- Home

- »

- Clinical Diagnostics

- »

-

Syphilis Testing Market Size, Share, Industry Report, 2033GVR Report cover

![Syphilis Testing Market Size, Share & Trends Report]()

Syphilis Testing Market (2026 - 2033) Size, Share & Trends Analysis Report By Technology (Molecular Diagnostics, Immunoassay, Others), By Location Of Testing (Laboratory Testing, Point of Care Testing), By Region, And Segment Forecasts

Market Size, 2025

$1.5BMarket Estimate, 2026

$1.6BMarket Forecast, 2033

$2.3BCAGR, 2026–2033

5.2%Syphilis Testing Market Summary

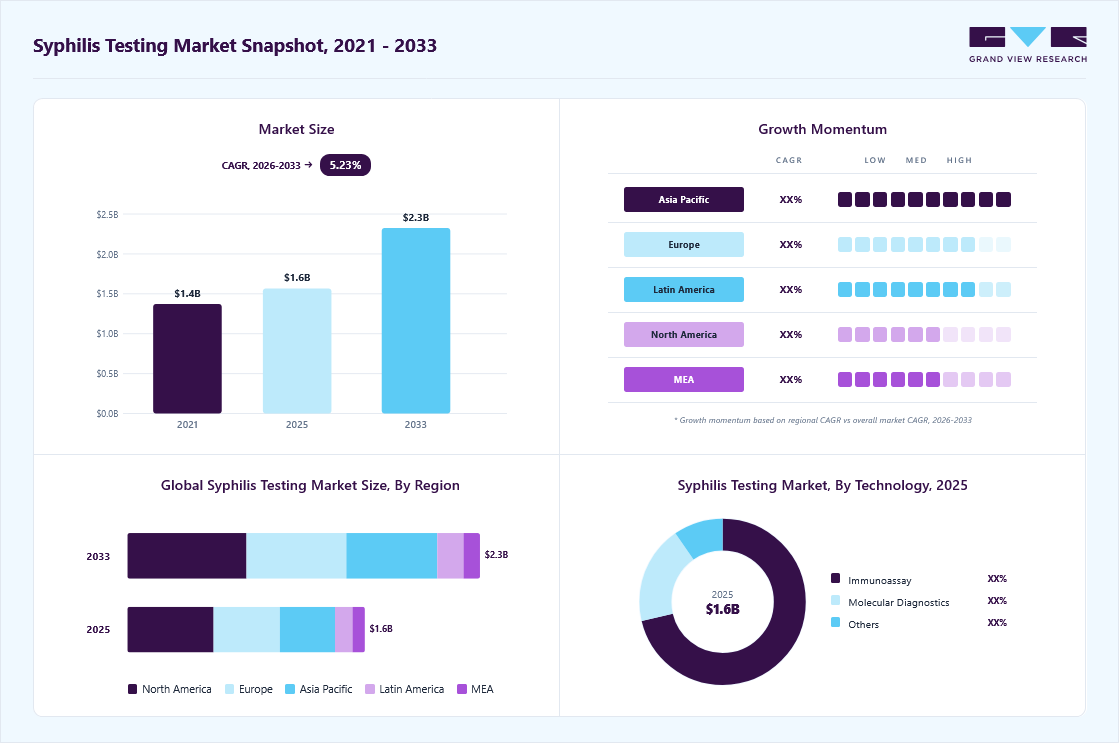

The global syphilis testing market size was valued at USD 1.5 billion in 2025 and is projected to grow from USD 1.6 billion in 2026 to USD 2.3 billion by 2033, at a CAGR of 5.2% from 2026 to 2033. The North America syphilis testing market held the largest share of 36.32% of the global market in 2025. Key market drivers for dual HIV/syphilis rapid diagnostics include the rising global burden of congenital syphilis and HIV co-infections, which continue to cause significant adverse pregnancy outcomes.

Key Market Trends & Insights

- By technology: Immunoassay segment led the market with the largest revenue share of 71.2% in 2025.

- By technology: Molecular diagnostics segment is anticipated to grow at the fastest CAGR during the forecast period.

- By location of testing: Laboratory testing segment led the market with the largest revenue share of 79.5% in 2025.

