- Home

- »

- Next Generation Technologies

- »

-

Cloud API Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Cloud API Market (2026 - 2033)Report]()

Cloud API Market (2026 - 2033)

Size, Share & Trends Analysis Report By Service Model (IaaS API, PaaS API, SaaS API), By Deployment (Public Cloud, Private Cloud, Hybrid Cloud/Multi-Cloud), By Enterprise Size, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$1.7BMarket Estimate, 2026

$2.0BMarket Forecast, 2033

$6.0BCAGR, 2026–2033

17.1%Cloud API Market Summary

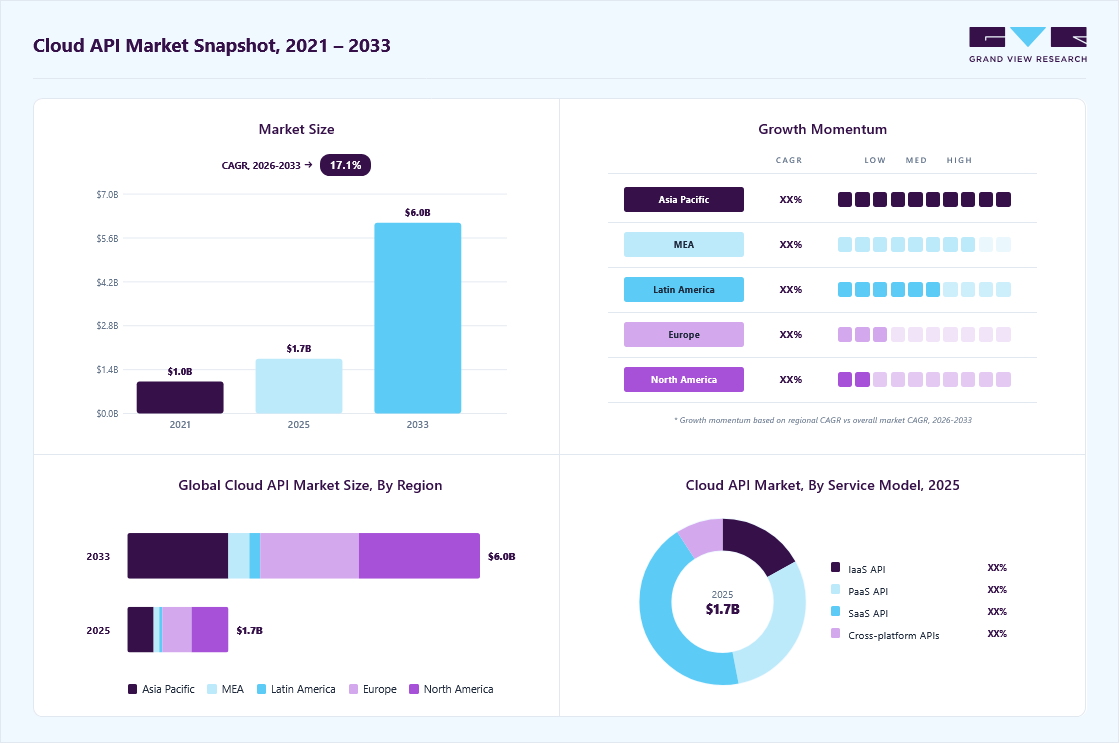

The global cloud API market size was estimated at USD 1.7 billion in 2025 and is projected to grow from USD 2.0 billion in 2026 to USD 6.0 billion by 2033, at a CAGR of 17.1% from 2026 to 2033, due to the accelerating shift toward cloud-native architectures and micro services-based application development. North America dominated the market with the largest revenue share of 36.5% in the global market in 2025.

Key Market Trends & Insights

- By service model: SaaS API held the largest market share of 43.8% in 2025.

- By deployment: Public cloud segment held the largest market share in 2025.

