven by increasing consumer demand for convenience and ready-to-eat products. Additionally, investments in automation and digital technologies are improving production efficiency and enabling manufacturers to meet the unique packaging needs of a diverse marketplace.

Key Packaging Machinery Company Insights

Some of the key players operating in the packaging machinery market include Tetra Laval International S.A., Krones AG, I.M.A. Industria Macchine Automatiche S.p.A, Sacmi, and GEA Group Aktiengesellschaft.

-

Tetra Laval International S.A. was established in 1993 and is headquartered in Pully, Switzerland. It is a leading multinational company that provides a wide range of systems for the processing, packaging, and distribution of food. The company consists of three industry groups, namely Tetra Pak, Delaval, and Sidel. Tetra Pak manufactures processing, packaging, and distribution machinery for liquid and food products including liquids, ice creams, processed foods, fruits, and vegetables. The company’s production facilities supply packaging material to more than 8,800 packaging machines across the globe. Sidel manufactures plastic packaging and complete packaging lines. Delaval is engaged in the manufacturing of equipment and complete systems for animal husbandry and milk production.

-

Krones AG was established in 1951 and is headquartered in Neutraubling, Germany. The company is engaged in the manufacturing of processing, filling, and packaging lines as well as individual machinery for filling beverages in cans or glass and plastic bottles. It caters to a large set of customers including breweries; juice & soft drink manufacturers; producers of spirits, wine, & sparkling wine; and companies in the liquid food industry. The company also caters to chemical, pharmaceutical, and cosmetic industries. It also offers innovative digitization and intralogistics solutions to its customers. The company’s business segments include digitalization, process technology, bottling & packaging equipment, intralogistics, and lifecycle service. The company’s bottling and packaging equipment segment consists of labeling technology, inspection technology, cleaning technology, plastics technology, packaging filling technology, palletizing technology, and conveyer technology.

Coesia S.p.A., SIG, Bradman Lake, MAILLIS, ROVEMA GmbH, ProMach, and Duravant are some of the emerging players in the packaging machinery market.

-

Coesia S.p.A. was established in 1923 and is headquartered in Bologna, Italy. Coesia S.p.A. is a group of companies engaged in the design, manufacturing, and distribution of industrial and packaging solutions. It operates through three business segments, namely, advanced automated machinery & materials, industrial process solutions, and precision gears.The group offers its services to various industries such as aerospace, automotive, beverage, chemicals, dairy, electronics, food, personal care, industrial goods, and tobacco. It designs and manufactures a wide range of machinery and solutions including filling, packing, cutting, wrapping, cartoning, printing & labeling, feeding, assembly & combining, and monitoring & inspection.

-

SIG was established in 1853 and is headquartered in Neuhausen, Switzerland. SIG Combibloc Group AG is a multinational company and operates as a subsidiary of SIG Combibloc Group Holdings S.à r.l. SIG Combibloc Group AG was formerly known as SIG Holding AG. It has filling technology that enables the highest level of speed and flexibility for production. The company’s filling machines are high in speed, efficient, reliable, and aseptic safety. It is a leading manufacturer and supplier of aseptic carton packaging and filling machines, carton packaging sleeves, spouts, and caps as well as aftermarket services for food & beverage producers worldwide.

Key Packaging Machinery Companies

The following key companies have been profiled for this study on the packaging machinery market.

-

Langley Holding plc

-

Maillis Group

-

Rovema GmbH

-

Douglas Machine Inc.

-

KHS Group

-

SIG

-

Tetra Laval International S.A.

-

Krones AG

-

I.M.A. Industria Macchine Automatiche S.p.A.

-

Syntegon Technology GmbH

-

ProMach

-

GEA Group Aktiengesellschaf

-

Sacmi

-

Coesia S.p.A.

-

Duravant

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., The Tetra Laval Group, Krones AG, Syntegon Technology GmbH)

- Mature players focus on delivering comprehensive packaging solutions across multiple machine categories and end-use industries.

- Their growth strategies are centered on continuous product innovation, global service network expansion, digitalization of packaging operations, and strategic acquisitions that broaden their technology portfolios and geographic reach.

- These companies increasingly emphasize turnkey packaging lines, automation, and sustainability-focused solutions to strengthen long-term customer relationships.

- Their primary strengths include extensive installed bases, strong brand recognition, global distribution and service capabilities, broad product portfolios, and deep expertise across food, beverage, pharmaceutical, and consumer goods applications.

- Their scale enables them to execute large, complex packaging projects while offering integrated solutions that improve production efficiency and operational reliability.

- Large organizational structures and extensive product portfolios can reduce operational flexibility and lengthen product development cycles.

- Additionally, their significant exposure to mature markets and large capital projects can make growth more dependent on economic conditions and customer capital expenditure cycles.

