- Home

- »

- Next Generation Technologies

- »

-

Smart Glasses Market Size And Share Report, 2026-2033GVR Report cover

![Smart Glasses Market (2026 - 2033)Report]()

Smart Glasses Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Monocular, Binocular, Audio, Immersive), By Operating System, By Glass Tinting Technology, By Application, By Connectivity, By Region, And Segment Forecasts

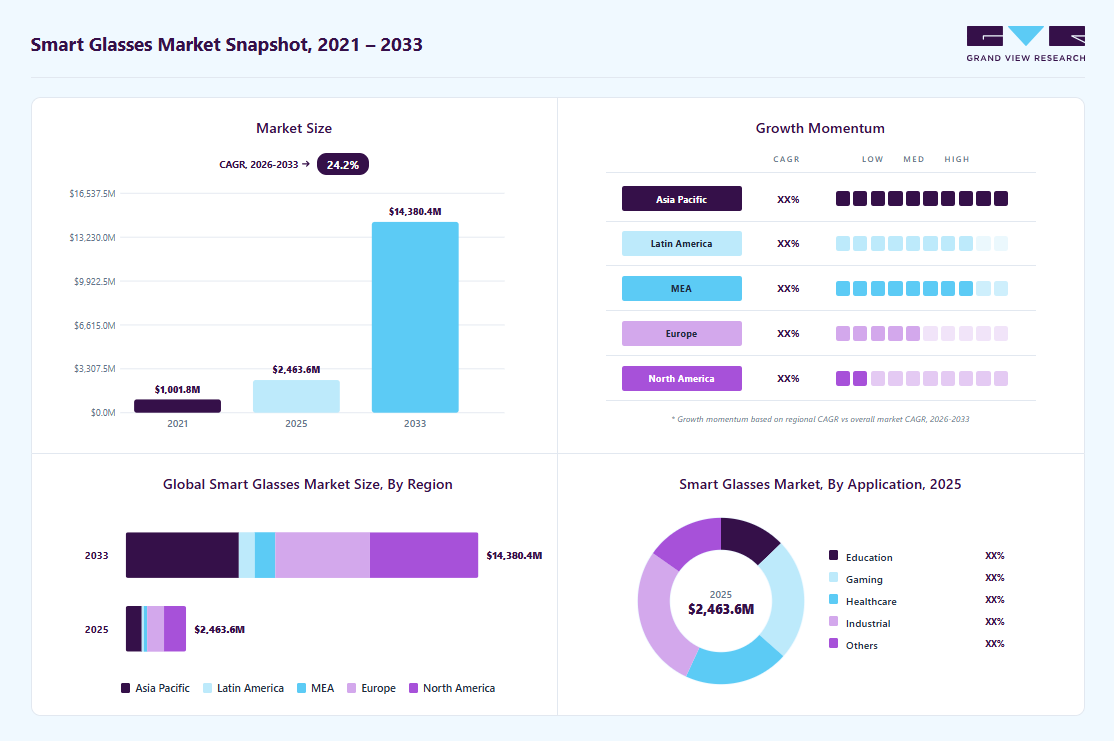

Market Size, 2025

$2.5BMarket Estimate, 2026

$3.2BMarket Forecast, 2033

$14.4BCAGR, 2026–2033

24.2%Smart Glasses Market Summary

The global smart glasses market size was valued at USD 2.5 billion in 2025 and is projected to grow from USD 3.2 billion in 2026 to USD 14.4 billion by 2033, at a CAGR of 24.2% from 2026 to 2033. The market in North America dominated with a revenue share of 34.4% in 2025. The market growth is fueled by growing adoption of augmented reality (AR) and artificial intelligence technologies, increasing demand for hands-free and connected wearable devices, and the expansion of enterprise applications across healthcare, manufacturing, logistics, and field services.

Key Market Trends & Insights

- By operating system: Android segment held the largest market share of 48.0% in 2025.

