- Home

- »

- Plastics, Polymers & Resins

- »

-

Beverage Container Market Size, Share Report, 2026-2033GVR Report cover

![Beverage Container Market (2026 - 2033)Report]()

Beverage Container Market (2026 - 2033)

Size, Share & Trends Analysis Report By Materials (Plastic, Glass, Metal, Paper & Paperboard), By Container Type (Cans, Cartons, Pouches), By End Use (Non Alcoholic Beverages, Alcoholic Beverages), By Region, And Segment Forecasts

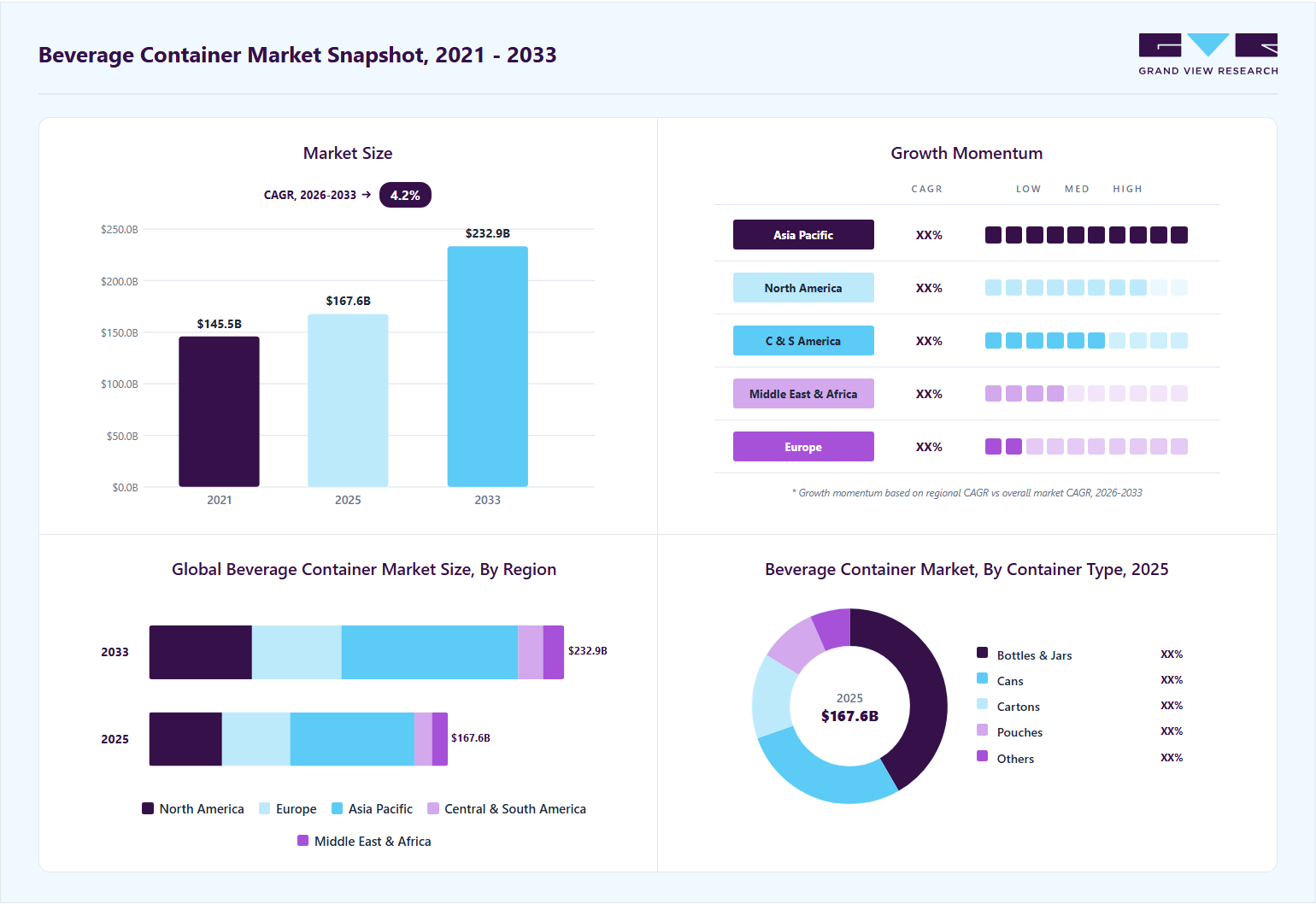

Market Size, 2025

$167.6BMarket Estimate, 2026

$174.0BMarket Forecast, 2033

$232.9BCAGR, 2026–2033

4.2%Beverage Container Market Summary

The global beverage container market size was valued at USD 167.6 billion in 2025 and is projected to grow from USD 174.0 billion in 2026 to USD 232.9 billion by 2033, at a CAGR of 4.2% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 41.6% in 2025. The market is driven by rising consumption of packaged and ready-to-drink beverages, growing demand for sustainable packaging, increasing premium beverage launches, expanding manufacturing capacity, and advancements in lightweight packaging technologies.

