- Home

- »

- Animal Health

- »

-

Veterinary Contract Manufacturing Market Report, 2026-2033GVR Report cover

![Veterinary Contract Manufacturing Market (2026 - 2033)Report]()

Veterinary Contract Manufacturing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Biologics, Pharmaceuticals), By Animal, By Service (Manufacturing Services, Packaging & Labelling Services), By Customer, By Region, And Segment Forecasts

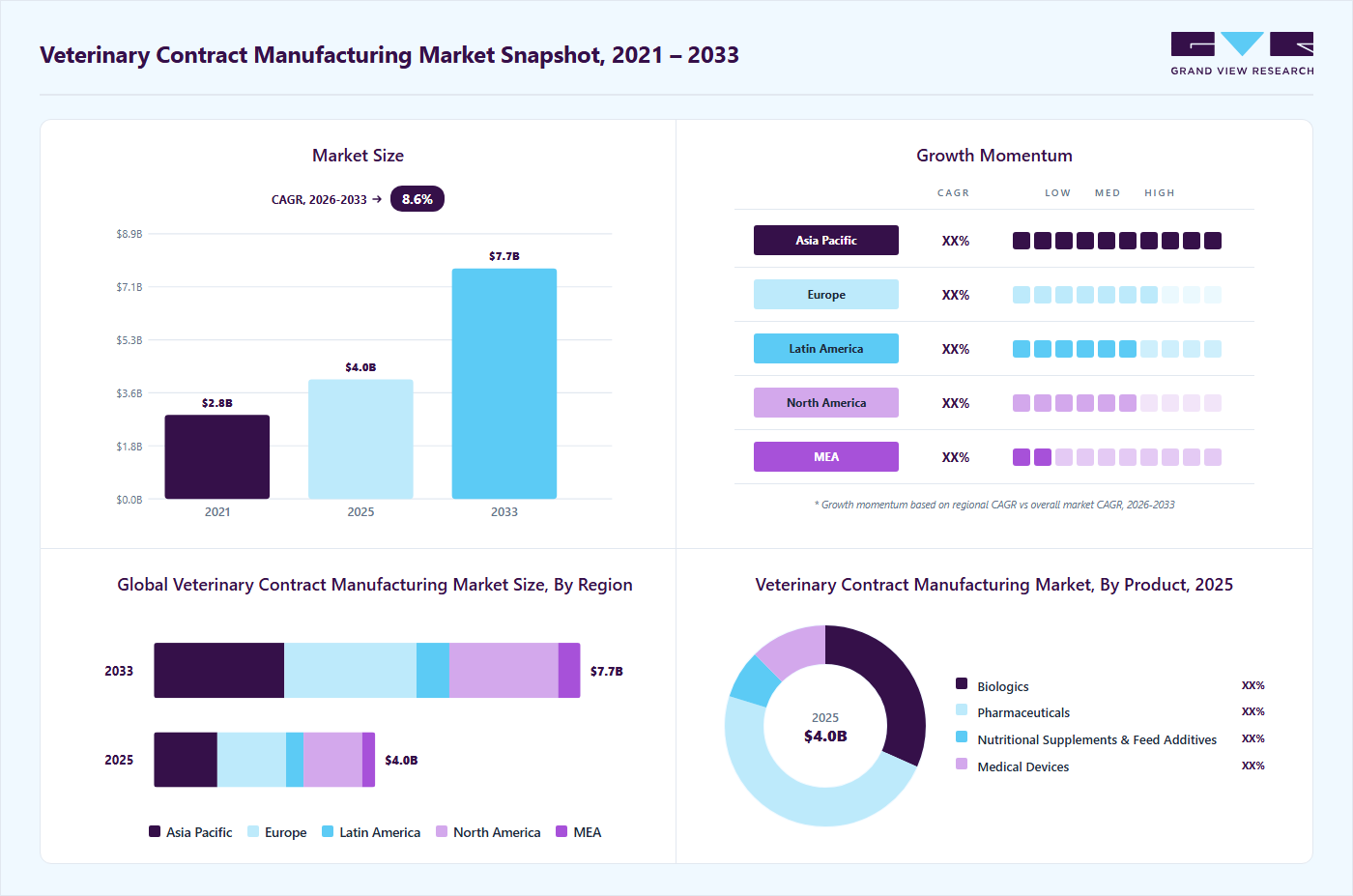

Market Size, 2025

$4.0BMarket Estimate, 2026

$4.4BMarket Forecast, 2033

$7.7BCAGR, 2026–2033

8.6%Veterinary Contract Manufacturing Market Summary

The global veterinary contract manufacturing market size was valued at USD 4.0 billion in 2025 and is projected to grow from USD 4.4 billion in 2026 to USD 7.7 billion by 2033, at a CAGR of 8.6% from 2026 to 2033. The Europe held the largest share of 31.1% of the global market in 2025. The major factors driving growth of the market include rising strategic focus on CMO core business models, increasing capacity expansion & investment in multi-species manufacturing, rising demand for infrastructure development and outsourced manufacturing contracts and favorable regulatory scenario.

Key Market Trends & Insights

- By product: Pharmaceuticals segment held the largest share of 48.1% in 2025.

- By animal: Production animal segment held the largest in the market in 2025.

- By service: Manufacturing services segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Europe (31.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The Germany led the Europe market in 2025.

Market Size & Forecast

- Market size in 2025: USD 4.0 Billion

- Estimated market size in 2026: USD 4.4 Billion

- Projected market size by 2033: USD 7.7 Billion

- CAGR (2026-2033): 8.6%

The market is driven by companies prioritizing CMO-focused business models to enhance operational efficiency and scalability. Animal health companies are shifting from in-house production to outsourcing, enabling them to focus on R&D, commercialization, and portfolio expansion while leveraging specialized manufacturing expertise. This transition is further supported by growing demand for complex biologics, APIs, and companion animal therapeutics. For instance, in April 2026, Prange Pharma acquired an animal health manufacturing site from MSD Animal Health in Italy, strengthening its contract manufacturing capabilities and strategic positioning in the CDMO space.

")

In addition, capacity expansion across multi-species manufacturing facilities is a major growth driver, as demand rises for vaccines, APIs, and therapeutics across livestock and companion animals. CDMOs are investing in advanced infrastructure to support diverse production needs, including poultry, swine, and pet healthcare segments. These investments enable flexible, large-scale production while meeting regulatory and quality requirements across geographies. For instance, in September 2025, Sai Life Sciences expanded its dedicated veterinary API manufacturing capacity in India, strengthening its role in global animal health supply chains. Such expansions reflect the industry’s shift toward integrated manufacturing platforms capable of handling multiple species and dosage forms, ultimately improving accessibility, reducing costs, and supporting the growing global demand for veterinary products.

