- Home

- »

- Medical Devices

- »

-

Structural Heart Procedures Market Size Report, 2026-2033GVR Report cover

![Structural Heart Procedures Market (2026 - 2033)Report]()

Structural Heart Procedures Market (2026 - 2033)

Size, Share & Trends Analysis Report By Procedure (TAVR, SAVR, LAAC, Mitral Repair (Annuloplasty), Septal Defect Closure), By Indication, By End-use, By Region, And Segment Forecasts

Market Size, 2025

$16.7BMarket Estimate, 2026

$18.3BMarket Forecast, 2033

$36.4BCAGR, 2026–2033

10.3%Structural Heart Procedures Market Summary

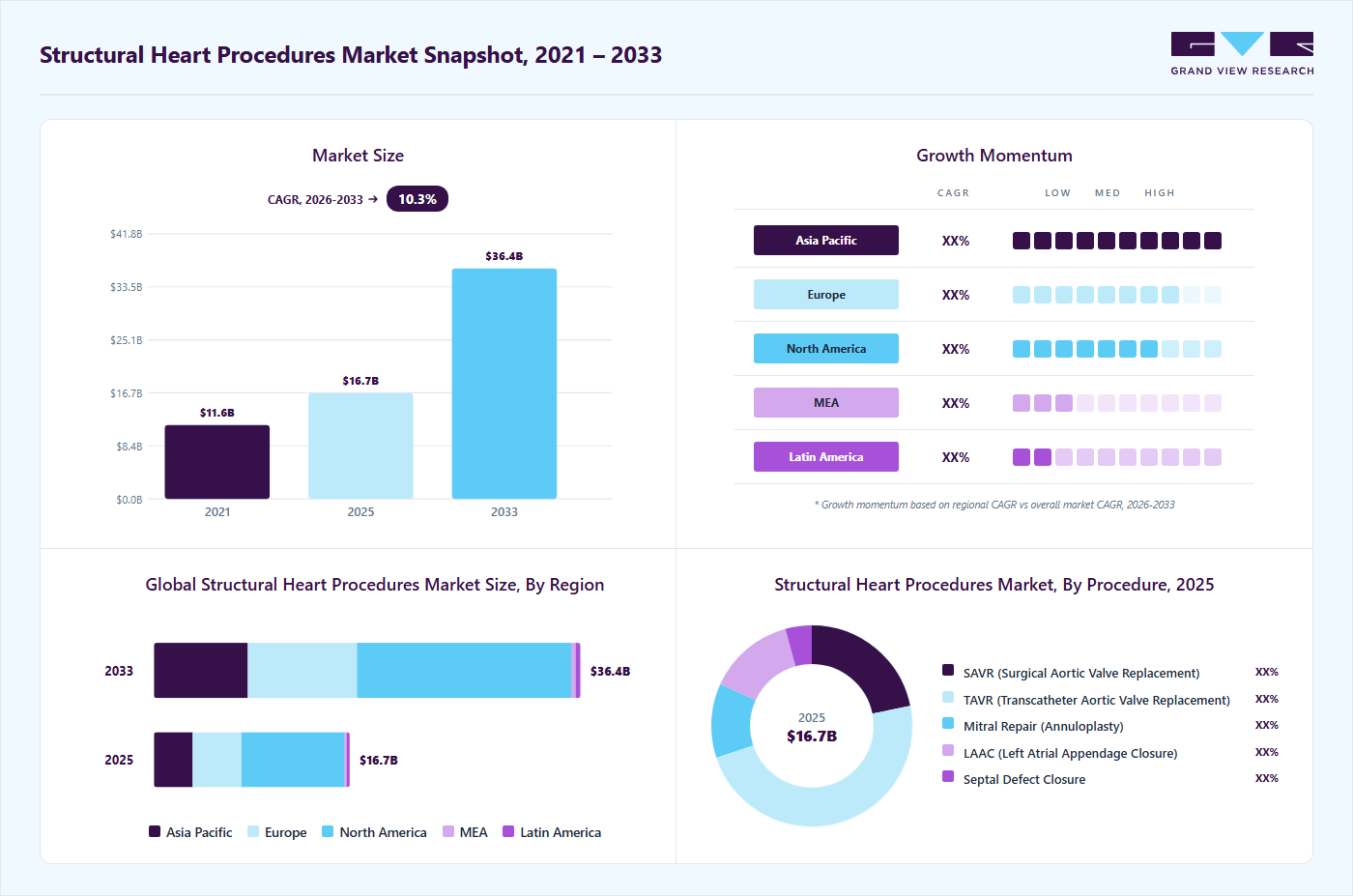

The global structural heart procedures market size was valued at USD 16.7 billion in 2025 and is projected to grow from USD 18.3 billion in 2026 to USD 36.4 billion by 2033, at a CAGR of 10.3% from 2026 to 2033. The market in North America dominated with a revenue share of 52.5% in 2025. Key factors driving this market are the rising global prevalence of structural heart diseases and cardiovascular diseases, and the increasing demand for minimally invasive surgeries.

Key Market Trends & Insights

- By procedure: AVR (trans catheter aortic valve replacement) segment held the largest market share of 48.0% in 2025.

- By indication: Aortic stenosis segment held the largest market share of 46.6% in 2025.

- By end use: Hospitals segment segment held the largest market share of 67.4% in 2025.

Regional Highlights

- Largest regional market: North America (52.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 16.7 Billion

- Estimated market size in 2026: USD 18.3 Billion

- Projected market size by 2033: USD 36.4 Billion

- CAGR (2026-2033): 10.3%

According to an Oxford Academic article published in January 2025, the global age-standardized prevalence of cardiovascular disease stands at approximately 7,179 cases per 100,000 individuals, highlighting the substantial and persistent global burden of heart-related conditions.")

The section below outlines key market drivers such as increased awareness about structural heart diseases,rising prevalence of cardiovascular diseases. It reflects technological advancements, a shift towards rising adoption of minimally invasive interventions, and technological advancements driving precision and safety in structural heart procedures.

Market Drivers

Increasing Awareness about Structural Heart Disease

