- Home

- »

- Plastics, Polymers & Resins

- »

-

Pharmaceutical Contract Packaging Market Size Report 2033GVR Report cover

![Pharmaceutical Contract Packaging Market (2026 - 2033)Report]()

Pharmaceutical Contract Packaging Market (2026 - 2033)

Size, Share & Analysis Report By Packaging Type (Primary, Secondary, Tertiary), By Material (Plastics, Paper & Paperboard, Glass, Aluminum Foil), By Region (North America, Europe, Asia Pacific, Latin America, MEA), And Segment Forecasts

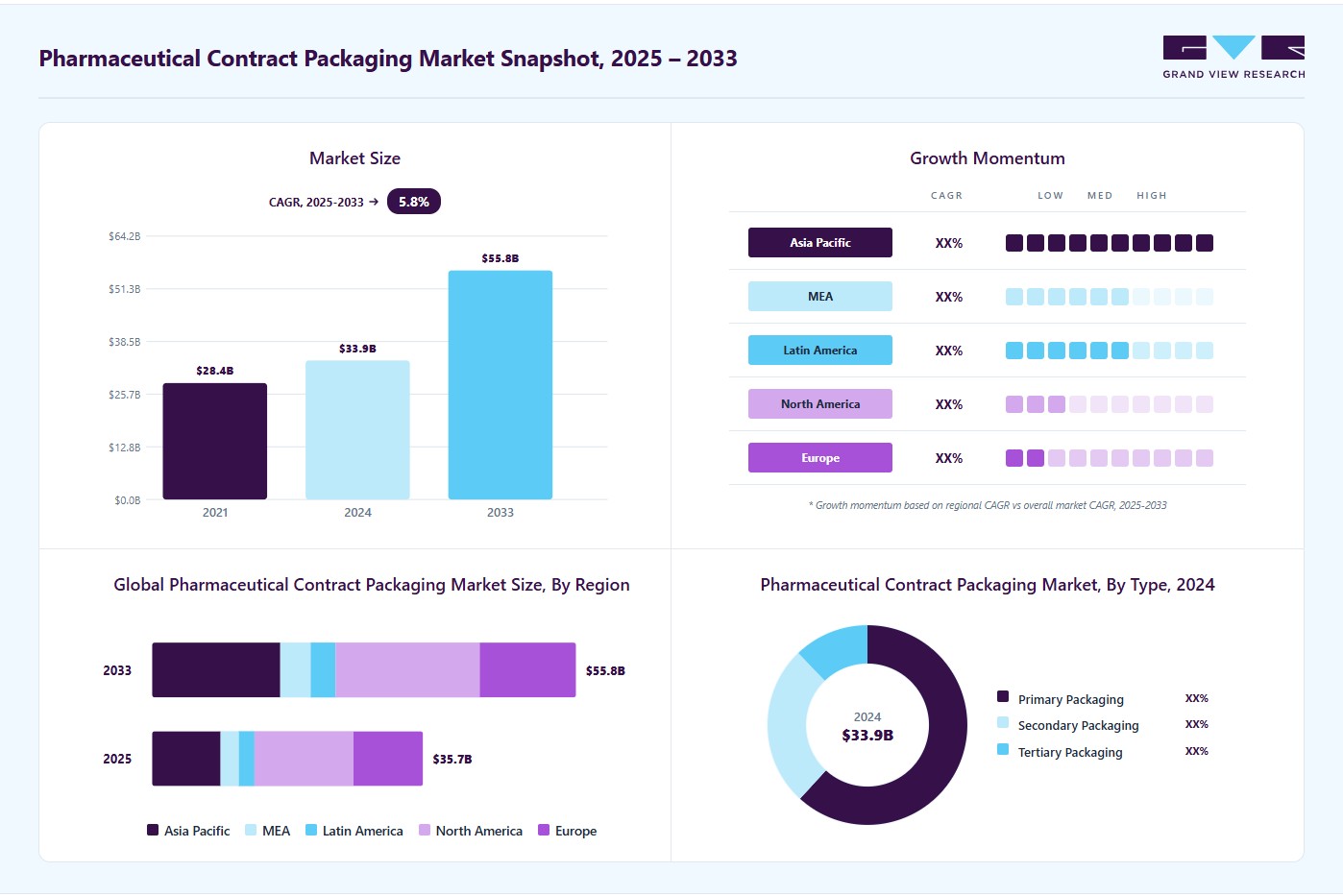

Market Size, 2025

$35.7BMarket Estimate, 2026

$37.6BMarket Forecast, 2033

$55.8BCAGR, 2026–2033

5.8%Pharmaceutical Contract Packaging Market Summary

The global pharmaceutical contract packaging market size was valued at USD 35.7 billion in 2025 and is projected to grow from USD 37.6 billion in 2026 to USD 55.8 billion by 2033, growing at a CAGR of 5.8% from 2026 to 2033. North America dominated the market with the largest revenue share of 36.5% in 2025. Growth outlook is driven by the increasing trend of outsourcing packaging operations to specialized contract packaging companies.

Key Market Trends & Insights

- By material: Plastic- segment led the market with the largest revenue share of 38.3% in 2025.

- By packaging type: Primary packaging segment led the market with the largest revenue share of 62.0% in 2025.

Regional Highlights

- Largest regional market: North America (36.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 35.7 Billion

- Estimated market size in 2026: USD 37.6 Billion

- Projected market size by 2033: USD 55.8 Billion

- CAGR (2026-2033): 5.8%

Facing pressure to cut costs and increase operational efficiency, pharmaceutical companies find outsourcing an effective solution. By partnering with packaging suppliers, they can focus on their core activities, such as drug discovery and development, leaving behind complex packaging, including compliance with regulatory requirements and managing new packaging for outside experts.Another key factor driving the market's growth is the demand for customized, complex packaging products such as biologics, biosimilars, and personalized medicines that require specialized packaging. For instance, biologics and injectables often require temperature-controlled, sterile, non-deformable packaging to ensure packaging stability and safety. Contract packaging suppliers have increasingly deployed the technical capabilities and resources to handle these complex packaging requirements, ensuring that pharmaceutical companies deliver quality to consumers while meeting stringent regulatory standards.

