- Home

- »

- Plastics, Polymers & Resins

- »

-

Plastic Films and Sheets Market Size, Industry Report, 2033GVR Report cover

![Plastic Films And Sheets Market Size, Share & Trends Report]()

Plastic Films And Sheets Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (LDPE/LLDPE, PVC, PA, BOPP, HDPE, CPP), By Application (Food, Consumer Goods, Medical, Construction), By Region, And Segment Forecasts

Market Size, 2025

$149.4BMarket Estimate, 2026

$157.7BMarket Forecast, 2033

$237.3BCAGR, 2026–2033

6.0%Plastic Films And Sheets Market Summary

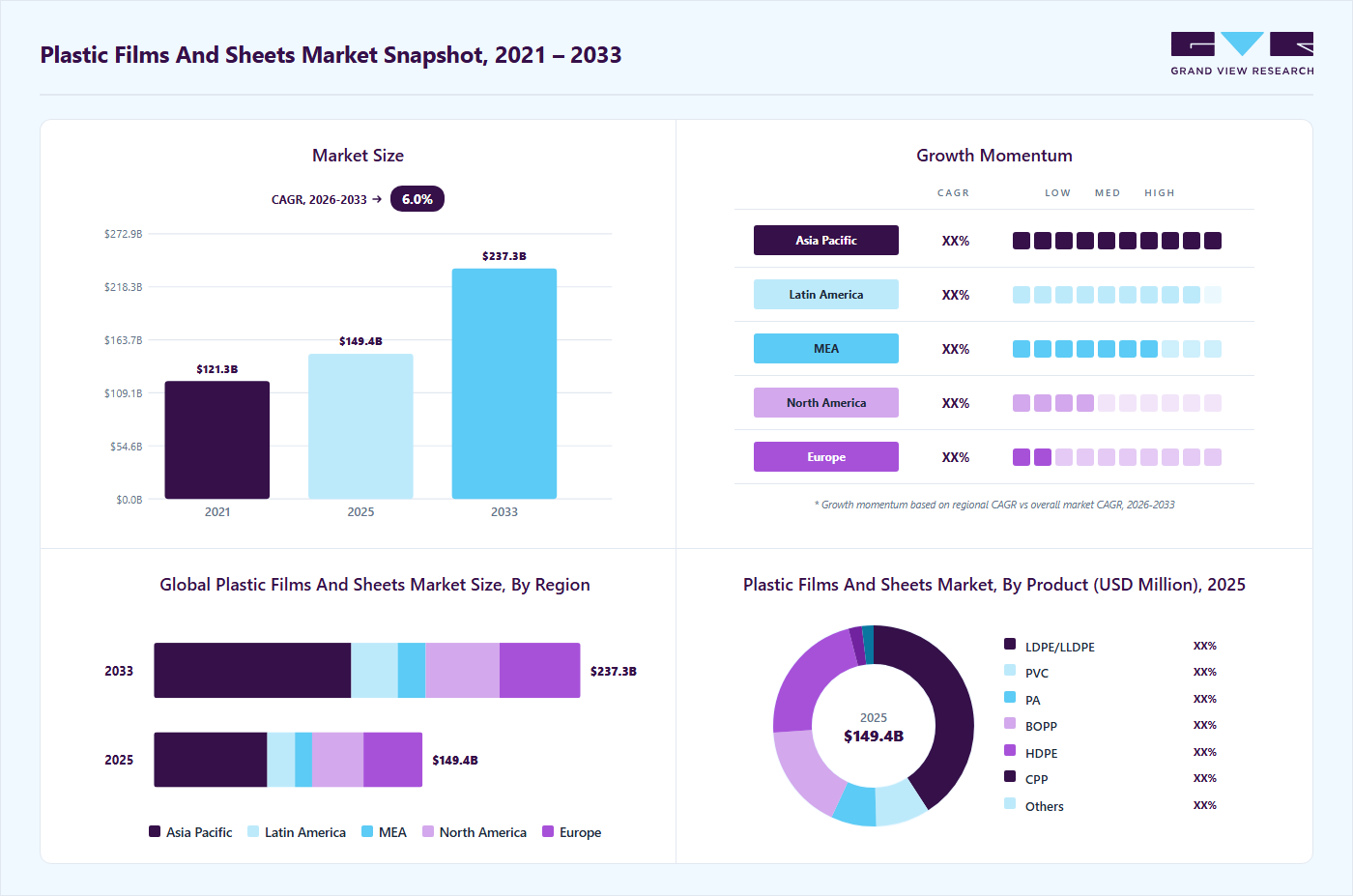

The global plastic films and sheets market size was valued at USD 149.4 billion in 2025 and is projected to grow from USD 157.7 billion in 2026 to USD 237.3 billion by 2033, at a CAGR of 6.0% from 2026 to 2033. The Asia Pacific plastic films and sheets market held the largest share of 42.2% of the global market in 2025. Rising demand for flexible packaging across food, beverages, and personal care products is increasing the consumption of plastic films and sheets.

Key Market Trends & Insights

- By product: LDPE/LLDPE segment led the market and accounting for 40.8% share in 2025.

- By product: BOPP segment is expected to grow at a 7.1% CAGR in revenue from 2026 to 2033.

- By application: Non-packaging segment is expected to grow at a CAGR of 7.3% from 2026 to 2033.

Regional Highlights

- Largest regional market: Asia Pacific (42.2% revenue share, 2025)

- By country: The plastic films and sheets industry in the U.S. is expected to grow at significant CAGR over the forecast period.

Market Size & Forecast

- Market size in 2025: USD 149.4 Billion

- Estimated market size in 2026: USD 157.7 Billion

- Projected market size by 2033: USD 237.3 Billion

- CAGR (2026-2033): 6.0%

These materials offer lightweight protection, product visibility, and extended shelf life, making them a preferred packaging format for manufacturers and retailers. The market is shifting from multi-layer, hard-to-recycle constructions to mono-material and high-barrier films that balance shelf life with recyclability. Manufacturers are standardizing resin blends and introducing compatibilizers to enable large-scale mechanical recycling. This reduces processing complexity and supports closed-loop claims required by major retailers. Investment in extrusion and coating technologies is increasing to deliver barrier performance without the use of mixed polymers.")

Market Dynamics