Regional Highlights

- Largest regional market: North America (36.32% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The syphilis testing industry in the U.S. held the largest revenue share in North America in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.5 Billion

- Estimated market size in 2026: USD 1.6 Billion

- Projected market size by 2033: USD 2.3 Billion

- CAGR (2026-2033): 5.2%

Syphilis, once considered a disease of the past, has reemerged as a significant public health and market concern in North America and globally.While the widespread use of penicillin in the mid-20th century had nearly eliminated syphilis in high-income countries, recent years have seen a sharp resurgence. In the U.S., reported cases increased by more than 80% between 2018 and 2022, rising from approximately 115,000 to over 207,000-the highest level since the 1950s. Of particular concern is congenital syphilis, which grew by 183% during the same period, reflecting gaps in maternal screening and early intervention.

")

In Canada, rising incidence in the Prairie provinces and northern territories-particularly among Indigenous populations further highlights disparities in access to timely diagnostics and treatment. These epidemiological shifts are creating heightened demand for innovative diagnostic solutions, decentralized testing models, and scalable public health interventions, positioning the infectious disease diagnostics market for accelerated growth.

Market Dynamics

The rising global prevalence of syphilis is significantly driving demand for syphilis testing worldwide. According to the World Health Organization report published on 29 May 2025, nearly 8 million adults aged 15-49 acquired syphilis, while active syphilis prevalence remained close to 0.6% globally. Persistent transmission and untreated infections continue to increase the need for routine screening and confirmatory diagnostics. Congenital syphilis also remains a major public health concern, causing approximately 355,000 adverse pregnancy outcomes annually, including stillbirths and neonatal deaths. These trends are accelerating the adoption of prenatal screening, rapid testing technologies, and public health surveillance programs across both developed and developing healthcare systems globally.

The U.S. is witnessing a significant rise in maternal and congenital syphilis cases, contributing to higher demand for prenatal and confirmatory diagnostic testing. According to a recent national health statistics report published in January 2026, the maternal syphilis rate increased from 280.4 per 100,000 births in 2022 to 357.9 in 2024, reflecting an approximately 28% increase over two years. The burden has risen sharply among high-risk populations, including American Indian and Alaska Native, Hispanic, and Black Non-Hispanic mothers. Increasing maternal infections are contributing to sustained growth in congenital syphilis cases, reinforcing the need for routine prenatal screening, rapid point-of-care diagnostics, and timely laboratory confirmation. These epidemiological trends are encouraging healthcare providers and public health agencies to strengthen early detection programs, expand access to decentralized testing, and increase adoption of automated immunoassay platforms to reduce adverse pregnancy outcomes and long-term disease complications.

Emerging economies are also experiencing a substantial syphilis burden, further supporting market growth. Sub-Saharan Africa continues to report some of the highest infection rates globally, with syphilis affecting up to 3%-9% of pregnant women in certain countries. China has similarly recorded rising incidence rates over the past decade, highlighting growing public health concerns associated with sexually transmitted infections. Increasing disease prevalence across these regions is strengthening demand for affordable point-of-care diagnostics, laboratory-based screening, and dual HIV/syphilis testing platforms. Government-led sexually transmitted infection control initiatives, maternal health programs, and expanding healthcare access are collectively supporting higher testing adoption and long-term growth of the syphilis testing industry globally.

Growing emphasis on elimination of mother-to-child transmission (EMTCT) programs by the WHO and national health bodies is creating strong demand for cost-effective, point-of-care solutions. Regulatory approvals, such as Health Canada’s clearance of MedMira’s Multiplo Rapid TP/HIV Test, and partnerships, such as CHAI-MedAccess-SD Biosensor, are accelerating adoption by ensuring affordability and accessibility. In addition, the push for decentralized testing in rural and underserved regions supports uptake, while technological improvements in accuracy and speed enhance market confidence.

Limited access to advanced diagnostic infrastructure remains a major restraint affecting the market growth. Despite advancements in diagnostic technologies, syphilis detection continues to rely heavily on antibody-based assays that cannot reliably distinguish active infection from previously treated diseases. As a result, healthcare providers often rely on multi-step testing algorithms that combine screening and confirmatory assays, thereby increasing turnaround time and the risk of delayed diagnosis or patient loss to follow-up. These challenges are particularly significant in decentralized healthcare systems, rural settings, and low-resource regions, where laboratory capacity, trained personnel, and access to confirmatory testing remain limited.