- By type: Audio segment held the largest market share of 28.0% in 2025.

- By application: Industrial segment held the largest market share of 27.0% in 2025.

- By glass tinting technology: Polymer-dispersed liquid crystals (PDLC) segment held the largest market share in 2025.

- By connectivity: Bluetooth segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (34.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 2.5 Billion

- Estimated market size in 2026: USD 3.2 Billion

- Projected market size by 2033: USD 14.4 Billion

- CAGR (2026-2033): 24.2%

Additionally, the rising demand for immersive experiences, real-time access to information, and seamless connectivity is pushing smart glasses from niche gadgets into mainstream wearable technology, thereby driving the industry's expansion. The continuous advancements in display technologies, miniaturized sensors, low-power processors, and wireless connectivity solutions such as Bluetooth and 5G are enhancing device performance, comfort, and functionality, thereby driving wider commercialization. Growing consumer interest in wearable technology and the integration of voice assistants and AI-powered features are further driving the rapid global expansion of the smart glasses industry. In addition, the rising adoption of smart glasses for fitness tracking, navigation assistance, remote communication, and real-time translation applications is expanding their appeal among both tech-savvy consumers and professional users worldwide.Additionally, the smart glasses industry is further supported by the expanding use of smart glasses across the industrial, healthcare, logistics, and education sectors, where they enable remote assistance, training, workflow optimization, and improved operational efficiency through immersive, interactive digital overlays. Increasing demand for remote collaboration tools and digital transformation initiatives is also accelerating adoption in enterprise environments. The growing integration of augmented reality platforms with enterprise software systems and cloud-based collaboration tools is further improving the functionality and scalability of smart glasses across professional applications.

")

Furthermore, the increasing investments from major technology companies and startups in developing next-generation smart glasses with enhanced AR capabilities, improved battery life, and lightweight ergonomic designs are accelerating innovation and commercialization, thereby strengthening market penetration across both consumer and enterprise segments. Key companies are focusing on strategic collaborations, mergers, and partnerships with software developers, semiconductor manufacturers, and telecom providers to create integrated wearable ecosystems and gain competitive advantages in the smart glasses industry.

Moreover, the growing development of supportive ecosystems, such as AR application platforms, cloud computing infrastructure, and 5G-enabled networks, is enabling seamless, real-time data processing and content delivery, further enhancing the usability and scalability of smart glasses across diverse end-use industries worldwide. The increasing availability of developer tools, software development kits (SDKs), and enterprise AR solutions is encouraging the creation of industry-specific applications tailored to operational efficiency, workforce training, remote collaboration, and customer engagement.

Market Dynamics

The smart glasses market is rapidly maturing from fragmented hardware experimentation into a cohesive ecosystem, where full-stack solutions, operating systems, AI frameworks, developer toolkits, and cloud connectivity enable scalable innovation, seamless interoperability, and accelerated mass-market adoption across consumer and enterprise segments. A central factor impacting the market is the shift from isolated devices to integrated ecosystems supported by major technology platforms across the smart eyewear market and broader wearable computing industry.

Key players such as Meta and Google LLC are developing full-stack ecosystems that include operating systems, AI frameworks, developer toolkits, and cloud connectivity. For instance, in December 2025, Google LLC announced its first AI smart glasses for a 2026 launch, with dual models: screen-free assistance glasses and display-equipped AR variants, strengthening growth across the AR smart glasses market and next-generation wearable platforms. Additionally, partnerships with Samsung, Warby Parker, and Gentle Monster on the Android XR platform are accelerating innovation in the AR and VR smart glasses market.