Furthermore, the increasing complexity of veterinary pharmaceuticals, including biologics, vaccines, and specialty formulations, is driving demand for outsourced manufacturing services. Some of the companies are depending on CDMOs to access advanced technologies, regulatory expertise, and scalable production without significant capital investment. This trend is particularly evident in emerging markets and niche product segments such as diagnostics and pet therapeutics. For instance, in January 2026, Zomedica entered into a contract manufacturing and services agreement with Rahm Sensor Development to diversify its offerings and expand revenue streams. Such collaborations highlight how outsourcing enables companies to accelerate market entry, optimize costs and enhance product innovation.

Moreover, the market is advancing due to stringent and evolving regulatory frameworks that emphasize product safety, quality, and traceability. Compliance with Good Manufacturing Practices (GMP), biosafety standards, and international guidelines encourages animal health companies to partner with specialized CDMOs possessing regulatory expertise. These partners help navigate complex approval processes across multiple regions, reducing compliance risks and time-to-market. In addition, harmonization efforts and government initiatives to strengthen veterinary oversight are promoting standardized manufacturing practices.

Market Dynamics

Growing investments in multi-species manufacturing facilities are driving the animal health CDMO market as demand increases for veterinary vaccines, APIs, biologics, and therapeutics across livestock and companion animals. CDMOs are expanding flexible production infrastructure to support poultry, swine, cattle, and pet healthcare applications while meeting global quality and regulatory standards. These expansions improve production scalability, supply chain efficiency, and product accessibility across international markets.

Increasing complexity in veterinary pharmaceuticals, including biologics, specialty formulations, diagnostics, and advanced vaccines, is accelerating outsourcing to CDMOs. Animal health companies are increasingly relying on external manufacturing partners to access advanced technologies, specialized expertise, and scalable production capabilities without major capital investments. Strategic collaborations and contract manufacturing agreements are also helping companies accelerate commercialization timelines, optimize operational costs, and strengthen innovation pipelines.