The market is further constrained by structural weaknesses in public health infrastructure and in the accessibility of treatment. Syphilis management remains highly dependent on benzathine penicillin G formulations such as Bicillin L-A, which have experienced recurring supply shortages due to a limited global manufacturing base. At the same time, the absence of a licensed vaccine continues to place substantial pressure on screening programs, partner notification efforts, and early disease detection initiatives. In several countries, public health funding limitations and workforce shortages have weakened sexually transmitted infection surveillance and testing capacity. Rural and underserved populations often face restricted laboratory access, delayed follow-up testing, and inadequate prenatal screening services, reducing timely diagnosis and treatment rates.

Although regulatory and public health initiatives are supporting gradual improvement, infrastructure disparities continue to limit large-scale testing adoption. Expanding use of at-home testing solutions, rapid diagnostic assays, and community-integrated screening programs is improving accessibility in certain regions. In addition, investments supporting confirmatory diagnostics, maternal screening initiatives, and decentralized healthcare delivery models are helping strengthen disease detection capabilities. However, inconsistent healthcare infrastructure, limited reimbursement support in some markets, and unequal access to laboratory networks continue to hinder widespread implementation of advanced syphilis testing solutions, particularly across low-income and geographically remote regions.

The expansion of point-of-care and at-home syphilis testing presents a major growth opportunity for the global market, particularly as rising infection rates increase the need for faster and more accessible screening solutions. Healthcare systems are increasingly adopting rapid diagnostic technologies that deliver results during a single patient visit, helping reduce treatment delays and patient loss to follow-up. This opportunity is especially important in prenatal screening programs, sexually transmitted infection clinics, and community health centers, where early diagnosis is critical for preventing congenital syphilis transmission. Growing demand for decentralized testing is encouraging manufacturers to develop portable, easy-to-use, and highly sensitive rapid immunoassays and dual HIV/syphilis testing platforms.

Regulatory approvals and product innovations are further accelerating market opportunities. In August 2024, NOWDiagnostics received U.S. Food and Drug Administration authorization for the First To Know Syphilis Test, the first over-the-counter at-home syphilis antibody test approved in the U.S. The test delivers results within approximately 15 minutes using a fingerstick blood sample, enabling individuals to perform initial syphilis screening privately at home without a prescription. The approval represents a major advancement in decentralized sexually transmitted infection diagnostics and is expected to improve early screening uptake among high-risk and underserved populations. The authorization also establishes a regulatory pathway for future consumer-accessible syphilis diagnostic products, supporting broader adoption of at-home and rapid testing technologies within the syphilis testing industry.

Market Concentration & Characteristics

Innovation is reshaping dual rapid testing, with companies like MedMira launching the Multiplo Rapid TP/HIV Test, capable of detecting both HIV-1/2 and syphilis antibodies from a single finger-prick with 100% HIV accuracy and 98% syphilis accuracy. Already deployed in Europe and Colombia and recently approved by Health Canada (Dec 2024), such devices offer immediate results without refrigeration. This innovation supports decentralized care, bridges gaps in underserved communities, and advances EMTCT goals.

M&A and collaborations are driving accessibility and affordability. For instance, in November 2021, MedAccess, CHAI, and SD Biosensor formed a partnership to distribute the STANDARD Q HIV/Syphilis Combo Test at under US$1 across 100+ LMICs. While outright acquisitions are moderate, such global collaborations mirror consolidation effects, enabling scale, affordability, and distribution synergies. Larger diagnostics firms are expected to target similar partnerships or acquisitions to strengthen infectious disease testing portfolios.

Regulation remains a catalyst, shaping adoption and market entry. Health Canada’s approval (Dec 2024) of MedMira’s dual test followed a 1,500+ subject clinical study in Alberta (2020-2022) co-led by top institutions, ensuring credibility. Similarly, the WHO prequalification of SD Biosensor’s STANDARD Q combo test allowed procurement by donor-funded programs in LMICs. Such regulatory endorsements reduce market hesitancy, ensure compliance with global EMTCT strategies, and create strong differentiation for approved products.

