- Home

- »

- Power Generation & Storage

- »

-

Solid State Battery Market Size & Share Report, 2026- 2033GVR Report cover

![Solid State Battery Market Size, Share & Trends Report]()

Solid State Battery Market (2026 - 2033) Size, Share & Trends Analysis Report By Battery Type (Thin Film Battery, Portable Battery), By Capacity, By Application (Consumer & Portable Electronics, Electric Vehicles), By Region, And Segment Forecasts

Market Size, 2025

$1.6BMarket Estimate, 2026

$2.3BMarket Forecast, 2033

$15.7BCAGR, 2026–2033

31.8%Solid State Battery Market Summary

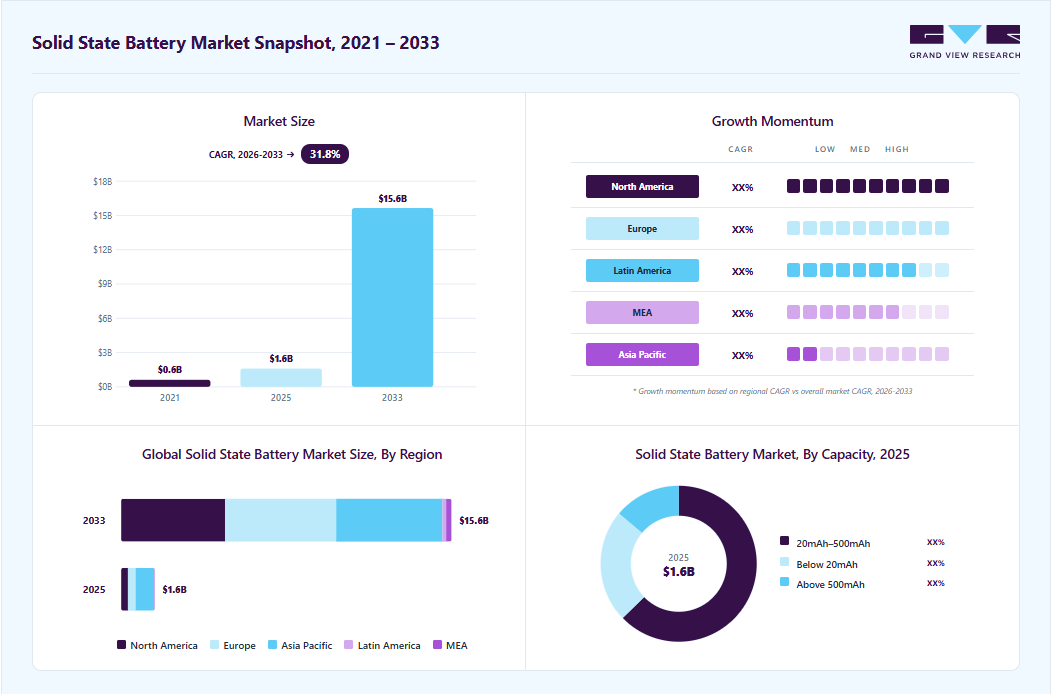

The global solid state battery market size was valued at USD 1.6 billion in 2025 and is projected to grow from USD 2.3 billion in 2026 to USD 15.7 billion by 2033, at a CAGR of 31.8% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 54.0% in 2025. The market is expected to witness steady growth over the next several years due to the increasing integration of renewable energy systems, rising demand for high-efficiency power architectures, and the shift toward decentralized and digitalized power distribution.

Key Market Trends & Insights

- By battery type: Thin film batteries held the largest market share of over 89.0% in 2025.

- By application: Consumer & portable electronics segment represents the largest application area for the market.

- By capacity: 20mAh-500mAh segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (54.0% revenue share, 2025)

- Fastest-growing regional market: North America (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.6 billion

- Estimated market size in 2026: USD 2.3 billion

- Projected market size by 2033: USD 15.7 billion

- CAGR (2026-2033): 31.8%

Deployment is being accelerated by the growing penetration of consumer & portable electronics, EV charging infrastructure, and industrial automation systems, along with advancements in power electronics, solid-state circuit breakers, and DC-optimized grid components.