Additionally, in February 2026, Samsung officially confirmed Android XR smart glasses (SM-O200P/J models) powered by Qualcomm Snapdragon AR1 silicon, featuring 12MP cameras, gesture controls, and Gemini AI integration, completing the triad of Meta AI OS, Google/Samsung Android XR, and Qualcomm silicon that transforms smart glasses from standalone hardware into interconnected platform ecosystems. Such announcements by key players reflect the definitive transition from fragmented hardware competition to unified platform dominance. As a result, device functionality is no longer limited by hardware alone but is expanded through software updates, AI integration, and third-party applications, further supporting the evolution of the smart eyewear technology market.

High production and component costs remain a major constraint on the smart glasses market. These devices depend on advanced hardware, such as micro-OLED displays, waveguides, precision optical modules, depth sensors, cameras, and custom semiconductor chips, which are costly to fabricate and require specialized, high-complexity supply chains, thereby elevating overall manufacturing costs.

Additionally, R&D expenditure further intensifies pricing pressure. Vendors are allocating substantial investment toward miniaturization, on-device AI integration, and the development of AR/VR software ecosystems; these costs are frequently reflected in end-product pricing. As a result, retail prices remain elevated, particularly for high-end models offering spatial computing and AI-enabled functionality within the expanding AR glass market.

Furthermore, cost reduction is constrained by limited economies of scale. Relative to mature consumer categories (such as smartphones), smart glasses remain in an early-stage growth phase with comparatively low production volumes. Low-volume manufacturing inhibits process optimization and purchasing leverage, keeping per-unit costs significantly higher than mainstream consumer electronics.

Industries such as manufacturing, logistics, field services, and maintenance are increasingly using smart glasses to improve operational efficiency and reduce human error. Digital transformation across industrial sectors is increasing the need for wearable computing solutions that support real-time decision-making and workflow automation. For instance, in April 2026, Vuzix expanded its smart glasses deployments in North America after receiving a six-figure follow-on order from AcuraFlow, which supports the continued rollout of its M400 smart glasses across industrial customer operations. Beyond industrial use cases, healthcare providers are increasingly adopting wearable visualization and remote-assistance solutions, contributing to growth in the medical smart glasses market for applications such as surgical navigation, telemedicine, and patient monitoring.

Market Concentration & Characteristics

The smart glasses market is moderately consolidated, with major technology companies, consumer electronics brands, and AR startups driving innovation through ecosystem integration, pricing strategies, and product design. While large companies dominate consumer segments, smaller firms focus on niche enterprise applications such as healthcare, logistics, manufacturing, and defense. Strategic collaborations, product launches, and investments in lightweight designs and improved battery performance are key competitive strategies shaping the market.

Smart glasses face strong product substitutes, such as smartphones, smartwatches, wireless earbuds, and AR/VR headsets, which offer similar communication, entertainment, and wearable computing capabilities. Smartphones remain the strongest product substitute due to their multifunctionality and widespread adoption. However, smart glasses offer advantages such as hands-free operation, real-time access to information, and immersive augmented reality experiences. Overall, the market is characterized by high innovation intensity, moderate M&A activity, limited regulatory impact, and strong enterprise-led adoption, with the industry currently in a high-growth and the accelerating expansion phase.

Type Insights

The audio segment accounted for the largest market share of over 28% in 2025, driven by the increasing demand for hands-free communication and wearable audio devices, owing to the growing consumer preference for seamless connectivity, voice assistant integration, and open-ear listening experiences. The rising popularity of smart audio eyewear for music streaming, calling, navigation assistance, and fitness activities is encouraging manufacturers to introduce lightweight, stylish products with enhanced sound quality and longer battery life. In addition, advancements in noise-reduction technologies, AI-enabled voice controls, and Bluetooth connectivity are further driving the rapid adoption of audio smart glasses among consumers and professionals alike.

The immersive segment is expected to register the fastest CAGR of over 26% from 2026 to 2033, driven by the expanding adoption of augmented reality (AR) and mixed reality technologies and the increasing demand for interactive digital experiences across gaming, entertainment, education, and enterprise applications. Businesses are increasingly utilizing immersive smart glasses for workforce training, remote collaboration, product visualization, and simulation-based learning, thereby improving operational efficiency and user engagement. Furthermore, continuous improvements in display resolution, spatial computing, gesture recognition, and real-time rendering technologies are enhancing immersive experiences and accelerating global segment growth.