")

Moreover, pharmaceutical products are subject to safety regulations, such as serialization requirements for traceability and compliance with Good Manufacturing Practices (GMP), ensuring that packaging adheres to the specific guidelines of regulatory bodies such as the FDA, EMA, and other regional agencies. Since packaging is critical to drug safety and counterfeit assurance, pharmaceutical companies have increasingly relied on experienced contract packagers to meet these evolving regulatory requirements and drive overall market expansion.

The growth of biopharmaceuticals and personalized medicine is another factor linking pharmaceutical industry expansion to packaging demand. Biologics and advanced therapies such as cell and gene therapies often require highly specialized packaging environments, including cold chain logistics and sterile containment. Contract packagers with expertise in temperature-controlled packaging, lyophilized product packaging, and prefilled syringes are increasingly sought after. For example, companies such as PCI Pharma Services and Catalent have expanded their facilities to support biologics packaging, reflecting the growing need for customized solutions aligned with pharmaceutical innovation trends.

Moreover, the globalization of pharmaceutical production and distribution magnifies the importance of contract packaging. With cross-border supply chains and rising exports of medicines from countries like India (the world’s largest supplier of generics) and China (a major API and formulation producer), packaging must meet diverse international regulatory standards such as FDA, EMA, and MHRA guidelines. Contract packagers act as strategic partners by offering multi-market compliant packaging and serialization services, enabling pharmaceutical companies to enter new geographies efficiently. This global expansion of the pharmaceutical industry, therefore, directly translates into sustained growth opportunities for contract packaging providers.