Sustainability is emerging as a key catalyst for the growth of next-generation energy storage globally, with governments and corporations prioritizing decarbonization, achieving net-zero targets, and implementing large-scale renewable energy deployment. Regions such as North America, Europe, and the Asia Pacific are integrating advanced storage systems to stabilize solar and wind output, improve grid resilience, and reduce reliance on fossil fuels. Advanced battery solutions are emerging as attractive long-term options due to enhanced safety, recyclability potential, and extended operational lifespan, which help lower lifecycle emissions and electronic waste. The global transition toward circular energy planning, including policies that support low-carbon industries, electric mobility, and sustainable smart-city infrastructures, positions next-generation battery technologies as the backbone for environmentally responsible power storage worldwide.

")

Technology adoption is advancing rapidly through strategic collaborations between energy infrastructure providers, automotive OEMs, and battery innovators. Breakthrough formats such as solid-state polymer batteries, solid-state lithium metal batteries, and thin-film solid-state batteries are gaining traction due to their compact design, improved safety, and higher energy performance compared to conventional lithium-ion chemistries. Global industrial stakeholders are evaluating modular storage units and micro-battery systems for applications in electric vehicles, aerospace, defense electronics, consumer electronics, and industrial automation. Early-stage manufacturing pilot lines, testbeds, and R&D centers are helping companies build supply chain readiness and workforce capabilities, laying the foundation for large-scale commercialization over the next decade.

Drivers, Opportunities & Restraints

The global market is primarily driven by the increasing demand for high-density, safe, and long-life energy storage across electric mobility, consumer electronics, and renewable integration projects. Advanced formats, including solid-state car batteries, solid-state polymer batteries, and thin-film batteries, are receiving attention for their superior energy density, longer cycle life, and enhanced thermal stability compared to conventional lithium-ion solutions. Notable developments in 2025 include the successful validation of next-generation solid-electrolyte materials by multiple battery developers, which has strengthened confidence in scaling these technologies for commercial applications worldwide.

Substantial growth opportunities exist as regions pursue technology localization, the adoption of large-scale renewable energy, and smart infrastructure programs. Smaller, high-performance formats, such as solid-state micro batteries and solid-state chip batteries, are ideal for aerospace, defense, sensors, IoT devices, and wearable electronics. Larger-capacity cells based on solid-state lithium metal batteries are being explored for grid stabilization, renewable energy integration, and electric transportation systems. In 2025, several global collaborations and feasibility studies between battery developers and energy corporations signalled strong potential for manufacturing partnerships, supply chain development, and localized production expansion.

Despite strong growth potential, global adoption faces hurdles due to high production costs, technical complexity, and limited large-scale manufacturing infrastructure. Challenges include ensuring stable electrode-electrolyte interfaces, preventing dendrite formation, achieving high production yields, and sourcing high-purity materials. The absence of fully matured supply chains in some regions increases reliance on imports and slows deployment. Even with technological breakthroughs in 2025, demonstrating improved electrolyte stability and scalable cell designs, affordability and large-volume availability remain primary constraints delaying widespread adoption.

Battery Type Insights

The thin film battery segment holds the dominant share within the battery type segmentation, driven by its compact design, lightweight structure, and ability to deliver stable power in ultra-miniaturized electronics. Its suitability for smart cards, RFID tags, medical patches, IoT sensors, and compact consumer devices has positioned it as the preferred choice for next-generation microelectronics. Demand continues to rise as industries move toward smaller, safer, and long-life power sources that can be integrated into flexible and ultra-thin form factors. Increasing investment in medical wearables, wireless monitoring systems, and skin-adhesive diagnostics has played a crucial role in strengthening the market position of thin-film chemistries, further supported by advancements in solid electrolyte interfaces and higher energy-density deposition techniques.

The portable battery segment has contributed noticeable revenue, but it trails behind thin-film systems due to its more conventional size and use cases. Portable cells remain relevant in mid-power applications, such as smart consumer electronics, industrial handheld devices, and emerging mobility solutions, where higher capacity is required compared to ultra-thin batteries. However, adoption is more gradual, influenced by higher manufacturing costs and the need to refine electrolyte integration for reliable scalability. Despite this, ongoing improvements in energy density, safety, and charging efficiency are expected to help the portable category expand over the next decade - particularly as consumer electronics and wearables continue to evolve toward enhanced performance and all-day operation.

