- Home

- »

- Next Generation Technologies

- »

-

Post-Quantum Cryptography Market Size Report, 2026-2033GVR Report cover

![Post-Quantum Cryptography Market (2026 - 2033)Report]()

Post-Quantum Cryptography Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Lattice-Based, Code-Based, Multivariate, Hash-Based), By Solution, By Services (Migration Services, Quantum Risk Assessment), By Enterprise Size, By Vertical, By Region, And Segment Forecasts

Market Size, 2025

$1.6BMarket Estimate, 2026

$2.2BMarket Forecast, 2033

$20.5BCAGR, 2026–2033

37.8%Post-Quantum Cryptography Market Summary

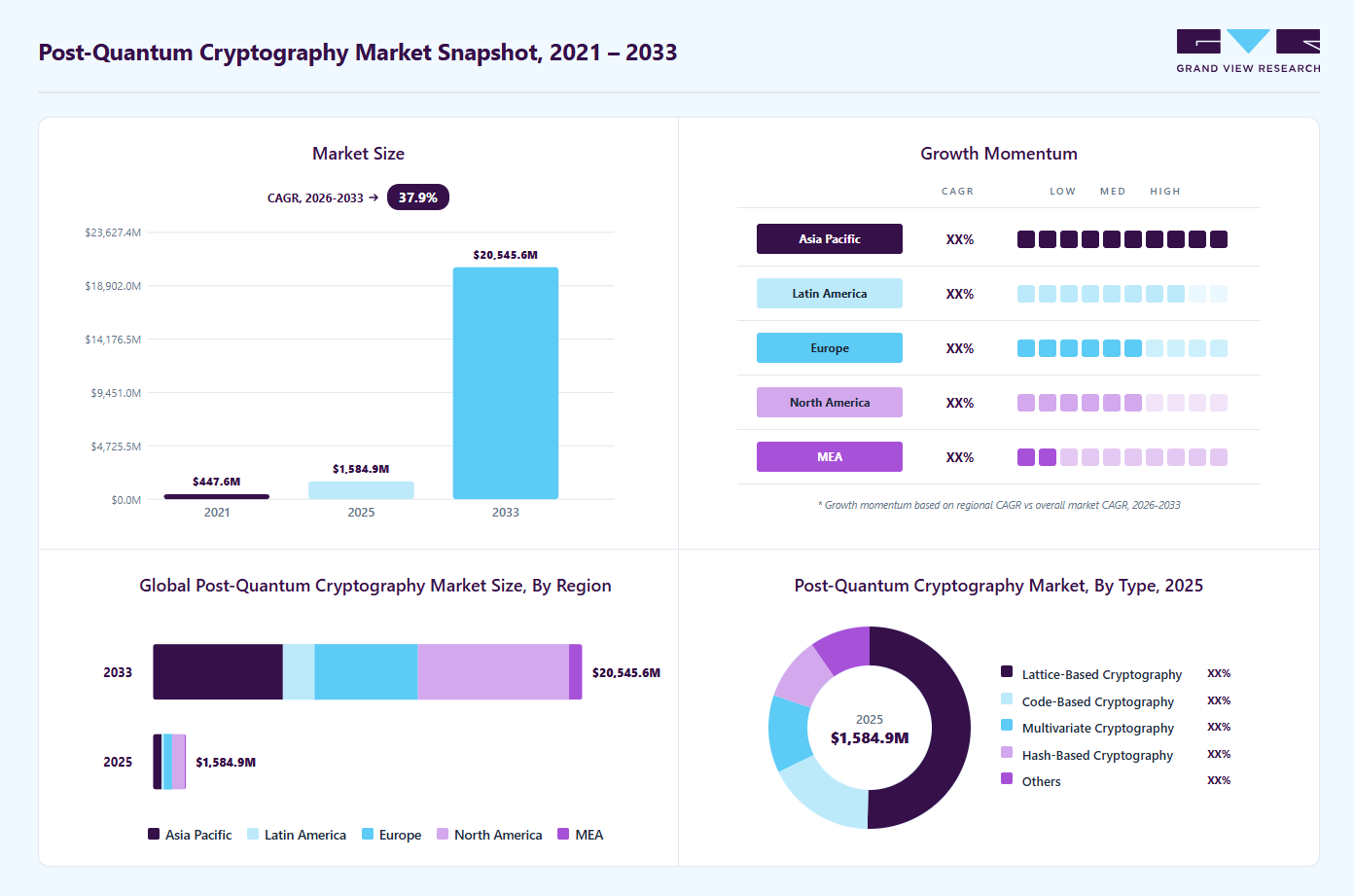

The global Post-Quantum cryptography market size was valued at USD 1.6 billion in 2025 and is projected to grow from USD 2.2 billion in 2026 to USD 20.5 billion by 2033, at a CAGR of 37.8% from 2026 to 2033. The market in North America dominated with a revenue share of 38.0% in 2025. The market is growing rapidly due to increasing concerns about the vulnerability of traditional encryption systems to quantum computing attacks.

Key Market Trends & Insights

- By enterprise size: Large enterprises segment held the largest market share of 72.0% in 2025.

- By services: Design, implementation, and consulting segment held the largest market share of 51.4% in 2025.

- By type: Lattice-based cryptography segment held the largest market share of 50.3% in 2025.

- By solution: Quantum-resistant algorithms segment held the largest market share in 2025.

- By vertical: Government and defense segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (38.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1.6 Billion

- Estimated market size in 2026: USD 2.2 Billion

- Projected market size by 2033: USD 20.5 Billion

- CAGR (2026-2033): 37.8%

Industries such as banking, healthcare, government, defense, and telecommunications are adopting quantum-resistant cybersecurity solutions to protect sensitive data and digital infrastructure. Rising investments in advanced encryption technologies, cloud security, and secure communications are further driving demand for post-quantum cryptography solutions worldwide.The post-quantum cryptography (PQC) market is experiencing strong growth due to increasing demand for quantum-resistant cybersecurity solutions across digital infrastructure and enterprise networks. Organizations are rapidly adopting advanced post-quantum encryption technologies to secure sensitive data, cloud platforms, connected devices, and communication systems against future quantum computing threats. Companies are increasingly launching quantum-safe security platforms, hardware-based