Market Dynamics

The pharmaceutical contract packaging market is experiencing robust growth driven by the increasing outsourcing of packaging operations by pharmaceutical and biotechnology companies, rising demand for specialized packaging solutions, and the growing complexity of drug formulations. Pharmaceutical manufacturers are increasingly partnering with contract packaging organizations (CPOs) to improve operational efficiency, reduce capital expenditures, ensure regulatory compliance, and accelerate time-to-market. The growing demand for biologics, injectables, personalized medicines, and high-value specialty drugs has significantly increased the need for advanced packaging capabilities, including sterile packaging, serialization, labeling, and cold-chain solutions. Additionally, stringent regulatory requirements related to product traceability, patient safety, and anti-counterfeiting measures are encouraging pharmaceutical companies to leverage the expertise of specialized contract packaging providers, supporting market expansion globally.

The growing trend of outsourcing packaging operations is a major factor driving the pharmaceutical contract packaging market. Pharmaceutical and biotechnology companies are increasingly focusing on their core competencies such as drug discovery, research and development, and commercialization, while outsourcing packaging activities to specialized service providers. Contract packaging organizations offer advanced packaging technologies, regulatory expertise, flexible production capacities, and cost-efficient operations, enabling pharmaceutical companies to optimize their supply chains and reduce operational complexities.

The rapid growth of biologics, biosimilars, vaccines, and injectable therapies further supports market demand. These products often require specialized packaging solutions, including sterile filling, cold-chain packaging, tamper-evident features, and serialization capabilities. Additionally, the increasing volume of clinical trials, expanding pharmaceutical production in emerging markets, and rising demand for patient-centric packaging formats such as prefilled syringes, blister packs, and unit-dose packaging are creating substantial opportunities for contract packaging providers. As pharmaceutical companies continue to seek greater flexibility and scalability, outsourcing packaging operations is expected to remain a key market growth driver.

Stringent regulatory requirements and complex quality assurance standards present significant challenges for the pharmaceutical contract packaging market. Contract packaging providers must comply with rigorous regulations established by health authorities and regulatory agencies regarding Good Manufacturing Practices (GMP), serialization, labeling accuracy, product traceability, contamination control, and packaging validation. Maintaining compliance across multiple jurisdictions can increase operational complexity and require substantial investments in quality systems, technology infrastructure, and workforce training. Additionally, packaging errors, labeling inaccuracies, and non-compliance with serialization mandates can result in product recalls, regulatory penalties, and reputational damage. The growing complexity of biologics, specialty pharmaceuticals, and temperature-sensitive products further increases the need for specialized packaging processes and strict quality controls. These factors create barriers for smaller contract packaging providers and can limit market expansion in highly regulated pharmaceutical environments.

The increasing demand for advanced pharmaceutical packaging solutions presents significant growth opportunities for market participants. Pharmaceutical companies are increasingly seeking contract packaging partners that can provide value-added services such as serialization, aggregation, anti-counterfeiting technologies, smart packaging, track-and-trace systems, and cold-chain packaging solutions. The implementation of global drug serialization regulations and rising concerns regarding counterfeit pharmaceuticals are accelerating investments in advanced packaging technologies. Furthermore, the expanding commercialization of biologics, cell and gene therapies, personalized medicines, and temperature-sensitive pharmaceutical products is generating strong demand for specialized packaging expertise. Contract packaging organizations offering integrated services, including packaging design, labeling, serialization, warehousing, and distribution support, are well-positioned to capitalize on these opportunities. Additionally, pharmaceutical manufacturing expansion across Asia-Pacific, Latin America, and the Middle East is creating new avenues for outsourcing partnerships. As pharmaceutical companies continue to prioritize supply chain efficiency, regulatory compliance, and patient safety, demand for advanced pharmaceutical contract packaging services is expected to increase substantially over the forecast period.