- By end use: IT & telecom segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (36.5% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 1.7 Billion

- Estimated market size in 2026: USD 2.0 Billion

- Projected market size by 2033: USD 6.0 Billion

- CAGR (2026-2033): 17.1%

Enterprises are decomposing monolithic systems into modular services that communicate via APIs, increasing the need for scalable, secure, and well-managed cloud APIs.As organizations modernize legacy infrastructure and adopt containerization technologies such as Kubernetes, APIs become the foundational integration layer enabling interoperability across distributed environments, thereby expanding demand for API gateways, management platforms, and developer portals.

")

The rapid expansion of digital transformation initiatives across industries also contributes to the growth of the cloud API industry. Enterprises in BFSI, healthcare, retail, manufacturing, and government sectors are digitizing customer journeys, automating workflows, and launching digital products at speed. For instance, in March 2026, Tech Mahindra and Orange Business announced to establish a five-year strategic alliance designed to fast-track comprehensive digital transformation programs for enterprise clients globally. The proposed partnership aims to advance AI-driven solutions, intelligent automation frameworks, and secure digital platforms. The collaboration is intended to deliver end-to-end transformation solutions that help enterprises modernize operations, enhance resilience, and accelerate innovation at scale.

Cloud APIs enable seamless integration between SaaS platforms, enterprise applications, mobile apps, IoT devices, and third-party ecosystems. The growing need for real-time data exchange, omnichannel engagement, and personalized user experiences significantly increases API traffic volumes and management complexity, fueling investment in cloud-based API infrastructure.

The proliferation of mobile applications, IoT deployments, and edge computing is further amplifying API consumption. Smartphones, wearable devices, connected vehicles, smart factories, and remote sensors generate continuous data streams that require cloud APIs for ingestion, processing, and analytics. As enterprises deploy IoT ecosystems at scale, API orchestration, rate limiting, and security capabilities become mission-critical, driving demand for robust cloud API solutions that ensure low latency and high availability.

Security and compliance requirements are also propelling the cloud API industry. With APIs increasingly serving as primary entry points to enterprise systems, organizations face heightened risks of API abuse, data breaches, and distributed denial-of-service (DDoS) attacks. Regulatory frameworks such as GDPR, HIPAA, PCI-DSS, and region-specific data protection laws mandate strict data governance and secure access controls. This has led to increased adoption of API authentication protocols (OAuth, OpenID Connect), encryption standards, API monitoring tools, and zero-trust architectures, strengthening the need for managed cloud API security platforms.

Market Dynamics

The increasing shift toward digital transformation initiatives, cloud computing adoption, and API-driven software architectures is a major factor driving the growth of the cloud API market. Enterprises across industries, including banking, healthcare, retail, manufacturing, telecommunications, and government, are rapidly adopting cloud-based applications, micro services, and connected digital ecosystems, creating strong demand for secure and scalable API integration solutions. The growing use of mobile applications, SaaS platforms, IoT devices, AI-powered services, and omnichannel customer engagement platforms has significantly accelerated the need for seamless real-time data exchange and interoperability across distributed enterprise environments.

In addition, several major cloud providers and enterprise software vendors expanded investments in AI-enabled API management, real-time integration platforms, and cloud-native developer ecosystems to strengthen digital transformation capabilities and improve enterprise connectivity. For instance, in December 2025, IBM Corporation enhanced its API Connect platform with AI-powered API lifecycle management, cloud-native gateway capabilities, and advanced developer tools to support agentic AI, hybrid-cloud integration, and enterprise connectivity. The updates are designed to help organizations improve API security, scalability, and digital transformation across distributed cloud environments. Such developments highlight the increasing industry focus on scalable integration, application modernization, and secure digital collaboration, thereby supporting the growth of the cloud API market.