Evolving regulatory frameworks emphasizing product safety, traceability, and manufacturing quality are supporting demand for specialized animal health CDMOs with strong compliance expertise. Adherence to GMP standards, biosafety regulations, and international veterinary guidelines is becoming increasingly important across global markets. CDMOs with established regulatory capabilities help animal health companies navigate complex approval processes, reduce compliance risks, and improve speed-to-market for veterinary products.

The veterinary contract manufacturing market faces a key restraint due to stringent regulatory requirements and the high costs associated with facility validation, biosafety compliance, and quality assurance processes. Manufacturers must comply with varying regional regulations for veterinary pharmaceuticals, biologics, and vaccines, increasing operational complexity and approval timelines. In addition, maintaining multi-species production capabilities and specialized infrastructure requires significant capital investment, which can limit expansion for small and mid-sized CDMOs and create barriers to entry in highly regulated markets.

Tariff and Trade Policy Impact on Veterinary Contract Manufacturing Market

Factor

Tariff & Trade Impact Analysis

Trade Liberalization & SPS Measures

WTO’s World Trade Organization SPS Agreement reduces tariff barriers but increases sanitary requirements, making compliance critical for veterinary manufacturers engaged in cross-border contract manufacturing.

Stringent Import Regulations

Regulatory bodies like U.S. Food and Drug Administration enforce strict import verification for veterinary products, increasing compliance costs and documentation requirements for contract manufacturers operating in global markets.

Harmonized Trade & Regulatory Frameworks

EU veterinary medicine regulations standardize import, manufacturing, and distribution rules, facilitating trade but increasing compliance complexity for CDMOs handling multi-country veterinary product manufacturing and exports.

Restricted Animal Trade Policies

National policies such as India’s livestock import restrictions and licensing under EXIM regulations limit free trade, impacting raw material sourcing and increasing dependency on domestic veterinary manufacturing capabilities.

Market Concentration & Characteristics

The veterinary contract manufacturing industry is highly fragmented, with a mix of global CDMOs and regional specialists. Key players such as Aenova Group, Grifols International, Labiana, Terumo Corporation (Terumo BCT), Kela Health, Vetio Animal Health, Parnell, among others compete alongside niche providers, driving competition through specialized capabilities, geographic presence, and strategic partnerships with animal health companies.

Innovation in the market is accelerating with advancements in biologics, vaccines, and novel drug delivery systems. CMOs are increasingly integrating technologies such as mRNA platforms, sustained-release formulations, and precision fermentation. In addition, innovation is focused on multi-species product development, enabling manufacturers to cater to diverse livestock and companion animal needs, thereby strengthening competitive differentiation.

The market is witnessing robust merger and acquisition activity as companies seek to expand capabilities, geographic reach, and service portfolios. Larger CDMOs are consolidating smaller niche players to strengthen end-to-end service offerings. For instance, in August 2025, Kemin Industries acquired Hennessy Research Associates, expanding its veterinary vaccine R&D, contract manufacturing capabilities, and strengthening its position in global animal health markets. This trend is intensifying competition while also creating integrated platforms capable of handling complex veterinary biologics and pharmaceutical manufacturing requirements.

Regulatory frameworks significantly influence veterinary contract manufacturing, ensuring product safety, efficacy, and quality. Compliance with GMP standards, biosafety norms, and country-specific veterinary guidelines increases operational complexity and costs. However, evolving regulatory harmonization and faster approval pathways for animal health products are improving market accessibility. Stringent regulations also act as barriers to entry, favoring established players with proven compliance capabilities and robust quality systems.

CMOs are expanding into integrated service offerings, including formulation development, analytical testing, packaging, and regulatory support. The companies seek for comprehensive services. In addition, specialized services such as biologics production, vaccine fill-finish, and cold chain logistics are gaining traction, enabling CMOs to capture greater value across the veterinary pharmaceutical value chain.

Manufacturers are actively expanding into emerging markets such as Asia-Pacific, Latin America, and the Middle East. These regions offer cost advantages, growing livestock populations, and increasing demand for animal healthcare products. In addition, regional expansion also helps mitigate supply chain risks and supports global clients with localized manufacturing and regulatory compliance.