Substitution risk exists but remains manageable. Traditional ELISA and PCR assays deliver gold-standard accuracy but are limited by infrastructure requirements and slower turnaround times. Rapid combo tests, like MedMira’s Multiplo and SD Biosensor’s STANDARD Q, provide point-of-care results in under 20 minutes at a fraction of the cost. However, emerging HIV self-tests and multiplex molecular platforms could act as substitutes. To maintain an edge, rapid test developers emphasize affordability (e.g., 32% price cut via CHAI-MedAccess) and ease of use.

End-users are highly concentrated in public health agencies, NGOs, and maternal health programs. For example, the CHAI-MedAccess-SD Biosensor partnership directly targets antenatal care in 100+ LMICs, aligning with WHO EMTCT goals. In high-income regions, adoption depends on government approvals, as seen with Health Canada’s 2024 clearance enabling rollout in Canadian hospitals and clinics. Indigenous populations in Canada’s Prairie provinces, experiencing disproportionately higher infection rates, highlight the need for targeted community health programs.

Technology Insights

The immunoassay segment led the market with the largest revenue share of 71.20% in 2025. Its dominance stems from widespread clinical adoption, established use in hospital laboratories, cost-effectiveness, and compatibility with high-throughput platforms. Immunoassays, including ELISA and chemiluminescent assays, are considered the gold standard for antibody detection, particularly in confirmatory testing. Their strong regulatory acceptance and extensive integration into public health programs further consolidate market leadership.

The molecular diagnostics segment is anticipated to grow at the fastest CAGR during the forecast period, driven by rising demand for early, highly sensitive detection of infections. PCR and next-generation sequencing (NGS)-based tools are gaining traction, particularly in monitoring viral load, resistance mutations, and detecting low-titer infections that may be missed by serology. Growth is accelerated by decentralization trends, falling costs of molecular platforms, and integration into point-of-care and multiplex assays. These attributes make molecular diagnostics critical in addressing gaps left by traditional methods, particularly in mother-to-child transmission screening and high-burden geographies.

Location of Testing Insights

The laboratory-based testing segment led the market with the largest revenue share of 79.56% in 2025, owing to its entrenched role as the clinical gold standard. Centralized laboratories and hospital-based diagnostic centers rely heavily on automated immunoassays, ELISAs, and confirmatory treponemal/non-treponemal workflows that ensure high accuracy and consistency. These platforms support high-volume testing, making them particularly valuable in national screening initiatives and prenatal care programs where reliability is paramount.

In the United States, laboratory giants such as Quest Diagnostics and LabCorp have built extensive syphilis testing infrastructure, often bundled with comprehensive STD panels that streamline testing workflows for clinicians. In Canada, providers such as LifeLabs and provincial public health labs dominate, integrating syphilis testing into routine sexual health and antenatal programs. Laboratories also benefit from established reimbursement pathways and integration with electronic medical records (EMRs), reinforcing their central role in healthcare systems.

Despite the growth of decentralized alternatives, laboratories continue to maintain their dominance because of their unmatched ability to handle confirmatory testing, complex case management, and integration with advanced molecular diagnostics. Particularly for high-risk populations and congenital syphilis investigations, laboratory workflows remain essential for providing definitive results.

The point-of-care (POC) testing segment is anticipated to grow at the fastest CAGR during the forecast period, reflecting shifting public health priorities toward accessibility, speed, and patient-centered care. The surge in congenital syphilis, which demands immediate detection and treatment, has highlighted the limitations of lab-centric models that rely on multiple visits and long turnaround times. In response, both regulators and companies are accelerating the adoption of rapid and at-home testing solutions.

A landmark example is Health Canada’s approval (December 2024) of MedMira’s Multiplo Rapid TP/HIV Test, a dual-purpose finger-prick device that delivers near-instant results for both HIV and syphilis, with no special storage requirements. Already in use across Europe and Colombia, the device is now positioned to close diagnostic gaps in both urban hospitals and remote Canadian communities. Similarly, in August 2024, the U.S. FDA authorized NOWDiagnostics’ First To Know Syphilis Test through the De Novo pathway, marking the first over-the-counter syphilis diagnostic available for at-home use. This regulatory milestone not only enables consumer-driven testing but also establishes a precedent for other developers to bring innovative syphilis POC solutions to market.

POC solutions are particularly critical in Indigenous and underserved communities across North America, where access to centralized laboratories is limited and travel times are prohibitive. Mobile outreach programs in regions like the Navajo Nation in the U.S. and Prairie provinces in Canada are leveraging these rapid devices to deliver same-day testing and treatment, reducing loss to follow-up.

