- Home

- »

- Advanced Interior Materials

- »

-

PVDF Membrane Market Size And Share Report, 2026-2033GVR Report cover

![PVDF Membrane Market (2026 - 2033)Report]()

PVDF Membrane Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product Type (Hydrophobic PVDF Membrane, Hydrophilic PVDF Membrane), By End-use (Water & Wastewater Treatment, Industrial Processing, Food & Beverage Processing), By Region, And Segment Forecasts

Market Size, 2025

$886.5MMarket Estimate, 2026

$941.4MMarket Forecast, 2033

$1,434.3MCAGR, 2026–2033

6.2%PVDF Membrane Market Summary

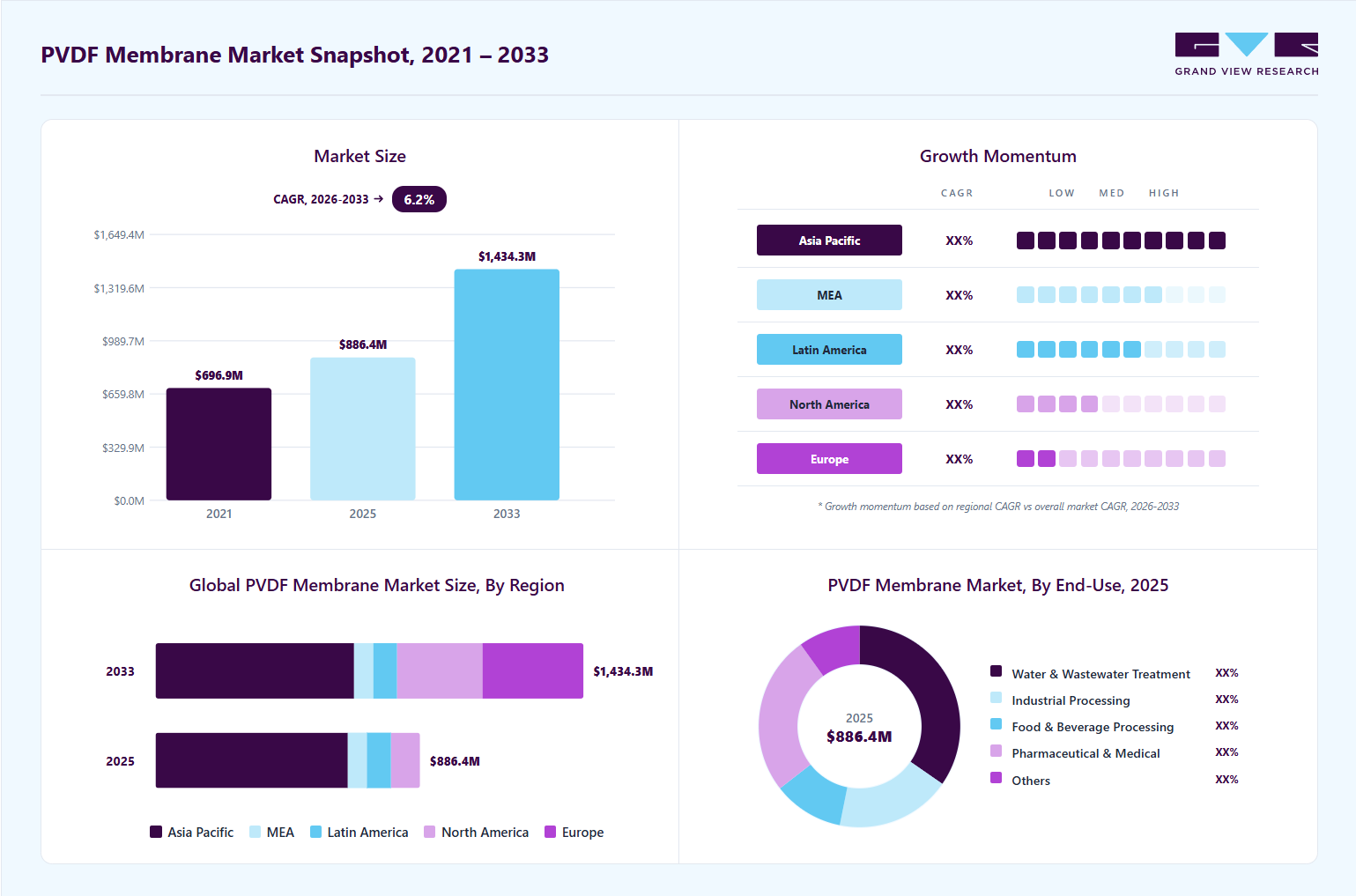

The global PVDF membrane market size was valued at USD 886.5 million in 2025 and is projected to grow from USD 941.4 million in 2026 to USD 1,434.3 million by 2033, at a CAGR of 6.2% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 44.9% in 2025. The demand for PVDF membranes is increasing significantly due to their extensive use in water and wastewater treatment applications across municipal and industrial sectors.

Key Market Trends & Insights

- By product type: Hydrophilic PVDF membrane segment held the largest market share of 55.8% in 2025.

- By end-use: Water & wastewater treatment segment held the largest market share of 34.7% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (44.9% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 886.5 Million

- Estimated market size in 2026: USD 941.4 Million

- Projected market size by 2033: USD 1,434.3 Million

- CAGR (2026-2033): 6.2%

Industries such as pharmaceuticals, biotechnology, food & beverage, and chemicals require highly durable membranes with superior chemical resistance and filtration efficiency. PVDF membranes offer excellent thermal stability, high porosity, and resistance to fouling, making them ideal for ultrafiltration and microfiltration systems. Rapid urbanization and growing concerns about freshwater scarcity are accelerating investments in advanced water purification technologies worldwide. In addition, stricter environmental regulations regarding industrial effluent discharge are compelling industries to adopt high-performance membrane filtration systems.")

Another major factor driving demand is the increasing adoption of PVDF membranes in the biopharmaceutical and healthcare industries. These membranes are widely used for sterile filtration, protein purification, and virus removal due to their low protein-binding characteristics and high chemical compatibility. The expansion of biologics manufacturing, vaccine production, and laboratory research is driving strong demand for reliable membrane