Product Insights

By product, the pharmaceuticals segment dominated the market with the largest revenue share of 48.1% in 2025, attributed to increasing demand for generics and advanced formulations. In addition, rising R&D spending and the prevalence of zoonotic diseases are accelerating outsourcing to specialized partners. Pharmaceutical companies leverage contract manufacturers’ scalability, regulatory expertise, and advanced technologies to reduce costs and accelerate time to market. Outsourcing demand is further supported by the expansion of personalized medicine, biosimilars, and biologics. In addition, the need for flexible, multi-product facilities and stringent compliance requirements strengthens the critical role of CDMOs and CMOs.

Biologics is projected to be the fastest growing segment in the market over the forecast period, driven by increasing demand for vaccines and monoclonal antibodies, and growth in intensive animal farming. In addition, advancements in biotechnology and immunology are enabling development of targeted therapies and next-generation vaccines. Some of the initiatives taken by government help in supporting animal health and food security that boost demand. Furthermore, pharmaceutical companies are outsourcing biologics production in large numbers due to high capital requirements, complex manufacturing processes, and the need for specialized facilities, driving growth of contract manufacturing partnerships in this segment.

Animal Insights

Based on animal, the production animals segment dominated the market with the largest revenue share in 2025. This can be attributed to increasing demand for animal protein, expansion of commercial production animals farming, and rising focus on food safety. Government initiatives supporting production animal’s productivity and disease control are boosting demand for vaccines, feed additives, and therapeutics. For instance, in February 2026, India’s Union Budget 2026 prioritized animal husbandry through funding for Livestock Farmer Producers Organizations (LFPOs), strengthening dairy value chain, vaccination programs and expanding veterinary infrastructure. In addition, large-scale farming requires consistent, high-volume production, encouraging pharmaceutical companies to depend on contract manufacturers for cost efficiency, scalability, and compliance with stringent quality and regulatory standards.

The companion segment is expected to exhibit the fastest CAGR during the forecast period, due to rising pet ownership, increasing humanization of pets, and higher spending on preventive and therapeutic care. In addition, expansion of pet insurance and veterinary services further supports growth. In addition, pharmaceutical companies are outsourcing production to specialized partners to manage complex formulations, ensure quality compliance, and accelerate time-to-market for innovative companion animal therapies.

Service Insights

On the basis of service, the manufacturing services segment held the largest share in 2025 and is also expected to grow at the fastest growth rate over the forecast period. The segment’s growth is influenced by rising demand for veterinary medicines, increasing outsourcing by animal health companies, and need for dedicated, regulatory-compliant manufacturing facilities. In addition, expansion of specialized capacity, highlights growing infrastructure investment. For instance, in September 2025, Sai Life Sciences inaugurated a veterinary API facility in Bidar, India enhancing manufacturing capabilities. In addition, focus on cost efficiency, scalable production, and reliable supply chains is accelerating partnerships with CMOs.

The packaging & labelling services segment is the second largest segment in terms of market share in 2025, driven by increasing regulatory focus on packaging compliance, product safety, and its traceability. Some of the initiatives highlight stricter monitoring and quality standards. For instance, in January 2026, Veterinary Medicines Directorate launched a packaging surveillance in UK to assess and monitor veterinary medicine packaging and reduce regulatory burden. In addition, growing need for accurate product information, anti-counterfeiting measures, and standardized labelling further supports demand.

Customer Insights

In terms of customer, the pharmaceutical and biotechnology companies segment accounted for the largest share in 2025 and is also expected to grow at the fastest over the forecast period, owing to increasing reliance on outsourcing to improve efficiency, reduce costs, and focus on core R&D activities. In addition, rising demand for veterinary biologics, vaccines, and advanced formulations has strengthened partnerships with CMOs and CDMOs offering specialized manufacturing and regulatory expertise. These companies outsource significant production volumes to meet growing global animal health demand, comply with stringent quality standards, and optimize supply chain efficiency across diverse markets.

The medical device companies segment is anticipated to witness considerable growth during the forecast period, driven by rising demand for innovative and high-precision animal health devices. In addition, increasing adoption of wearable monitoring devices, diagnostic tools, and minimally invasive veterinary procedures is supporting market expansion. Some of the technological advancements such as 3D printing for pet prosthetics and implants, portable monitoring devices, and smart device integration are further accelerating production capabilities.