The increasing awareness about structural heart diseases is playing a key role in improving early diagnosis and treatment of conditions such as valve disorders, cardiomyopathy, and congenital heart abnormalities. Increased awareness among patients and healthcare providers is encouraging regular cardiac checkups and the use of diagnostic tools such as electrocardiograms (ECGs) and echocardiography to detect abnormalities in heart structure and function. In November 2025, according to a study presented at the American Heart Association’s Scientific Sessions, an AI-based algorithm combined with smartwatch ECG sensors can help detect structural heart diseases, including weakened heart muscle, damaged valves, and thickened cardiac tissue. Such innovations are increasing public and clinical awareness of structural heart diseases and leading to earlier diagnosis and intervention.

Shift toward minimally invasive and trans catheter procedures

The structural heart procedures market is increasingly driven by the adoption of minimally invasive interventions, which provide safer alternatives to traditional open-heart surgery. Trans catheter procedures, including Trans catheter Aortic Valve Replacement (TAVR) and Trans catheter Mitral Valve Repair (TMVR), have become an essential component of structural heart interventions. By allowing valve replacement or repair without open-heart surgery, these procedures significantly lower complication rates and improve survival, contributing to their rapid adoption across hospitals and cardiac centers globally. For instance, according to an NIH article published in March 2025, 98,504 TAVR procedures were performed in the U.S. in 2022, up sharply from 4,666 in 2012, highlighting the exponential growth and increasing acceptance of this minimally invasive therapy.

Rising Prevalence of Cardiovascular Diseases

The increasing prevalence of CVDs is a key driver of the structural heart devices market due to the growing aging population. Factors such as sedentary lifestyles, poor diets, and demographic aging contribute to the growing frequency of heart-related ailments, fueling demand for advanced medical devices to manage these conditions. For instance, a 2024 report by the World Heart Federation noted a rise in global CVD mortality from 12.1 million in 1990 to 20.5 million in 2021. CVD accounts for the majority of global deaths, with low- and middle-income countries bearing 80% of the burden.

