- Home

- »

- Next Generation Technologies

- »

-

Computer Vision Hardware Market Size Report, 2026-2033GVR Report cover

![Computer Vision Hardware Market Size, Share & Trends Report]()

Computer Vision Hardware Market (2026 - 2033) Size, Share & Trends Analysis Report By Processor (Graphics Processing Units (GPUs)), By Imaging Device, By Sensor, By Memory & Storage Units, By Networking Module (Wired, Wireless), By Region And Segment Forecasts

Market Size, 2025

$16.9BMarket Estimate, 2026

$20.1BMarket Forecast, 2033

$71.1BCAGR, 2026–2033

19.8%Computer Vision Hardware Market Summary

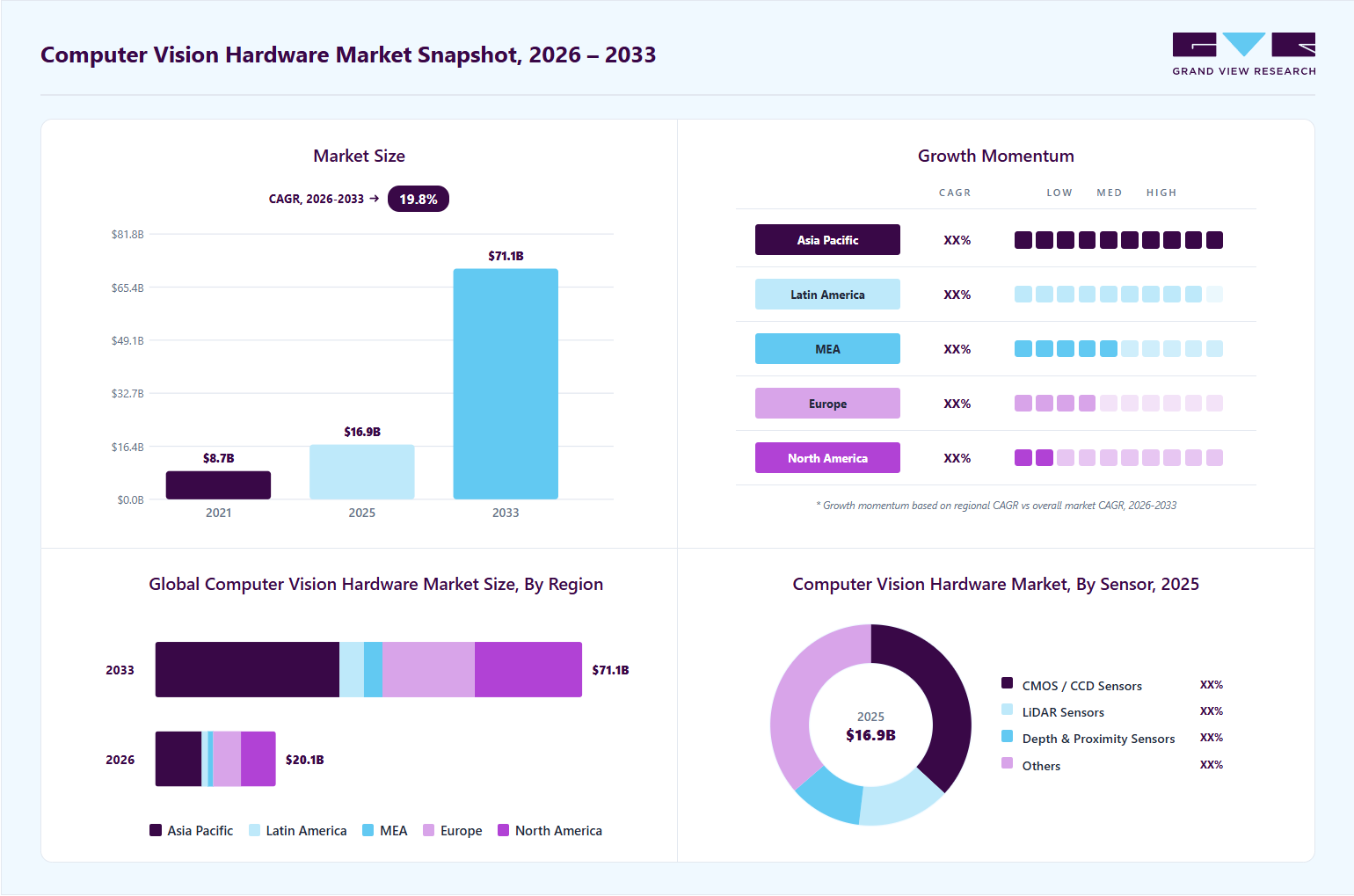

The global computer vision hardware market size was valued at USD 16.9 billion in 2025 and is projected to grow from USD 20.1 billion in 2026 to USD 71.1 billion by 2033, at a CAGR of 19.8% from 2026 to 2033. Asia Pacific dominated the global computer vision hardware industry, accounting for 37.7% of revenue in 2025. This growth is driven by the proliferation of AI and deep learning technologies across imaging and automation systems.