Regional Insights

North Americaveterinary contract manufacturing market is advancing over the forecast period. This can be attributed to advanced biologics manufacturing adoption, strong CDMO presence, rising animal health R&D partnerships and increasing outsourcing by pharma companies. The region witnesses high competition with established CMOs and CDMOs such as Argenta Holdco Limited, TriRx Pharmaceutical Services, Vetio, and Cambrex expanding biologics and multi-dosage capabilities. These players compete on integrated services, regulatory expertise, and scale. The regulations in this region are governed by the U.S. Food and Drug Administration and USDA Center for Veterinary Biologics, that enforces cGMP compliance and stringent biologics approval processes, ensuring high entry barriers and quality-driven competition.

U.S. Veterinary Contract Manufacturing Market Trends

The veterinary contract manufacturing industry in the U.S. accounted for the highest market share in the North America market, owing to rising demand for biologics and animal vaccines, onshore manufacturing preference, stringent regulatory requirements for U.S.-based production, and increasing acquisitions by animal health companies. The country is advancing due to strategic mergers and acquisitions by established players with local CDMOs. For instance, in March 2025, Syngene International acquired U.S. biologics facility to expand capacity and support animal health clients requiring domestic manufacturing. In addition, market competition is also driven by CDMOs focusing on service expansion to strengthen their U.S. presence. For instance, in July 2025, Superior Supplement Manufacturing expanded its pet supplement contract manufacturing services, enhancing capabilities in soft chews, capsules, tablets, and gummies to meet rising pet health demand. Such factors boost market growth.

Canada veterinary contract manufacturing industryis expected to grow at a significant CAGR during the forecast periodpropelled by strong government support for animal health preparedness and cross-border collaboration in veterinary biologics regulation. The market is further driven by proactive government initiatives to strengthen animal health infrastructure and emergency preparedness. For instance, the Public Health Agency of Canada secured avian influenza vaccine supplies to enhance readiness, reflecting growing demand for scalable manufacturing support. Furthermore, cross-border regulatory collaboration further supports innovation, streamlined approvals, and increased outsourcing to specialized CMOs.

Europe Veterinary Contract Manufacturing Market Trends

The veterinary contract manufacturing industry in Europe dominated the market with a revenue share of 31.1%, driven by strong EU regulatory support, rising veterinary medicine approvals and growing vaccine innovation and public-private collaborations. The market in this region is competitive, led by established players. According to a report of January 2026, the European Medicines Agency recommended 30 veterinary medicines in 2025, reflecting strong pipeline growth and outsourcing demand. In addition, initiatives such as vaccine innovation hubs and collaborations are enhancing manufacturing capabilities. In addition, competition is also driven by advanced biologics expertise, regulatory compliance, and integrated CDMO services across Europe.

The veterinary contract manufacturing industry in the UK is expected to grow significantly over the forecast period, due to rising focus on biosecurity infrastructure; stringent antimicrobial stewardship; supply chain resilience initiatives; regulatory continuity for manufacturing and batch release. UK veterinary contract manufacturing industry is moderately consolidated with strong regulatory oversight by the Veterinary Medicines Directorate, fostering partnerships between pharma firms and CMOs. Government initiatives such as the 2025 vaccine availability framework aim to boost domestic manufacturing capacity and innovation. In addition, rising investments such as GBP 1 billion (~USD 1.3 billion) in biosecurity labs strengthens disease preparedness and demand for outsourced production.

Germany veterinary contract manufacturing industryheld the largest share in 2025 in Europe. The country’s growth is influenced by rising pet ownership and livestock health demand, strong pharmaceutical manufacturing base, increasing R&D funding. The country witnesses moderately consolidated landscape led by players such as Boehringer Ingelheim, Bayer AG, Vetoquinol, and global firms like Zoetis. In addition, companies emphasize CDMO partnerships, advanced biologics manufacturing, and regulatory expertise. For instance, in January 2025, HIPRA launched its CDMO division, securing its first strategic biologics contract within nine months, leveraging decades of expertise in vaccine development, R&D, and large-scale manufacturing.