Globally, WHO-endorsed dual HIV/syphilis combo tests, such as the STANDARD Q (SD Biosensor) supplied under the CHAI-MedAccess partnership, are further demonstrating the role of POC platforms in advancing elimination of mother-to-child transmission (EMTCT) targets. As syphilis rates rise, the market is shifting toward hybrid models, where centralized labs maintain their dominance for confirmatory and large-scale screening, while POC testing grows rapidly as a frontline solution to improve accessibility, equity, and speed of diagnosis.

Regional Insights

North America dominated the global syphilis testing market with the largest revenue share of 36.32% in 2025. The U.S. drives this leadership through high testing volumes at Quest Diagnostics, Labcorp, and public health laboratories, where syphilis is included in comprehensive STD panels. Recent FDA clearances of innovative diagnostics, such as NOWDiagnostics’ at-home syphilis test, are expanding access and creating a consumer-directed market. In Canada, LifeLabs and provincial health authorities emphasize antenatal screening and community outreach programs, particularly in the Prairie provinces. Growing congenital syphilis rates and strong federal funding continue to fuel demand across both laboratory and point-of-care channels.

U.S. Syphilis Testing Market Trends

The syphilis testing market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by a sharp epidemiologic rebound-reported cases rose ~80% from 2018-2022-plus major policy and regulatory responses. The FDA’s August 2024 De Novo authorization for NOWDiagnostics’ at-home antibody test created an OTC consumer testing channel, while NIH investments ($2.4M in 2024; $2.7M in 2025 grants) are accelerating next-gen molecular and electrochemical POC diagnostics. Implementation models (e.g., University of Chicago ED opt-in screening; Navajo Nation mobile outreach) emphasize decentralized testing and same-day treatment to reduce loss to follow-up. Persistent challenges-Bicillin L-A shortages, declining CDC STD prevention funding, and congenital syphilis spikes-sustain demand for rapid, confirmatory, and field-deployable tests.

Europe Syphilis Testing Market Trends

The syphilis testing market in Europe is shaped by growing incidence and strong national health systems prioritizing targeted screening. The UK and Germany report steady case increases, prompting expansion of free sexual health services and antenatal programs. Laboratories dominate with automated immunoassays, while CE-marked rapid tests are used in community clinics. Digital integration into public health networks improves surveillance and contact tracing. Procurement remains cost-sensitive, requiring suppliers to deliver value-driven pitches. Future growth is likely through dual HIV/syphilis rapid tests in antenatal care, and enhanced use of digital reporting platforms. Strong regulation and robust reimbursement systems create barriers but ensure market stability.

The UK syphilis testing market shows modest upticks in syphilis diagnoses (early-stage cases: 9,535 in 2024 vs 9,375 in 2023; overall cases 13,030 vs 12,456). Public programs emphasize free, confidential testing and targeted messaging to high-risk groups (MSM, young adults). Policy momentum-NHS rollout of gonorrhea vaccination programs-illustrates prevention orientation, while surveillance highlights rising antibiotic resistance in gonorrhea. Market opportunities center on integrated sexual-health POC devices and digital linkage-to-care solutions. Buyers favor validated rapid dual tests for antenatal screening and community clinics; regulatory acceptance and NHS procurement cycles will determine commercial scale-up.

The syphilis testing market in Germany accounted for a significant share of the European market in 2025. The syphilis landscape mirrors broader EU increases in bacterial STIs; testing and genomic surveillance (WGS) are expanding to track resistant strains. Clinical laboratories remain primary purchasers, using automated immunoassays for screening and molecular techniques for complex cases. Growing public-health focus on MSM and young adult engagement, plus improved surveillance, is creating demand for rapid POC diagnostics in sexual-health clinics and outreach programs. Vendors that combine high sensitivity with integration into municipal public health reporting and partner notification workflows will find traction as Germany scales targeted screening and antimicrobial resistance monitoring.

