- Home

- »

- Power Generation & Storage

- »

-

Train Battery Market Size, Share & Growth Report 2026-2033GVR Report cover

![Train Battery Market Size, Share & Trends Report]()

Train Battery Market (2026 - 2033) Size, Share & Trends Analysis Report By Type (Lead Acid Battery, Lithium Ion Battery), By Technology (Conventional Lead Acid Battery, Valve Regulated Lead Acid Battery), By Application (Metros, High-speed Trains), By Region, And Segment Forecasts

Market Size, 2025

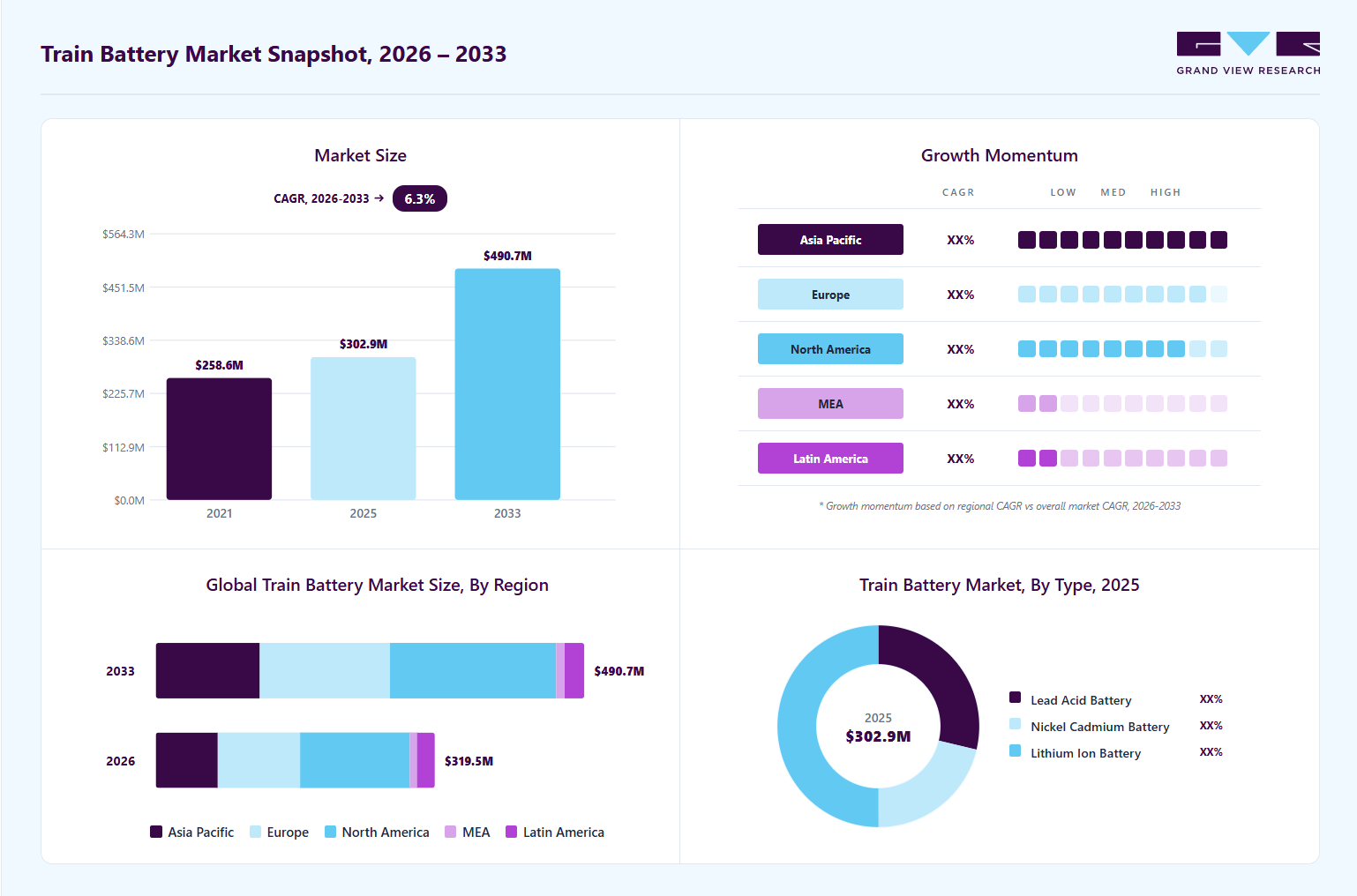

$302.9MMarket Estimate, 2026

$318.5MMarket Forecast, 2033

$490.7MCAGR, 2026–2033

8.3%Train Battery Market Summary

The global train battery market size was valued at USD 302.90 million in 2025 and is projected to grow from USD 319.53 million in 2026 to USD 490.73 million by 2033, at a CAGR of 6.3% from 2026 to 2033. North America dominated the global market with the largest revenue share of 39.41% in 2025. The global market is primarily driven by increasing investments in railway electrification, modernization of passenger and freight rail fleets, and the growing adoption of battery-powered and hybrid train technologies.

Key Market Trends & Insights

- The train battery industry in the U.S. is expected to grow at a CAGR of 5.9% from 2026 to 2033.

- In 2025, the lithium ion battery type segment accounted for the largest revenue share of 50.03%.

- By technology, valve regulated lead acid battery segment captured the largest revenue share of 35.67% in 2025.

- Based on application, high-speed trains segment is expected to grow at the fastest CAGR of 11.4% from 2026 to 2033.

Market Size & Forecast

- 2025 Market Size: USD 302.90 Million

- 2026 Market Size: USD 319.53 Million

- 2033 Projected Market Size: USD 490.73 Million

- CAGR (2026-2033): 6.3%

- North America: Largest market in 2025

- Asia Pacific: Fastest growing market

Rising demand for reliable auxiliary power, backup energy systems, and energy-efficient rail operations, coupled with government initiatives aimed at reducing transportation emissions and promoting sustainable mobility, is further supporting market growth. In addition, advancements in battery technology and expanding metro, light rail, and high-speed rail networks are accelerating the deployment of train batteries worldwide.")