Market Concentration & Characteristics

The industry is relatively mature, particularly in regions such as Europe and North America. The industry is sensitive to macroeconomic conditions, such as GDP growth, healthcare spending, and currency fluctuations. In growing economies, increasing healthcare expenditure and rising pharmaceutical production stimulate demand for contract packaging services. Conversely, economic downturns in some parts of the world pressure pharmaceutical manufacturers to cut costs, potentially delaying new packaging investments. Inflation in raw materials, energy, and labor costs also directly impacts the pricing and profitability of packaging contracts.

Rivalry among existing players is intense, driven by a mix of established global leaders and specialized regional players. Competition is based on capabilities, regulatory compliance, technological innovation, speed, and cost efficiency. The industry is fragmented with differentiated services (primary, secondary, tertiary packaging; serialization; cold-chain packaging), which reduces price wars but increases competition for high-value clients. Consolidation trends, M&A activity, and investment in advanced technologies such as AI-based inspection and serialization platforms further intensify rivalry as players seek to secure long-term contracts and global footprints.

The pharmaceutical contract packaging industry has moderate entry barriers. While initial capital investment for packaging lines and regulatory compliance can be substantial, technological advancements and modular packaging solutions have lowered some barriers. New entrants must navigate stringent FDA, EMA, and local regulatory frameworks, acquire GMP-certified facilities, and build credibility in a highly quality-sensitive industry. However, niche opportunities such as biologics, personalized medicines, and small-batch contract packaging allow smaller specialized players to enter without needing large-scale operations.

Analyst Perspective

The Pharmaceutical Contract Packaging Market’s next phase of growth will be driven less by basic outsourcing demand and more by the industry's ability to provide specialized, compliant, and value-added packaging solutions. Demand is expanding across biologics, injectables, vaccines, clinical trial materials, and specialty pharmaceuticals, but growth in higher-value segments will depend on advanced capabilities such as serialization, cold-chain packaging, regulatory compliance, and supply chain integration. Contract packaging organizations with scalable infrastructure, global regulatory expertise, automation capabilities, and end-to-end service offerings are expected to strengthen their competitive position, while smaller providers may face challenges related to quality assurance requirements, capital-intensive technology investments, and increasing customer expectations for integrated packaging and logistics solutions.

Material Insights

Based on material, the plastic- segment led the market with the largest revenue share of 38.3% in 2025, mainly due to their versatility, cost-effectiveness, durability, ease of manufacturing, and ability to be molded into various shapes and sizes. These materials are ideal for special packaging such as bottles, blister packs, vials, and ampoules, commonly used in the pharmaceutical industry. In addition, plastics and polymers can be easily tailored to specific regulatory requirements for sterility, tamper-proof, and child-resistance, making them popular materials for chemical packaging.

The plastic material segment holds a significant share due to its versatility, durability, and cost-effectiveness compared to alternatives such as glass or metal. Plastics such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), and polyvinyl chloride (PVC) are widely used for blister packs, bottles, vials, caps, and closures. These materials provide excellent barrier properties against moisture, oxygen, and light, ensuring drug stability and extended shelf life. For instance, high-density polyethylene (HDPE) bottles are extensively used for solid oral dosage forms such as tablets and capsules, while PET is preferred for liquid formulations due to its clarity and strength.

The glass segment is forecast to grow at the fastest CAGR over the forecast period. The glass segment in pharmaceutical contract packaging holds a critical role owing to its unmatched barrier properties, chemical inertness, and regulatory compliance advantages. Glass containers such as vials, ampoules, syringes, and bottles are widely used for packaging biologics, injectables, and sensitive formulations where protection from moisture, oxygen, and chemical interaction is paramount. The rise of biologics and biosimilars has particularly boosted the demand for glass-based packaging, as these drugs require high stability and sterility. For example, the growing market for monoclonal antibodies (mAbs) and vaccines has fueled the adoption of sterile glass vials and prefilled syringes among pharmaceutical companies outsourcing packaging operations to contract packagers.