Key Market Trends & Insights

- By material: Plastic segment held the largest market share of 39.8% in 2025.

- By container type: Bottles & jars segment held the largest market share of 41.6% in 2025.

- By end use: Non alcoholic beverages segment held the largest market share of 78.1% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (41.6% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 167.6 Billion

- Estimated market size in 2026: USD 174.0 Billion

- Projected market size by 2033: USD 232.9 Billion

- CAGR (2026-2033): 4.2%

The increasing consumption of packaged beverages such as bottled water, soft drinks, energy drinks, dairy beverages, and ready-to-drink products is a major driver for the beverage container market. Rapid urbanization, changing consumer lifestyles, and rising preference for convenience-based consumption continue to increase demand for portable and single-use beverage packaging solutions across global markets.Growing environmental concerns and stricter packaging regulations are accelerating the shift toward sustainable beverage containers. Beverage manufacturers are increasingly adopting recyclable materials such as aluminum, glass, and recycled PET to reduce plastic waste and meet sustainability commitments. Consumer preference for eco-friendly packaging is further supporting demand for sustainable container solutions.

")

The expansion of premium beverages, including craft drinks, flavored beverages, functional drinks, and premium alcoholic products, is driving demand for visually appealing and innovative packaging formats. Beverage brands are investing in advanced container designs, high-quality printing, and differentiated packaging to strengthen brand positioning and improve shelf visibility in competitive retail markets.

Continuous innovation in lightweight packaging technologies is supporting market growth by improving transportation efficiency and reducing material costs. Manufacturers are developing thinner aluminum cans, lightweight plastic bottles, and durable packaging solutions that maintain product safety while lowering logistics expenses. These advancements are helping beverage companies improve operational efficiency and sustainability performance.

Market Dynamics

The growing global consumption of packaged and ready-to-drink (RTD) beverages is a major driver of the beverage container market, as consumers increasingly prefer convenient and portable drink options. Rising urbanization, changing lifestyles, and busy consumer routines are increasing demand for bottled water, soft drinks, energy drinks, dairy beverages, alcoholic drinks, and ready-to-drink tea and coffee products. Beverage containers are widely used to maintain product quality, improve shelf life, and support efficient transportation and storage across retail channels.

Rising disposable incomes and growing middle-class populations are driving higher spending on packaged beverages, particularly in emerging economies. The increasing popularity of premium, functional, and health-focused drinks is encouraging beverage companies to adopt innovative and attractive packaging formats. The expansion of supermarkets, convenience stores, and e-commerce platforms is further supporting global demand for beverage containers across plastic, metal, glass, and carton packaging formats.

Raw material price volatility is a major restraint for the beverage container market, as the industry heavily depends on materials such as aluminum, PET resin, glass, and steel. Fluctuations in crude oil prices, energy costs, mining activities, and global supply-demand conditions can significantly increase manufacturing expenses and reduce profit margins for container producers. Additionally, supply chain disruptions and inflationary pressures create uncertainty in raw material procurement, making it difficult for manufacturers to maintain stable pricing and long-term operational planning in a highly competitive market.

Market Concentration & Characteristics

The beverage container industry is characterized by strong demand from the foodservice, alcoholic beverages, soft drinks, dairy, and ready-to-drink segments, supported by increasing consumption of packaged beverages and rising focus on sustainable packaging solutions. The market is witnessing continuous innovation in lightweight materials, recyclable packaging, refillable containers, and fiber-based cartons as manufacturers respond to tightening environmental regulations and brand sustainability targets. Major companies such as Amcor plc, Tetra Pak, SIG, and Elopak are increasingly investing in circular packaging technologies and recyclable beverage container solutions to strengthen their market position. In February 2026, Amcor plc announced that its polypropylene beverage cups achieved “Widely Recyclable” certification across the U.S., reflecting the growing industry emphasis on recyclable beverage packaging infrastructure.