technologies. Furthermore, the rapid development of biotechnology facilities in emerging economies is boosting the consumption of high-quality filtration materials. The increasing prevalence of chronic diseases and rising investments in healthcare infrastructure are also indirectly supporting membrane demand. As pharmaceutical manufacturers prioritize contamination-free production environments, PVDF membranes are gaining significant traction.

Technological innovation remains a key trend shaping the PVDF membrane market. Manufacturers are increasingly focusing on developing advanced hydrophilic PVDF membranes with enhanced anti-fouling properties and higher filtration efficiency. Surface modification technologies and nanocomposite membrane structures are being introduced to improve permeability, durability, and chemical resistance. These innovations are helping reduce maintenance costs and extend membrane lifespan in industrial applications. Companies are also investing in energy-efficient membrane systems for desalination and wastewater treatment plants. The integration of smart monitoring systems and automated filtration technologies is further enhancing operational efficiency.

Market Dynamics

One of the primary drivers of the PVDF membrane market is the rapid expansion of wastewater treatment infrastructure worldwide. Governments and private organizations are investing heavily in advanced filtration systems to address growing water pollution and freshwater shortages. PVDF membranes provide superior durability, chlorine resistance, and long operational life compared to conventional filtration materials, making them highly preferred in treatment facilities.

Industrial sectors, including mining, petrochemicals, and textiles, are increasingly adopting membrane bioreactor (MBR) systems utilizing PVDF membranes for efficient wastewater recycling. Rising industrialization in the Asia Pacific and the Middle East is further driving the installation of membrane-based purification technologies. The growing focus on zero-liquid discharge systems also drives higher market demand.

One of the major restraints in the PVDF membrane market is the high production and operational cost associated with PVDF-based filtration systems. PVDF resin is relatively expensive compared to alternative membrane materials such as polysulfone (PSF) and polypropylene (PP), increasing the overall manufacturing cost of membranes. In addition, the fabrication process for PVDF membranes requires advanced technologies, controlled processing conditions, and specialized equipment, which further raises production expenses.

