- Home

- »

- Advanced Interior Materials

- »

-

Structural Steel Market Size And Share Report, 2026-2033GVR Report cover

![Structural Steel Market (2026 - 2033)Report]()

Structural Steel Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Angles, Channels, Rounds, Squares, Beams), By Application (Non-residential, Residential), By Region (North America, Europe, Asia Pacific, Latin America, MEA), And Segment Forecasts

Market Size, 2025

$123.4BMarket Estimate, 2026

$128.0BMarket Forecast, 2033

$202.1BCAGR, 2026–2033

6.7%Structural Steel Market Summary

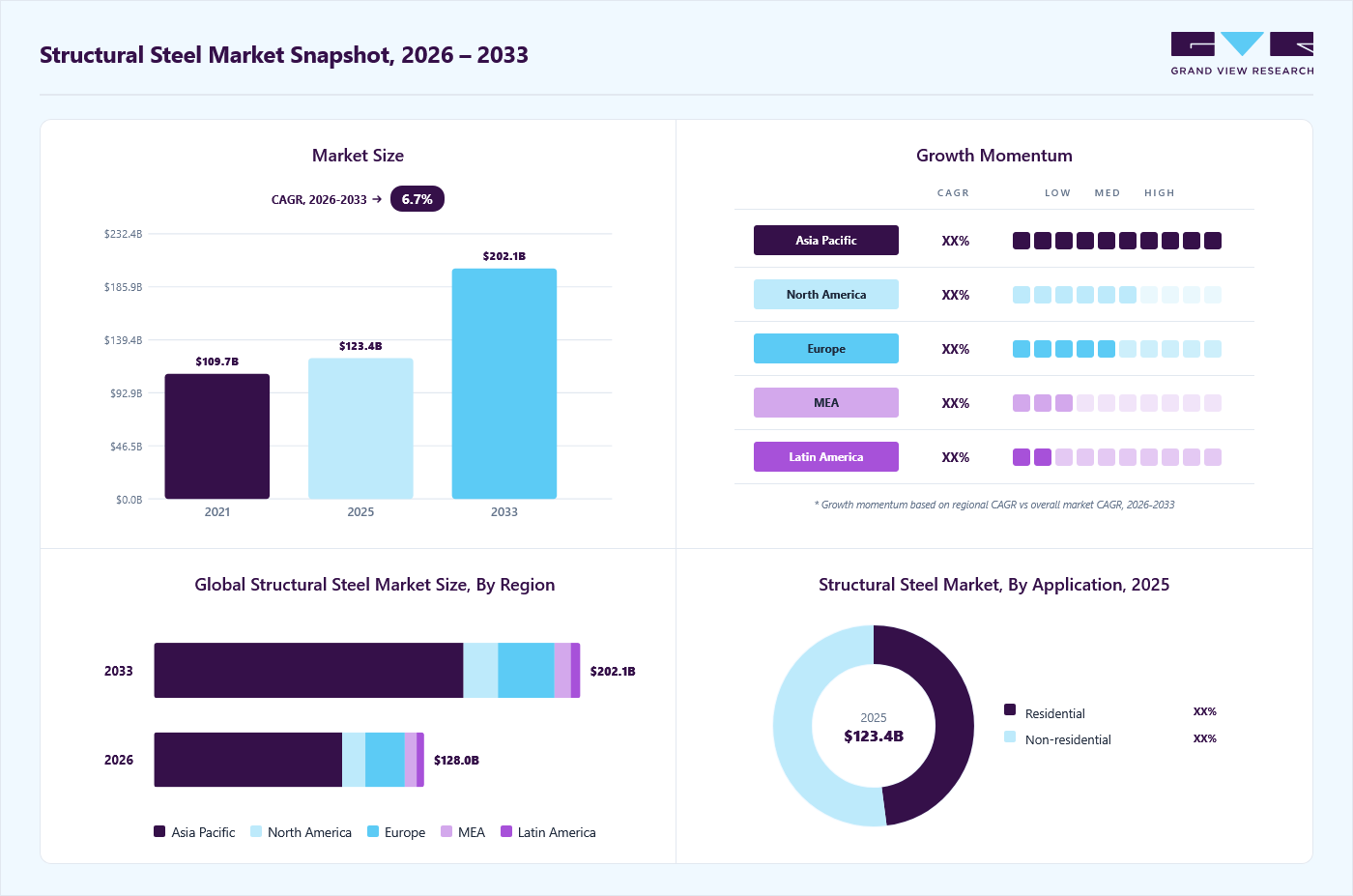

TThe global structural steel market size was valued at USD 123.4 billion in 2025 and is projected to grow from USD 128.0 billion in 2026 to USD 202.1 billion by 2033, at a CAGR of 6.7% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 69.4% in 2025. The market is experiencing robust growth, primarily driven by rising demand for large-scale infrastructure development, rapid urbanization, and increased investment in commercial and industrial construction across both developed and emerging economies.