The plastic films and sheets industry is being driven by increasing demand for lightweight, durable, and cost-efficient packaging materials across food & beverage, healthcare, agriculture, construction, consumer goods, and industrial applications. Plastic films and sheets offer strong barrier properties, flexibility, printability, moisture resistance, and extended shelf-life performance, making them highly suitable for modern packaging and protective applications. Rapid urbanization, changing consumer lifestyles, and rising packaged goods consumption are continuing to strengthen global market demand.

Packaging applications remain the largest growth contributor to the market. Plastic films are extensively utilized in flexible packaging, food wraps, pouches, industrial packaging, shrink films, and protective liners because they improve product safety, logistics efficiency, and shelf-life stability. Growth in e-commerce, convenience food consumption, and organized retail sectors is significantly increasing demand for advanced multilayer and specialty packaging films. Sustainability-focused packaging innovation is also accelerating development of recyclable, downgauged, and bio-based film solutions.

One of the major restraints affecting the plastic films and sheets market is increasing environmental concern regarding plastic waste generation and disposal. Governments and regulatory agencies across multiple regions are implementing stricter regulations related to single-use plastics, recycling mandates, and packaging sustainability requirements. These regulatory pressures are increasing compliance costs and forcing manufacturers to invest heavily in recyclable, biodegradable, and circular packaging technologies.

Market Concentration & Characteristics

The market growth stage is medium, and growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as Toray Industries, Inc., British Polythene Ltd., Toyobo Co., Ltd., Berry Global, Inc., SABIC, and others play a significant role in shaping the market dynamics. These leading players often drive innovation in the market by introducing new products, technologies, and materials to meet the industry's evolving demands.

Innovation in the films market focuses on modular, process-driven improvements that allow for recyclable mono-material constructions and thinner gauges. Equipment manufacturers and converters are implementing integrated MDO cast lines, advanced extrusion controls, and targeted additives to improve barrier and seal performance while using single-resin structures. Suppliers are also testing chemical-recycling-ready formulations and printable high-barrier coatings to expand flexible films into higher-value categories. These developments reduce the need for lamination and support closed-loop goals promoted by industry groups.