cryptographic solutions, and advanced encryption technologies to strengthen protection against emerging quantum cyber risks. For instance, in April 2025, PQShield, a UK-based cybersecurity and post-quantum cryptography (PQC) company, launched the UltraPQ-Suite, introducing PQPlatform-TrustSys, a post-quantum cryptography Root of Trust solution designed for ASIC and FPGA hardware compliance with emerging NIST and NSA CNSA 2.0 standards. The suite includes fast, secure, and compact PQC solutions for networking, automotive, industrial IoT, and critical infrastructure applications.

")

Post-Quantum Cryptography (PQC) is witnessing increasing integration of advanced cybersecurity technologies at the hardware level across connected devices and critical infrastructure systems. Organizations are focusing on strengthening data protection against evolving cyber threats. Demand for secure semiconductor solutions is increasing across industrial and enterprise applications. Connected devices are increasingly incorporating embedded security features to improve system reliability and protection. Companies are developing hardware-based security solutions with integrated encryption and authentication capabilities for next-generation applications. For instance, in October 2025, SEALSQ, a semiconductor and cybersecurity company based in Switzerland, launched the Quantum Shield QS7001, a hardware-embedded post-quantum cryptography chip featuring NIST-standardized PQC algorithms. The chip supports quantum-resistant security for IoT, healthcare, defense, energy, and critical infrastructure applications.

Demand for secure communication solutions and data protection technologies is increasing across multiple industries. Cloud computing providers are focusing on strengthening encryption frameworks and enterprise cybersecurity for digital services and cloud-based workloads. IoT device manufacturers are integrating advanced cybersecurity technologies and post-quantum cryptography solutions to protect connected devices and networks. The automotive industry is planning to improve connected vehicle cybersecurity and protection for autonomous driving systems. Defense organizations are increasing investments in quantum-resistant communication technologies and secure data transmission solutions for critical infrastructure applications. Financial institutions are adopting advanced encryption methods and cybersecurity solutions to secure digital transactions and customer information. Increasing digital transformation, cloud adoption, and expansion of connected infrastructure are supporting demand for next-generation cybersecurity technologies.