Asia Pacific Veterinary Contract Manufacturing Market Trends

Asia Pacific veterinary contract manufacturing industry is expected to grow at the fastest CAGR over the forecast period. The anticipated rising livestock population and disease burden, increasing pet ownership and premium care spending, government-led animal health infrastructure expansion and cost advantages attracting outsourcing is advancing region’s growth. The region is highly fragmented with regional CMOs in China and India competing on cost while global players expand partnerships and outsourcing networks. The manufacturers in India leverage strong generics expertise, while multinational firms increasingly outsource to the region to scale biologics and vaccine production capacity

The veterinary contract manufacturing industry in China held the largest revenue shareandis witnessing new growth opportunities due to rising government regulation and GMP enforcement by Ministry of Agriculture and Rural Affairs, expansion of livestock disease surveillance systems, rising demand for animal disease control, growth in livestock farming, and increasing partnerships to improve veterinary medicine use in China. The market is highly fragmented yet rapidly scaling, with domestic CMOs leveraging cost-efficient manufacturing, advanced facilities, and regulatory expertise to attract global clients. Some of the players differentiate via end-to-end services and compliance with GMP certifications issued by government authorities. Moreover, international collaborations and technology-driven capabilities intensify competition, while local firms benefit from strong supply chains and policy support, creating a mix of global entrants and strong domestic manufacturers competing on scale, cost, and quality.

The market for veterinary contract manufacturing in India is witnessing notable growth due to rising livestock population & dairy demand, cost-efficient GMP manufacturing base, strong government animal health initiatives and biotech investments and alongside disease-control programs and rural veterinary infrastructure expansion. For instance, in February 2026, the Technology Development Board (TDB) of India's Department of Science and Technology (DST) announced financial support for M/s Biovet Private Limited to establish a facility for indigenous veterinary hormone production. Such initiatives boost contract manufacturing capabilities.

Latin America Veterinary Contract Manufacturing Market Trends

The veterinary contract manufacturing industry in Latin America is driven by rising livestock exports, government-led animal health programs, expansion of local vaccine manufacturing, and increasing multinational investments in regional production facilities. The market is moderately consolidated with global players like Zoetis, Elanco, and Ceva Santé Animale expanding manufacturing footprints, while regional firms enhance CDMO capabilities. In addition, partnerships with local governments and contract production agreements are intensifying competition and improving supply chain localization.

Brazil veterinary contract manufacturing industryis gaining momentum due to increasing government animal health programs (One Health surveillance), rising disease outbreaks boosting vaccine demand, and attainment of foot-and-mouth disease-free status improving global trade and investment. The country is witnessing growth due to multinationals and regional firms invest in local manufacturing facilities to serve large livestock sectors. For instance, in March 2025, Vetanco inaugurated a 4,000 sqm facility in Brazil, with regulatory compliance, future organic additive production plans, and strong participation from authorities and industry stakeholders.

Middle East & Africa Veterinary Contract Manufacturing Market Trends

The veterinary contract manufacturing industry in MEA is advancing, due to rising zoonotic disease control programs, growing government-led food security strategies, increasing local manufacturing push, and local investments. For instance, in November 2025, Fabtech Technologies Limited secured a contract to build a veterinary medicines facility in Africa driven by increasing demand for animal health products and food security goal strengthening its global expansion. In addition, local firms focus on cost-efficient manufacturing, while international companies bring advanced technologies and regulatory expertise, intensifying competition across biologics and generics segments.

South Africa veterinary contract manufacturing industryis growing due to export-oriented meat safety regulations and regional capacity expansion supported by projects. The country’s market is moderately consolidated, led by multinational CDMOs and regional players offering dosage manufacturing and packaging. Companies compete on regulatory compliance (e.g., DALRRD standards), cost efficiency, and localized production.

Saudi Arabia veterinary contract manufacturing industryis fueled by rising livestock and poultry production under Saudi Vision 2030, increasing focus on food security, growing demand for veterinary biologics and feed additives, and strategic partnerships expanding product access and local distribution. The market is advancing, led by multinational CMOs and regional distributors collaborating with local firms. For instance, in May 2025, Vetanco partnered with Al-Emar International enhance supply chains and gradual localization of manufacturing capabilities.

Key Veterinary Contract Manufacturing Company Insights

Some of the key companies include Aenova Group, Grifols International, Labiana, Terumo Corporation (Terumo BCT), Kela Health, Vetio Animal Health, Parnell, among others. The market is fragmented in nature, with regional contract manufacturers competing on cost and specialization.