Packaging Type Insights

Based on packaging type, the primary packaging segment led the market with the largest revenue share of 62.0% in 2025, and is forecasted to grow at a the highest CGAR of 6.2% over the coming years. Primary packaging includes blister packs, bottles, vials, ampoules, syringes, and pouches that come into direct contact with medicines. Its dominance is attributed to strict regulatory compliance requiring tamper-evident, contamination-free, and secure packaging that maintains drug stability throughout its shelf life.

Demand for innovative and sustainable solutions in primary pharmaceutical packaging is also increasing as companies focus on patient-centric designs and eco-friendly materials. Contract packagers are adopting advanced technologies such as cold-form foil blister packs, prefilled syringes, and single-dose vials to cater to the rising demand for biologics, injectables, and specialty drugs. For instance, West Pharmaceutical Services has expanded its contract packaging solutions for injectable therapies, reflecting the segment’s evolution beyond conventional packaging to highly specialized formats that support precision medicine and self-administration trends.

The vials sub-segment is forecasted to grow at a significant CAGR over the coming years. Vials are a crucial component of the primary packaging segment, particularly for injectable drugs, vaccines, biologics, and high-value specialty medicines. They are designed to maintain sterility, ensure precise dosing, and protect sensitive formulations from contamination, moisture, and light. Vials are typically made from glass or specialty plastics, and their sizes can range from 1 mL to 50 mL or more depending on the dosage requirements. For example, small-volume glass vials are standard for vaccines, while larger vials are often used for injectable biologics. Their critical role in injectable drug delivery makes vials an indispensable part of pharmaceutical contract packaging operations.

Regional Insights

North America dominated the pharmaceutical contract packaging market with the largest revenue share of 36.5% in 2025. The North America pharmaceutical contract packaging market represents one of the most mature and technologically advanced markets. The region benefits from a highly developed pharmaceutical sector, stringent regulatory frameworks, and strong demand for outsourced packaging solutions from both innovator and generic drug manufacturers. For instance, according to the European Federation of Pharmaceutical Industries Associations (EFPIA), North America accounted for 53.3% of global pharmaceutical sales as of 2024, far outpacing Europe, which held 22.7%. Generic drugs accounted for 84% of total U.S. pharmaceutical sales, supporting the country’s strong position in supplying cost-effective medications globally.

U.S. Pharmaceutical Contract Packaging Market Trends

The pharmaceutical contract packaging market in the U.S. held the largest share in the North America region in 2025. Its dominance is primarily driven by the country’s status as a global pharmaceutical hub, hosting a significant concentration of both innovator and generic drug manufacturers. The U.S. pharmaceutical sector emphasizes stringent regulatory compliance, including FDA guidelines, the Drug Supply Chain Security Act (DSCSA), and Good Manufacturing Practices (GMP), which encourages manufacturers to outsource complex packaging operations to specialized contract packaging providers. This regulatory environment ensures high demand for services such as serialization, tamper-evident packaging, labeling, and combination packaging for complex formulations.

Europe Pharmaceutical Contract Packaging Market Trends

The Europe pharmaceutical contract packaging industry recorded a market share of 25.7% in 2025. Europe is a mature and highly regulated market for pharmaceutical contract packaging, characterized by strong compliance requirements and advanced manufacturing standards. The region has a well-established pharmaceutical industry, with countries such as Germany, Switzerland, France, and the UK hosting a large number of pharmaceutical manufacturers and biotech companies. This concentration of pharmaceutical production drives demand for contract packaging services, including primary, secondary, and tertiary packaging solutions.

The presence of major pharmaceutical giants such as Bayer, Boehringer Ingelheim, and Merck KGaA further fuels the need for advanced and compliant packaging solutions. Contract packaging organizations (CPOs) in Germany are tasked with meeting stringent EU-wide requirements, including serialization, tamper-evident seals, and child-resistant formats under the EU Falsified Medicines Directive (FMD). This strict regulatory environment encourages CPOs to implement state-of-the-art technologies like track-and-trace systems and smart packaging formats, cementing Germany’s role as a hub for compliance-driven packaging innovation.