The increasing adoption of battery-powered and hybrid rail transportation presents a major growth opportunity for the train battery industry. Train batteries are increasingly being utilized for propulsion support, auxiliary power systems, signaling, emergency backup, and onboard energy storage applications due to their ability to improve energy efficiency, reduce emissions, and support sustainable rail operations. Rising investments in railway electrification, fleet modernization programs, and advanced battery technologies are expected to create significant long-term revenue opportunities for market participants. Growing deployment of metro systems, high-speed rail networks, and battery-electric trains across developed and emerging economies is further accelerating demand for reliable and high-performance train battery solutions.

High capital investment requirements associated with advanced battery technologies, charging infrastructure, system integration, and battery replacement remain a key challenge for the train battery industry. In addition, fluctuations in raw material prices, supply chain disruptions, and dependence on critical minerals such as lithium, nickel, and cobalt can affect manufacturing costs and profitability. Stringent safety requirements, battery disposal concerns, and competition from alternative rail electrification technologies may further restrain market expansion.

Market Dynamics

The growing focus on railway electrification and sustainable transportation is emerging as a major driver for the global train battery industry. Governments, railway operators, and transit authorities are increasingly adopting battery-based energy storage solutions to reduce carbon emissions, improve operational efficiency, and support low-emission mobility goals. This transition is accelerating investments in advanced battery systems, rail infrastructure modernization, and battery-powered train technologies to deliver cleaner and more efficient transportation solutions. Supportive policy frameworks, transportation decarbonization targets, public transit investments, and railway modernization programs are further strengthening the commercial viability of train battery deployments globally.

The passenger rail, metro, and high-speed rail sectors are witnessing increasing adoption of advanced batteries for auxiliary power, emergency backup, and hybrid propulsion applications due to their reliability, efficiency, and ability to reduce dependence on diesel-powered systems. Urban transit networks are also integrating modern battery technologies to enhance operational flexibility and energy management. As a result, battery manufacturers, rail technology providers, and transportation authorities are expanding production capabilities, strengthening supply chains, and investing in next-generation battery innovations, driving significant growth across the train battery ecosystem.