Glass Tinting Technology Insights

The polymer-dispersed liquid crystals (PDLC) segment accounted for the largest market share in 2025, fueled by the rising demand for energy-efficient and privacy-enhancing glass technologies, owing to the increasing adoption of smart infrastructure and modern architectural solutions. PDLC smart glass is gaining traction in commercial buildings, healthcare facilities, automotive applications, and the hospitality sector due to its ability to instantly switch between transparent and opaque states, improving energy management and occupant comfort. Additionally, growing investments in smart buildings and sustainable construction projects are further supporting the adoption of PDLC-based smart glass technologies worldwide.

The electrochromic (EC) segment is expected to register the fastest CAGR from 2026 to 2033, owing to the growing focus on energy conservation and sustainable building technologies, and the increasing implementation of green construction standards and energy-efficient infrastructure solutions. Its expanding use in commercial buildings, transportation, luxury automobiles, and aircraft windows is further accelerating market demand. Moreover, advancements in tinting technologies, durability, and automation systems are improving product performance and supporting broader commercialization.

Operating System Insights

The Android segment accounted for the largest market share in 2025, fueled by the widespread adoption of Android operating systems in wearable devices, owing to the platform’s flexibility, extensive application ecosystem, and compatibility with various hardware configurations. Manufacturers are increasingly choosing Android for developing cost-effective smart glasses with customizable interfaces, AI integration, and seamless smartphone connectivity. Additionally, the growing availability of Android-based AR applications, enterprise mobility solutions, and cloud-supported services is further strengthening the adoption of Android-powered smart glasses across consumer and industrial sectors.

The Linux segment is expected to register the fastest CAGR from 2026 to 2033, owing to the increasing demand for open-source and customizable operating systems, and the need for secure, flexible, and scalable software platforms in enterprise and industrial applications. Linux-based smart glasses are widely preferred in sectors such as manufacturing, defense, healthcare, and logistics due to their strong security features, efficient performance, and compatibility with advanced AR and IoT systems. Furthermore, the growing adoption of edge computing, AI-enabled analytics, and enterprise-grade wearable solutions is encouraging organizations to deploy Linux-powered smart glasses for mission-critical operations.

Application Insights

The industrial segment accounted for the largest market share in 2025, owing to the increasing adoption of Industry 4.0 technologies and digital transformation initiatives, and the growing need for real-time data access, remote assistance, and operational efficiency in manufacturing and field operations. Moreover, the integration of AR visualization, AI-powered analytics, and IoT connectivity is further improving industrial productivity and workplace safety, thereby strengthening segment growth.

The healthcare segment is expected to register the fastest CAGR from 2026 to 2033, driven by the increasing adoption of digital healthcare technologies and telemedicine solutions, as the need for real-time patient monitoring, remote consultations, and enhanced clinical workflows grows. Furthermore, advancements in AR-assisted visualization, AI-powered diagnostics, and secure data integration are improving medical accuracy and operational efficiency, thereby supporting the rapid expansion of smart glasses in the healthcare industry.

Connectivity Insights

The Bluetooth segment accounted for the largest market share in 2025, driven by the rising demand for wireless wearable connectivity solutions, owing to the increasing use of smartphones, wireless audio streaming, and IoT-enabled devices. Continuous advancements in Bluetooth Low Energy (BLE), faster pairing capabilities, and improved audio synchronization are further enhancing device efficiency and user convenience, thereby accelerating segment growth among consumers and enterprise users.

The USB segment is expected to register the fastest CAGR from 2026 to 2033, driven by the growing need for reliable wired connectivity and fast data transfer capabilities, as well as the increasing use of smart glasses in industrial, healthcare, and enterprise environments. Additionally, the growing adoption of smart glasses for professional applications that require stable connectivity, such as diagnostics, industrial inspections, and AR-assisted workflows, is further driving the adoption of USB-enabled solutions globally.