Key Veterinary Contract Manufacturing Companies:

The following key companies have been profiled for this study on the veterinary contract manufacturing market.

- Aenova Group

- Grifols International

- Labiana

- Argenta Holdco Limited

- Kela Health

- Vetio Animal Health

- TriRx Pharmaceutical Services

- Parnell

- VetViva Richter GmbH

- Tecton Industries

- Ubio Biotechnology Systems Pvt Ltd

- Terumo Corporation (Terumo BCT)

- BioVenic

- Esco Aster Pte. Ltd

- Alicanto Vetcare

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Player: Thermo Fisher Scientific, Inc.

- Operate end-to-end integrated platforms covering formulation, scale-up, GMP manufacturing, packaging, and regulatory support.

- Expand capacity via large-scale investments, acquisitions, and multi-species manufacturing facilities to serve global pharma clients and ensure supply chain reliability.

- Deep regulatory expertise and GMP compliance systems across multiple geographies (US, EU, etc.), reducing approval risk for clients.

- Scalability and global infrastructure, enabling large-volume production, complex biologics manufacturing, and long-term supply agreements.

- High operational costs due to complex infrastructure, compliance systems, and large fixed-capital facilities.

- Lower agility, making it harder to quickly adapt to niche or rapidly evolving product innovations compared to smaller competitors.

Emerging Player: PromoCell GmbH

- Focus on specialized, niche capabilities such as biologics, vaccines, or small-batch production to quickly win early outsourcing contracts.

- Build growth through strategic partnerships and regional expansion, often targeting cost-competitive manufacturing hubs (e.g., Asia-Pacific) to attract global clients.

- Strong advantage in flexibility and customization, allowing rapid adaptation to new molecules, dosage forms, and small client requirements.

- Cost-efficient operations and lean structures enable competitive pricing and faster turnaround times in early-stage outsourcing deals.

- Limited scale and capacity constraints, making it difficult to support high-volume or global supply contracts.

- Weaker regulatory track record and quality systems, which can restrict entry into highly regulated markets like the US and EU.

Recent Developments

-

In April 2026, Shelter Pharma qualified technical evaluation for a veterinary medicines tender from Verka Dairies, marking progress in securing large-scale domestic supply contracts in the veterinary healthcare segment. Such an initiative boosts domestic contract manufacturing opportunities through institutional tenders, increasing competition among local CDMOs and enhancing production scale capabilities.

-

In April 2026, Parnell acquired Noble Pharma LLC, adding an FDA- and DEA-accredited U.S. manufacturing facility, strengthening production capabilities, ensuring supply continuity, and supporting expansion of its veterinary product portfolio. Such an initiative drives consolidation and capacity expansion, intensifying competition among global CMOs while improving reliability and scalability of veterinary contract manufacturing services.

-

In February 2026, Lucky Core Industries inaugurated a new animal health veterinary medicine manufacturing facility at Sheikhupura, Pakistan, expanding production capacity, strengthening local manufacturing footprint, and enhancing its veterinary pharmaceutical portfolio. This strengthens regional manufacturing capacity, reducing outsourcing demand while encouraging localized contract manufacturing partnerships and improving supply chain efficiency.

Veterinary Contract Manufacturing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4.0 billion

Estimated market size in 2026

USD 4.4 billion

Projected market size by 2033

USD 7.7 billion

Growth rate

CAGR of 8.6% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, animal, service, customer, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Thailand; South Korea; Australia; Brazil; Argentina; South Africa; UAE; Saudi Arabia; Kuwait; Qatar; Oman

Key companies profiled

Aenova Group; Grifols International; Labiana; Argenta Holdco Limited; Kela Health; Vetio Animal Health; TriRx Pharmaceutical Services; Parnell; VetViva Richter GmbH; Tecton Industries; Ubio Biotechnology Systems Pvt Ltd; Terumo Corporation (Terumo BCT); BioVenic; Esco Aster Pte. Ltd; Alicanto Vetcare

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Veterinary Contract Manufacturing Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global veterinary contract manufacturing market report based on product, animal, service, customer, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Biologics

-

Vaccines

-

Other Biologics

-

-

Pharmaceuticals

-

Parasiticides

-

Anit-infectives

-

Anti-inflammatory & Analgesics

-

Others Pharmaceuticals

-

-

Nutritional Supplements & Feed Additives

-

Medical Devices

-

-

Animal Outlook (Revenue, USD Million, 2021 - 2033)