Asia Pacific Pharmaceutical Contract Packaging Market Trends

The Asia Pacific pharmaceutical contract packaging industry is projected to witness the fastest CAGR during the forecast period, due to its rapidly growing pharmaceutical and biotechnology industries. Countries such as China, India, and Japan have become major hubs for pharmaceutical manufacturing and clinical research, creating a substantial demand for outsourced packaging solutions. For instance, India’s increasing role as a global supplier of generic drugs requires sophisticated packaging for compliance with both domestic and international regulatory standards. Similarly, Japan’s aging population and high demand for specialty pharmaceuticals further fuel the need for efficient contract packaging services that ensure safety, traceability, and compliance with strict regulations.

The pharmaceutical contract packaging industry in China is home to numerous contract manufacturing organizations (CMOs) and pharmaceutical companies that are increasingly outsourcing packaging solutions to specialized providers to meet both domestic and international demand. High-volume production of generic drugs, active pharmaceutical ingredients (APIs), and over-the-counter medications has created significant opportunities for contract packaging players to offer efficient, scalable, and cost-effective solutions. Furthermore, China’s position as the world’s second-largest pharmaceutical market, behind only the U.S., provides a solid foundation for the growth of the pharmaceutical contract packaging segment. The presence of major domestic pharmaceutical companies such as Sinopharm, Jiangsu Hengrui Medicine, CSPC Pharmaceutical, and WuXi AppTec enhances local production capabilities and drives innovation in packaging technologies.

Key Pharmaceutical Contract Packaging Company Insights

Some key players in the pharmaceutical contract packaging market are Amcor plc, BALL CORPORATION, Nipro Corporation, Daito Pharmaceutical Co., Ltd., Pfizer, and others.

Emerging technologies, such as serialization, RFID tagging, track-and-trace solutions, and smart packaging with IoT integration, present significant opportunities for contract packagers to differentiate themselves. Regulatory requirements in markets such as the U.S., EU, and Brazil mandate serialization and traceability to prevent counterfeit drugs. Providers that can integrate these technologies into packaging lines efficiently, while reducing costs and cycle times, gain a competitive edge. For instance, integrating 2D barcodes and tamper-evident seals allows pharmaceutical firms to comply with regulations and maintain supply chain transparency.

-

In August 2025, Amcor plc expanded its healthcare packaging network by opening a new warehouse and distribution facility in San José, Costa Rica. This strategically located center aims to serve medical customers across the Americas, improving supply chain efficiency for products like trays, die-cut lids, forming films, bags, pouches, and labels.

-

In August 2025, SCHOTT Pharma launched the SCHOTT TOPPAC polymer cartridge, the industry's first ready-to-use (RTU) polymer cartridge that complies with ISO dimensions. It offers glass-like functional performance with added break resistance, is compatible with all major fill-and-finish lines and injection devices such as pen systems, and currently comes in 1.5 ml, 3 ml, and 5 ml formats, with a 10 ml version in development.

Key Pharmaceutical Contract Packaging Companies:

The following key companies have been profiled for this study on the pharmaceutical contract packaging market.

-

Amcor plc

-

NIPRO

-

Daito Pharmaceutical Co., Ltd.

-

West Pharmaceutical Services, Inc.

-

CCL Industries Inc.

-

Aphena Pharma Solutions

-

PCI Pharma Services

-

Reed-Lane

-

Wasdell Packaging Group

-

Tjoapack

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Amcor plc, NIPRO, West Pharmaceutical Services, Inc, CCL Industries Inc)

- Mature players focus on offering end-to-end solutions that include primary, secondary, and tertiary packaging, serialization, labeling, artwork management, and regulatory support.

- These players emphasize smart packaging, serialization, and track-and-trace technologies to comply with global regulations.