Regional Insights

North America dominated the smart glasses market with a share of over 34.4% in 2025, driven by the strong presence of leading technology companies and rapid adoption of advanced wearable technologies, owing to increasing investments in augmented reality (AR), artificial intelligence (AI), and enterprise digital transformation initiatives. The region is witnessing high demand for smart glasses across healthcare, manufacturing, defense, and logistics sectors for applications such as remote collaboration, workflow optimization, and real-time data visualization.

U.S. Smart Glasses Market Trends

The U.S. smart glasses industry dominated the North American market with a share of over 88% in 2025, fueled by the increasing investments in AR and mixed reality technologies by major technology companies, owing to the rising demand for next-generation wearable computing solutions across consumer and enterprise sectors. The country has a strong ecosystem of software developers, semiconductor manufacturers, and AI-driven technology providers that support rapid product innovation and commercialization.

Europe Smart Glasses Market Trends

The Europe smart glasses industry is expected to grow at a CAGR of over 23% from 2026 to 2033, owing to the region’s strong emphasis on advanced technology adoption and operational efficiency. European enterprises are increasingly deploying smart glasses for workforce training, maintenance support, logistics management, and healthcare applications. Additionally, supportive government initiatives promoting Industry 4.0 technologies, growing investments in AR development, and rising demand for energy-efficient wearable devices are further contributing to the expansion of the smart glasses market across Europe.

The Germany smart glasses industry is expected to grow significantly in the coming years, driven by strong industrial digitization initiatives and the country’s leadership in Industry 4.0 adoption. Manufacturing, automotive, and engineering companies are increasingly deploying smart glasses to support hands-free assembly guidance, remote expert assistance, quality inspection, and workforce training. Government-backed programs promoting industrial automation in R&D and enterprise AR solutions are further strengthening market expansion across both industrial and healthcare sectors.

The UK smart glasses industry is witnessing rapid expansion, supported by the rapid adoption of digital healthcare and enterprise collaboration technologies, and the increasing demand for remote communication, virtual assistance, and immersive training solutions. Moreover, growing investments in AI-powered wearable technologies, expanding startup ecosystems, and rising interest in smart consumer electronics are further supporting the growth of the smart glasses market in the UK.

Asia Pacific Smart Glasses Market Trends

The Asia Pacific smart glasses industry is expected to grow at the fastest CAGR of 27% from 2026 to 2033, driven by rapid technological advancements and expanding consumer electronics adoption, and the increasing urbanization, rising disposable incomes, and growing investments in digital infrastructure across emerging economies. Countries in the region are witnessing an increasing deployment of smart glasses across the industrial manufacturing, healthcare, education, and retail sectors to support digital transformation and operational efficiency.

The China smart glasses industry is being accelerated by the country’s strong electronics manufacturing ecosystem and the rapid adoption of AI and AR technologies, driven by significant government support for digital innovation and smart technology development. Chinese companies are increasingly investing in smart wearable devices for consumer entertainment, industrial automation, healthcare, and education applications, thereby driving the market growth.

The Japan smart glasses industry is expanding steadily, driven by the growing adoption of advanced robotics, automation, and wearable technologies, as well as the country’s strong focus on technological innovation and smart industrial solutions. Japanese enterprises are utilizing smart glasses for remote maintenance, workforce training, precision manufacturing, and healthcare support applications to improve operational efficiency and address labor shortages.

Key Smart Glasses Company Insights

Some of the key players operating in the market include Microsoft Corporation, Amazon.com,Inc, and Google LLC, among others.