Emerging & Regional Players (e.g., ROVEMA GmbH, Pro Mach, Inc., regional players)

- Some of the merging players primarily pursue growth through targeted acquisitions, niche market specialization, and expansion into high-growth packaging segments.

- On the other hand, many focus on flexible manufacturing solutions, automation technologies, and customer-specific packaging systems to build market share.

- Their strategies often emphasize agility, innovation, and rapid portfolio expansion in underserved or evolving application areas.

- These companies benefit from greater operational flexibility, faster decision-making, and the ability to respond quickly to changing customer requirements.

- Their focused approach enables them to develop specialized solutions, capitalize on emerging packaging trends, and compete effectively in growth-oriented market segments.

- Emerging players tend to possess smaller installed bases, more limited global service networks, and lower brand recognition than established industry leaders.

- They may also face challenges in securing large multinational contracts and maintaining consistent growth as they integrate acquisitions and scale operations across new markets

Recent Developments

-

In February 2024, IMA Group, a producer of automatic machines for pharmaceutical, food, and battery processing and packaging, unveiled two artificial intelligence (AI) solutions designed to improve the efficiency and effectiveness of its customer services. The IMA Sandbox solution is a collaborative, cloud-based platform that facilitates co-development and partnership in creating advanced algorithms within a secure and shared environment.

-

In July 2024, Eliter Packaging Machinery launched its newest model of automatic sleeving machine, the Multi-Wrap C-80S, designed for multipacks with a maximum speed of 80 wraps per minute. This machine efficiently groups packaging containers such as cans, bottles, cups, and pots into various configurations, ranging from 1x2x1 to 1x4x1, as well as cluster-pack formats like 2x2x1 and 2x3x1. It features a grouping system that enables quick changeovers to accommodate different packaging arrangements.

-

In July 2024, Cama Group introduced a new top-loading packaging machine, the MTL. This flexible, modular system significantly enhances the efficiency of packaging a variety of boxes.

Packaging Machinery Market Report Scope

Report Attribute

Details

Market size in 2025

USD 62.1 billion

Estimated market size in 2026

USD 64.3 billion

Projected market size by 2033

USD 91.9 billion

Growth rate

CAGR of 5.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Machine type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; Russia; Spain; Italy; China; India; Japan; Australia; South Korea; Brazil; Saudi Arabia; UAE

Key companies profiled

Langley Holding plc; Maillis Group; Rovema GmbH; Douglas Machine Inc.; KHS Group; SIG; Tetra Laval International S.A.; Krones AG; I.M.A. Industria Macchine Automatiche S.p.A.; Syntegon Technology GmbH; ProMach; GEA Group Aktiengesellschaf; Sacmi; Coesia S.p.A.; Duravant

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Packaging Machinery Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global packaging machinery market report based on machine type, application, and region:

-

Machine Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Filling

-

Labelling

-

Form Fill & Seal

-

Cartoning

-

Wrapping

-

Palletizing

-

Bottling Line

-

Others

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Beverages

-

Food

-

Chemicals

-

Personal Care

-

Pharmaceuticals

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Russia

-

UK

-

Spain

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Machine Type

Revenue Capture Definition

Filling Machines

Filling machines are packaging systems designed to accurately dispense liquids, powders, granules, pastes, or semi-solid products into containers such as bottles, cans, pouches, cartons, or jars before sealing and distribution.

Labelling Machines

Labelling machines automatically apply product identification, branding, regulatory, and tracking labels onto packaged goods, ensuring consistency, accuracy, and compliance with industry requirements.

Form Fill & Seal Machines

Form Fill & Seal (FFS) machines integrate package formation, product filling, and sealing operations into a single automated process, commonly used for flexible packaging formats such as pouches, sachets, and bags.

Cartoning Machines

Cartoning machines are automated systems that erect, fill, and close cartons or boxes around products, providing protection, handling convenience, and retail-ready packaging.

Wrapping Machines

Wrapping machines apply protective packaging materials such as films, stretch wraps, or shrink wraps around products or product groups to enhance stability, protection, and presentation during transportation and storage

Palletizing Machines

Palletizing machines automatically arrange and stack packaged products onto pallets according to predefined patterns, improving warehouse efficiency, handling, and logistics operations.

Bottling Lines

Bottling lines are integrated packaging systems comprising multiple machines that perform bottle filling, capping, labeling, inspection, and packaging operations in a continuous production sequence

Others

This category includes specialized or ancillary packaging equipment such as closing, case / tray handling, bottling line, bundling, conveying, feeding & handling, inspection & testing equipment.

Segment - End Use

Revenue Capture Definition

Beverages

The beverage segment includes manufacturers of alcoholic and non-alcoholic drinks that utilize packaging machinery for filling, sealing, labeling, wrapping, and palletizing products in bottles, cans, cartons, and flexible packaging formats.