Substitution pressure differs by application and is influenced by regulatory requirements and economic performance. In fast-moving consumer goods, fiber-based liners, coated paper, and thin aluminum laminates compete where recyclability claims or shelf appearance are important. In specialized applications, rigid plastics and glass remain preferred when barrier properties or reusability add value. In agriculture, alternatives are assessed based on crop performance and soil impact rather than simply on material origin. Policy measures and procurement rules increasingly determine where films still hold an advantage.

Product Insights

The LDPE/LLDPE segment led the market in product segmentation by revenue, accounting for 40.8% in 2025, and is projected to grow at a 6.2% CAGR from 2026 to 2033. Converters are adopting advanced resin grades that allow for thinner gauges while maintaining mechanical and barrier performance. Suppliers like ExxonMobil and Dow report new metallocene and architecture innovations that support downgauging and higher PCR loading. This reduces the material used per pack and lowers logistics costs for brand owners. Demand for these grades is strongest in areas where automated packaging lines and cost pressures make material efficiency essential.

The BOPP segment is projected to grow at a 7.1% CAGR during the forecast period. Specialty BOPP producers are adjusting product portfolios to meet rising safety and recyclability expectations. Taghleef Industries has announced PFAS-restricted raw material programs and invested in specialty lines for bio-based and re-granulated PP. Brand owners and label converters favor BOPP grades for their reliable sealing, printability, and lower chemical footprint. This preference boosts demand for premium BOPP for food-grade overwraps and high-speed label applications, where regulatory compliance and line uptime are crucial criteria.

Application Insights

The packaging sector dominated with 82.4% of revenue in 2025, and it is expected to grow at a 5.7% CAGR from 2026 to 2033, due to its versatility in both rigid and flexible formats. Major fast-moving consumer goods companies are tightening film specifications to meet recyclability and recycled-content goals. Unilever and Amcor have publicly expanded their R&D and commercial efforts for recycle-ready films and PCR integration. Procurement teams now focus on mono-material constructions and verified supply chains to meet corporate targets and retail requirements. This situation compels converters to co-invest in pilot lines and technical validation to secure long-term packaging contracts.

The non-packaging segment is projected to grow at a 7.3% CAGR over the forecast period. The use of films in agriculture and infrastructure remains growth-positive, as they provide measurable gains in yield, water efficiency, and crop protection. The Food and Agriculture Organization (FAO) emphasizes the productivity and resource efficiency benefits of mulches and greenhouse films, while agencies such as the USDA support the development of biodegradable alternatives. These developments encourage manufacturers to commercialize durable and compostable non-packaging films for precision agriculture and construction membranes.

Regional Insights

The plastic films and sheets industry in the Asia Pacific held the largest revenue share of 42.2% in 2025. The region is expected to grow at a CAGR of 7.3% over the forecast period. This can be attributed to rapid industrialization and expanding consumer markets. Countries such as China, India, and Japan collectively account for a significant portion of global film production and consumption. Rising urban populations and increasing disposable incomes are boosting demand for packaged foods, healthcare products, and consumer goods that depend on flexible film packaging. In addition, government investments in infrastructure and agricultural modernization are driving demand for construction sheets, geomembranes, and agricultural films across the region.

The China plastic films nd sheets industry serves as the manufacturing and consumption hub for plastic films in Asia. The country has a large polymer production base and a widespread flexible packaging industry that supports food processing, electronics, and consumer goods manufacturing. Plastic films are commonly used in food packaging, agricultural mulch films, and protective layers for construction projects. The rapid rise of e-commerce platforms and organized retail is boosting demand for packaging films and courier packaging materials. China also ranks among the largest global consumers of polyethylene films used in packaging and agriculture.

North America Plastic Films And Sheets Market Trends

The plastic films and sheets industry growth in North American is strongly driven by the mature flexible packaging industry and increasing demand for high-performance packaging formats. The Flexible Packaging Association notes that over 60% of flexible packaging materials in the U.S. are plastic films, particularly polyethylene and polypropylene, used for food and consumer goods packaging. Food processors and retail chains are increasingly choosing lightweight films to extend shelf life and improve distribution efficiency. The growth of e-commerce logistics and protective packaging applications is also boosting the use of stretch, shrink, and protective films throughout the region.