Fluctuations in the availability and pricing of critical battery materials remain a significant restraint for the global train battery industry. Many manufacturers continue to face challenges associated with sourcing lithium, nickel, cobalt, and other key raw materials, which can impact production costs, supply stability, and long-term procurement strategies. Supply chain disruptions, geopolitical uncertainties, and evolving environmental regulations further restrict efficient market expansion across several regions.

The dependence on complex battery manufacturing processes and global supply networks can reduce the economic feasibility of large-scale train battery deployments. Market participants also face challenges related to battery lifecycle management, recycling requirements, safety compliance, and technology upgrade costs, which may delay investment decisions and project implementation. As a result, supply-side constraints and cost pressures continue to influence the long-term growth trajectory of the global train battery industry.

Type Insights

The lithium ion battery segment dominated the market with the largest revenue share of 50.03% in 2025 due to its high energy density, lightweight design, long service life, and superior charging efficiency compared to conventional battery technologies. Increasing adoption of battery-powered and hybrid trains, growing investments in railway electrification, and rising demand for reliable onboard energy storage systems have significantly boosted the deployment of lithium-ion batteries across passenger, freight, metro, and high-speed rail applications. In addition, continuous advancements in battery performance, safety, and lifecycle management have further strengthened the segment’s leading market position.

The nickel-cadmium (Ni-Cd) batteries segment is expected to grow at the fastest CAGR of 4.3% from 2026 to 2033 driven by their high reliability, long operational life, and ability to perform effectively under extreme temperatures and demanding railway environments. Ni-Cd batteries are widely used in critical rail applications such as emergency backup power, signaling systems, and onboard auxiliary functions where durability and operational safety are essential. Continued investments in rail infrastructure modernization and the replacement of aging battery systems in existing train fleets are expected to support steady demand for Ni-Cd batteries over the forecast period.

Technology Insights

The valve regulated lead acid battery segment captured the largest revenue share of 35.67% in 2025 due to its proven reliability, low maintenance requirements, cost-effectiveness, and widespread use in railway applications. VRLA batteries are extensively deployed in starting, lighting, ignition (SLI), signaling, emergency backup, and auxiliary power systems owing to their robust performance, long service life, and ability to operate under demanding rail conditions. Their established adoption across passenger trains, freight locomotives, metro systems, and rail infrastructure has continued to support the segment's dominant market position.

The lithium titanate oxide (LTO) segment is expected to grow at the fastest CAGR of 19.2% from 2026 to 2033 driven by its superior safety profile, ultra-fast charging capabilities, long cycle life, and excellent performance under extreme temperature conditions. These advantages make LTO batteries highly suitable for modern rail applications, including battery-powered trains, hybrid locomotives, and rapid-transit systems that require frequent charging and high operational reliability. Growing investments in advanced railway electrification projects and increasing demand for durable, high-performance energy storage solutions are expected to further accelerate the adoption of LTO batteries across the train industry.

Application Insights

The metros segment captured the largest revenue share of 37.95% in 2025 due to the widespread expansion of urban transit networks, increasing investments in metro rail infrastructure, and growing demand for reliable onboard power systems. Metro trains require advanced battery solutions for auxiliary power, emergency backup, signaling, lighting, and operational safety systems. Rapid urbanization, rising passenger traffic, and government initiatives to promote efficient and sustainable public transportation have further accelerated the deployment of battery technologies across metro rail networks, supporting the segment's leading market position.

The high speed trains segment is expected to grow at the fastest CAGR of 11.4% from 2026 to 2033 driven by increasing investments in high-speed rail infrastructure, rising demand for efficient long-distance transportation, and ongoing modernization of rail fleets. Governments across Asia Pacific, Europe, and the Middle East are expanding high-speed rail networks to reduce road congestion and lower transportation emissions, creating strong demand for advanced battery systems used in auxiliary power, backup energy storage, and onboard operational functions. In addition, advancements in battery technology and the growing focus on energy-efficient rail operations are expected to further accelerate segment growth during the forecast period.