- Mature players leverage scale, automation, and global networks to manage high-volume contracts for multinational pharma firms.

- Mature players’ geographic presence allows them to serve clients worldwide, ensuring faster market entry and resilience against disruptions

- Advanced automation, compliance, and global infrastructure drive higher fixed costs, making them less cost-competitive in emerging markets compared to local firms.

- Frequent acquisitions can lead to integration challenges, cultural clashes, and inconsistent service quality across acquired entities.

Emerging Players (Aphena Pharma Solutions, Daito Pharmaceutical Co., Ltd., PCI Pharma Services, Reed-Lane, Tjoapack)

- Emerging players focus on tailored solutions and quick turnaround times for small and mid-sized pharmaceutical and biotech companies.

- These players build strong relationships with generic drug manufacturers, nutraceutical brands, and small biotech firms

- Lower overheads and leaner operations often allow them to offer competitive pricing, making them attractive to small and mid-tier pharma companies.

- Emerging players specialize in small-batch, customized packaging with fast turnaround for biotech and generics.

- Emerging players may lack the capital to invest in advanced technologies, serialization systems, or sustainability infrastructure, limiting competitiveness.

- Many smaller players rely heavily on a few clients. Losing one major contract can significantly disrupt their revenue stream.

Pharmaceutical Contract Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 35.7 billion

Estimated market size in 2026

USD 37.6 billion

Projected market size by 2033

USD 55.8 billion

Growth rate

CAGR of 5.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, packaging type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Sweden, Norway, Denmark, China; Japan; India; South Korea; Australia;Thailand, Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Amcor plc; NIPRO; Daito Pharmaceutical Co., Ltd.; West Pharmaceutical Services, Inc.; CCL Industries Inc.; Aphena Pharma Solutions; PCI Pharma Services; Reed-Lane; Wasdell Packaging Group; Tjoapack

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Pharmaceutical Contract Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global pharmaceutical contract packaging market report based on material, packaging type, and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Plastic

-

Paper & Paperboard

-

Glass

-

Aluminum Foil

-

Others

-

-

Packaging Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Primary Packaging

-

Bottles

-

Vials

-

Ampoules

-

Blister Packs

-

Others

-

-

Secondary Packaging

-

Tertiary Packaging

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Sweden

-

Denmark

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Material

Revenue capture definition

Plastic

Revenue generated from contract packaging services utilizing plastic-based packaging materials, including bottles, blister packs, pouches, containers, vials, and closures used for pharmaceutical products.

Paper & Paperboard

Revenue generated from packaging services involving paper and paperboard materials, including cartons, labels, inserts, leaflets, and secondary packaging solutions for pharmaceutical products.

Glass

Revenue generated from packaging services involving glass-based pharmaceutical containers such as vials, ampoules, bottles, cartridges, and prefillable syringes used for drug storage and delivery.

Aluminum Foil

Revenue generated from packaging services utilizing aluminum foil materials in blister packs, sachets, strip packs, wraps, and barrier packaging solutions designed to protect pharmaceutical products from moisture, light, and oxygen.

Segment - Packaging Type

Revenue capture definition

Primary Packaging

Revenue generated from contract packaging services associated with packaging components that directly contain pharmaceutical products, including blister packs, bottles, vials, syringes, ampoules, cartridges, and other immediate-contact packaging formats.

Secondary Packaging

Revenue generated from packaging services involving outer packaging solutions that provide protection, product information, branding, and regulatory labeling, including cartons, boxes, sleeves, labels, and package inserts.

Tertiary Packaging

Revenue generated from packaging services related to bulk handling, warehousing, shipping, and distribution of pharmaceutical products, including corrugated shippers, pallets, shrink wraps, palletization, and logistics packaging solutions.

Estimation Model

Pharmaceutical Products Layer

Packaging Services Layer

Packaging Volume Layer

Revenue Generation Layer

Which pharmaceutical products require contract packaging services?