Type Insights

The lattice-based cryptography segment led the market in 2025, accounting for over 50.3% of global revenue due to its strong resistance against quantum computing attacks and efficient encryption performance. Adoption is increasing as NIST-standardized algorithms such as CRYSTALS-Kyber and CRYSTALS-Dilithium support secure communication and digital identity verification. Technology is gaining demand across cloud security, financial services, defense systems, and critical infrastructure applications. Its strong quantum resistance is supporting long-term quantum-safe cybersecurity strategies among enterprises and governments. Rising investments in post-quantum cryptography research and quantum-resistant encryption technologies are further supporting market growth.

The hash-based cryptography segment is anticipated to register the highest CAGR during the forecast period due to increasing demand for secure digital signature solutions and quantum-resistant authentication technologies. Solutions such as SPHINCS+ are gaining adoption because they provide long-term security without reliance on complex mathematical assumptions. Their simplicity, strong resistance against quantum attacks, and suitability for low-power environments support adoption across IoT security, embedded systems, and edge computing applications. Growing focus on data integrity protection, secure authentication systems, and lightweight cryptographic solutions is accelerating demand for hash-based post-quantum cryptography technologies globally.

Solution Insights

The quantum-resistant algorithms led the market in 2025 as organizations increasingly adopted quantum-safe cryptography solutions to replace vulnerable classical encryption methods. Growing adoption of standardized post-quantum algorithms, rising cybersecurity concerns, and increasing regulatory focus are supporting deployment across enterprise, government, and critical infrastructure applications. Their ability to protect sensitive data and digital communication against future quantum computing threats is strengthening market demand. Increasing collaboration between governments, cybersecurity companies, and technology providers is further accelerating the adoption of quantum-resistant encryption technologies globally.

The quantum-safe authentication solutions segment is anticipated to register the highest CAGR during the forecast period due to increasing demand for secure identity verification and quantum-resistant authentication technologies. Rising incidents of cyberattacks, identity theft, and data breaches are supporting the adoption of advanced authentication frameworks across financial services, healthcare, enterprise IT, and cloud security applications. Integration of post-quantum cryptography into authentication protocols is improving protection for digital access, user verification, and secure communication systems.

Services Insights

The design, implementation, and consulting segment dominated the market in 2025 due to the complexity of integrating post-quantum cryptography solutions into existing IT and cybersecurity infrastructure. Organizations are increasingly seeking expert consulting, customized deployment strategies, and risk assessment services to support seamless migration and regulatory compliance. Growing demand for tailored cybersecurity solutions across enterprise, government, financial services, and critical infrastructure applications is supporting market growth.

The migration services segment is expected to register significant growth during the forecast period as organizations transition from classical encryption methods to quantum-resistant cryptography solutions. Increasing awareness of quantum computing threats, compatibility challenges, and the need for secure cryptographic upgrades is driving demand for migration and integration services. These services help organizations minimize operational disruption while improving cybersecurity infrastructure and compliance readiness.

Enterprise Size Insights

The large enterprises segment dominated the market in 2025 due to increasing investments in advanced cybersecurity solutions, complex IT infrastructure, and stringent regulatory compliance requirements. Industries such as financial services, healthcare, and telecommunications are increasingly adopting post-quantum cryptography solutions to protect sensitive data, intellectual property, and digital operations from future quantum computing threats. Growing focus on quantum-safe cybersecurity frameworks and secure enterprise communication is further supporting adoption among large organizations.

The small and medium enterprises (SMEs) segment is expected to register the highest CAGR during the forecast period due to increasing awareness of quantum computing risks and rising demand for affordable cybersecurity solutions. Adoption of cloud-based post-quantum cryptography solutions and managed security services is reducing deployment barriers for SMEs. Increasing regulatory focus on data protection and growing demand for secure digital infrastructure are further accelerating the adoption of quantum-resistant cybersecurity technologies across small and medium businesses.

Vertical Insights

The government and defense segment held the largest share of the market in 2025 due to increasing demand for quantum-resistant cybersecurity solutions to protect national security systems and sensitive information. Governments and defense organizations are prioritizing the adoption of post-quantum cryptography technologies to secure communication networks, intelligence systems, and critical infrastructure against future quantum computing threats. Rising government investments, strategic cybersecurity initiatives, and regulatory mandates are accelerating the deployment of quantum-safe encryption technologies across defense and public sector applications.