-

Microsoft Corporation designs and develops mixed-reality and enterprise smart glasses solutions under its HoloLens product line. Its portfolio includes AR head-mounted displays, spatial mapping software, cloud integration via Azure, AI-based computer vision, and industrial remote-assistance platforms. The company serves industries such as manufacturing, healthcare, defense, aerospace, construction, education, energy, and logistics, supporting use cases including training, equipment maintenance, surgical visualization, and digital twin implementation.

-

Google LLC develops smart glasses and augmented reality platforms focused on enterprise productivity and industrial applications. Its product offerings include Google Glass Enterprise Edition, AR software development kits, computer vision tools, voice control systems, and cloud-based data services. The company serves sectors such as logistics, healthcare, manufacturing, field services, warehousing, and utilities, enabling hands-free workflows, real-time information access, remote collaboration, and operational efficiency.

Lumus Ltd. and Vuzix Corporation are some of the emerging market participants in the smart glasses market.

-

Lumus Ltd. designs and develops optical waveguide display engines and augmented-reality visualization components for smart glasses manufacturers. Its product portfolio includes transparent waveguide optics, high-brightness display modules, micro-projectors, and AR system reference designs. The company primarily serves smart glasses OEMs, defense contractors, industrial solution providers, and automotive HUD developers, enabling lightweight, high-resolution, energy-efficient AR displays.

-

Vuzix Corporation designs and manufactures smart glasses and wearable display technologies focused on enterprise and industrial markets. Its offerings include monocular and binocular AR smart glasses, waveguide-based optics, voice-controlled interfaces, enterprise device management software, and ruggedized wearable systems. The company serves logistics, manufacturing, healthcare, warehousing, field services, and defense sectors, supporting applications such as remote assistance, order picking, inspection, and telemedicine.

Key Smart Glasses Companies:

The following key companies have been profiled for this study on the smart glasses market.

-

Amazon.com, Inc.

-

Vuzix Corporation

-

Bose Corporation

-

Flows Bandwidth

-

Google LLC

-

Lenovo

-

Lumus Ltd.

-

Magic Leap, Inc.

-

Microsoft Corporation

-

Razer Inc.

Recent Developments

-

In March 2026, Vuzix Corporation expanded deployment of Vuzix smart glasses across North America through follow-on orders of M400 devices and new Ultralite Pro OEM smart glasses for additional workflows. This expansion demonstrates increasing large-scale enterprise adoption of smart glasses across logistics, warehousing, and robotics applications.

-

In January 2026, Lumus Ltd. expanded its waveguide optics commercialization through partnerships with global OEM manufacturers, enabling integration into next-generation AR smart glasses platforms.

-

In December 2025, Google LLC announced a collaboration with Warby Parker to develop AI-powered smart glasses using Android XR and Gemini AI, targeting lightweight, all-day wearable devices with advanced multimodal capabilities. This partnership strengthens Google’s push toward consumer-ready AI smart glasses with integrated design and ecosystem scalability.

Competitive benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Google LLC, Amazon.com, Inc., Vuzix Corporation, Microsoft Corporation

- Focus on developing integrated smart glasses ecosystems combining AR hardware, AI software, and cloud services.

- Emphasize AI-driven capabilities such as voice assistants, real-time analytics, and spatial computing.

- Strong global brand presence, advanced R&D investments, and established ecosystems integrating hardware, software, and cloud services.

- Benefit from scalable infrastructure, extensive developer ecosystems, and cross-device integration capabilities.

.

- Face challenges such as high device costs, limited battery performance, and slower innovation cycles.

- They encounter difficulties in driving mass consumer adoption, balancing privacy concerns, and differentiating products in a competitive market with specialized AR startups and niche technology providers.

Emerging Players: Lumus Ltd., Razer, Inc., Lenovo

- Focus on specialized smart glasses solutions, including enterprise AR devices, optical components, and XR platforms, targeting niche applications.

- Emphasize innovation in core technologies such as waveguide optics, spatial computing, and low-latency streaming.

- Ability to rapidly innovate in areas like optics, immersive AR hardware, and XR streaming platforms.