High level of investment in packaging innovation, production expansion, and strategic collaborations aimed at meeting evolving regulatory and consumer requirements, are boosting the market growth. Companies are focusing on high-barrier recyclable films, fiber-based packaging systems, and reusable container programs to enhance sustainability and operational efficiency. For instance, in March 2026, Amcor plc expanded its Italy facility to increase production of recycle-ready packaging solutions aligned with upcoming European packaging regulations. Additionally, Tetra Pak collaborated with Sunware in February 2026 to convert recycled beverage carton materials into new circular consumer products, highlighting the industry’s accelerating shift toward closed-loop packaging systems and circular economy initiatives.

Material Insights

The plastic segment dominated the market in 2025, accounting for 39.8% of the total market share, due to its lightweight properties, cost-effectiveness, durability, and strong compatibility with high-volume beverage applications. PET and HDPE containers continue to witness widespread adoption across carbonated drinks, bottled water, dairy products, juices, and ready-to-drink beverages due to their excellent barrier performance and transportation efficiency. In addition, advancements in recycled PET (rPET), lightweight bottle designs, and improved recyclability are supporting continued demand for plastic beverage containers despite increasing environmental scrutiny. Beverage manufacturers also prefer plastic packaging for its design flexibility, convenience, and lower logistics costs compared to glass and metal alternatives.

The paper & paperboard segment is gaining traction in the market due to rising sustainability initiatives, increasing restrictions on single-use plastics, and growing consumer preference for renewable and recyclable packaging materials. Beverage companies are increasingly adopting paper-based cartons, fiber bottles, and paper cups to strengthen their environmental commitments and reduce carbon footprints. Technological advancements in barrier coatings, moisture resistance, and aseptic carton packaging are further improving the performance and shelf life of paper-based beverage containers. Additionally, major packaging manufacturers are investing in recyclable, fiber-based packaging innovations to align with circular-economy goals and evolving regulatory standards across North America and Europe.

Container Type Insights

The bottles & jars segment dominated the market in 2025, accounting for 41.6% of the total market share, due to its extensive use across bottled water, carbonated soft drinks, juices, alcoholic beverages, dairy products, and functional beverages. Strong demand for PET bottles, glass bottles, and rigid plastic jars is driven by their durability, product protection, ease of transportation, and compatibility with high-speed filling operations. In addition, bottles and jars offer strong branding and shelf-appeal advantages through customizable shapes, labeling, and transparency features. The segment also benefits from increasing adoption of recyclable PET, lightweight packaging technologies, and refillable glass container systems across both developed and emerging markets.

The pouches segment is gaining momentum and is projected to expand at the fastest rate over the forecast period. Growth is being driven by rising demand for lightweight, portable, and cost-efficient beverage packaging formats. Flexible pouches are increasingly used for juices, energy drinks, dairy beverages, baby drinks, and functional beverages due to their convenience, lower material consumption, and reduced transportation costs. Growing consumer preference for on-the-go consumption and single-serve packaging is further accelerating adoption across retail and foodservice channels. Moreover, advancements in recyclable mono-material pouches and high-barrier flexible packaging technologies are supporting the segment’s growth as beverage brands focus on sustainability and packaging innovation.

End Use Insights

The non alcoholic beverages segment dominated the market in 2025, accounting for 78.1% of total demand, driven by the large-scale consumption of bottled water, carbonated soft drinks, juices, dairy beverages, energy drinks, tea, coffee, and functional beverages across global markets. Rising urbanization, changing consumer lifestyles, and increasing demand for convenient ready-to-drink products continue to support strong packaging requirements in this segment. In addition, growing health awareness has accelerated demand for fortified beverages, flavored water, plant-based drinks, and low-sugar beverage products, further increasing the need for innovative and sustainable beverage containers. For instance, according to the latest beverage outlook published by Kearney in April 2026, rising demand for health-focused beverages and ongoing packaging innovations are significantly transforming global beverage consumption trends.

The alcoholic beverages segment is witnessing steady growth due to the rising global consumption of beer, wine, spirits, ready-to-drink cocktails, and premium alcoholic beverages. Increasing demand for premium packaging, product differentiation, and enhanced shelf appeal is driving the adoption of glass bottles, aluminum cans, and specialty beverage containers across the segment. The expansion of craft breweries, flavored alcoholic beverages, and canned cocktail categories is also driving higher global packaging demand. In addition, beverage manufacturers are increasingly focusing on sustainable packaging materials, lightweight glass bottles, and recyclable metal cans to meet evolving environmental regulations and consumer preferences for eco-friendly packaging solutions. Supporting this trend, Ball Corporation announced in 2026 that its North American aluminum can production capacity for the year had already been fully committed due to strong demand from beverage companies, particularly in alcoholic and ready-to-drink beverage categories.