Food

The food segment comprises producers of processed foods, dairy products, bakery items, confectionery, frozen foods, and snacks that rely on packaging machinery to ensure product safety, shelf life, and efficient distribution.

Chemicals

The chemicals segment includes manufacturers of industrial, agricultural, and specialty chemical products that require packaging equipment for safe handling, filling, labeling, and transportation of liquids, powders, and hazardous materials.

Personal Care

The personal care segment encompasses manufacturers of cosmetics, skincare products, toiletries, fragrances, and hygiene products that use packaging machinery to support high-speed, precise, and aesthetically consistent packaging operation.

Pharmaceutical

The pharmaceutical segment includes drug manufacturers and healthcare product producers that utilize packaging machinery for filling, blister packaging, labeling, serialization, and cartoning while meeting stringent regulatory and quality standards.

Others

This category includes niche industries automotive, electronics and electrical equipment, construction components, machinery, and luxury goods among others.

Estimation Model

Manufacturer Revenue Mapping Layer

Production Capacity & Shipment Layer

Channel & Regional Distribution Layer

Revenue Layer

Who supplies packaging machinery?

How many machines are supplied annually?

How does equipment reach end users?

How much market revenue is generated?

Identify major packaging machinery manufacturers and system integrators globally. Analyze company revenues attributable to packaging equipment, business segment disclosures, annual reports, investor presentations, and product portfolio allocations to establish the organized market base.

Estimate manufacturing capacity, annual equipment shipments, order backlogs, production volumes, and regional manufacturing footprints of key suppliers. Assess output by machine type including filling, labeling, form-fill-seal, cartoning, wrapping, palletizing, and bottling systems.

Analyze OEM sales, distributor networks, system integrators, and regional sales channels. Allocate equipment shipments across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa based on supplier presence, installation activity, and end-user demand.

Translate annual equipment demand into revenue using machine-specific ASPs and project values. Cross-validate estimates with manufacturer revenues, shipment data, order activity, and installed equipment trends to derive the total market value.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Company Market Share Analysis

A market share analysis of leading packaging machinery manufacturers was conducted, highlighting their relative positions within the global market. The assessment evaluated company revenues, product portfolio strength, geographic presence, end-use industry exposure, and strategic developments to estimate the competitive standing of key participants.

This analysis helped the client to understand the competitive structure of the market, identify market leaders and challengers, and benchmark company performance against peers. The insights aided in competitive intelligence, partnership evaluations, and strategic planning initiatives.

Regional Segmentation

The study provided a regional analysis of the packaging machinery market, including market size, growth trends, demand drivers, technology adoption patterns, and end-use industry dynamics across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

This analysis enabled stakeholders to identify high-growth regions, evaluate regional demand variations, and understand the influence of manufacturing activity, consumer goods production, automation investments, and regulatory requirements on market development. The findings supported geographic expansion and resource allocation decisions.

Opportunity Assessment

The report included a comprehensive opportunity assessment identifying attractive growth areas across machine types, end-use industries, technologies, and regional markets. A particular emphasis was placed on automation, smart packaging systems, sustainable packaging solutions, and emerging manufacturing hubs.

This assessment helped the client to prioritize investment opportunities, identify underserved market segments, and align product development strategies with evolving industry requirements. It also provided an outlook of areas expected to generate the strongest growth potential during the forecast period.

Frequently Asked Questions About This Report

The global packaging machinery market size was estimated at USD 62.1 billion in 2025 and is expected to reach USD 64.3 billion in 2026.

The global packaging machinery market, in terms of revenue, is expected to grow at a compound annual growth rate of 5.2% from 2026 to 2033 to reach USD 91.9 billion by 2033.

Some of the key players operating in the packaging machinery market include Langley Holding plc, Maillis Group, Rovema GmbH, Douglas Machine Inc., KHS Group, SIG, Tetra Laval International S.A., Krones AG, I.M.A. Industria Macchine Automatiche S.p.A., Syntegon Technology GmbH, ProMach, GEA Group Aktiengesellschaf, Sacmi, Coesia S.p.A., Duravant, among others.

The packaging machinery market is experiencing significant growth driven by various factors, including the rising demand for packaged goods, advancements in technology, and increasing consumer preferences for convenience.

Asia Pacific dominated the packaging machinery market with the largest revenue share of 38.8% in 2025.

Asia Pacific is anticipated to be one of the fastest-growing regional markets over the forecast period, supported by expanding manufacturing activities, rising consumer goods production, and increasing packaging automation investments.

The filling segment led the market with the largest revenue share of 19.7% in 2025.

Key trends include increasing adoption of automation and robotics, integration of smart packaging technologies, growing demand for flexible packaging solutions, and machinery designed for sustainable packaging materials.

The food segment accounted for 36.0% of the market in 2025, maintaining its position as the largest application area due to the growing demand for packaged, ready-to-eat, and convenience food products worldwide.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.