Market opportunity analysis

Integration of Artificial Intelligence (AI)

Artificial intelligence (AI) presents a key opportunity in the structural heart procedures market by improving diagnostic accuracy, procedural planning, and patient selection. Structural interventions such as TAVR, mitral valve repair, and left atrial appendage closure require detailed evaluation of cardiac anatomy, which can be efficiently analyzed using AI-enabled imaging tools. AI can assist clinicians in automated analysis of CT scans and echocardiography, enabling accurate valve sizing, identification of anatomical variations, and optimized procedural strategies. In addition, AI-based predictive analytics can support risk stratification and treatment decision-making, helping physicians determine the most appropriate intervention while reducing procedural complications and improving clinical outcomes.

Growing Demand for Personalized & Patient-Specific Devices

The growing demand for personalized and patient-specific structural heart devices represents another major opportunity in the market. Structural heart conditions often vary significantly based on patient anatomy, valve morphology, and comorbidities, creating the need for customized treatment solutions. Device manufacturers are increasingly focusing on developing advanced transcatheter valves, customized implants, and adaptable delivery systems that can accommodate variations such as small annulus sizes, bicuspid valves, or complex structural defects. These innovations enable physicians to provide more precise and effective interventions, expanding treatment options for patients who may not be suitable for standard devices.

Market Concentration & Characteristics

The chart below illustrates the relationships among industry concentration, industry characteristics, and industry participants. There is a medium degree of innovation, a moderate level of merger & acquisition activities, a moderate impact of regulations, a medium product substitute, and moderate expansion of the industry.

The market is witnessing a moderate degree of innovation driven by the expansion of minimally invasive trans catheter therapies, advanced imaging systems, and improved device technologies that allow physicians to treat complex valve disorders without open-heart surgery. These advancements help reduce procedural risks and recovery time while improving clinical outcomes. For instance, in 2024, the U.S. Food and Drug Administration approved the EVOQUE Tricuspid Valve Replacement System developed by Edwards Lifesciences, the first trans catheter therapy designed to treat severe tricuspid regurgitation, representing rapid technological progress in structural heart interventions.

Key players are increasingly engaging in mergers and acquisitions to strengthen their technological capabilities and expand their structural heart treatment portfolios. These strategic transactions help companies enhance innovation and address unmet clinical needs in cardiovascular care. For instance, in July 2024, Edwards Lifesciences announced agreements to acquire JenaValve Technology and Endotronix for approximately USD 1.2 billion to expand its trans catheter therapy portfolio for aortic regurgitation and heart failure management.

Regulatory frameworks and approval processes play a key role in ensuring the safety, quality, and effectiveness of structural heart devices. While stringent regulatory requirements can lengthen product approval timelines, they also help maintain high clinical standards and increase physician and patient confidence in advanced cardiovascular therapies.

Companies in the structural heart procedures market are expanding into new regions with high cardiovascular disease prevalence and strengthening collaborations with hospitals and cardiac centers to increase the adoption of advanced structural heart therapies. In August 2025, Abbott Laboratories announced that its Navitor Transcatheter Aortic Valve Implantation (TAVI) system received CE Mark in Europe for an expanded indication to treat patients with symptomatic severe aortic stenosis at low and intermediate surgical risk. The approval was supported by positive safety and effectiveness results from the VANTAGE clinical trial, enabling the device to be used across all surgical risk categories in Europe.

Procedure Insights

By procedure, the TAVR (Trans catheter Aortic Valve Replacement) segment dominated the market in 2025 and accounted for the largest revenue share of 48.0%. Technological advancements in valve design and delivery systems have improved procedural accuracy and safety, encouraging physicians to use TAVR in broader patient groups beyond high-risk individuals, and driving the growth of the market. For instance, in May 2025, the U.S. Food and Drug Administration (FDA) approved Edwards Lifesciences’ SAPIEN 3 trans catheter heart valve for the treatment of patients with asymptomatic severe aortic stenosis, enabling physicians to intervene earlier in the disease progression before severe symptoms develop. This approval reflects the growing clinical confidence in TAVR and the shift toward preventive structural heart interventions.