Key Market Trends & Insights

- By product: Beams segment held the largest market share of 32.0% in 2025.

- By application: Non-residential segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (69.4% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 123.4 Billion

- Estimated market size in 2026: USD 128.0 Billion

- Projected market size by 2033: USD 202.1 Billion

- CAGR (2026-2033): 6.7%

Structural steel’s high strength-to-weight ratio, design flexibility, and recyclability are further reinforcing its adoption in modern construction projects, particularly in high-rise buildings, transportation infrastructure, and energy facilities.The market is increasingly aligned with ESG and sustainability objectives, primarily because steel is inherently recyclable and compatible with the circular economy. Structural steel is 100% recyclable without loss of mechanical properties, and a significant share of global production already relies on recycled scrap processed through electric arc furnaces (EAFs). This substantially reduces raw material extraction, energy consumption, and lifecycle emissions compared to alternative construction materials. As governments and developers prioritize low-carbon building materials, structural steel is gaining preference in green-certified projects and sustainable infrastructure programs.

")

From a governance and environmental compliance perspective, steel producers are actively investing in decarbonization technologies, including hydrogen-based direct-reduced iron (DRI), increased integration of renewable energy, and process efficiency improvements. Transparency in emissions reporting, adoption of environmental product declarations (EPDs), and adherence to global standards such as ISO 14001 and ESG disclosure frameworks are strengthening stakeholder confidence. These initiatives not only support regulatory compliance but also enhance long-term resilience, making structural steel a key material in sustainable urban development and climate-resilient infrastructure.

Drivers, Opportunities & Restraints

The market is primarily driven by strong demand from the infrastructure and construction sectors, where large government-backed projects and urban development initiatives continue to drive steel use for bridges, buildings, metros, and industrial facilities. For example, India’s domestic steel demand is forecast to grow about 8% in FY26, supported by ongoing infrastructure and construction activity even amid price pressures, according to ICRA’s recent industry outlook. In addition, major Indian steelmakers such as Jindal Steel are expanding structural steel capacity, planning to double output at their Raigarh facility by 2028 to meet rising demand from the infrastructure, energy, and industrial sectors.

Significant opportunities lie in the transition toward sustainable, technologically advanced construction and in underpenetrated end-use segments. Structural steel’s recyclability and compatibility with modern construction practices (such as prefabrication and modular systems) make it favorable for green building standards and faster project delivery, while emerging uses in data centers and renewable energy infrastructure signal broader demand. A recent ConstructConnect report highlights that data center construction spending has surged, driving demand for structural steel amid a five-fold increase in project starts over two years, illustrating how new end markets can expand steel’s application base.

Market expansion is constrained by price volatility and supply-chain challenges, which directly affect project economics and margins. Steel and other metal prices have remained unpredictable, with construction firms reporting ongoing cost pressures entering 2026 due to tariffs, energy costs, and metal price swings, conditions that are tightening margins and complicating long-term contracts. In India, while demand is healthy, steel price pressures and corrections from earlier spikes have kept producer margins under strain despite robust activity, underscoring how pricing volatility restrains structural growth in the steel market.

Product Insights

The beams segment, which includes I-beams, H-beams, and universal beams, accounted for the largest market revenue share of over 32.0% in 2025. These products are widely used in load-bearing frameworks for commercial buildings, bridges, industrial facilities, and large-span structures due to their strength and versatility. Demand for beams continues to rise globally, supported by ongoing infrastructure and construction activities in both developed and developing regions.

Angles (L-shaped sections) and channels (C-shaped sections) are essential for supporting structural frameworks and secondary construction needs. Angles are commonly used for bracing, frames, and smaller structural elements, while channels are often applied in architectural and civil engineering projects, such as wall supports and modular assemblies. Though their share is lower than that of beams, they remain key market components due to their adaptability and widespread application.