-

Production Animals

-

Bovine

-

Poultry

-

Swine

-

Ovine & Caprine

-

Aquaculture

-

-

Companion Animals

-

Dogs

-

Cats

-

Horses

-

Others

-

-

Other Animals

-

-

Service Outlook (Revenue, USD Million, 2021 - 2033)

-

Manufacturing Services

-

Finished Drug Product Manufacturing

-

Oral Solid Dose (OSD)

-

Oral Liquid Dose

-

Injectables & Sterile Manufacturing

-

Others

-

-

API Manufacturing

-

Medical Device Manufacturing

-

-

Packaging & Labelling Services

-

Other Services

-

-

Customer Outlook (Revenue, USD Million, 2021 - 2033)

-

Pharmaceutical & Biopharmaceutical Companies

-

Animal Feed & Nutrition Companies

-

Medical Device Companies

-

Other Customer

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Saudi Arabia

-

Kuwait

-

Qatar

-

Oman

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

New business entry on the veterinary CDMO market

Detailed assessment of entry strategies into the veterinary contract manufacturing market, covering dosage form capabilities (injectables, oral solids, topicals, biologics), facility and GMP compliance requirements, regulatory pathways (USDA, EMA-Vet, national VMAs), and partnerships vs. greenfield models. Includes benchmarking of incumbent CMOs by therapeutic area, species focus, and capacity.

Equips new entrants and investors with a clear go-to-market roadmap, identifies underserved species segments (equine, aquaculture, exotic animals), and highlights regulatory white spaces where speed-to-market advantages exist.

Market segmentation & demand analysis

Granular segmentation across species (companion animals, livestock, poultry, aquaculture), product type (vaccines, antiparasitic, anti-infective, nutraceuticals), and buyer (veterinary clinics, farms, distributors), and geography (North America, Europe, Asia Pacific, Latin America, MEA). Includes demand drivers such as pet humanization trends, and food safety regulations.

Enables clients to identify highest-growth segments and prioritize manufacturing capacity investments, contract negotiations, and portfolio expansion aligned with species-specific demand trajectories and regulatory tailwinds.

Company profiles— generic veterinary product manufacturers

Profiles of key companies producing generic veterinary products, covering product portfolios, manufacturing capabilities, regulatory approvals, geographic reach, pricing strategies, and recent M&A or partnership activity. Coverage includes relevant Tier 2 generics manufacturers by region.

Supports competitive benchmarking, helps identify acquisition or co-manufacturing targets, and provides a basis for differentiation strategy against established generic players in companion animal and livestock markets.

Frequently Asked Questions About This Report

The global veterinary contract manufacturing market size was valued at USD 4.0 billion in 2025 and is estimated at USD 4.4 billion for 2026.

The global veterinary contract manufacturing market is expected to grow at a CAGR of 8.6% from 2026 to 2033, reaching USD 7.7 billion by 2033.

In the product segment, pharmaceuticals segment held the largest share of 48.1% of the market in 2025. This can be attributed to increasing demand for generics and advanced formulations. In addition, rising R&D spending and the prevalence of zoonotic diseases are accelerating outsourcing to specialized partners.

Key players include Aenova Group; Grifols International; Labiana; Argenta Holdco Limited; Kela Health; Vetio Animal Health; TriRx Pharmaceutical Services; Parnell; VetViva Richter GmbH; Tecton Industries; Ubio Biotechnology Systems Pvt Ltd; Terumo Corporation (Terumo BCT); BioVenic; Esco Aster Pte. Ltd; Alicanto Vetcare.

The major factors driving growth of the market include rising strategic focus on CMO core business models, increasing capacity expansion & investment in multi-species manufacturing, rising demand for infrastructure development and outsourced manufacturing contracts and favorable regulatory scenario.

Europe dominated with a 31.1% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The manufacturing services segment held the largest revenue share in 2025 and is the fastest-growing service.

The production animal segment held the largest revenue share in 2025, while companion is the fastest-growing animal.

The pharmaceutical and biotechnology companies segment held the largest revenue share in 2025 and is the fastest-growing customer.

About the Author(s)

Animal Health Research Team

Healthcare · Animal HealthThis report was authored by the animal health research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the animal health segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.