The cloud API market faces significant challenges due to rising cybersecurity risks, complex API management requirements, and increasing concerns regarding data privacy and regulatory compliance. APIs frequently handle sensitive enterprise and customer data, making them attractive targets for cyberattacks such as API abuse, credential theft, distributed denial-of-service (DDoS) attacks, and unauthorized access attempts. As organizations expand interconnected cloud ecosystems, managing API authentication, encryption, access control, and traffic monitoring across multiple platforms becomes increasingly complex and resource-intensive.

In addition, enterprises operating in regulated industries such as healthcare, banking, and government must comply with strict data protection regulations and industry-specific security standards, which may increase implementation costs and deployment complexity. Integration challenges associated with legacy systems, inconsistent API standards, vendor lock-in concerns, and interoperability limitations across hybrid-cloud and multi-cloud infrastructures further complicate adoption. The market is also characterized by rising operational costs related to API lifecycle management, continuous monitoring, version control, and performance optimization.

Market Concentration & Characteristics

The cloud API market is moderately concentrated, with the presence of major global cloud service providers, API management platform vendors, and enterprise software companies alongside emerging API-first technology firms and integration specialists. Leading companies maintain strong market positions through extensive cloud ecosystems, developer platforms, strategic enterprise partnerships, and broad API management capabilities across industries such as banking, healthcare, retail, telecommunications, manufacturing, and government. These players offer integrated solutions including API gateways, API lifecycle management, micro services orchestration, identity and access management, real-time data integration, analytics, and security platforms, creating competitive advantages through scalability, interoperability, and robust developer support. High barriers to entry arise from the need for advanced cloud infrastructure, compliance with evolving data privacy regulations, and the growing complexity of multi-cloud and hybrid-cloud environments.

In terms of market characteristics, the industry is highly technology-driven and characterized by rapid innovation in artificial intelligence, low-code/no-code integration, micro services architecture, serverless computing, and API security technologies. Rising enterprise digital transformation initiatives, increasing adoption of cloud-native applications, and growing demand for seamless system integration and real-time data exchange are major demand drivers. Moreover, the market is characterized by strong emphasis on API standardization, high scalability requirements, increasing focus on cybersecurity and API governance, and continuous demand for improved developer experience. Organizations increasingly prioritize flexible, secure, and scalable API ecosystems to accelerate application development, enable partner integrations, and support omnichannel digital services across distributed enterprise environments.

Service Model Insights

The SaaS API segment dominated the industry and accounted for a revenue share of 43.8% in 2025, driven by the rapid proliferation of SaaS applications across enterprise functions such as CRM, ERP, HRM, finance, marketing automation, and collaboration tools. As organizations adopt best-of-breed SaaS solutions rather than monolithic systems, APIs become critical for enabling seamless interoperability, workflow automation, and data synchronization across multiple cloud applications. The rise of low-code/no-code platforms and iPaaS solutions is further increasing API consumption, as business users require standardized, well-documented APIs to orchestrate processes without deep coding expertise.

The cross-platform APIs segment is anticipated to grow at the highest CAGR during the forecast period due to the growing need for consistent functionality and performance across heterogeneous operating systems, devices, and development environments. Enterprises are targeting simultaneous deployment across iOS, Android, web, desktop, smart TVs, and emerging platforms such as wearables and in-vehicle systems, creating demand for APIs that abstract platform-specific complexities and provide unified service layers.

Deployment Insights

The public cloud segment dominated the market and accounted for the largest revenue share in 2025, driven by the growing enterprise preference for asset-light IT models that convert capital expenditure into predictable operational expenditure while enabling rapid global scalability. Organizations are leveraging hyperscale infrastructure from providers such as Amazon Web Services, Microsoft Azure, and Google Cloud to access elastic compute, managed databases, serverless runtimes, and integrated AI services without maintaining physical infrastructure.

The hybrid cloud/multi-cloud segment is expected to grow at a significant CAGR during the forecast period as enterprises seek architectural resilience, regulatory flexibility, and strategic vendor diversification in increasingly complex IT environments. Organizations are distributing mission-critical workloads across private infrastructure and multiple public cloud providers to mitigate concentration risk, avoid vendor lock-in, and align data residency with jurisdictional mandates. Cross-cloud workload orchestration platforms enable consistent policy enforcement, container portability, and centralized governance across disparate environments.