Market Concentration & Characteristics

The PVDF membrane market is moderately consolidated, with several multinational companies dominating global production capacities and technological innovation. Major players compete based on membrane efficiency, durability, product customization, and pricing strategies. Leading manufacturers are heavily investing in research and development activities to introduce advanced anti-fouling and high-flux membrane products. Strategic partnerships, acquisitions, and the expansion of manufacturing facilities are common approaches to strengthening market presence.

Asian manufacturers, particularly those in China and Japan, are increasing production capacity to meet growing regional demand. Despite the presence of established players, emerging companies are entering the market with specialized filtration solutions for niche applications. The competitive environment is expected to intensify as industries increasingly adopt advanced membrane technologies.

The PVDF membrane market faces competition from alternative membrane materials, including polysulfone (PSF), polyethersulfone (PES), polypropylene (PP), and ceramic membranes. These substitutes are often selected based on specific application requirements, operational costs, and chemical compatibility. Ceramic membranes, for instance, provide exceptional thermal and chemical resistance and are increasingly used in highly corrosive industrial environments. However, their high production costs limit widespread adoption in cost-sensitive applications. PES and PSF membranes are also widely utilized in water treatment and biopharmaceutical applications due to their affordability and good filtration performance.

Product Type Insights

The hydrophilic PVDF membrane segment accounted for the highest revenue share of 55.8% in 2025, driven by its extensive use in water treatment, biopharmaceutical filtration, and laboratory applications that require high permeability and efficient liquid separation. Hydrophilic PVDF membranes offer superior wettability, low fouling tendencies, and excellent filtration performance, making them highly suitable for ultrafiltration and microfiltration processes. These membranes are widely utilized in municipal wastewater treatment plants, industrial water recycling systems, and sterile pharmaceutical filtration applications. Increasing global investments in clean water infrastructure and rising demand for high-purity liquid filtration technologies are significantly supporting segment growth.

The hydrophobic PVDF membrane segment is expected to grow at a CAGR of 6.5% over the forecast period, due to increasing demand for gas filtration, air venting, and specialized industrial separation applications. Hydrophobic PVDF membranes possess excellent moisture resistance and high chemical stability, making them ideal for filtration processes involving gases, solvents, and aggressive chemical environments. These membranes are increasingly used in pharmaceutical vent filtration, semiconductor manufacturing, battery applications, and industrial processing systems where liquid repellency and contamination control are critical. Growing investments in biotechnology, electronics manufacturing, and cleanroom operations are creating substantial opportunities for hydrophobic membrane technologies.

End-use Insights

The water & wastewater treatment segment held the highest revenue share of 34.7% in 2025, driven by increasing global demand for advanced filtration technologies to address water scarcity, industrial pollution, and stringent environmental regulations. PVDF membranes are widely used in ultrafiltration, microfiltration, and membrane bioreactor (MBR) systems due to their excellent chemical resistance, durability, and anti-fouling properties. Municipal water treatment facilities and industrial sectors such as chemicals, mining, food & beverage, and power generation are increasingly adopting PVDF membrane systems for efficient wastewater recycling and purification. Rapid urbanization and growing investments in desalination and water reuse infrastructure, particularly in the Asia Pacific and the Middle East, continue to strengthen segment growth.

The pharmaceutical & medical segment is expected to grow at a CAGR of 6.7% over the forecast period, due to rising demand for sterile filtration, biologics manufacturing, and advanced laboratory separation processes. PVDF membranes are widely preferred in pharmaceutical and biotechnology applications due to their low protein-binding properties, high purity, and compatibility with aggressive chemicals and sterilization procedures. Increasing production of vaccines, monoclonal antibodies, and biologic drugs is driving demand for reliable membrane filtration systems used for contamination control and purification. In addition, expansion of healthcare infrastructure and growing investments in biopharmaceutical research are supporting segment growth worldwide. The rising focus on high-quality drug manufacturing standards and stringent regulatory requirements for sterile processing are further expected to accelerate the adoption of PVDF membrane technologies in medical and pharmaceutical applications.

