- Home

- »

- Sensors & Controls

- »

-

Switchgear Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Switchgear Market (2026 - 2033)Report]()

Switchgear Market (2026 - 2033)

Size, Share & Trends Analysis Report By Voltage Type (Low Voltage, Medium Voltage, High Voltage), By Insulation (Air, Gas), By Installation (Indoor, Outdoor), By End Use (T & D Utilities, Commercial & Residential), By Region, And Segment Forecasts

Market Size, 2025

$112.9BMarket Estimate, 2026

$119.7BMarket Forecast, 2033

$197.7BCAGR, 2026–2033

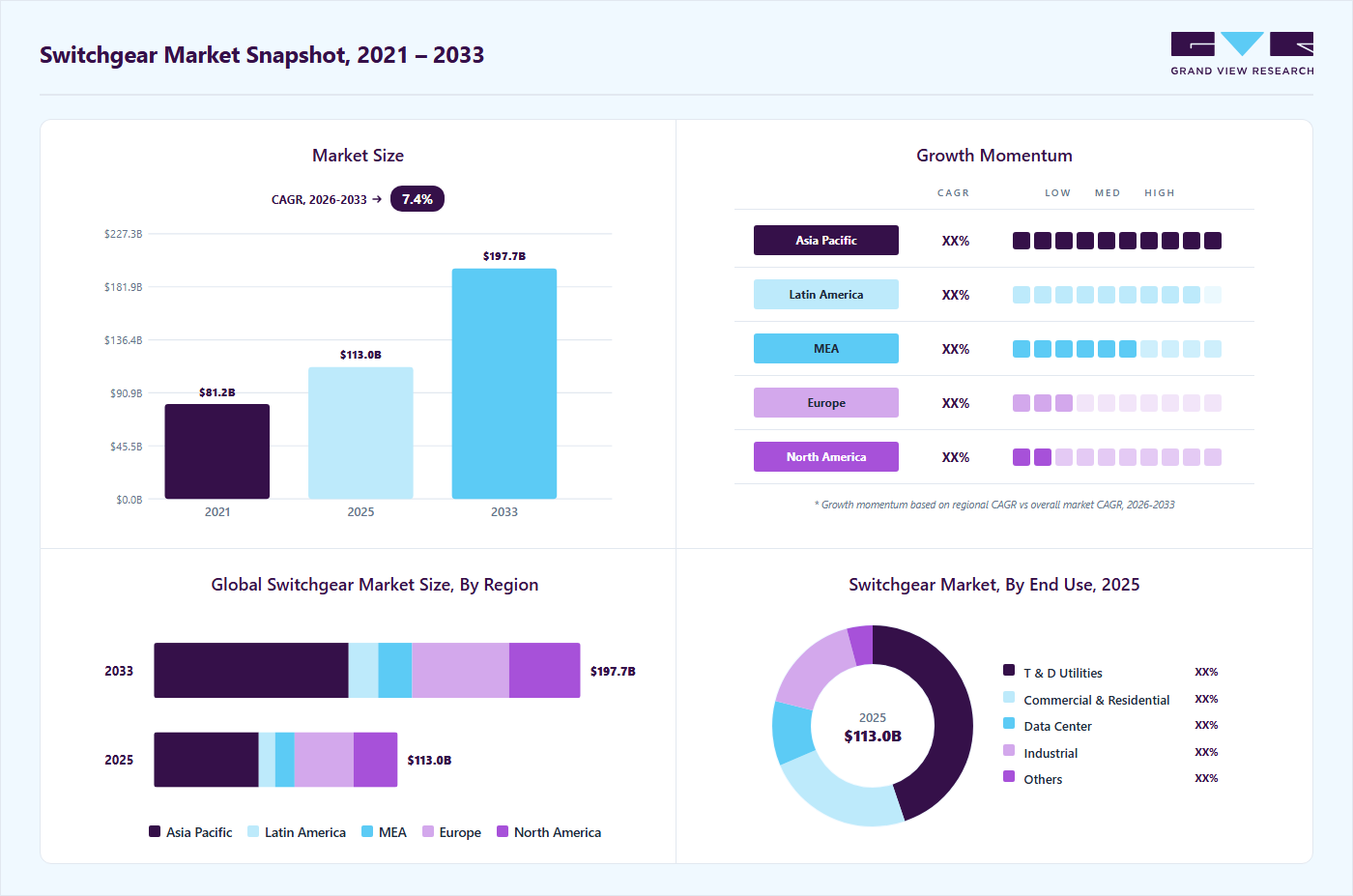

7.4%Switchgear Market Summary

The global switchgear market size was valued at USD 112.9 billion in 2025 and is projected to grow from USD 119.7 billion in 2026 to USD 197.7 billion by 2033, at a CAGR of 7.4% from 2026 to 2033. The Asia Pacific held the largest share of 42.9% of the global market in 2025. A major factor expected to drive the global switchgear industry is the growing emphasis on developing smart grid infrastructure.