Capacity Insights

The 20 mAh - 500 mAh capacity segment dominates the market, supported by its broad applicability across wearables, smart consumer electronics, industrial sensors, medical monitoring devices, GPS trackers, and next-generation portable equipment. These batteries offer an ideal balance of compact size, stable energy density, long operational life, and enhanced safety, making them suitable for devices that require continuous yet moderate power delivery. The rise of connected health devices, AR/VR accessories, digital authentication tools, and high-performance smartwatches has significantly strengthened demand for this capacity range. Manufacturers are increasingly integrating advanced electrolyte materials and thin-film architectures to achieve faster charging, improved thermal tolerance, and greater lifespan-driving this segment’s sustained leadership.

The below 20 mAh capacity segment is poised to exhibit the fastest CAGR over the forecast period, primarily due to its demand in ultra-miniaturized medical patches, RFID, micro-sensors, and smart cards, as the segment continues to benefit from IoT miniaturization trends. Meanwhile, cells with capacities above 500 mAh are being evaluated for high-power consumer electronics, industrial handheld systems, and early mobility platforms, with progress dependent on overcoming manufacturing scale and cost barriers. As material innovations reduce internal resistance and improve electrode-electrolyte interfaces, both non-dominant segments are expected to grow at a healthy pace-especially as demand expands for longer battery runtime across industrial IoT, smart consumer devices, and compact mobility applications.

Application Insights

The consumer & portable electronics segment represents the largest application area for the market, driven by the global proliferation of smartphones, tablets, laptops, gaming consoles, smart home devices, and handheld gadgets. Demand for compact, high-performance energy storage solutions has surged as OEMs increasingly prioritize longer runtimes, fast-charging capability, and safety across consumer electronics. Miniaturization trends and the transition toward sleeker, lightweight form factors are further accelerating adoption in this category, with manufacturers integrating next-generation battery technologies to elevate device efficiency and overall user experience. The segment continues to benefit from rising digitalization, expanding consumer purchasing power, and rapid product innovation cycles from electronics brands.

Beyond consumer applications, batteries are gaining traction in electric vehicles, energy harvesting, wearable devices, medical devices, and other industrial and commercial uses. The electric vehicle category is witnessing steady momentum due to OEM electrification roadmaps and global sustainability commitments, while energy-harvesting systems are emerging as an attractive space for powering low-maintenance IoT sensors and industrial automation devices. Wearable and medical electronics, including smartwatches, fitness trackers, hearing aids, and portable medical tools, are also developing into high-growth pockets as the focus on remote health monitoring increases worldwide. Although these segments currently trail consumer electronics in market share, technology upgrades, cost reductions, and ecosystem expansion are expected to broaden their contribution over the forecast period.

Regional Insights

The North American solid state battery industry is expanding rapidly, driven by strong investments in electric vehicles (EVs), consumer electronics, and energy storage solutions. The region accounted for roughly one-third of global demand in 2024, with government incentives and private R&D funding helping to accelerate commercialization timelines. A recent milestone in 2025 was when Factorial Energy, in collaboration with Stellantis, validated automotive-sized solid-state battery cells with an energy density of around 375 Wh/kg, marking one of the closest steps yet toward real-world EV integration.

U.S. Solid State Battery Market Trends

The U.S. solid state battery industry dominates the North America market due to its advanced innovation ecosystem and high concentration of startups and OEM partnerships. Companies such as QuantumScape and Factorial Energy are driving commercialization by scaling pilot production and refining electrolyte technologies for EV and stationary storage applications. The latest update in 2025 indicated that manufacturers in the U.S. began shipping advanced nano-sulfide solid electrolytes globally, highlighting the nation’s transition from laboratory-scale innovation to early-stage commercial manufacturing.