Application Insights

Non-residential applications, including commercial buildings, industrial facilities, institutional projects, and infrastructure, account for the largest share of structural steel consumption. This segment continues to grow rapidly as investments in infrastructure, industrial projects, and commercial construction expand worldwide. Structural steel is preferred for these projects because of its durability, strength, and suitability for long-span and high-rise structures.

The non-residential segment is anticipated to register the fastest CAGR of 6.9% from 2026 to 2033. The residential segment includes single-family homes, multi-story apartments, and mixed-use developments. Although its share is smaller than that of non-residential construction, residential construction continues to contribute to structural steel demand, driven by urbanization and modern housing requirements. Structural steel is increasingly used in residential buildings for faster construction, modular designs, and long-term sustainability.

Regional Insights

North America structural steel market held a significant market share, driven by continuous investments in infrastructure, commercial construction, and industrial projects. The region benefits from stable demand across sectors such as transportation, energy, and high-rise commercial developments. Advanced construction technologies, such as prefabrication and modular steel systems, are increasingly adopted to reduce project timelines and improve cost efficiency.

U.S. Structural Steel Market Trends

The structural steel market in the U.S. is the largest contributor to North America. Federal and state infrastructure initiatives, including highway expansion, bridge rehabilitation, and public building projects, support growth. The demand for high-strength steel in industrial facilities and commercial complexes further reinforces the market, while sustainable construction practices continue to favor steel over alternative materials.

Europe Structural Steel Market Trends

The structural steel market in Europe holds steady growth, largely driven by infrastructure modernization, commercial construction, and renewable energy projects. Countries such as Germany, France, and the UK are investing in industrial facilities and urban development, while green building regulations encourage the use of recyclable steel. Ongoing retrofitting of older structures and adoption of modular steel construction techniques are also supporting market expansion.

Asia Pacific Structural Steel Market Trends

Asia Pacific dominated the structural steel market with the largest market revenue share of over 69.4% in 2025, and is the fastest-growing, driven by rapid urbanization, large-scale infrastructure projects, and industrial expansion. Countries like China, India, and Southeast Asian nations are investing heavily in high-rise buildings, bridges, airports, and energy infrastructure. Rising demand from residential and non-residential construction, combined with government-led infrastructure programs, positions the region as a key global growth driver.

Latin America Structural Steel Market Trends

The structural steel market in Latin America is growing steadily, fueled by investments in infrastructure, industrial facilities, and commercial construction. Countries such as Brazil and Mexico are undertaking highway projects, urban development initiatives, and expanding energy infrastructure. While the market faces challenges from economic fluctuations, structural steel remains a preferred choice due to its durability, flexibility, and long-term cost benefits.

Middle East & Africa Structural Steel Market Trends

The structural steel market in the Middle East and Africa regions is seeing increasing demand, driven by large-scale infrastructure, industrial, and commercial projects. Nations like Saudi Arabia, the UAE, and South Africa are investing in transportation, energy, and urban development. The market is further driven by mega construction projects, including airports, commercial complexes, and high-rise buildings, with structural steel favored for its strength, design flexibility, and ability to support rapid construction timelines.

Key Structural Steel Company Insights

Some of the key players operating in the market include ArcelorMittal S.A., JSW Steel Limited, and others.

-

ArcelorMittal S.A. is a Luxembourg-based global steel producer founded in 2006 through the merger of Arcelor and Mittal Steel. The company manufactures a wide range of steel products, including structural steel for construction, industrial, and infrastructure projects. ArcelorMittal emphasizes innovation and sustainability, investing in low-carbon steel technologies and supplying steel to large-scale commercial and infrastructure developments worldwide.

-

JSW Steel Limited is an India-based steel manufacturer established in 1982, with operations spanning domestic and international markets. The company produces structural steel, long products, and special steel grades for construction, infrastructure, and industrial applications. JSW Steel focuses on sustainable manufacturing practices, including energy-efficient production and recycling, and supplies steel to large-scale infrastructure projects, commercial buildings, and residential construction.

-

Tata Steel Limited is an India-based multinational steel company founded in 1907, producing a wide portfolio of steel products, including structural steel for residential, commercial, and industrial use. The company emphasizes sustainability and innovation, implementing eco-friendly production methods and advanced manufacturing technologies. Tata Steel serves infrastructure projects, high-rise construction, and industrial facilities globally and is recognized for its contributions to urban development and construction growth.