Regional Insights

North America Train Battery Market Trends

North America train battery industry held the largest revenue share of 39.41% in 2025 due to extensive railway infrastructure, ongoing modernization of passenger and freight rail fleets, and increasing adoption of battery-powered and hybrid locomotives. The region benefits from significant investments in rail transportation upgrades, growing demand for reliable auxiliary and backup power systems, and the presence of leading battery manufacturers and technology providers. In addition, supportive government initiatives aimed at reducing transportation emissions and improving energy efficiency have accelerated the deployment of advanced battery solutions across rail networks, strengthening North America's position in the global market.

U.S. Train Battery Market Trends

U.S. train battery industry dominated the North America market in 2025 owing to its extensive freight and passenger rail network, substantial investments in railway modernization, and increasing adoption of advanced battery technologies for auxiliary power, signaling, and hybrid rail applications. The country's strong presence of rail operators, battery manufacturers, and technology providers, coupled with growing efforts to improve energy efficiency and reduce emissions from transportation systems, has driven demand for high-performance train batteries. In addition, government funding for rail infrastructure upgrades and sustainable transportation initiatives has further supported market growth across the U.S.

Europe Train Battery Market Trends

Europe train battery industry accounted for a significant share of the global market in 2025 due to its well-established railway infrastructure, strong focus on sustainable transportation, and ongoing investments in rail electrification and fleet modernization. Countries across the region are actively promoting low-emission mobility solutions and replacing diesel-powered trains with battery-electric and hybrid alternatives to support decarbonization goals. Increasing deployment of regional battery-powered trains, coupled with supportive government policies and investments in smart rail technologies, is expected to drive steady market growth.

Germany train battery industry is one of the leading markets for train batteries in Europe due to its advanced railway network, strong commitment to sustainable mobility, and growing adoption of battery-powered trains. The country is investing heavily in rail modernization projects and the deployment of alternative propulsion technologies to reduce carbon emissions and improve operational efficiency. Supported by the presence of major rail technology providers, battery manufacturers, and government-backed clean transportation initiatives, Germany continues to play a pivotal role in advancing battery-based rail solutions across the European rail sector.

Asia Pacific Train Battery Market Trends

Asia Pacific train battery industry is expected to register the fastest CAGR from 2026 to 2033 due to rapid railway expansion, increasing urbanization, and growing investments in electrified and battery-powered rail transportation. Countries such as China, India, Japan, and South Korea are investing heavily in metro systems, high-speed rail networks, and sustainable transportation infrastructure. Rising demand for reliable onboard power systems and increasing adoption of energy-efficient rail technologies are expected to create significant growth opportunities across the region.

China train battery industry is one of the most promising markets due to its extensive railway network, continuous expansion of high-speed rail infrastructure, and strong government support for the electrification of transportation. The country is witnessing increasing deployment of advanced battery systems in metro trains, light rail transit, and battery-powered locomotives. Growing investments in smart transportation, railway modernization, and domestic battery manufacturing capabilities are expected to accelerate market growth over the forecast period.

Latin America Train Battery Market Trends

Latin America train battery industry is an emerging market supported by ongoing investments in railway infrastructure modernization, urban transit development, and improving rail connectivity. Countries such as Brazil, Mexico, and Argentina are gradually upgrading passenger and freight rail systems to enhance operational efficiency and reliability. Increasing demand for backup power systems, signaling applications, and energy-efficient rail solutions is expected to support market expansion across the region.

Middle East & Africa Train Battery Market Trends

The Middle East & Africa train battery industry is gaining traction due to growing investments in rail transportation projects, metro network development, and railway electrification initiatives. Governments across the region are focusing on expanding public transportation infrastructure and improving intercity connectivity to support economic development and urbanization. Although the market remains at a developing stage, increasing adoption of modern rail technologies and demand for reliable onboard energy storage systems are expected to drive future growth.