U.S. Plastic Films and Sheets Market Trends

The U.S. plastic films and sheets industry is the core demand center in North America, driven by its large packaged food, pharmaceutical, and consumer goods industries. Major food manufacturers and retail chains rely on multilayer barrier films to extend shelf life for meat, dairy, and ready-to-eat products. Flexible packaging has become the dominant format for many food categories, supported by advanced converting and polymer processing capabilities. In addition, the rapid expansion of online grocery and parcel shipping is increasing demand for protective films such as air-bubble films and stretch wraps.

Europe Plastic Films And Sheets Market Trends

The plastic films and sheets industry in Europe is witnessing the influence of regulatory frameworks and circular economy policies on the demand for advanced plastic films and sheets. European Union initiatives aimed at improving packaging recyclability and reducing waste are motivating manufacturers to develop recyclable mono-material films and bio-based options. Consequently, converters are investing in new extrusion technologies and sustainable material solutions. Simultaneously, the region continues to see strong demand from food packaging, construction membranes, and industrial protective films. Europe produces millions of tons of plastic film each year, underscoring the scale of its packaging and industrial sectors.

Key Plastic Films And Sheets Company Insights

The plastic films and sheets industry is highly competitive, with several key players dominating the market. Major companies include Toray Industries, Inc., British Polythene Ltd., Toyobo Co., Ltd., Berry Global, Inc., and SABIC, among others. This industry is marked by intense competition, with leading companies investing heavily in research and development to improve the performance, cost-efficiency, and sustainability of their products.

Key Plastic Films And Sheets Companies:

The following key companies have been profiled for this study on the plastic films and sheets market.

- Toray Industries, Inc.

- British Polythene Ltd.

- Toyobo Co., Ltd.

- Berry Global, Inc.

- SABIC

- Plastic Film Corporation of America

- Sealed Air

- Dow

- DuPont de Nemours, Inc.

- Novolex

- Amcor plc

- UFlex Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Toray Industries, Inc.; Berry Global, Inc.; SABIC

- Broad portfolios of flexible packaging films, industrial sheets, specialty barrier films, and sustainable polymer solutions across food packaging, healthcare, agriculture, and industrial applications.

- Significant investment in recyclable packaging technologies, multilayer film innovation, and lightweight material development.

- Integrated manufacturing infrastructure and global distribution networks supporting large-scale packaging demand.

- Strong polymer processing expertise and advanced film extrusion capabilities.

- Established global manufacturing footprint and diversified end-use penetration.

- Large-scale production capabilities improve operational efficiency and supply reliability.

- High exposure to petrochemical feedstock and energy price volatility.

- Significant sustainability-related investment and environmental compliance requirements.

- Dependence on packaging industry cycles and consumer demand trends affects market stability.

Emerging Players: British Polythene Ltd.; Toyobo Co., Ltd.; Plastic Film Corporation of America

- Focus on customized film solutions, specialty industrial sheets, and region-specific packaging applications.

- Flexible manufacturing strategies supporting niche customer requirements and mid-scale production capabilities.

- Expansion into specialty agricultural films, industrial liners, technical packaging, and performance film applications.

- Greater operational flexibility and responsiveness to customized packaging and industrial film requirements.

- Strong specialization in selected high-value and regional film applications.

- Faster adaptation to evolving customer performance and sustainability requirements.

- Smaller global manufacturing and distribution footprint compared with multinational packaging leaders.

- Limited economies of scale in raw material procurement and production operations.

- Higher dependence on selected regional markets and niche industrial applications.

Recent Developments

-

In April 2025, Borouge announced a strategic expansion program to add polyethylene capacity and lift total polyolefins output above 6.6 million tons per annum by 2028, targeting higher export volumes and increased downstream feedstock availability.

-

In November 2024, ExxonMobil announced more than USD 200 million investment to expand advanced recycling at its Baytown and Beaumont sites, adding about 350 million pounds/year of chemical-recycling capacity and strengthening the supply of recycled feedstock usable in polyethylene production.