Regional Insights

Asia Pacific dominated the global PVDF membrane market and accounted for the largest revenue share of 44.9% in 2025, due to rapid industrialization, increasing investments in wastewater treatment infrastructure, and strong growth in the pharmaceutical and electronics manufacturing sectors. Countries such as China, Japan, South Korea, and India are witnessing substantial demand for advanced filtration systems across industrial and municipal applications. The region also benefits from expanding lithium-ion battery manufacturing capacity, which supports electric vehicle production. Rising urban populations and growing concerns about water scarcity are prompting governments to invest in desalination and water reuse projects. Additionally, favorable manufacturing costs and the increasing presence of membrane manufacturers contribute to regional market dominance. The strong expansion of the biotechnology and semiconductor industries further strengthens demand for PVDF membrane technologies.

China is one of the fastest-growing markets for PVDF membranes, driven by large-scale investments in water treatment infrastructure and battery manufacturing facilities. The country’s rapidly expanding electric vehicle industry is increasing demand for PVDF materials in lithium-ion battery applications. Industrial wastewater treatment regulations are becoming stricter, encouraging the adoption of advanced membrane filtration systems across the chemical, textile, and electronics industries. Chinese manufacturers are also increasing domestic membrane production capacities to reduce import dependence and improve technological competitiveness. Government initiatives promoting environmental sustainability and clean energy development continue to support market expansion.

North America PVDF Membrane Market Trends

North America is experiencing steady growth in the PVDF membrane market due to increasing adoption of advanced water treatment technologies and strong demand from the pharmaceutical industries. The U.S. and Canada are investing heavily in wastewater recycling systems and in modernizing municipal water infrastructure. The growing emphasis on sustainable industrial operations and stringent environmental regulations are supporting the adoption of membrane filtration. In addition, expansion of biotechnology research and biologics manufacturing facilities is driving demand for sterile filtration membranes. The region also benefits from technological innovation and the strong presence of leading membrane manufacturers. Rising investments in the semiconductor and clean energy sectors are expected to further contribute to market growth.

U.S. PVDF Membrane Market Trends

The PVDF membrane market in the U.S.is driven by strong demand from pharmaceutical, biotechnology, semiconductor, and industrial water treatment sectors. Increasing investments in biologics production and vaccine manufacturing are significantly supporting membrane consumption. Strict environmental standards established by regulatory agencies are encouraging industries to implement advanced wastewater treatment technologies. Additionally, the growing adoption of membrane bioreactor systems in municipal water facilities is driving demand for durable PVDF membranes. The expansion of electric vehicle battery manufacturing and renewable energy storage projects is also contributing to market growth. Ongoing technological advancements in filtration efficiency and membrane durability continue to strengthen the U.S. market position.

Europe PVDF Membrane Market Trends

Europe is witnessing significant growth in the PVDF membrane market, driven by stringent environmental regulations and increased focus on water conservation initiatives. Countries across the region are investing in advanced wastewater treatment systems to achieve sustainability targets and circular economy objectives. The pharmaceutical and food processing industries are major consumers of PVDF membrane technologies for high-purity filtration applications. In addition, Europe’s growing renewable energy and electric vehicle sectors are increasing demand for PVDF-based battery materials. Research institutions and membrane manufacturers in the region are actively developing innovative anti-fouling membrane solutions.

The Germany PVDF membrane market remains a key contributor to the European PVDF membrane market due to its strong industrial manufacturing base and advanced environmental policies. The country has a well-established pharmaceutical, chemical, and automotive industry, driving substantial demand for membrane filtration technologies. Increasing investments in wastewater recycling and industrial process optimization are accelerating the adoption of membranes. Germany’s leadership in electric vehicle manufacturing is also boosting demand for PVDF materials used in lithium-ion batteries. Furthermore, the country emphasizes technological innovation and sustainable manufacturing practices, encouraging the development of advanced filtration solutions. The presence of major industrial equipment manufacturers further supports market expansion.