Asia Pacific Solid State Battery Market Trends

The solid state battery industry in the Asia Pacific captured the largest market share of over 54.0% in 2025, driven by the expansion of EV manufacturing, booming demand for consumer electronics, and large-scale investments in renewable energy storage. The region accounted for more than half of the global market share in 2024, with Japan, South Korea, and China spearheading advancements in sulfide, oxide, and polymer electrolyte chemistries. In 2025, the Asia Pacific experienced a surge in pilot-line upgrades for EV-grade solid-state cells, indicating that large-scale production for automotive applications is nearing reality across multiple countries.

Europe Solid State Battery Market Trends

The solid state battery industry in Europe is steadily strengthening its position in the ecosystem through a combination of automotive alliances, sustainability regulations, and cross-border energy transition policies. The region is preparing for mass deployment of next-generation EV batteries, supported by automakers that are integrating solid-state technology into future vehicle platforms. A key development occurred in 2025 when Volkswagen’s battery unit, PowerCo, advanced its partnership with QuantumScape to lay the groundwork for large-scale solid-state cell production in Europe, thereby accelerating the region’s roadmap for next-generation EV adoption.

Latin America Solid State Battery Market Trends

The solid state battery industry in Latin America currently represents a smaller share of the global market; however, momentum is building as EV adoption increases and governments seek to integrate energy storage into renewable power grids. The region accounted for roughly 3% of global demand in 2024, with long-term growth expected as lithium-rich countries explore upstream and downstream investments. The most recent market update for 2025 projected that Latin America would record the highest growth rate among emerging regions, as early-stage development projects for both energy storage and EV applications began to materialize.

Middle East & Africa Solid State Battery Market Trends

The solid state battery industry in the Middle East & Africa is still in an early stage, but it is gaining traction as countries accelerate clean mobility initiatives and expand renewable energy storage infrastructure. Adoption is being driven largely by government programs promoting EV penetration, smart city development, and solar-plus-storage installations, particularly in the UAE, Saudi Arabia, and South Africa. In the latest industry development in 2025, several regional energy and infrastructure players initiated feasibility studies with global battery manufacturers to assess the deployment of solid-state batteries in large-scale grid storage and next-generation electric fleet projects, indicating that commercial pilot activity could begin before the decade ends.

Key Solid State Battery Company Insights

Some of the key players operating in the global market include QuantumScape Corporation and Solid Power, among others.

-

QuantumScape Corporation is one of the most influential participants in the global landscape, specializing in lithium-metal cell technology designed to significantly enhance driving range, fast-charging performance, and safety across electric mobility platforms. The company’s proprietary solid ceramic separator eliminates the need for graphite anodes, enabling higher energy density and longer lifecycle stability under extreme operating conditions. QuantumScape continues to collaborate with leading automotive OEMs to accelerate commercial deployment, supported by ongoing pilot-line expansion and multilayer cell testing to meet scalability requirements for next-generation electric vehicles and high-performance energy storage systems.

-

Solid Power plays a pivotal role in shaping the commercial phase of the solid-state battery industry, manufacturing sulfide-based electrolyte materials and high-energy battery cells engineered for automotive and industrial electrification. The company’s scalable roll-to-roll development framework and electrolyte production model enable competitive cost efficiencies while maintaining enhanced thermal tolerance and extended operational lifetimes. Solid Power partners with major automotive groups for qualification testing and vehicle-oriented validation, supporting the transition to safer, higher-capacity battery technologies for electric mobility, aerospace platforms, and large-format renewable energy storage systems.

-

Toyota Motor Corporation remains one of the most strategically invested organizations in the global solid-state battery landscape, leveraging its automotive manufacturing scale to accelerate the commercialization of next-generation energy storage for mass-market electric vehicles. The company focuses on solid-electrolyte battery technologies that deliver ultra-fast charging, long-distance driving capability, and superior temperature resistance while preserving long-term safety and durability. Toyota’s multi-phase deployment roadmap involves collaboration with material suppliers, battery developers, and automotive partners, aiming to introduce solid-state battery-powered vehicles within its broader electrification strategy for passenger cars, hybrid systems, and next-generation mobility fleets.

Key Solid State Battery Companies:

The following are the leading companies in the solid state battery market. These companies collectively hold the largest Market share and dictate industry trends.

- BrightVolt Solid-State Batteries

- Hitachi Zosen Corporation

- Ilika Ltd.