The LAAC (Left Atrial Appendage Closure) segment in the structural heart procedures market is anticipated to witness the fastest CAGR over the forecast period. The increasing number of large randomized clinical trials evaluating LAAC as an alternative to long-term anticoagulation therapy fuels the growth of the market. According to the SOLACI article published in November 2025, the CLOSURE-AF randomized clinical trial evaluated catheter-based left atrial appendage closure compared with best medical therapy in patients with atrial fibrillation who had both high stroke risk and high bleeding risk. The trial enrolled 912 patients across 42 clinical sites, with participants having a CHA₂DS₂-VASc score ≥2 and a high bleeding risk (HAS-BLED ≥3 or prior bleeding history). The median patient age was approximately 79 years, and about 38.6% of participants were women. Patients were randomized to receive either LAAC or optimal medical therapy, and the median follow-up duration in the study was approximately 3 years, during which outcomes such as stroke, systemic embolism, cardiovascular death, and major bleeding were evaluated.

Indication Insights

By Indication, the aortic stenosis segment dominated the structural heart procedures market in 2025, accounting for the largest revenue share of 46.6%. The increasing prevalence of aortic stenosis, driven by aging populations and improved diagnostic screening, fuels market growth. According to an NCBI article published in April 2025, clinical evidence shows that the condition has become one of the most common forms of valvular heart disease in developed healthcare systems. Epidemiological studies indicate that aortic stenosis affects approximately 2-3% of adults over the age of 65, and the prevalence increases significantly with age, reaching around 7% among individuals older than 80 years. Moreover, the prevalence is expected to be doubled by 2050.

The Atrial Fibrillation (Stroke Prevention via LAAC) segment is anticipated to witness the fastest CAGR over the forecast period. The growing real-world evidence displaying the safety and effectiveness of next-generation LAAC devices in large patient populations drives the growth of the market. According to an NCBI article published in September 2024, an analysis from the U.S. NCDR Left Atrial Appendage Occlusion Registry evaluated 97,185 patients who underwent LAAC using the WATCHMAN FLX Left Atrial Appendage Closure Device. The registry reported a 97.5% implantation success rate (94,784 of 97,185 patients). At 45-day follow-up, ischemic stroke occurred in 0.23% of patients, while major bleeding occurred in 3.1%. At 1 year, the rate of any stroke was 1.5%, including 1.2% ischemic stroke, demonstrating favorable real-world safety and stroke prevention outcomes for LAAC procedures in atrial fibrillation patients.

End-use Insights

The hospitals segment dominated the structural heart procedures market in 2025 with a revenue share of 67.4%. Hospitals have increasingly invested in advanced catheterization laboratories and hybrid operating rooms to support minimally invasive cardiac interventions. According to Definitive Healthcare, LLC, an article published in June 2025, more than 800 hospitals in the U.S. were performing Trans catheter Aortic Valve Replacement (TAVR) procedures as of 2024, reflecting the rapid expansion of hospital-based structural heart programs and the increasing adoption of minimally invasive valve treatments.

The specialized cardiac centers segment is anticipated to register the fastest growth rate over the forecast period. The rise of comprehensive structural heart programs within specialized cardiac centers, which allows these facilities to perform high volumes of minimally invasive cardiovascular procedures, fuels the growth of the market. According to Virginia Mason Franciscan Health, in June 2025, the Structural Heart and Valve Program at Virginia Mason Franciscan Health has performed more than 2,500 trans catheter structural heart procedures across its centers, demonstrating the increasing procedural capacity of specialized cardiac institutes for managing complex valve and structural heart diseases. These programs integrate cardiologists, cardiac surgeons, and interventional specialists to deliver coordinated treatment and improve patient outcomes through advanced catheter-based therapies.

Regional Insights

The North America structural heart procedures market dominated the industry in 2025, accounting for the largest revenue share of 52.5%, driven by strong healthcare infrastructure, early adoption of minimally invasive technologies, and supportive regulatory frameworks. Moreover, Clinical research and regulatory progress have accelerated adoption in the region. For instance, in 2025, the TCTMD reported that the U.S. Food and Drug Administration expanded approval of TAVR for certain asymptomatic patients with severe aortic stenosis, following positive results from the EARLY-TAVR clinical trial, highlighting the region’s leadership in advancing structural heart therapies.