Central and South America PVDF Membrane Market Trends

Central and South America are gradually emerging as a promising market for PVDF membranes due to increasing investments in municipal water treatment and industrial wastewater management. Countries such as Brazil and Mexico are focusing on improving water infrastructure to address pollution and freshwater availability concerns. Mining, food processing, and chemical industries are increasingly adopting membrane filtration technologies to comply with environmental regulations. Growing urbanization and industrialization are creating additional demand for efficient water purification systems. In addition, healthcare infrastructure development and pharmaceutical manufacturing expansion are supporting membrane usage. Although market penetration remains relatively lower compared to developed regions, long-term growth prospects remain positive.

Middle East & Africa PVDF Membrane Market Trends

The Middle East & Africa region is experiencing rising demand for PVDF membranes primarily due to increasing desalination projects and water reuse initiatives. Countries across the Gulf region are investing heavily in advanced membrane technologies to address severe freshwater scarcity challenges. Industrial sectors, including oil & gas, petrochemicals, and power generation, are adopting PVDF membrane systems for wastewater treatment and process water purification. Government sustainability initiatives and infrastructure modernization programs are supporting market growth across the region. In Africa, urbanization and improving access to clean drinking water are driving investments in water treatment facilities.

Key PVDF Membranes Company Insights

Some of the key players operating in the market include TORAY INDUSTRIES, INC. and Merck KGaA

-

TORAY INDUSTRIES, INC. is a leading manufacturer of advanced membrane filtration technologies, including PVDF membranes used in water treatment, desalination, biotechnology, and industrial separation applications. The company focuses on high-performance filtration systems known for their durability, chemical resistance, and efficient purification capabilities.

-

Merck KGaA provides membrane filtration solutions for biopharmaceutical, laboratory, and life science applications. Its PVDF membrane products are widely utilized in sterile filtration, protein analysis, and pharmaceutical manufacturing processes requiring high purity and low protein-binding characteristics.

GVS S.p.A. and Asahi Kasei Corporation are some of the emerging market participants in the PVDF membrane market.

-

GVS S.p.A. specializes in advanced filtration technologies, including PVDF membrane products for healthcare, laboratory, industrial, and water treatment applications. The company focuses on high-efficiency membrane solutions designed for contamination control and precision filtration processes.

-

Asahi Kasei Corporation is a prominent manufacturer of membrane and separation technologies used in water purification, medical filtration, and industrial processing applications. The company leverages its expertise in advanced materials and chemical engineering to develop durable PVDF membrane solutions with enhanced filtration performance.

Key PVDF Membranes Companies:

The following key companies have been profiled for this study on the PVDF membranes market.

- Merck KGaA

- TORAY INDUSTRIES, INC.

- Pall Corporation

- Solvay S.A.

- 3M

- Asahi Kasei Corporation

- GVS S.p.A.

- Pentair plc

- Mitsubishi Chemical Corporation

- Kovalus Separation Solutions

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Merck KGaA; TORAY INDUSTRIES, INC.; Pall Corporation; Solvay S.A.

- Focus on expanding membrane manufacturing capacities for water treatment, biopharmaceutical, and industrial filtration applications.

- Invest heavily in R&D for advanced anti-fouling, high-flux, and chemically resistant PVDF membrane technologies.

- Strong global brand recognition and extensive distribution networks across industrial and healthcare sectors.

- Advanced technological expertise in membrane engineering, fluoropolymers, and high-purity filtration systems.

- High operational and manufacturing costs due to energy-intensive fluoropolymer production processes.

- Exposure to environmental regulations and raw material price volatility affecting PVDF production economics.

Emerging Players: GVS S.p.A.; Pentair plc; Kovalus Separation Solutions

- Focus on niche applications such as laboratory filtration, industrial wastewater reuse, and decentralized water treatment systems.

- Expand product portfolios through customized membrane solutions and specialized filtration technologies.

- Greater operational flexibility and faster response to evolving customer requirements and niche market demands.