Key Market Trends & Insights

- By voltage type: The high voltage segment held the largest market share of 50.2% in 2025.

- By insulation: The air segment accounted for the largest market revenue share in 2025.

- By installation: The indoor segment accounted for the largest market revenue share in 2025.

- By end use: T&D utilities accounted for the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (fastest CAGR, 2026-2033)

- By country: China held a substantial revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 112.9 Billion

- Estimated market size in 2026: USD 119.7 Billion

- Projected market size by 2033: USD 197.7 Billion

- CAGR (2026-2033): 7.4%

Governments of developed and emerging economies are focused on upgrading the existing electric grid infrastructure to ensure an efficient electricity supply and reduce failures of electrical components during power transmission. Switchgear aids in lowering the damage to the components that are connected to the power supply during the event of a power surge by interrupting the power flow.Due to rapid urbanization and industrialization, the increasing demand for power in emerging economies has led to a strong emphasis on developing efficient power transmission and distribution networks, ultimately driving demand for switches, fuses, and circuit breakers. This high demand for products from the power sector is expected to drive the growth of the global switchgear industry. In addition, the rise of new factories, commercial buildings, and residential complexes is further driving demand for robust electrical distribution and protection systems. Medium-voltage switchgear is experiencing rapid adoption in these sectors. Supportive government policies, infrastructure development programs, and foreign direct investment (FDI) inflows are further strengthening the switchgear industry.

")

Aging power infrastructure and rising electricity consumption are prompting large-scale investments in grid modernization, particularly in developed markets. Switchgear plays a pivotal role in enabling intelligent grid operations by protecting electrical circuits and supporting automation and real-time control. The growing adoption of digital switchgear equipped with IoT sensors, remote monitoring, and predictive maintenance capabilities is enhancing operational efficiency and reducing downtime. Utilities and transmission operators are increasingly upgrading to smart switchgear systems as part of broader grid digitalization strategies, fueling market growth.

Significant strides in switchgear technologies, including gas-insulated switchgear (GIS) and solid-state switchgear, have revolutionized the landscape of electrical infrastructure. The seamless integration of digital technologies, such as the Internet of Things (IoT) and advanced analytics, has ushered in a new era of switchgear management. These rapid advancements in switchgear technologies, coupled with the integration of digital solutions, have spurred substantial growth in the switchgear industry. Benefits such as improved operational efficiency, reduced maintenance costs, and increased system reliability have made the adoption of these technologies highly desirable for industries across the board. As a result, such factors provide lucrative opportunities for the growth of the switchgear industry in the coming years.

Switchgear systems typically involve high initial capital expenditure, which can deter potential adopters and constrain market expansion. The significant costs associated with the procurement, installation, and maintenance of these systems pose a particular challenge in developing regions, where financial constraints are prevalent. These upfront financial requirements represent a substantial barrier, especially for cost-sensitive sectors that prioritize short-term affordability over long-term infrastructure investment. The total expenditure includes the purchase of switchgear components, integration, commissioning, and ongoing servicing, all of which contribute to increased overall costs. Thus, these financial demands remain a key restraint on the broader adoption and growth of the switchgear industry.

Voltage Type Insights

The high voltage segment led the market with the largest revenue share of 50.2% in 2025. The dominance is primarily driven by sustained investments in transmission infrastructure, grid modernization, and large-scale renewable energy integration. Utilities worldwide are increasingly deploying high-voltage switchgear to support long-distance power transmission, improve grid reliability, and accommodate rising electricity demand resulting from urbanization and industrial expansion. The transition toward renewable energy sources such as wind and solar has further accelerated HV installations, as these projects require robust transmission networks to connect remote generation sites to load centers.