U.S. Structural Heart Procedures Market Trends

The structural heart procedures industry in the U.S. dominated the North America market with the largest share in 2025. Clinical advancements further drive the expansion of structural heart interventions in the U.S. healthcare system. For instance, in November 2025, UC Davis Health performed the world’s first trans catheter procedure using a new valve repair device designed to treat both mitral and tricuspid regurgitation, highlighting the country’s role in pioneering structural heart technologies.

Europe Structural Heart Procedures Market Trends

The structural heart procedures industry in Europe is anticipated to register significant growth during the forecast period, driven by the rising use of minimally invasive trans catheter therapies to treat complex valvular heart diseases such as aortic stenosis and mitral regurgitation. Moreover, technologically advanced product launches drive the growth of the market. For instance, in September 2025, Abbott received CE mark approval in Europe for the expanded indication of its Navitor TAVI system to treat patients with low and intermediate surgical risk severe aortic stenosis, broadening the availability of minimally invasive valve replacement technologies across European healthcare systems.

The Germany structural heart procedures industry is expected to grow considerably during the forecast period, driven by a strong network of cardiac hospitals and active clinical research. Minimally invasive treatments such as trans catheter aortic valve implantation (TAVI) are widely used for patients with severe aortic stenosis who are at higher risk for open-heart surgery. For instance, as per the American College of Cardiology Foundation. An article published in April 2024, the DEDICATE-DZHK6 randomized clinical trial, conducted across 38 cardiac centers in Germany, enrolled 1,414 patients and compared TAVI with surgical aortic valve replacement (SAVR) at 12-month follow-up, demonstrating strong outcomes for the minimally invasive approach.

The structural heart procedures industry in Italy is expected to grow considerably during the forecast period, driven by clinical research evaluating optimized treatment pathways for trans catheter aortic valve implantation (TAVI), which fuels the growth of the market. According to a Springer Nature article published in April 2025, the BENCHMARK registry, a multicenter European study assessing best-practice clinical pathways for TAVI, included 300 patients treated in Italian cardiac centers as part of a broader cohort from several European countries. The study found that implementing streamlined care protocols significantly improved efficiency without compromising safety.

Asia Pacific Structural Heart Procedures Market Trends

The structural heart procedures industry in the Asia Pacific is anticipated to be the fastest-growing region, driven by the increasing burden of valvular heart disease, the growing elderly population, and the rapid adoption of minimally invasive catheter-based interventions. For instance, in December 2025, cardiologists at Jupiter Hospital in Pune, India, successfully performed a motorized Trans catheter Aortic Valve Implantation (TAVI) procedure on a high-risk patient with severe aortic stenosis. The motorized system enabled greater precision in valve positioning through a small groin puncture rather than open-heart surgery, and the patient was discharged only two days after the procedure.

The Japan structural heart procedures industry is anticipated to register a significant growth rate during the forecast period. The structural heart procedures landscape in Japan is growing as the country adopts advanced trans catheter technologies to treat severe valvular heart diseases, particularly among its aging population. According to a Springer Nature Limited article published in April 2025, a study using the Nara Kokuho Database analyzed 446 patients who underwent TAVI, with an average age of 84.1 years and 63.7% women, highlighting its common use in elderly patients with severe aortic stenosis. The study reported strong outcomes, with survival rates of 95.1% at 1 year, 90.5% at 2 years, and 69.0% at 5 years, supporting the effectiveness of minimally invasive valve replacement therapies in Japan.

The structural heart procedures industry in China is anticipated to register a significant growth rate during the forecast period, due to technological advancement and increasing clinical adoption of trans catheter therapies for complex valvular diseases. For instance, in September 2025, when the China National Medical Products Administration (NMPA) approved the J-VALVE Transfemoral (TF) Trans catheter Aortic Valve Replacement system, developed by Suzhou Jiecheng under Genesis MedTech, making it the first transfemoral TAVR device in China specifically approved for treating aortic regurgitation.