- Strong specialization in targeted filtration segments such as healthcare, industrial water treatment, and contamination control.

- Limited global manufacturing scale and lower financial resources compared to multinational industry leaders.

- Smaller distribution networks and weaker brand visibility in highly competitive international markets.

Recent Developments

-

In November 2025, TORAY INDUSTRIES, INC. opened a new reverse-osmosis membrane manufacturing facility in Dammam, Saudi Arabia, to strengthen its membrane business for desalination, industrial water reuse, and wastewater treatment projects in the Middle East.

-

In September 2025, Merck KGaA inaugurated a EUR 150 million climate-neutral filtration manufacturing facility in Blarney, Ireland, to expand production of tangential flow filtration (TFF) and virus-filtration membrane modules used in biopharmaceutical processing and advanced membrane filtration applications.

PVDF Membrane Report Market Scope

Report Attribute

Details

Market size in 2025

USD 886.5 million

Estimated market size in 2026

USD 941.4 million

Projected market size by 2033

USD 1,434.3 million

Growth rate

CAGR of 6.2% from 2026 to 2033

Base year for estimation

2025

Actual estimates

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product Type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Central and South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; Japan; India

Key companies profiled

Kovalus Separation Solutions; Merck KGaA; TORAY INDUSTRIES, INC.; Pall Corporation; Solvay S.A.; 3M; Asahi Kasei Corporation; GVS S.p.A.; Pentair plc; Mitsubishi Chemical Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global PVDF Membrane Market Report Segmentation

This report forecasts revenue growth at regional & country levels and provides an analysis on the industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global PVDF membrane market report on the basis of product type, end-use, and region:

-

Product Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Hydrophobic PVDF Membrane

-

Hydrophilic PVDF Membrane

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Water & Wastewater Treatment

-

Industrial Processing

-

Food & Beverage Processing

-

Pharmaceutical & Medical

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

-

Central and South America

-

Middle East and Africa

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Demand Analysis

Detailed country-level assessment of PVDF membrane demand across water treatment, pharmaceuticals, biotechnology, electronics, and industrial filtration sectors. Includes analysis of desalination projects, wastewater infrastructure investments, and regional manufacturing trends.

Helps identify high-growth regional markets and prioritize expansion opportunities. Supports regional investment and distribution planning.

Competitive Benchmarking

Benchmarking of major PVDF membrane manufacturers based on membrane technology, production capacity, pricing positioning, R&D investments, product innovation, geographic reach, and recent strategic developments.

Assists in evaluating competitive intensity, identifying market gaps, and developing differentiation strategies.

Opportunity Assessment

Evaluation of emerging growth opportunities across advanced water reuse systems, biopharmaceutical filtration, semiconductor ultrapure water processing, lithium-ion battery applications, and sustainable industrial separation technologies utilizing PVDF membranes.

Identify high-potential application areas and future revenue opportunities. Support investment prioritization, innovation planning, and market entry strategies. Reveal long-term growth drivers associated with clean water infrastructure, healthcare expansion, and energy transition initiatives.

Frequently Asked Questions About This Report

The hydrophilic PVDF membrane segment led with a 55.8% revenue share in 2025.

The water & wastewater treatment segment accounted for the largest share of 34.7% in 2025.

The global PVDF membrane market size was estimated at USD 886.5 million in 2025 and is expected to reach USD 941.4 million in 2026.

The global PVDF membrane market is expected to grow at a compound annual growth rate of 6.2% from 2026 to 2033 to reach USD 1,434.3 million by 2033.

Asia Pacific dominated with a 44.9% revenue share in 2025.

Some key players in the PVDF membrane market include Kovalus Separation Solutions, Merck KGaA, TORAY INDUSTRIES, INC., Pall Corporation, Solvay S.A., 3M, Asahi Kasei Corporation, GVS S.p.A., Mitsubishi Chemical Corporation, and Pentair plc.

Key factors driving the growth of the PVDF membrane market include rising demand for advanced water purification, industrial wastewater treatment, biopharmaceutical filtration, and high-performance separation technologies.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.