Enterprise Size Insights

The large enterprise segment dominated the market and accounted for the largest revenue share in 2025 due to the scale, complexity, and integration intensity of their digital ecosystems. Multinational corporations operate across multiple business units, geographies, and regulatory environments, requiring high-throughput API infrastructures capable of handling massive transaction volumes and complex inter-application dependencies. Their focus on enterprise-wide digital governance, centralized identity management, advanced observability, and API lifecycle standardization accelerates investment in robust API management platforms.

The small & medium enterprises segment is expected to grow at a significant CAGR during the forecast period due to increasing access to plug-and-play digital infrastructure that lowers technical and financial barriers to technology adoption. SMEs are leveraging subscription-based API services with minimal upfront investment, enabling them to integrate payment gateways, logistics tracking, CRM systems, and digital marketing tools without building in-house IT teams. The growing availability of pre-built connectors and marketplace-based integrations reduces implementation complexity and accelerates deployment timelines, which is critical for resource-constrained businesses

End Use Insights

The IT & telecom segment dominated the market and accounted for the largest revenue share in 2025 due to the rapid evolution of 5G networks, network function virtualization (NFV), and software-defined networking (SDN), which rely heavily on API-driven architectures for dynamic service provisioning and orchestration. Telecom operators are exposing network capabilities-such as messaging, billing, identity verification, and location services through standardized APIs to enable developer ecosystems and value-added digital services.

The healthcare segment is expected to grow at a significant CAGR over the forecast period due to the increasing digitization of clinical, administrative, and patient engagement workflows across hospitals, diagnostics centers, insurers, and healthtech platforms. Regulatory mandates promoting electronic health records (EHR) interoperability supported by standards such as FHIR (Fast Healthcare Interoperability Resources) are driving API-based data exchange between providers, payers, pharmacies, and laboratories. The rise of telemedicine platforms, remote patient monitoring devices, and AI-assisted diagnostics requires secure, real-time API connectivity for transmitting medical data, imaging results, and treatment analytics.

Regional Insights

North America cloud API market dominated the global market with the largest revenue share of 36.5% in 2025, driven by the region’s mature digital economy and high concentration of technology innovators, hyperscale cloud providers, and API-first startups. Enterprises across fintech, e-commerce, media, and SaaS verticals increasingly design products with API-centric architectures to enable rapid partner onboarding and ecosystem expansion. The strong venture capital environment and active M&A landscape further accelerate API productization and third-party developer engagement.

U.S. Cloud API Market Trends

The cloud API market in the U.S. is expected to grow significantly at a CAGR of 15.9% from 2026 to 2033, due to a highly developed platform economy where digital marketplaces and super apps depend on scalable API infrastructures to integrate payments, logistics, identity verification, and AI services. Federal digital modernization initiatives and open data programs are encouraging standardized API adoption across public sector agencies.

Europe Cloud API Market Trends

The cloud API market in Europe is anticipated to register considerable growth from 2026 to 2033 due to stringent data sovereignty and interoperability mandates under regional regulatory frameworks, which require structured and secure cross-border data exchange. The region’s strong industrial base is integrating APIs into Industry 4.0 initiatives, enabling machine-to-machine communication and smart manufacturing ecosystems.

The U.K. cloud API market is expected to grow rapidly in the coming years, owing to banking and fintech innovation, where regulated API exposure has transformed financial service delivery. Regulatory oversight by the Financial Conduct Authority has accelerated API standardization across banking institutions, fostering competitive digital ecosystems. London’s position as a global fintech hub further stimulates API consumption across payments, regtech, and insurtech platforms.