The medium voltage segment is expected to witness at the fastest CAGR over the forecast period. With increasing urbanization, industrialization, and the rapid expansion of renewable energy sources, demand for efficient, reliable electrical distribution systems is rising. Medium-voltage systems ensure safe and efficient power distribution, protection, and control in medium-voltage networks. Moreover, upgrading aging electrical infrastructure, particularly in emerging economies, presents substantial market potential. In addition, the increasing focus on grid resilience, smart grid technologies, and the integration of advanced digital solutions are driving the demand for innovative medium-voltage products and solutions.

Insulation Insights

The air segment accounted for the largest market revenue share in 2025. The high share can be due to its cost efficiency, operational reliability, and widespread applicability across utility, industrial, and commercial power distribution networks. Air insulation remains the preferred choice for many installations, particularly in regions where land availability is less constrained, as AIS systems offer a simpler design architecture, easier maintenance, and lower upfront capital costs than gas-insulated or solid-insulated alternatives. Utilities and industrial operators continue to favor air-insulated solutions for substations and distribution networks because of their proven performance, scalability, and suitability for both indoor and outdoor installations.

The gas segment is expected to register at the fastest CAGR of 7.7% during the forecast period.The growing demand for reliable, efficient power distribution infrastructure, particularly in developing economies, is driving the expansion of the gas segment. These advanced switchgear systems offer numerous advantages, including enhanced safety features, compact size, and superior environmental performance. In addition, the increasing focus on renewable energy sources and the integration of smart grid technologies are driving the adoption of gas insulation, as they provide seamless integration with renewable power generation and enable efficient monitoring and control of electricity networks.

Installation Insights

The indoor segment accounted for the largest market revenue share in 2025. The growing emphasis on safety and reliability in electrical systems has led to an increased demand for indoor installations, as they offer enhanced protection against environmental elements and unauthorized access. The rising adoption of smart grid technologies and the integration of renewable energy sources has spurred the need for advanced indoor solutions capable of efficiently managing power distribution and accommodating complex grid configurations. In addition, the ongoing urbanization & expansion of infrastructure in developing economies have fueled the demand for indoor switchgear installations, as they provide space-saving benefits and can be easily integrated into compact urban environments.

The outdoor segment is expected to witness at the fastest CAGR over the forecast period. The increasing demand for reliable, efficient power distribution systems across industries and utility sectors has driven the need for robust outdoor installations. These installations provide enhanced protection against harsh environmental conditions, such as extreme temperatures, moisture, and dust, ensuring an uninterrupted power supply. The rapid expansion of renewable energy generation adoption, including solar and wind power, has necessitated outdoor deployment to connect these decentralized energy sources to the grid efficiently. In addition, the growing focus on electrification and the modernization of existing infrastructure in emerging economies has led to the adoption of outdoor switchgear solutions for distribution networks in urban and rural areas.

End Use Insights

The transmission & distribution utilities (T & D utility) segment led the market with the largest revenue share of 44.72% in 2025. The increasing demand for reliable and uninterrupted power supply drives the need for efficient switchgear to manage and control electrical power distribution. In addition, expanding renewable energy sources and integrating smart grid technologies require advanced switchgear systems to accommodate complex power flows and ensure grid stability. Moreover, the need to upgrade the aging infrastructure and replace outdated switchgear with more efficient and environmentally friendly alternatives is a significant driver in the market. The growing focus on enhancing grid resilience and mitigating the risks of power outages and electrical faults is driving the adoption of advanced switchgear technologies with enhanced safety features.

The commercial & residential segment is expected to register at the fastest CAGR over the forecast period. Rapid urbanization and industrialization in the segment are key factors driving the demand for switchgear, as they require efficient electrical distribution and protection systems. In addition, the expansion of data centers, the adoption of smart grids, and the growing emphasis on renewable energy sources contribute to market growth. In the residential sector, factors such as rising disposable incomes, a growing urban population, and the need for enhanced safety measures are driving the demand for switchgear. Moreover, the ongoing digitalization and home automation trends, coupled with the growing demand for electric vehicles and energy-efficient solutions, further boost the market demand, as residential consumers seek reliable electrical infrastructure and advanced control systems.

Regional Insights

The switchgear market in North America is driven by population growth, industrialization, and urbanization, which has amplified the need for efficient power distribution and transmission systems in the region. This has created a significant market for switchgear, which plays a crucial role in controlling, protecting, and isolating electrical equipment. Moreover, the aging infrastructure and the growing focus on grid modernization and renewable energy integration are further propelling the demand for advanced switchgear solutions in North America. In addition, the emergence of smart grids and the rapid adoption of digital technologies, such as IoT and cloud computing, create opportunities to integrate intelligent switchgear systems that enhance energy management and optimize operational efficiency.