The IT & ITES segment is expected to register the highest CAGR in the market during the forecast period due to increasing reliance on cloud computing, digital services, and secure data exchange platforms. Rising cyberattacks targeting customer data, enterprise applications, and digital infrastructure are driving demand for quantum-resistant cybersecurity solutions. Adoption of technologies such as 5G, IoT, and edge computing is further increasing the need for post-quantum cryptography solutions to secure connected networks and communication systems. IT service providers are increasingly integrating quantum-safe encryption technologies to support regulatory compliance and strengthen data protection frameworks.

Regional Insights

North America held the largest share of the post-quantum cryptography market in 2025, accounting for over 38.0% of global revenue due to advanced technological infrastructure, strong cybersecurity investments, and early adoption of quantum-resistant cryptography solutions. The presence of major technology companies, cybersecurity providers, and government agencies is accelerating the development and deployment of post-quantum cryptography technologies across enterprise and public sector applications. Increasing regulatory initiatives, including the U.S. National Quantum Initiative, are further supporting the adoption of quantum-safe cybersecurity frameworks to address future quantum computing threats.

U.S. Post-Quantum Cryptography Market Trends

The post-quantum cryptography industry in the U.S. is anticipated to witness significant growth due to increasing focus on national cybersecurity, data privacy, and protection against future quantum computing threats. Rising regulatory mandates and cybersecurity initiatives are driving investments in quantum-resistant cryptography solutions across government and enterprise sectors.

Europe Post-Quantum Cryptography Market Trends

The post-quantum cryptography industry in Europe is expected to grow significantly due to stringent data protection regulations, increasing cybersecurity investments, and rising focus on digital sovereignty. Government initiatives and industry collaborations are accelerating the adoption of quantum-safe cryptographic solutions across enterprise and public sector applications. Growing emphasis on privacy, compliance, and secure digital transformation is further supporting market growth.

Asia Pacific Post-Quantum Cryptography Market Trends

The post-quantum cryptography industry in the Asia Pacific is anticipated to register the highest CAGR during the forecast period due to rapid digital transformation, expanding IT infrastructure, and increasing investments in quantum technology research. Rising cybersecurity awareness, growing cyber threats, and increasing government initiatives are accelerating the adoption of quantum-resistant cryptography solutions across enterprise and public sector applications.

Key Post-Quantum Cryptography Company Insights

Some key companies in the post-quantum cryptography vertical are NXP Semiconductor, Thales, Palo Alto Networks, and IBM Corporation.

-

NXP Semiconductors provides secure connectivity and embedded security solutions with an increasing focus on post-quantum cryptography technologies to protect devices against future quantum computing threats. The company integrates quantum-resistant cryptography capabilities into its secure processing platforms for automotive, industrial, IoT, and communication applications. NXP also collaborates with organizations such as the National Institute of Standards and Technology to support the development of quantum-safe cybersecurity solutions and future-ready encryption technologies.

-

Thales Group provides cybersecurity, digital identity, and quantum-safe encryption solutions with integration of advanced post-quantum cryptography algorithms for secure communication and authentication applications. The company offers crypto-agile security solutions and hybrid cryptography technologies to support protection against emerging quantum computing risks. Thales is also participating in global standardization initiatives and expanding deployment of quantum-resistant cybersecurity technologies across government, enterprise, telecommunications, and secure digital infrastructure applications.

Key Post-Quantum Cryptography Companies:

The following key companies have been profiled for this study on the post-quantum cryptography market.

- Cloudflare, Inc.

- NXP Semiconductor

- Thales

- IDEMIA

- Palo Alto Networks

- DigiCert

- Kloch Technologies, LLC

- PQ Solutions Limited

- PQShield Ltd.

- Entrust Corporation

- IBM Corporation

Recent Developments

-

In March 2026, Bain & Company, Inc. announced a strategic collaboration with IBM Corporation to deliver post-quantum cryptography (PQC) risk assessments and quantum-safe transformation services for private equity and enterprise clients. This partnership focuses on identifying cryptographic vulnerabilities, developing migration strategies, and supporting the adoption of quantum-resistant security solutions to prepare organizations for future quantum computing threats.