Key Train Battery Company Insights

Some of the key players operating in the global train battery industry include AEG Power Solutions, Amara Raja Group, East Penn Manufacturing Company, ENERSYS., EXIDE INDUSTRIES LTD., FIRST NATIONAL BATTERY, FURUKAWA ELECTRIC CO., LTD., among others.

-

EnerSys is one of the key players in the train battery industry, engaged in the development and manufacturing of advanced energy storage solutions for railway applications. The company supplies batteries for starting, lighting and ignition (SLI) systems, auxiliary power units, signaling systems, and onboard rail equipment. Through its extensive product portfolio and global distribution network, EnerSys supports rail operators with reliable, high-performance battery technologies designed to enhance operational efficiency, safety, and fleet reliability.

-

Exide Industries Ltd. is a prominent participant in the train battery industry, specializing in the production of lead-acid and advanced battery solutions for passenger trains, metro systems, locomotives, and railway infrastructure applications. The company focuses on delivering durable and maintenance-efficient batteries for backup power, onboard electrical systems, and railway signaling networks. Its strong manufacturing capabilities, broad customer base, and continuous investments in battery innovation position it as a significant supplier to the global rail transportation sector.

Key Train Battery Companies:

The following key companies have been profiled for this study on the train battery market.

-

AEG Power Solutions

-

Amara Raja Group

-

East Penn Manufacturing Company

-

ENERSYS.

-

EXIDE INDUSTRIES LTD.

-

FIRST NATIONAL BATTERY

-

FURUKAWA ELECTRIC CO., LTD.

-

GS Yuasa International Ltd.

-

Hitachi Rail Limited

-

HOPPECKE Carl Zoellner & Sohn GmbH

-

FENGRI POWER & ELECTRIC CO., LIMITED.

-

Power & Industrial Battery Systems GmbH

-

Saft2022

-

SEC Battery

-

Shuangdeng Group Co, Ltd

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Saft Groupe; Hitachi Energy; GS Yuasa Corporation; EnerSys; Leclanché SA

Focus on development of lithium-ion, nickel-based, and hybrid battery systems for rail propulsion, auxiliary power, and energy storage applications.

Expand partnerships with railway OEMs and operators to support electrification, regenerative braking, and low-emission train technologies.

Strong industrial battery manufacturing expertise, established railway partnerships, and broad product portfolios support long-term market presence.

Advanced battery safety systems, high-cycle performance, and integrated energy management capabilities strengthen competitive positioning.

High R&D and certification costs associated with railway-grade battery systems.

Dependence on raw material supply chains and long railway procurement cycles may affect profitability and project timelines.

Emerging Players: Skeleton Technologies; HOPPECKE Rail Systems; Lithium Werks; PowerUp Technology; Freudenberg e-Power Systems

Focus on lightweight lithium-ion battery platforms, fast-charging systems, supercapacitor integration, and modular rail energy storage technologies.

Invest in battery systems designed for hybrid trains, regenerative braking, and non-electrified rail corridor applications.

Greater flexibility in adopting next-generation battery chemistries, compact system architectures, and rapid innovation cycles.

Strong focus on sustainable mobility, high-power charging, and energy-efficient rail operations supports market differentiation.

Limited commercial deployment scale and lower production capacity compared to established battery manufacturers.

High dependence on pilot projects, OEM collaborations, and infrastructure investments may affect large-scale commercialization.

Recent Developments

-

In January 2026, Great Western Railway launched the UK’s first battery-only passenger train service on the West Ealing-Greenford route in London. The rapid-charging train can recharge in approximately 3.5 minutes and is expected to support rail decarbonization efforts by providing a low-emission alternative to diesel-powered regional trains.

-

In November 2025, Hitachi Rail and battery technology partners continued expanding battery-powered and hybrid train development programs across Europe, focusing on reducing diesel dependence, improving energy efficiency, and supporting sustainable railway modernization initiatives. The projects are aimed at accelerating the adoption of battery-electric rolling stock on non-electrified rail routes.