Regional Insights

Asia Pacific dominated the market in 2025 due to rapid urbanization, an expanding middle-class population, rising packaged beverage consumption, and strong manufacturing capabilities across emerging economies. The region benefits from increasing demand for bottled water, carbonated soft drinks, dairy beverages, and ready-to-drink tea and coffee products, particularly in countries such as China, India, Japan, and Southeast Asian nations. Moreover, the presence of large-scale packaging manufacturers, low production costs, and growing investments in sustainable packaging technologies continue to strengthen regional market growth.

China Beverage Container Market Trends

China represents a key market within the Asia Pacific region, driven by its massive beverage production industry, strong domestic consumption, and expanding e-commerce and food delivery sectors. Rising demand for convenient packaged beverages, functional drinks, and premium bottled products has significantly increased the need for plastic bottles, aluminum cans, carton packaging, and glass containers. Furthermore, government initiatives promoting recyclable packaging materials and the country’s large-scale investments in advanced manufacturing infrastructure are accelerating innovation and production expansion in the beverage container industry.

North America Beverage Container Market Trends

North America accounted for 24.4% of the market in 2025, supported by high consumption of packaged beverages, strong demand for sustainable packaging solutions, and widespread adoption of advanced beverage packaging technologies. The region has witnessed increasing use of recyclable aluminum cans, lightweight PET bottles, and paper-based beverage cartons as beverage manufacturers focus on reducing environmental impact and complying with sustainability regulations. In addition, the growing popularity of ready-to-drink beverages, energy drinks, and functional beverages continues to support strong packaging demand across the region.

The U.S. beverage container market plays a central role in regional market growth, driven by the presence of leading beverage companies, strong innovation in packaging materials, and high consumer demand for convenience-oriented beverage products. The country is witnessing rising investments in recycling infrastructure, recycled PET production, and aluminum can manufacturing to support circular economy goals. In addition, growing consumption of bottled water, premium beverages, canned cocktails, and plant-based drinks is accelerating demand for innovative and sustainable beverage containers across retail and foodservice channels.

Europe Beverage Container Market Trends

Europe accounted for 22.8% of the market in 2025, supported by stringent environmental regulations, strong recycling systems, and increasing adoption of circular packaging solutions across the beverage industry. The region has been at the forefront of sustainable packaging innovation, with beverage manufacturers and packaging companies investing heavily in reusable glass bottles, recyclable cartons, fiber-based packaging, and recycled plastic containers. Furthermore, rising consumer preference for environmentally responsible products and strict European Union regulations on single-use plastics are encouraging the transition toward eco-friendly beverage container solutions.

Key Beverage Container Company Insights

The competitive environment of the beverage container market is moderately fragmented, characterized by the presence of global packaging manufacturers, container solution providers, and regional packaging companies. Key players compete on the basis of sustainability innovation, material efficiency, lightweight packaging technologies, production capacity, and advanced recycling capabilities. The market is witnessing increasing competition through strategic partnerships, production expansions, acquisitions, and investments in recyclable, reusable, and fiber-based beverage packaging solutions, which continue to reshape the competitive landscape.

-

In April 2026, Ardagh Glass Packaging‑North America has launched a new 275 ml flint (clear) beverage bottle co‑developed with Fitz’s Bottling Company, a leading U.S. craft soda and mixer brand, to package Fitz’s Tonic Water, Tonic Water Zero and Club Soda. The bottle is designed to showcase the product inside while enhancing shelf appeal and brand differentiation, and it is manufactured in the U.S. using 100% recyclable glass that can be endlessly recycled without loss of purity or quality.

-

In March 2025, Amcor plc introduced an industry-first 2oz retort bottle featuring its proprietary StormPanel technology, developed in collaboration with Insymmetry to address growing demand for durable and shelf-stable packaging for low-acid nutritional shots, coffee, and dairy-based beverages.

Key Beverage Container Companies:

The following key companies have been profiled for this study on the beverage container market.

- Amcor plc

- Crown Holdings

- Ball Corporation

- ALPLA

- Dart Container Corporation

- Tetra Pak

- SIG

- Elopak

- O-I Glass

- Captiva Containers

- Graham Packaging

- CCL Container

- The Cary Company

- Silgan Containers

- Kaufman Container

Competitve Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Amcor plc; Crown Holdings; Ball Corporation; ALPLA; Dart Container Corporation; Tetra Pak; SIG

- Mature players focus on high-volume manufacturing, global distribution networks, and long-term supply agreements with beverage brands.

- Invest in sustainable packaging solutions, lightweight materials, recycling infrastructure, and advanced filling technologies.