Asia Pacific Syphilis Testing Market Trends

The syphilis testing market in the Asia Pacific is projected to grow at the fastest CAGR over the forecast period. Asia-Pacific presents diverse dynamics, with China and Japan leading in laboratory-based immunoassays and antenatal screening, while Southeast Asia emphasizes cost-effective rapid testing. Rising incidence, urbanization, and maternal health programs drive demand. China’s provincial procurement favors high-volume labs and WHO-prequalified dual tests, while Japan expands targeted syphilis clinics but requires rigorous validation for new technologies. In lower-income countries, donor-driven programs supply affordable rapid kits for maternal health. Market opportunities lie in combining rapid testing with digital follow-up to ensure timely treatment. Strategic partnerships and localized regulatory alignment are critical for success in this fragmented yet high-growth regional market

The China syphilis testing market is characterized by expanding laboratory capacity and rapid scale-up of point-of-care screening in urban and provincial health systems. National antenatal screening initiatives and rising STI surveillance drive demand for affordable dual HIV/syphilis rapid assays, lab immunoassays, and molecular confirmatory tests. Manufacturers that offer WHO-aligned, low-cost combo tests and scalable platforms can access procurement through provincial health networks. Challenges include bridging urban-rural access gaps and ensuring confirmatory lab follow-through; opportunities exist to integrate POC testing with telemedicine and maternal health programs.

The syphilis testing market in Japan is anticipated to grow at a significant CAGR during the forecast period.Japan has responded to localized outbreaks-Tokyo reported 3,667 syphilis cases in 2022 (a 50% rise from 2021)-by expanding testing access (extended clinic hours, holiday/Sunday services) and pairing syphilis with HIV screening. The market is conservative, favoring laboratory immunoassays for confirmatory diagnosis, but authorities are piloting POC expansions to improve early detection in young adults. Vendors should prioritize regulatory compliance, clinician education, and demonstration projects tied to prenatal care; culturally sensitive outreach and anonymity-preserving distribution channels will support uptake among younger and stigmatized populations.

Latin America Syphilis Testing Market Trends

The syphilis testing market in Latin America is anticipated to grow at a substantial CAGR during the forecast period. Latin America, led by Brazil, prioritizes syphilis testing within maternal and child health programs due to high congenital syphilis rates. Public procurement dominates, with Ministries of Health sourcing WHO-prequalified dual HIV/syphilis tests for antenatal care. Laboratories remain important for confirmatory testing, but POC diagnostics in community clinics are increasingly adopted to enable same-visit treatment initiation. Brazil’s federal health system purchases at scale, driving strong demand for affordable, reliable supply chains. The region’s price sensitivity favors cost-effective solutions, and partnerships with local distributors and NGOs are essential. Demonstrating improved maternal outcomes is key to sustained growth and procurement renewals.

The Brazil syphilis testing market is growing at a rapid pace. Brazil’s public health priorities emphasize antenatal screening and reducing congenital syphilis, creating sizable demand for dual HIV/syphilis rapid tests and low-cost POC kits. Regional initiatives and NGO partnerships (mirrored by CHAI/MedAccess/SD Biosensor models) have created price-sensitive procurement channels across LMICs. Large public purchasers (Ministry of Health, regional health secretariats) prioritize WHO-prequalified products that enable on-site testing in primary care and maternity clinics. Vendors that can combine cost competitiveness, supply reliability, and integration with prenatal programs will be well-positioned to scale across Brazil and neighboring markets.

Middle East and Africa Syphilis Testing Market Trends

The syphilis testing market in the Middle East and Africa is expected to grow significantly during the forecast period. In Africa, syphilis remains a major driver of adverse birth outcomes ~11% of stillbirths are attributable to syphilis, so maternal screening is a key market. WHO and donor-funded procurement drive uptake of low-cost, WHO-prequalified combo tests (e.g., STANDARD Q). Infrastructure constraints favor POC and rapid combo diagnostics that do not require cold chain or complex lab infrastructure. In the Middle East, markets are heterogeneous: wealthier GCC countries invest in lab and molecular capacity, while low-resource countries rely on NGO and donor programs. Scalability depends on procurement frameworks, donor support, and local capacity-building.

The Saudi Arabia syphilis testing market is anticipated to grow at a significant CAGR during the forecast period. Saudi Arabia’s health system emphasizes centralized lab capacity and antenatal screening in public hospitals; demand for high-quality immunoassays and confirmatory molecular testing remains strong. At the same time, Gulf Cooperation Council (GCC) initiatives and private hospitals are open to rapid POC solutions for screening travelers, migrant worker clinics, and perinatal care. Market entry requires regulatory clearance, adherence to national procurement, and partnerships with major hospital groups. Opportunities exist for accredited dual HIV/syphilis rapid tests that meet Saudi regulatory standards and can be deployed in maternal health and occupational-health screening programs.