Latin America Structural Heart Procedures Market Trends

Thestructural heart procedures industry in Latin America is expected to grow significantly over the forecast period. Cardiac centers across countries such as Brazil and Argentina are actively participating in clinical studies assessing the effectiveness of Trans catheter Aortic Valve Implantation (TAVI) for treating severe aortic stenosis. According to an NCBI article published in October 2025, a multicenter study in Chile analyzed outcomes of aortic valve interventions in 1,250 patients aged 75 years or older, including 683 TAVI procedures and 567 surgical valve replacements (SAVR). The study reported lower in-hospital mortality for TAVI (4.5%) compared with SAVR (6.9%), along with a shorter hospital stay of 4 days versus 14 days, highlighting the increasing adoption of minimally invasive valve replacement procedures in Latin America.

The Brazil structural heart procedures industryis growing significantly over the forecast period. Brazil is strengthening its capabilities in minimally invasive structural heart procedures, driven by specialized cardiac centers and increasing expertise in catheter-based valve therapies. According to the NCBI article in December 2025, a clinical evaluation of 325 patients undergoing TAVI reported a median age of 84 years with 58% female patients, and showed improved outcomes as one-year mortality declined from 25% to 14.9% after advancements in procedural techniques and device technology.

Middle East And Africa Structural Heart Procedures Market Trends

Thestructural heart procedures industry in the Middle East and Africa is growing significantly over the forecast period, driven by the fact that hospitals across the region are increasingly adopting trans catheter aortic valve implantation for treating patients with severe aortic stenosis who are considered high risk for conventional open heart surgery. According to the Radcliffe Medical Media. An article published in March 2023, a clinical outcomes study conducted at a major cardiovascular center in the UAE, evaluated 183 patients undergoing transfemoral TAVR, where the median patient age was 76 years, and 42.1% of patients were women. The study reported favorable outcomes, including 30-day mortality of 0.6%, stroke rate of 0.6%, and major vascular complications of 2.2%, indicating that emerging structural heart programs in the Middle East achieve clinical results comparable to those of well-established international cardiac centers.

The South Africa structural heart procedures industryis expected to grow over the forecast period. Cardiovascular disease (CVD) represents a major and growing health burden in South Africa, significantly increasing the demand for advanced cardiac treatment procedures, including structural heart interventions. According to the article published in SciELO in 2024, epidemiological data indicate that cardiovascular diseases account for approximately 17–17.5% of all deaths in the country, meaning nearly one in six deaths is linked to heart disease or stroke. In addition, estimates suggest that around 215 people die every day from cardiovascular conditions, with about five heart attacks and ten strokes occurring every hour.

Key Structural Heart Procedures Company Insights

Key participants in the market are focusing on devising innovative business growth strategies in the form of product portfolio expansions, partnerships & collaborations, mergers & acquisitions, and business footprint expansions.

Key Structural Heart Procedures Companies:

The following key companies have been profiled for this study on the structural heart procedures market.

- Abbott (St. Jude Medical)

- Medtronic

- Boston Scientific Corporation

- Edwards Lifesciences Corporation

- Lepu Medical Technology

- LivaNova PLC

- ATRICURE, INC

- Anteris Technologies

- Micro Interventional Devices, Incorporated

- JenaValve

- W. L. Gore & Associates, Inc.

- Occlutech

- Comed BV

Recent Developments

-

In March 2025, Medtronic launched its Evolut FX+ trans catheter aortic valve (TAVI) system in India after approval by the Central Drugs Standard Control Organisation, offering improved coronary access via a redesigned frame while maintaining proven valve performance for treating severe aortic stenosis.

-

In January 2025, Abbott introduced the Navitor Vision trans catheter aortic valve system in India to treat patients with symptomatic severe aortic stenosis who are at high or extreme surgical risk. The next-generation TAVI technology includes enhanced visibility markers to improve valve positioning accuracy and support minimally invasive valve replacement procedures.