- Ion Storage Systems

- Panasonic Energy Co., Ltd.

- QuantumScape Corporation

- Samsung SDI Co., Ltd.

- Solid Power

- STMicroelectronics

- Toyota Motor Corporation

Recent Developments

-

In November 2025, QuantumScape announced the successful validation of its next-generation 24-layer prototype cell through third-party automotive testing, demonstrating consistent fast-charging capability from 10% to 80% in under 15 minutes while maintaining high energy retention across extended cycle simulations. This milestone strengthens commercial readiness for solid-electrolyte lithium-metal battery deployment in electric mobility platforms and supports ongoing qualification trials with leading global OEMs.

-

In October 2025, Solid Power expanded its sulfide-based electrolyte production line, increasing output capacity to support multiple automakers conducting B-sample cell testing for upcoming EV platforms. The company also began scaling roll-to-roll cathode-anode assembly processes to improve manufacturability and reduce cost barriers associated with commercial-grade solid-state battery adoption.

-

In September 2025, Toyota confirmed progress toward mass-production feasibility by completing in-vehicle testing of its solid-electrolyte battery pack designed for long-range performance models, achieving a projected driving range of more than 1,000 km per charge under controlled test conditions. The company outlined plans to integrate its next-generation energy storage roadmap into mid-to-late-decade EV launches, supported by strategic co-development programs with materials and electrolyte suppliers.

Solid State Battery Market Report Scope

Report Attribute

Details

Market Definition

The solid-state battery market size represents the total annual revenue generated from the production, sale, and commercialization of solid-state batteries and related technologies across automotive, consumer electronics, aerospace, and energy storage applications.

Market size in 2025

USD 1.6 billion

Estimated market size in 2026

USD 2.3 billion

Projected market size by 2033

USD 15.7 billion

Growth rate

CAGR of 31.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Battery type, capacity, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; Spain; France; Italy; Russia; China; India; Japan; South Korea; Australia; Brazil; Colombia; Paraguay; Saudi Arabia; UAE; South Africa; Egypt

Key companies profiled

BrightVolt Solid-State Batteries; Hitachi Zosen Corporation; Ilika Ltd.; Ion Storage Systems; Panasonic Energy Co., Ltd.; QuantumScape Corporation; Samsung SDI Co., Ltd.; Solid Power; STMicroelectronics; Toyota Motor Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Solid State Battery Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global solid state battery market report on the basis of battery type, capacity, application, and region:

-

Battery Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Thin Film Battery

-

Portable Battery

-

-

Capacity Outlook (Revenue, USD Million, 2021 - 2033)

-

Below 20mAh

-

20mAh-500mAh

-

Above 500mAh

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer & Portable Electronics

-

Electric Vehicles

-

Energy Harvesting

-

Wearable & Medical Devices

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Russia

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Colombia

-

Paraguay

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

Egypt

-

-

Frequently Asked Questions About This Report

Key factors include increasing demand for high-density, safe, and long-life energy storage across electric mobility, consumer electronics, and renewable integration projects

The global solid state battery market size was estimated at USD 1.6 billion in 2025 and is expected to reach USD 2.3 billion in 2026.

The global solid state battery market is expected to grow at a compound annual growth rate of 31.8% from 2026 to 2033 to reach USD 15.7 billion by 2033.

The thin film batteries held the highest market share of over 89.0% in 2025.

SSome of the key players operating in the global solid state battery market include BrightVolt Solid-State Batteries; Hitachi Zosen Corporation; Ilika Ltd.; Ion Storage Systems; Panasonic Energy Co., Ltd.; QuantumScape Corporation; Samsung SDI Co., Ltd.; Solid Power; STMicroelectronics; Toyota Motor Corporation, and others.

Asia Pacific dominated with a revenue share of 54.0% in 2025

North America is the fastest-growing region over the forecast period.

The 20 mAh - 500 mAh capacity segment dominates the market, while below 20 mAh capacity is the fastest-growing segment.

The consumer & portable electronics segment held the highest market share in 2025.

About the Author(s)

Power Generation & Storage Research Team

Energy & Power · Power Generation & StorageThis report was authored by the power generation & storage research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the power generation & storage segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.