Which packaging activities are outsourced to contract packaging organizations (CPOs)?

How many pharmaceutical units are contract packaged?

How much revenue is generated?

Analyze global production volumes of prescription drugs, OTC medicines, biologics, biosimilars, vaccines, injectables, clinical trial products, and specialty pharmaceuticals that are outsourced for packaging operations.

Apply outsourcing penetration rates across primary packaging, secondary packaging, tertiary packaging, blister packaging, bottle filling, labeling, serialization, kitting, cold-chain packaging, and clinical trial packaging services.

Estimate packaging demand based on the number of pharmaceutical units outsourced for packaging, including bottles, blister packs, vials, ampoules, prefilled syringes, cartons, and shipping units processed by contract packaging providers annually.

Multiply contract-packaged volumes by average service fees across packaging types, service complexity, regulatory requirements, dosage forms, therapeutic applications, and geographic regions to derive total market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Advanced Pharmaceutical Packaging Technology Trends

Conducted a focused analysis of emerging pharmaceutical packaging technologies, including serialization and track-and-trace systems, smart packaging, tamper-evident solutions, cold-chain packaging, sustainable packaging materials, and automation in packaging operations.

Helps stakeholders identify high-growth technology segments, evaluate innovation trends in pharmaceutical packaging, and assess opportunities arising from regulatory compliance, product security, and supply chain digitization.

Pharmaceutical Outsourcing & Packaging Demand Assessment

Evaluated outsourcing trends across prescription drugs, OTC products, biologics, biosimilars, vaccines, injectables, and specialty pharmaceuticals, including demand for primary, secondary, tertiary, and clinical trial packaging services.

Enables stakeholders to understand demand drivers, identify high-growth therapeutic and packaging segments, and evaluate outsourcing opportunities across pharmaceutical value chains.

Contract Packaging Infrastructure & Market Opportunity Analysis

Assessed contract packaging capacity expansions, automation investments, regulatory requirements, serialization mandates, cold-chain infrastructure development, and regional pharmaceutical manufacturing growth influencing contract packaging demand.

Supports investment and expansion strategies by identifying high-growth regional markets, evaluating regulatory and technological developments, and uncovering opportunities arising from increasing pharmaceutical production and outsourcing activities.

Frequently Asked Questions About This Report

North America dominated the pharmaceutical contract packaging market as of 2025 owing to the quality service offerings by the Contract Packaging Organizations (CPOs) and Contract Development and Manufacturing Organizations (CDMOs) based in the U.S. In addition, most of the pharmaceutical companies outsource their packaging activities to North America to simplify entry into the U.S. markets.

Some of the key companies operating in the pharmaceutical contract packaging market include Amcor plc, BALL CORPORATION, Nipro Corporation, Daito Pharmaceutical Co., Ltd., Pfizer CentreOne, West Pharmaceutical Services, Inc., WestRock Company, Patheon (Thermo Fisher Scientific Inc.), Catalent, Inc., and Baxter BioPharma Solutions.

Key factors that are driving the market growth include increasing stringent quality requirements and outsourcing of pharmaceutical packaging to emerging countries. In addition, pharmaceutical companies are outsourcing packaging activities to service providers to reduce the overall cost of production.

Based on material, plastic dominated the pharmaceutical contract packaging market with a revenue share of 38.3% in 2025.

Based on packaging type, primary packaging dominated the pharmaceutical contract packaging market with a revenue share of 62.0% in 2025.

Glass is expected to grow at the fastest CAGR of 6.5% in the global pharmaceutical contract packaging market over the forecast period.

The global pharmaceutical contract packaging market size was estimated at USD 35.7 billion in 2025 and is expected to reach USD 37.6 billion in 2026 .

The global pharmaceutical contract packaging market is expected to grow at a compound annual growth rate of 5.8% from 2026 to 2033 to reach USD 55.8 billion by 2033.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.