Key Syphilis Testing Company Insights

Market leaders are engaged in extensive R&D to develop technologically advanced, cost-efficient testing products. Besides, several organizations are incorporating strategies such as mergers & acquisitions to expand their market presence and are anticipated to create significant growth opportunities over the forecast period. For instance, in May 2023, Charles Thermo Fisher Scientific, Inc. entered into a partnership with Pfizer Inc. to enhance the availability of localized access to next-generation sequencing-based testing for cancer patients in international markets.

Key Syphilis Testing Companies:

The following key companies have been profiled for this study on the syphilis testing market.

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd.

- Bio-Rad Laboratories, Inc.

- Siemens Healthineers AG

- Danaher Corporation (Beckman Coulter)

- Thermo Fisher Scientific Inc.

- bioMérieux SA

- OraSure Technologies, Inc.

- Chembio Diagnostics, Inc.

- SD Biosensor, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Player: Abbott

- Matured players focus on scale-driven operations, leveraging large installed laboratory platforms, automated immunoassay and molecular systems, and long-term contracts with hospitals and reference labs. Their strategy emphasizes menu expansion, regional regulatory compliance, and integrating syphilis testing into broader infectious disease panels to drive recurring reagent revenues.

- Their key strengths lie in global brand recognition, extensive regulatory approvals, strong distribution networks, and deep R&D resources. High-throughput systems enable cost efficiency and reliability, while bundled test menus increase customer lock-in. These players benefit from established trust among clinicians and laboratories, allowing them to dominate centralized laboratory-based syphilis testing volumes.

- Mature players often face slower innovation cycles, higher product costs, and limited agility in responding to decentralized or home-based testing demand. Their reliance on centralized laboratories makes them less competitive in point-of-care and OTC settings. In addition, large organizational structures can delay market responses to emerging public health needs and to price-sensitive markets.

Emerging Player: OraSure Technologies Inc.

- Emerging players prioritize agility, focusing on rapid, point-of-care, and decentralized syphilis testing solutions. Their operations are optimized for speed-to-market, public health tenders, and partnerships with NGOs and governments. They emphasize affordability, ease of use, and accessibility, particularly in low-resource settings and community-based screening programs.

- Their competitive advantage lies in innovation, flexible manufacturing, and strong alignment with global health priorities. Many offer rapid or dual HIV/syphilis tests, lower pricing, and WHO prequalification. These players excel at reaching underserved populations and at adapting quickly to evolving testing needs, giving them strong growth potential despite a smaller market presence.

- Emerging players face challenges such as limited global distribution, lower brand recognition in developed markets, and dependence on public-sector funding. Regulatory approvals can be resource-intensive, and scaling production consistently remains a risk. They may also lack the comprehensive test menus and long-term customer contracts that support sustained revenue stability.

Recent Developments

-

In August 2024, the U.S. FDA authorized the First To Know Syphilis Test by NOWDiagnostics, Inc., the first over-the-counter, at-home syphilis antibody test. Using a finger-stick blood sample, it delivers results in 15 minutes, similar to pregnancy or COVID-19 home tests. Although it cannot differentiate between past and active infections, its approval via the De Novo pathway reflects regulatory recognition of urgent public health needs. This milestone lowers barriers for consumer-focused diagnostics and sets a precedent for rapid, accessible syphilis testing. Enabling at-home testing, it expands early detection, reduces transmission, and empowers individuals to seek timely care.

-

In March 2025, in Canada, the Canadian Institutes of Health Research (CIHR), in partnership with Indigenous leaders, established the Ayaangwaamiziwin Center, a $7 million Indigenous-led initiative to combat syphilis in Prairie and northern communities. The program delivers culturally safe testing, treatment, and community-based care, addressing disproportionately high infection rates among Indigenous populations. By embedding community leadership and culturally appropriate approaches, it reduces barriers to access, improves follow-up adherence, and enhances trust in healthcare interventions. The initiative integrates modern diagnostics with mobile outreach strategies and local engagement, serving as a model for equitable public health interventions targeting vulnerable populations in both rural and urban settings.