Plastic Films And Sheets Market Report Scope

Report Attribute

Details

Market size in 2025

USD 149.4 billion

Estimated market size in 2026

USD 157.7 billion

Projected market size by 2033

USD 237.3 billion

Growth rate

CAGR of 6.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Brazil

Key companies profiled

Toray Industries, Inc.; British Polythene Ltd.; Toyobo Co., Ltd.; Berry Global, Inc.; SABIC; Plastic Film Corporation of America; Sealed Air; Dow; DuPont de Nemours, Inc.; Novolex; Amcor plc; UFlex Ltd.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Plastic Films And Sheets Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global plastic films and sheets market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

LDPE/LLDPE

-

PVC

-

PA

-

BOPP

-

HDPE

-

CPP

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Packaging

-

Food

-

Consumer Goods

-

Medical

-

Others

-

-

Non-Packaging

-

Construction

-

Healthcare

-

Agriculture

-

Others

-

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Delivered comprehensive regional analysis across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. The study evaluated packaging demand trends, food processing growth, industrial manufacturing activity, agricultural film consumption, healthcare packaging requirements, and regional sustainability regulations influencing plastic films and sheets demand patterns.

Supported region-specific expansion and investment planning. Identified high-growth packaging and industrial manufacturing hubs driving film demand. Improved understanding of regional supply-demand dynamics and sustainability-driven market trends. Enabled optimized production, distribution, and commercialization strategies.

Trade Assessment

Conducted trade assessment covering global export-import flows of flexible packaging films, industrial sheets, polyethylene films, polypropylene films, PET sheets, specialty barrier materials, and multilayer packaging systems. The study analyzed regional manufacturing concentration, resin sourcing patterns, tariff structures, logistics networks, recycling regulations, and geopolitical influences affecting international market competitiveness.

Supported procurement optimization and supply chain risk management. Identified strategic sourcing regions and major global trade corridors within the packaging materials value chain. Improved understanding of import dependence, export competitiveness, and raw material supply risks. Enabled proactive planning against trade disruptions, feedstock volatility, and sustainability-related regulatory changes.

Cross-Segmentation

Delivered cross-segment analysis across resin type, film structure, application, end-use industry, processing technology, and regional demand trends. The assessment evaluated interactions between flexible food packaging, healthcare packaging systems, industrial liners, agricultural films, construction materials, recyclable packaging technologies, and specialty barrier film applications.

Improved understanding of high-growth application intersections and premium-value packaging opportunities. Supported product portfolio optimization and targeted commercialization planning. Enabled identification of emerging demand combinations and sustainability-driven innovation opportunities across the plastic films and sheets industry.

Frequently Asked Questions About This Report

The global plastic films and sheets market size was valued at USD 149.4 billion in 2025 and is estimated at USD 157.7 billion for 2026.

The global plastic films and sheets market is expected to grow at a CAGR of 6.0% from 2026 to 2033, reaching USD 237.3 billion by 2033.

The LDPE/LLDPE segment dominated the market across product segmentation in terms of revenue, accounting for 40.8% market share in 2025, and is forecast to grow at a 6.2% CAGR from 2026 to 2033.

Asia Pacific dominated with a 42.2% revenue share in 2025.

Key players include Toray Industries, Inc.; British Polythene Ltd.; Toyobo Co., Ltd.; Berry Global, Inc.; SABIC; Plastic Film Corporation of America; Sealed Air; Dow; DuPont de Nemours, Inc.; Novolex; Amcor plc; UFlex Ltd.

The packaging segment led with a 82.4% revenue share in 2025.

Some key players operating in the plastic films and sheets market include Toray Industries, Inc., British Polythene Ltd., Toyobo Co., Ltd., Berry Global, Inc., SABIC, Plastic Film Corporation of America, Sealed Air, Dow, DuPont de Nemours, Inc., Novolex, Amcor plc, and UFlex Ltd.

Rising demand for flexible packaging across food, beverages, and personal care products is increasing the consumption of plastic films and sheets. These materials offer lightweight protection, product visibility, and extended shelf life, making them a preferred packaging format for manufacturers and retailers.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.