The cloud API market in Germany held a substantial market share in 2025 due to its advanced manufacturing and automotive sectors, where APIs enable industrial automation, predictive maintenance, and connected vehicle ecosystems. The country’s emphasis on engineering precision and secure enterprise IT architecture drives demand for highly reliable and compliant API infrastructures.

Asia Pacific Cloud API Market Trends

The cloud API market in Asia Pacific held a significant share in the global market in 2025, due to rapid digital consumer adoption, super-app ecosystems, and cross-border e-commerce expansion. Emerging economies are leapfrogging traditional IT infrastructure by directly adopting cloud-native application stacks, increasing API penetration across mobile-first services. Regional digital payment ecosystems, online marketplaces, and ride-hailing platforms rely extensively on scalable APIs to handle large concurrent user bases.

The Japan cloud API market is expected to grow rapidly in the coming years, driven by enterprise modernization efforts aimed at replacing legacy mainframe systems with interoperable cloud-based architectures. Large corporations are investing in API enablement to support digital transformation across manufacturing, retail, and financial services.

The cloud API market in China held a substantial share in 2025, due to large-scale digital platforms that integrate payments, social commerce, logistics, and entertainment within unified ecosystems. Technology conglomerates such as Alibaba Group and Tencent continuously expand API capabilities to support mini-program ecosystems and third-party developer networks.

Key Cloud API Companies Insights

Key players operating in the cloud API industry are Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Corporation, Oracle Cloud, Salesforce, Inc., and Alibaba Cloud. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

Key Cloud API Companies:

The following key companies have been profiled for this study on the cloud API market.

- Amazon Web Services (AWS)

- Axway

- Broadcom (Layer7 API Management)

- Citrix Systems, Inc.

- Google Cloud

- IBM Corporation

- Kong Inc.

- Microsoft Corporation

- Oracle

- Postman, Inc.

- Red Hat (3scale)

- Salesforce (MuleSoft)

- SAP SE

- Tyk Technologies

- WSO2

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Corporation, Oracle Cloud, Salesforce, Inc., and Alibaba Cloud

- Expanding AI-enabled API management, hybrid-cloud integration, and cloud-native developer platforms.

- Investing in API security, micro services orchestration, real-time integration, and multi-cloud connectivity solutions.

- Strengthening enterprise ecosystems through low-code/no-code integration tools and API monetization platforms.

- Strong global cloud infrastructure and extensive enterprise customer base.

- Broad end-to-end portfolios covering API gateways, integration platforms, analytics, security, and developer ecosystems.

- Strong partnerships with enterprises, ISVs, telecom providers, and system integrators supporting large-scale digital transformation initiatives.

- Complex pricing structures and vendor lock-in concerns may limit customer flexibility.

- Legacy enterprise integration environments can increase migration complexity and deployment timelines.

- Large organizational structures may slow innovation and customization for niche API requirements.

Emerging Players: Citrix Systems, Inc., Salesforce, Tyk Technologies, WSO2

- Focusing on API-first architectures, lightweight API gateways, open-source platforms, and cloud-native integration solutions.

- Developing AI-driven API automation, Kubernetes-native API management, and developer-centric integration platforms.

- Expanding flexible deployment models for hybrid-cloud and multi-cloud environments.

- Faster innovation cycles and greater flexibility in addressing evolving enterprise integration needs.

- Strong specialization in API security, open-source ecosystems, microservices management, and developer experience optimization.

- Easier integration with modern cloud-native applications and DevOps workflows.

- Limited global infrastructure scale and smaller enterprise support ecosystems compared to hyperscalers.

- Dependence on partnerships and third-party cloud providers for broader market reach.

- Lower brand recognition in highly regulated and large-enterprise environments.

Recent Developments

-

In November 2025, Microsoft launched the public preview of its new Exchange Online Admin API, a REST-based, cmdlet-style interface designed to help organizations move away from legacy EWS and modernize administrative automation over HTTP. The preview introduces endpoints such as OrganizationConfig, AcceptedDomain, Mailbox, MailboxFolderPermission, DistributionGroupMember, and DynamicDistributionGroupMember, enabling streamlined management of tenant settings, mailbox properties, folder permissions, and group memberships.