Syphilis Testing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.5 billion

Estimated market size in 2026

USD 1.6 billion

Projected market size by 2033

USD 2.3 billion

Growth rate

CAGR of 5.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Number of Tests in Million, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology, location of testing, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Sweden; Denmark; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Abbott Laboratories; F. Hoffmann-La Roche Ltd.; Bio-Rad Laboratories, Inc.; Siemens Healthineers AG; Danaher Corporation (Beckman Coulter); Thermo Fisher Scientific Inc.; bioMérieux SA; OraSure Technologies, Inc.; Chembio Diagnostics, Inc.; SD Biosensor, Inc.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Syphilis Testing Market Report Segmentation

This report forecasts revenue growth and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global syphilis testing market based on technology, location of testing, cancer type, function, and region:

-

Technology Outlook (Number of Tests in Million; Revenue, USD Million, 2021 - 2033)

-

Molecular Diagnostics

-

Immunoassay

-

Others

-

-

Location of Testing Outlook (Number of Tests in Million; Revenue, USD Million, 2021 - 2033)

-

Laboratory Testing

-

Commercial/Private labs

-

Public Health Labs

-

-

Point of Care Testing

-

-

Regional Outlook (Number of Tests in Million; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-matrix analysis across testing type, end user, and geography

Developed a comprehensive cross-matrix integrating testing modality (treponemal, non-treponemal, rapid tests, molecular assays), end users (hospitals, diagnostic laboratories, blood banks, clinics), and regional adoption trends.

Enabled identification of high-growth testing segments and unmet diagnostic demand areas across healthcare settings.

Comparative benchmarking of rapid tests versus laboratory-based assays

Conducted side-by-side assessment of rapid diagnostic tests, ELISA, RPR/VDRL, chemiluminescence assays, and molecular testing workflows across sensitivity, specificity, turnaround time, scalability, and cost efficiency.

Supported evaluation of technology transition trends and platform prioritization strategies

Competitive benchmarking of syphilis diagnostic manufacturers

Benchmarked global and regional companies based on product portfolio, pricing, regulatory approvals, distribution networks, innovation pipeline, and point-of-care capabilities.

Enabled strategic positioning and competitor differentiation planning.

Workflow transition analysis from centralized to decentralized testing

Evaluated the migration trend from laboratory-based testing toward decentralized and point-of-care syphilis diagnostics across hospitals, clinics, and community healthcare settings.

Highlighted opportunities in rapid testing expansion and decentralized diagnostic adoption.

Frequently Asked Questions About This Report

North America dominated with a 36.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The laboratory-based testing segment led with a 79.6% revenue share in 2025, while the point-of-care (POC) testing is the fastest-growing segment.

The immunoassay segment currently holds the largest share of 71.2% in 2025. Its dominance stems from widespread clinical adoption, established use in hospital laboratories, cost-effectiveness, and compatibility with high-throughput platforms. Immunoassays, including ELISA and chemiluminescent assays, are considered the gold standard for antibody detection, particularly in confirmatory testing. Their strong regulatory acceptance and extensive integration into public health programs further consolidate market leadership.

Key players include Abbott Laboratories; F. Hoffmann-La Roche Ltd.; Bio-Rad Laboratories, Inc.; Siemens Healthineers AG; Danaher Corporation (Beckman Coulter); Thermo Fisher Scientific Inc.; bioMérieux SA; OraSure Technologies, Inc.; Chembio Diagnostics, Inc.; SD Biosensor, Inc.

Key market drivers for dual HIV/syphilis rapid diagnostics include the rising global burden of congenital syphilis and HIV co-infections, which continues to cause significant adverse pregnancy outcomes. Growing emphasis on elimination of mother-to-child transmission (EMTCT) programs by WHO and national health bodies is creating strong demand for cost-effective, point-of-care solutions. Regulatory approvals, such as Health Canada’s clearance of MedMira’s Multiplo Rapid TP/HIV Test, and partnerships like CHAI–MedAccess–SD Biosensor, are accelerating adoption by ensuring affordability and accessibility.

The global syphilis testing market size was valued at USD 1.5 billion in 2025 and is estimated at USD 1.6 billion for 2026.

The global syphilis testing market is expected to grow at a CAGR of 5.2% from 2026 to 2033, reaching USD 2.3 billion by 2033.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.