- Strong focus on emerging use cases such as enterprise AR, gaming wearables, and data visualization.

- Lower brand visibility and financial resources compared to established competitors.

- Dependence on partnerships for scaling production, distribution, and ecosystem integration

Smart Glasses Market Report Scope

Report Attribute Details

Market size in 2025

USD 2.5 billion

Estimated market size in 2026

USD 3.2 billion

Projected market size by 2033

USD 14.4 billion

Growth rate

CAGR of 24.2% from 2026 to 2033

Base year of estimation

2025

Actual data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in Thousand Units, Revenue in USD Million/ Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, glass tinting technology, operating system, application, connectivity, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Amazon. Com, Inc.; Vuzix Corporation; Bose Corporation; Flows Bandwidth; Google LLC; Lenovo; Lumus Ltd.; Magic Leap, Inc.; Microsoft Corporation; Razer Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Smart Glasses Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global smart glasses market report based on type, glass tinting technology, operating system, application, connectivity, and region.

-

Type Outlook (Volume, Thousand Units; Revenue, USD Million; 2021 - 2033)

-

Monocular

-

Binocular

-

Audio

-

Immersive

-

Others

-

-

Glass Tinting Technology Outlook (Volume, Thousand Units; Revenue, USD Million; 2021 - 2033)

-

Polymer-Dispersed Liquid Crystals

-

Electrochromic (EC) Smart Glass

-

Photochromic

-

Suspended Particles Device (SPD)

-

Others

-

-

Operating System Outlook (Volume, Thousand Units; Revenue, USD Million; 2021 - 2033)

-

Android

-

Linux

-

Others

-

-

Application Outlook (Volume, Thousand Units; Revenue, USD Million; 2021 - 2033)

-

Education

-

Gaming

-

Healthcare

-

Industrial

-

Others

-

-

Connectivity Outlook (Volume, Thousand Units; Revenue, USD Million; 2021 - 2033)

-

Bluetooth

-

HDMI

-

USB

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Market Entry & Expansion Assessment

Regional demand sizing and forecasting

Customer segmentation and buying behavior analysis

Competitive landscape benchmarking

Regulatory and distribution channel assessment

Identified high-growth market opportunities

Supported go-to-market strategy development

Highlighted investment priorities and risks

Enabled data-driven expansion planning

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline and patent review

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

North America dominated with a 34.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Android segment led with a 48.0% revenue share in 2025, while Linux is the fastest-growing operating system.

The industrial segment held the largest share (over 27.0%) in 2025, while healthcare is the fastest-growing application.

The Bluetooth segment held the largest revenue share in 2025, while USB is the fastest-growing connectivity.

The global smart glasses market size was valued at USD 2.5 billion in 2025 and is estimated at USD 3.2 billion for 2026.

The global smart glasses market is expected to grow at a CAGR of 24.2% from 2026 to 2033, reaching USD 14.4 billion by 2033.

The audio segment accounted for the largest market share of over 28.0% in 2025. The demand for hands-free audio experiences drives segmental growth. Audio-enabled smart glasses have gained popularity among consumers seeking a seamless blend of entertainment and utility, as these glasses allow users to listen to music, receive calls, and interact with virtual assistants without needing additional accessories. Advancements in bone conduction and open-ear audio technologies strengthen this segment’s leadership by delivering improved sound quality, thereby securing its position as a key driver of sustained market growth.

Key players include Amazon.Com, Inc.; Vuzix Corporation; Bose Corporation; Flows Bandwidth; Google LLC; Lenovo; Lumus Ltd.; Magic Leap, Inc.; Microsoft Corporation; Razer Inc.

The smart glasses market is growing, driven by the convergence of technological advancements and rising consumer demand for wearables. Technological advancements in miniaturized displays, AI-powered computer vision, sensor integration, and edge computing are significantly enhancing user experience and accelerating the growth of the smart glasses industry.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.