-

In March 2025, Telefónica announced a collaboration with Google Cloud to streamline authentication for millions of developers by integrating Open Gateway capabilities with Google Firebase APIs. The initiative is designed to make it easier for developers to access network functions, improve API interoperability, and speed up global uptake of Open Gateway services through a more seamless and scalable integration framework.

Cloud API Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.7 billion

Estimated Market size in 2026

USD 2.00 billion

Projected Market size by 2033

USD 6.04 billion

Growth rate

CAGR of 17.1% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Service model, deployment, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Amazon Web Services (AWS); Axway; Broadcom (Layer7 API Management); Citrix Systems, Inc.; Google Cloud; IBM Corporation; Kong Inc.; Microsoft; Oracle; Postman, Inc.; Red Hat (3scale); Salesforce (MuleSoft); SAP; Tyk Technologies; WSO2

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud API Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cloud API market report based on service model, deployment, enterprise size, end use, and region:

-

Service Model Outlook (Revenue, USD Billion, 2021 - 2033)

-

IaaS API

-

PaaS API

-

SaaS API

-

Cross-platform APIs

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Public Cloud

-

Private Cloud

-

Hybrid Cloud/Multi-Cloud

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small & Medium Enterprises

-

Large Enterprise

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT & Telecom

-

Manufacturing

-

Healthcare

-

Retail & E-Commerce

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cloud API adoption assessment across enterprise verticals

- Analysis of API adoption trends across BFSI, healthcare, retail, telecom, manufacturing, and government sectors.

- Evaluation of enterprise use cases, including digital banking, omnichannel commerce, connected healthcare, and IoT integration.

- Identified high-growth industry verticals and emerging API use cases.

- Supported vertical-focused expansion and sales prioritization strategies.

- Highlighted sector-specific integration and security requirements.

AI-enabled API management opportunity analysis

- Assessment of AI integration trends in API lifecycle management, automated testing, predictive analytics, traffic optimization, and intelligent monitoring.

- Benchmarking of vendors offering AI-driven API automation capabilities.

- Identified emerging AI-driven API innovation opportunities.

- Supported strategic planning for intelligent API management solutions.

- Highlighted automation trends improving operational efficiency and developer productivity.

Cloud API opportunities in telecom and 5G ecosystems

- Assessment of API monetization opportunities linked to 5G, edge computing, and telecom network virtualization.

- Analysis of telecom operator investments in open APIs and network-as-a-service platforms.

- Identified emerging revenue streams in telecom API ecosystems.

- Supported expansion into edge computing and 5G integration markets.

- Highlighted strategic opportunities in programmable network infrastructure.

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The SaaS API segment held the market with the largest revenue share of 43.8% in 2025, while cross-platform APIs is the fastest-growing segment.

The public cloud segment held the market with the largest revenue share in 2025, while hybrid cloud/multi-cloud is the fastest-growing segment.

The large segment dominated the market with the largest revenue share in 2025, while small & medium enterprises is the fastest-growing segment.

The IT & telecom segment accounted for the largest revenue share in 2025, while healthcare is the fastest-growing segment.

North America dominated with a revenue share of 36.5% in 2025.

Key players operating in the cloud API industry are Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Corporation, Oracle Cloud, Salesforce, Inc., and Alibaba Cloud.

The rapid expansion of digital transformation initiatives across industries also contributes to the growth of the cloud API industry. Enterprises in BFSI, healthcare, retail, manufacturing, and government sectors are digitizing customer journeys, automating workflows, and launching digital products at speed.

The global cloud API market size was valued at USD 1.7 billion in 2025 and is projected to reach USD 2.0 billion in 2026.

The global cloud API market is expected to grow at a CAGR of 17.1% from 2026 to 2033, reaching USD 6.0 billion by 2033.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.