Train Battery Market Report Scope

Report Attribute

Details

Market Definition

The global train battery industry comprises revenues generated from the sale and deployment of batteries used in railway rolling stock for traction, auxiliary power, and backup energy applications. The market includes batteries installed in locomotives, passenger coaches, metro trains, trams, and battery-powered or hybrid trains to support reliable rail operations, improve energy efficiency, and reduce emissions.

Market size value in 2025

USD 302.90 million

Market size value in 2026

USD 319.53 million

Revenue forecast in 2033

USD 490.73 million

Growth rate

CAGR of 6.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Type, technology, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; Russia; China; India;Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

AEG Power Solutions; Amara Raja Group; East Penn Manufacturing Company; ENERSYS.; EXIDE INDUSTRIES LTD.; FIRST NATIONAL BATTERY; FURUKAWA ELECTRIC CO., LTD.; GS Yuasa International Ltd.; Hitachi Rail Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Train Battery Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global train battery market report based on type, technology, application, and region.

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Lead Acid Battery

-

Nickel Cadmium Battery

-

Lithium Ion Battery

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Conventional Lead Acid Battery

-

Valve Regulated Lead Acid Battery

-

Gel Tubular Lead Acid Battery

-

Sinter/PNE Ni-Cd Battery

-

Pocket Plate Ni-Cd Battery

-

Fiber/PNE Ni-Cd Battery

-

Lithium Iron Phosphate (LFP)

-

Lithium Titanate Oxide (LTO)

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Metros

-

High-speed Trains

-

Light Rails/Trams/Monorails

-

Passenger Coaches

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Opportunity Assessment

Customized regional analysis covering country-level Train Battery Market size, railway electrification trends, fleet modernization initiatives, battery-powered and hybrid train adoption, regulatory framework, infrastructure investments, and competitive landscape across targeted geographies

Enabled identification of high-growth regions, investment opportunities, favorable regulatory environments, and market expansion prospects within the rail transportation sector

Market Segment Analysis

Additional cross-segmentations across battery type (lead acid battery, nickel cadmium battery, lithium ion battery), technology (conventional lead acid battery, valve regulated lead acid battery, gel tubular lead acid battery, sinter/pne ni-cd battery, pocket plate ni-cd battery, fiber/pne ni-cd battery, lithium iron phosphate (LFP), lithium titanate oxide (LTO), others), application (metros, high-speed trains, light rails/trams/monorails, passenger coaches), and regional markets tailored to strategic requirements

Provided deeper market intelligence, enhanced demand forecasting, stronger competitive benchmarking, and improved strategic planning across key market segments

Company Profiling

Customized profiling of selected Train Battery Market participants based on client preference, including company overview, product portfolio, battery technologies, manufacturing capabilities, strategic developments, financial insights, and market positioning

Delivered focused competitive intelligence, supported partnership and acquisition evaluation, and improved understanding of leading manufacturers, technology providers, and emerging market participants

Frequently Asked Questions About This Report

The global train Battery market size was estimated at USD 275 million in 2023 and is expected to reach USD 288.42 million in 2024.

The global train Battery market is expected to witness a compound annual growth rate of 5.8% from 2024 to 2030 to reach USD 402.82 million by 2030.

Lithium-ion battery was the largest segment accounting for a share of 46.75% of the global train Battery market revenue in 2023. The demand for train batteries primarily driven by the expansion of railway networks.

Some key players operating in the train Battery market include AEG Power Solutions, Amara Raja Group, East Penn Manufacturing Company, ENERSYS., EXIDE INDUSTRIES LTD., FIRST NATIONAL BATTERY, FURUKAWA ELECTRIC CO., LTD., GS Yuasa International Ltd., Hitachi Rail Limited, HOPPECKE Carl Zoellner & Sohn GmbH, FENGRI POWER & ELECTRIC CO., LIMITED., Power & Industrial Battery Systems GmbH, Saft2022, SEC Battery, Shuangdeng Group Co, Ltd and others.

Key factors driving the growth of the train Battery market include the increasing adoption of electrification in the railway industry and the emphasis on reducing pollution.

About the Author(s)

Power Generation & Storage Research Team

Energy & Power · Power Generation & StorageThis report was authored by the power generation & storage research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the power generation & storage segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.