U.S. Switchgear Market Trends

The switchgear market in the U.S. accounted for the largest market revenue share in North America in 2025. The U.S. switchgear industry is characterized by ongoing grid modernization efforts, a surge in renewable energy integration, and the development of resilient, intelligent infrastructure. Federal investments in energy storage, electric vehicle charging networks, and climate-resilient systems are expanding the need for advanced switchgear technologies. The presence of a mature utility sector and increasing demand from data centers and industrial automation continue to support market growth.

Asia Pacific Switchgear Market Trends

Asia Pacific dominated the global switchgear market with the largest revenue share of 42.99% in 2025 and is expected to grow at the fastest CAGR of 8.7% during the forecast period. Rapid industrialization and urbanization across the region are boosting the demand for electricity, thereby fueling the need for efficient and reliable switchgear solutions. The growing focus on renewable energy sources and the integration of smart grid technologies are leading to the adoption of advanced switchgear systems capable of handling complex power distribution networks. Moreover, the expansion of industries such as oil and gas, manufacturing, and construction, coupled with investments in infrastructure development projects, is further propelling the demand for switchgear products in the Asia Pacific region. The rising awareness about the importance of electrical safety and the need for uninterrupted power supply is creating opportunities for market growth, as end-users are prioritizing the installation of reliable switchgear systems to safeguard their operations and ensure uninterrupted power flow.

The switchgear market in India is expected to grow at the fastest CAGR during the forecast period, driven by rapid urbanization, industrial expansion, and government-led initiatives such as Power for All and the Smart Cities Mission. The increasing investments in grid modernization, rural electrification, and renewable energy projects are propelling demand for both low- and medium-voltage switchgear. In addition, the Make in India policies are encouraging domestic manufacturing, creating opportunities for local and international players, and thereby driving demand for switchgear solutions.

The China switchgear market held a substantial market share in the Asia Pacific in 2025, driven by its extensive investments in infrastructure, energy transmission, and smart grid development. The government’s focus on decarbonization and the expansion of clean energy, including ultra-high-voltage projects, continues to drive demand for high-voltage switchgear solutions. For instance, in May 2025, Hitachi Energy Ltd announced the delivery of the world’s first sulfur hexafluoride (SF₆)-free 550 kV gas-insulated switchgear (GIS) to the Central China Branch of the State Grid Corporation of China. This groundbreaking milestone represents a major advancement in efforts to decarbonize the power grid and supports China’s broader goal of achieving carbon neutrality by 2060.

Europe Switchgear Market Trends

The switchgear market in Europe is expected to register at a notable CAGR from 2026 to 2033. Europe's market is being driven by aggressive decarbonization goals, widespread electrification, and the transition to renewable energy. The European Union’s Green Deal and stringent environmental regulations are accelerating the adoption of digital and environmentally sustainable switchgear systems. Smart grid projects across countries such as Germany, the UK, France, and Italy are driving demand for high-performance, low-emission switchgear technologies.

The UK switchgear market is expected to grow at a significant CAGR during the forecast period.The country’s commitment to achieving net-zero emissions by 2050 is fostering the adoption of low-loss, eco-friendly switchgear technologies. Urban infrastructure developments and the electrification of public transport networks are creating additional demand across residential, commercial, and utility segments.

The switchgear market in Germany held a substantial market share in Europe in 2025. Germany’s market is driven by its advanced industrial base, smart energy transition policies, and a strong push toward a decentralized power system. Germany’s acceleration of its Energiewende strategy is driving increased demand for high-efficiency, digital switchgear to enable the integration of renewables and maintain grid stability.

Key Switchgear Company Insights

Some of the key companies in the switchgear industry include ABB Ltd., Eaton Corporation, General Electric, and Siemens AG, among others. These companies focus on technological innovation, extensive product portfolios, and global distribution networks. The growth of these companies is driven by the need for advanced, eco-friendly, and digitally integrated switchgear solutions, particularly as utilities and industries modernize their electrical infrastructure.

-

ABB Ltd. is a key player in the switchgear industry, delivering advanced low- and medium-voltage systems designed for safety, reliability, and efficiency. The company has a strong global footprint and offers digital switchgear with integrated condition monitoring and predictive maintenance capabilities. The company’s focus on electrification, automation, and sustainable energy solutions has made it a preferred partner for utilities and large-scale industrial clients worldwide.