- Strong global presence, diversified product portfolios, and established relationships with multinational beverage companies.

- High production capacity and advanced automation enable cost efficiency, product consistency, and large-scale supply reliability.

- High dependence on raw material prices such as aluminum, resin, and glass increases operational cost volatility.

- Large-scale operations and legacy production systems can reduce flexibility in responding to changing consumer packaging trends.

Emerging Players: Captiva Containers; Graham Packaging; The Cary Company; Kaufman Container

- Focus on customized beverage packaging solutions, flexible production volumes, and regional customer partnerships.

- Expand through niche packaging segments, innovative container designs, and quick turnaround manufacturing services.

- Greater flexibility in serving small and mid-sized beverage brands with customized packaging requirements.

- Faster decision-making and lower operational complexity support quicker product development and market responsiveness.

- Limited financial resources restrict investments in large-scale automation, recycling capabilities, and global expansion.

- Smaller production capacity and limited geographic reach reduce competitiveness against established global manufacturers.

Beverage Container Market Report Scope

Report Attribute

Details

Market size in 2025

USD 167.6 billion

Estimated market size in 2026

USD 174.0 billion

Projected market size by 2033

USD 232.9 billion

Growth rate

CAGR of 4.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, Container Type, End Use, and Region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Key companies profiled

Amcor plc; Crown Holdings; Ball Corporation; ALPLA; Dart Container Corporation; Tetra Pak; SIG; Elopak; O-I Glass; Captiva Containers; Graham Packaging; CCL Container; The Cary Company; Silgan Containers; Kaufman Container

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Beverage Container Market Report Segmentation

This report forecasts revenue growth at the regional, and country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the beverage container market report on the basis of material, container type, end use, and region:

-

Material Outlook (Revenue, USD Billion, 2021 - 2033)

-

Plastic

-

Glass

-

Metal

-

Paper & Paperboard

-

Others

-

-

Container Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Bottles & Jars

-

Cans

-

Cartons

-

Pouches

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Non Alcoholic Beverages

-

Alcoholic Beverages

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation Analysis

Detailed assessment of the beverage container market across various regions. Country-level analysis for key markets including the U.S., China, Germany, India, Japan, and Brazil, covering production capacity, consumption trends, regulations, and demand across alcoholic and non alcoholic beverages.

Enabled identification of high-demand regions, regulatory impact assessment, and region-specific growth opportunities for capacity expansion and market entry strategies.

Cross-Segmentation

Comprehensive segmentation analysis by material, container type, and end use. Comparative assessment of plastic, glass, metal, and paper & paperboard containers across bottles & jars, cans, cartons, and pouches for both non-alcoholic beverages and alcoholic beverages. Evaluation included demand trends, packaging preferences, sustainability adoption, and application suitability across various segments.

Supported targeted product positioning, portfolio optimization, and identification of high-growth material and container combinations across alcoholic and non-alcoholic beverage applications.

Competitive Benchmarking

Benchmarking of major beverage container manufacturers based on product portfolio, geographic presence, financial performance, regional presence, production capabilities, sustainability initiatives, and strategy mapping. Comparative analysis of companies such as Amcor plc, Ball Corporation, ALPLA, and Tetra Pak.

Assisted in evaluating competitive intensity, identifying benchmark business models, and understanding strategic differentiation adopted by major industry participants.

Frequently Asked Questions About This Report

The global beverage container market size was valued at USD 167.6 billion in 2025 and is estimated at USD 174.0 billion for 2026.

The global beverage container market is expected to grow at a CAGR of 4.2% from 2026 to 2033, reaching USD 232.9 billion by 2033.

Asia Pacific dominated with a 41.6% revenue share in 2025.

The beverage container market is driven by rising consumption of packaged and ready-to-drink beverages, growing demand for sustainable packaging, increasing premium beverage launches, expanding manufacturing capacity, and advancements in lightweight packaging technologies.

The plastic segment led with a 39.8% revenue share in 2025, while the paper & paperboard segment is the fastest-growing.

The bottles & jars segment led with a 41.6% revenue share in 2025, while the pouches segment is the fastest-growing.

The non alcoholic beverages segment led with a 78.1% revenue share in 2025, while the alcoholic beverages segment is the fastest-growing.

Key players include Amcor plc; Crown Holdings; Ball Corporation; ALPLA; Dart Container Corporation; Tetra Pak; SIG; Elopak; O-I Glass; Captiva Containers; Graham Packaging; CCL Container; The Cary Company; Silgan Containers; Kaufman Container

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.