Key Structural Steel Companies:

The following key companies have been profiled for this study on the structural steel market.

- ArcelorMittal S.A.

- Baogang Group

- Evraz plc

- Gerdau S.A.

- JSW Steel Limited

- Nippon Steel Corporation

- POSCO

- Steel Authority of India Limited (SAIL)

- Tata Steel Limited

- United States Steel Corporation

Recent Developments

-

JSW Steel announced on 21 July 2025 a planned allocation of approximately USD 2.4 billion (INR 20,000 crore) in capital expenditure for FY26, with most funding designated for expanding its Dolvi steel plant capacity from 10 million tons to 15 million tons by September 2027. This investment aims to support broader production growth and downstream projects across the company’s operations, strengthening its position in long‑term steel demand markets.

-

Jindal Steel revealed on 29 December 2025 an expansion plan to double structural steel capacity at its Raigarh facility from 1.2 million to 2.4 million tons per annum by mid‑2028, enhancing capabilities to produce larger and more complex heavy structural sections for infrastructure and energy projects. While the company did not disclose the total investment publicly, this strategic capacity ramp‑up accompanies broader capital commitments that exceed USD 1.5 billion across growth projects.

-

ArcelorMittal reported on 5 February 2026 that it expects a roughly 2 % rise in global steel demand for 2026, supported by operational improvements and trade protections, and highlighted continued profitability and momentum with core earnings significantly above forecasts. The company is also benefiting from European policy measures such as the Carbon Border Adjustment Mechanism, which could enhance regional competitiveness and demand for steel products.

Structural Steel Market Report Scope

Report Attribute

Details

Market definition

The market size represents the annual sales value of structural steel products in a particular year.

Market size in 2025

USD 123.4 billion

Estimated market size in 2026

USD 128.0 billion

Projected market size by 2033

USD 202.1 billion

Growth rate

CAGR of 6.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue and volume forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; Russia; Turkey; France; Spain; Poland; China; Taiwan; Thailand; Malaysia; Singapore; Hong Kong; Vietnam; Philippines; India; Australia; New Zealand; Indonesia; Brazil; Colombia; Chille; Saudi Arabia; UAE; Iran; South Africa

Key companies profiled

ArcelorMittal S.A.; Baogang Group; Evraz plc; Gerdau S.A.; JSW Steel Limited; Nippon Steel Corporation; POSCO; SAIL; Tata Steel Limited; United States Steel Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Structural Steel Market Report Segmentation

This report forecasts country revenue growth and analyzes the latest trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global structural steel market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Angles

-

Channels

-

Rounds

-

Squares

-

Beams

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Residential

-

Non-residential

-

Institutional

-

Commercial

-

Offices

-

Others

-

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Russia

-

Turkey

-

France

-

Spain

-

Poland

-

-

Asia Pacific

-

China

-

Taiwan

-

Thailand

-

Malaysia

-

Singapore

-

Hong Kong

-

Vietnam

-

Philippines

-

India

-

Australia

-

New Zealand

-

Indonesia

-

-

Latin America

-

Brazil

-

Colombia

-

Chille

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Iran

-

South Africa

-

-

Frequently Asked Questions About This Report

Some key players in the structural steel market include ArcelorMittal S.A., Baogang Group, Evraz plc, Gerdau S.A., JSW Steel Limited, Nippon Steel Corporation, POSCO, SAIL, Tata Steel Limited, United States Steel Corporation, and others.

The key driver of the structural steel market is the rapid expansion of construction and infrastructure projects, including commercial buildings, industrial facilities, bridges, and transportation networks. This demand is further reinforced by urbanization, government-led infrastructure spending, and the preference for steel due to its high strength, durability, and faster construction timelines.

Non-residential held the largest revenue share in 2025.

Asia Pacific dominated with a 69.4% revenue share in 2025.

The global structural steel market size was estimated at USD 123.4 billion in 2025 and is expected to reach USD 128.0 billion in 2026.

The global structural steel market is expected to grow at a compound annual growth rate of 6.7% from 2026 to 2033 to reach USD 202.1 billion by 2033.

Beams accounted for the largest market revenue share of over 32.0% in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.