-

In February 2026, Cloudflare, Inc. launched its post-quantum cryptography-enabled SASE platform, integrating quantum-safe encryption across its global connectivity cloud. The launch helps organizations protect data and communications against future quantum computing threats and adopt quantum-resistant security standards.

-

In April 2025, PQShield launched PQPlatform-TrustSys, a quantum-safe Root of Trust solution designed to enable ASICs and FPGAs to comply with emerging PQC standards such as the NSA’s CNSA 2.0. Built around a PQC-first architecture, PQPlatform-TrustSys facilitates secure boot, secure update, and lifecycle key management with minimal integration effort, while providing strong key origin and permission tracking to maintain security even if the host system is compromised.

-

In April 2025, NetApp embedded post-quantum cryptography into its storage portfolio for file and block workloads, leveraging NIST-standardized encryption algorithms to protect data against emerging quantum threats. This integration enhances cyber resiliency by securing data at rest and in transit, enabling customers to adopt a proactive security approach at the storage layer.

-

In March 2025, NIST selected the HQC algorithm as a backup post-quantum encryption standard to complement ML-KEM, the primary algorithm for general encryption. HQC is based on error-correcting codes, a different mathematical foundation than ML-KEM’s structured lattices, providing an alternative defense should vulnerabilities be found in ML-KEM. NIST plans to release a draft standard for HQC within a year, with finalization by 2027, ensuring a strong and diversified approach to securing data against future quantum threats.

Post-Quantum Cryptography Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.6 billion

Estimated market size in 2026

USD 2.2 billion

Projected market size by 2033

USD 20.5 billion

Growth rate

CAGR of 37.8% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, solution, services, enterprise size, vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Cloudflare, Inc.; NXP Semiconductor; Thales; IDEMIA; Palo Alto Networks; DigiCert; Kloch Technologies, LLC; PQ Solutions Limited; PQShield Ltd.; Entrust Corporation; IBM Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Post-Quantum Cryptography Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global post-quantum cryptography market based on type, solution, services, enterprise size, vertical, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Lattice-Based Cryptography

-

Code-Based Cryptography

-

Multivariate Cryptography

-

Hash-Based Cryptography

-

Others

-

-

Solution Outlook (Revenue, USD Million, 2021 - 2033)

-

Quantum-Resistant Algorithms

-

Quantum-Safe Cryptographic Libraries

-

Quantum-Safe Authentication Solutions

-

Quantum-Resistant Encryption Solutions

-

Quantum-Safe VPN, Email, Messaging

-

Quantum-Safe Blockchain Solutions

-

Quantum-Safe Hardware

-

-

Services Outlook (Revenue, USD Million, 2021 - 2033)

-

Design, Implementation, and Consulting

-

Migration Services

-

Quantum Risk Assessment

-

-

Enterprise Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Small & Medium Enterprises (SMEs)

-

Large Enterprises

-

-

Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

BFSI

-

Retail & E-commerce

-

Healthcare

-

Government and Defense

-

IT & ITES

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

KSA

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The large enterprises segment led with a 72.0% revenue share in 2025, while small and medium enterprises is the fastest-growing segment.

The design, implementation, and consulting segment held the highest market share of 51.4% in 2025.

The lattice-based cryptography segment accounted for the largest share of 50.3% in 2025, while hash-based cryptography is the fastest-growing segment.

The quantum-resistant algorithms segment accounted for the largest share in 2025, while quantum-safe authentication solutions is the fastest-growing segment.

Some key players operating in the post-quantum cryptography market include NXP Semiconductor, Thales, IDEMIA, Palo Alto Networks, DigiCert, Kloch Technologies, LLC, PQ Solutions Limited, PQShield Ltd, Entrust Corporation, IBM Corporation.

Key factors driving the post-quantum cryptography market's growth include increasing cybersecurity threats from advancing quantum computing, rising demand for quantum-resistant encryption across sectors like government and finance, ongoing government initiatives and standardization efforts, and continuous technological innovations in cryptographic algorithms and quantum key distribution.

The global post-quantum cryptography market size was estimated at USD 1.6 billion in 2025 and is expected to reach USD 2.2 billion in 2026.

The global post-quantum cryptography market is expected to grow at a compound annual growth rate of 37.8% from 2026 to 2033 to reach USD 20.5 billion by 2033.

North America dominated the post-quantum cryptography market with a share of 38.0% in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.