-

In March 2024, Medtronic announced U.S. FDA approval of its newest-generation Evolut FX+ Transcatheter Aortic Valve Replacement (TAVR) system for treating patients with symptomatic severe aortic stenosis across all surgical risk categories. The system features an updated frame design with significantly larger coronary access windows to improve catheter maneuverability while maintaining the valve performance benefits of the Evolut platform.

-

In November 2024, Abbott announced the first patient procedures using its investigational balloon-expandable transcatheter aortic valve implantation (TAVI) system for treating symptomatic severe aortic stenosis. The system represents the first step toward Abbott’s software-guided, AI-enabled TAVI platform, designed to improve procedural precision and complement the company’s Navitor TAVI System.

Structural Heart Procedures Market Report Scope

Report Attribute

Details

Market size in 2025

USD 16.7 billion

Estimated Market size in 2026

USD 18.3 billion

Projected Market size by 2033

USD 36.4 billion

Growth rate

CAGR of 10.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast data

2026 - 2033

Quantitative units

Revenue in USD million/billion, number of procedures in thousand units, and CAGR from 2026 to 2033

Report coverage

Revenue & procedure forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Procedure, indication, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Germany; UK; Spain; Italy; France; Norway; Denmark; Sweden; Japan; China; India; Australia; Thailand; South Korea; Brazil; Mexico; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Abbott (St. Jude Medical); Medtronic; Boston Scientific Corporation; Edwards Lifesciences Corporation; Lepu Medical Technology; LivaNova PLC; ATRICURE, INC;

Anteris Technologies; Micro Interventional Devices, Incorporated; JenaValve; W. L. Gore & Associates, Inc.; Occlutech; Comed BVCustomization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Structural Heart Procedures Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and analyzes industry trends in each sub-segment from 2021 to 2033. For this study, Grand View Research, Inc. has segmented the global structural heart procedures market report based on procedure, indication, end-use, and region:

-

Procedure Outlook (Number of Procedures, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

TAVR (Trans catheter Aortic Valve Replacement)

-

SAVR (Surgical Aortic Valve Replacement)

-

LAAC (Left Atrial Appendage Closure)

-

Mitral Repair (Annuloplasty)

-

Septal Defect Closure

-

Atrial septal defect (ASD)

-

Patent foramen ovalve (PFO)

-

-

-

Indication Outlook (Number of Procedures, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Aortic Stenosis

-

Mitral Regurgitation

-

Congenital Heart Defects

-

Atrial Fibrillation (Stroke Prevention via LAAC)

-

Tricuspid Regurgitation

-

-

End-use Outlook (Number of Procedures, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Specialized Cardiac Centers

-

Others

-

-

Regional Outlook (Number of Procedures, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Spain

-

Italy

-

France

-

Denmark

-

Norway

-

Sweden

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The TAVR (Trans catheter Aortic Valve Replacement) segment led with a 48.0% revenue share in 2025, while LAAC (Left Atrial Appendage Closure) is the fastest-growing procedure.

The aortic stenosis segment led with a 46.6% revenue share in 2025, while atrial fibrillation (stroke prevention via LAAC) is the fastest-growing.

Hospitals segment held the largest share (over 67.0%) in 2025, while specialized cardiac centers is the fastest-growing segment.

Key players include Abbott (St. Jude Medical); Medtronic; Boston Scientific Corporation; Edwards Lifesciences Corporation; Lepu Medical Technology; LivaNova PLC; ATRICURE, INC; Anteris Technologies; Micro Interventional Devices, Incorporated; JenaValve; W. L. Gore & Associates, Inc.; Occlutech; Comed BV.

Key factors driving structural heart procedures market are the rising global prevalence of structural heart diseases, cardiovascular diseases, and the increasing demand for minimally invasive surgeries.

North America dominated the structural heart procedures market in 2025 and accounted for the largest revenue share of 52.5%, driven by strong healthcare infrastructure, early adoption of minimally invasive technologies, and supportive regulatory frameworks.

The global structural heart procedures market size was valued at USD 16.7 billion in 2025 and is estimated at USD 18.3 billion for 2026.

The global structural heart procedures market is expected to grow at a CAGR of 10.3% from 2026 to 2033, reaching USD 36.4 billion by 2033.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.