-

Siemens AG is a global technology powerhouse headquartered in Germany, known for its extensive portfolio in power transmission and distribution. The company offers a comprehensive range of switchgear solutions, including air-insulated, gas-insulated, and digital switchgear systems tailored for utilities, industrial operations, and infrastructure projects.

Key Switchgear Companies:

The following key companies have been profiled for this study on the switchgear market.

- ABB Ltd.

- Eaton Corporation

- General Electric

- Hitachi Limited

- Bharat Heavy Electricals Limited (BHEL)

- Crompton Greaves

- Powell Industries

- Legrand

- Atlas Electric, Inc.

- Siemens AG

Recent Developments

-

In November 2025, Schneider Electric introduced GM AirSeT, an SF6-free primary GIS solution using pure-air insulation and vacuum interruption. The system supports condition-based maintenance through embedded sensors, is designed for high-rating utility, industrial, and data center applications, and aligns with sustainable grid modernization goals.

-

In October 2025, Siemens launched NX Air 11 kV air-insulated MV switchgear in Qatar. The product delivers reliable, resource-efficient power distribution for local utilities and critical infrastructure, with nearly 500,000 units deployed globally. The launch included live demonstrations and professional engagement to support regional adoption.

-

In July 2025, ABB supplied next-generation SF6-free SafeRing and SafePlus Air 24 kV GIS to E.ON in Germany. The deployment supports the EU F-gas phase-out, maintains existing operational footprint, and enables utilities to transition seamlessly to environmentally friendly MV switchgear while reducing greenhouse gas emissions.

Switchgear Market Report Scope

Report Attribute

Details

Market size in 2025

USD 112.9 billion

Estimated market size in 2026

USD 119.7 billion

Projected market size by 2033

USD 197.7 billion

Growth rate

CAGR of 7.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Voltage type, insulation, installation, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Spain; Italy; China; Japan; India; South Korea; Australia; Brazil; Argentina; KSA; UAE; and South Africa

Key companies profiled

ABB Ltd.; Eaton Corporation; General Electric; Hitachi Limited; Bharat Heavy Electricals Limited (BHEL); Crompton Greaves; Powell Industries; Legrand; Atlas Electric, Inc.; Siemens AG

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Switchgear Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global switchgear market report based on voltage type, insulation, installation, end use, and region:

-

Voltage Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Low Voltage

-

Medium Voltage

-

High Voltage

-

-

Insulation Outlook (Revenue, USD Million, 2021 - 2033)

-

Air

-

Gas

-

Others

-

-

Installation Outlook (Revenue, USD Million, 2021 - 2033)

-

Indoor

-

Outdoor

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

T & D Utilities

-

Commercial & Residential

-

Data Center

-

Industrial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Spain

-

Italy

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global switchgear market size was valued at USD 112.9 billion in 2025 and is estimated at USD 119.7 billion in 2026.

The global switchgear market is expected to grow at a CAGR of 7.4% from 2026 to 2033, reaching USD 197.7 billion by 2033.

Asia Pacific is the fastest-growing region and is expected to grow at a CAGR of 8.7% during the forecast period.

The high voltage segment led the market with the largest revenue share of 50.2% in 2025, while the medium voltage segment is expected to witness the fastest growth during the forecast period.

The air insulation segment held the largest market revenue share in 2025, while the gas insulation segment is expected to register the fastest CAGR of 7.7% during the forecast period.

The indoor segment accounted for the largest market revenue share in 2025, while the outdoor segment is expected to witness the fastest growth over the forecast period.

The transmission & distribution utilities segment led the market with the largest revenue share of 44.72% in 2025, while the commercial & residential segment is expected to register the fastest CAGR during the forecast period.

Asia Pacific dominated the global switchgear market with the largest revenue share of 42.9% in 2025.

Some of the key players operating in the switchgear market include ABB Ltd., Eaton Corporation, General Electric, Hitachi Limited, Bharat Heavy Electricals Limited (BHEL), Crompton Greaves, Powell Industries, Legrand, Atlas Electric, Inc., and Siemens AG.

Key factors driving the switchgear market include growing investments in smart grid infrastructure, modernization of aging power grids, and increasing electricity demand due to urbanization and industrialization.

About the Author(s)

Sensors & Controls Research Team

Semiconductors & Electronics · Sensors & ControlsThis report was authored by the sensors & controls research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the sensors & controls segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.