Key Market Trends & Insights

- The computer vision hardware market in China led the Asia Pacific market and held the largest revenue share in 2025.

- By processor, Graphics Processing Units (GPUs) led the market, holding the largest revenue share of 28.6% in 2025.

- By imaging device, the 3D cameras & stereo vision cameras segment held the dominant market position.

- By sensor, CMOS/CCD sensors held the dominant position in the market.

- By memory & storage units, high-speed DRAM held the dominant position in the market.

- By networking module, wired held the dominant position in the market.

Market Size & Forecast

- 2025 Market Size: USD 16.9 Billion

- 2033 Projected Market Size: USD 71.1 Billion

- CAGR (2026-2033): 19.8%

- Asia Pacific: Largest market in 2025

The expansion of Industry 4.0 and industrial automation is driving the deployment of machine vision hardware in manufacturing environments. Rising adoption of autonomous vehicles and advanced driver-assistance systems is accelerating demand for high-performance vision sensors.Rising demand for Physical AI is increasing across advanced sensing applications. Real-time spatial intelligence is becoming essential for autonomous systems and smart infrastructure. Industries are focusing on instant environment understanding through AI-enabled perception. This is driving the adoption of high-resolution vision and LiDAR-based hardware. It is also strengthening demand for edge-based processing and low-latency decision systems. For instance, in April 2026, Innoviz Technologies Ltd, a LiDAR technology company based in Israel, launched the InnovizTwo Ultra Long-Range LiDAR with up to 1 km sensing capability and high-resolution 3D perception. It is designed for autonomous systems, infrastructure monitoring, and security applications requiring long-range, real-time environmental awareness.

")

The market is expanding rapidly, driven by the surge in adoption of autonomous vehicles, Advanced Driver-Assistance Systems (ADAS), and intelligent transportation infrastructure. Automotive manufacturers are increasingly investing in vision-enabled hardware, AI-powered imaging systems, and high-performance sensors to improve safety, navigation, and traffic monitoring. The healthcare sector is also driving demand through medical imaging systems, diagnostic vision solutions, and robotic surgery platforms, increasing the need for high-accuracy, low-power computer vision devices. Retail and security industries are leveraging smart cameras, edge vision systems, and AI-based surveillance solutions for analytics, tracking, and safety monitoring, while smart city initiatives are further strengthening adoption for urban surveillance and regulatory compliance.

The growth of edge computing, Internet of Things (IoT), and mobile vision applications is enabling real-time data processing and low-latency decision-making at the edge. Investments from semiconductor companies, startups, and research institutions are accelerating innovation in AI-enabled vision processors, CMOS sensors, LiDAR systems, and embedded hardware solutions. Strategic collaborations across industries are supporting large-scale deployment, while government initiatives focused on digital infrastructure, industrial automation, and AI-driven safety standards are reinforcing long-term market expansion of the Computer Vision Hardware industry.

Market Dynamics

The rapid adoption of autonomous vehicles and Advanced Driver-Assistance Systems (ADAS) is a major market driver. Automotive manufacturers are increasingly integrating AI-enabled cameras, LiDAR systems, radar fusion technologies, and high-resolution image sensors to improve vehicle perception, safety, navigation, and real-time decision-making capabilities under complex driving conditions.

This growing deployment of vision-based automotive technologies is significantly increasing demand for advanced computer vision hardware with low latency, high accuracy, and strong environmental adaptability. Rising focus on collision avoidance, lane detection, pedestrian recognition, and traffic monitoring is further strengthening adoption. As the automotive industry advances toward higher levels of vehicle autonomy, the requirement for scalable, high-performance vision systems continues to accelerate market growth.

The high cost of advanced components such as LiDAR systems, high-resolution cameras, and AI-enabled processors is a key market restraint. These components require complex design, precision manufacturing, and advanced semiconductor technologies, which significantly increase overall system costs. This limits adoption in cost-sensitive applications and emerging markets.

The high pricing also impacts large-scale deployment in industries such as automotive, industrial automation, and surveillance. Organizations often face challenges balancing performance requirements with budget constraints, which slows the widespread adoption of advanced computer vision hardware solutions.

The expansion of Industry 4.0 and smart manufacturing is creating significant market opportunities. Manufacturers are increasingly deploying machine vision systems, AI-enabled cameras, high-resolution sensors, and smart imaging devices to improve production efficiency, accuracy, and operational control across automated production lines.

This is driving the adoption of automated quality inspection, defect detection, predictive maintenance, and real-time process monitoring solutions in industrial environments. Integration of IoT, robotics, and edge computing with computer vision hardware enables faster decision-making and reduces downtime. As factories become more connected and data-driven, demand for scalable, intelligent vision systems continues to grow across global manufacturing industries.

Market Concentration & Characteristics

The computer vision hardware industry is moderately fragmented with pockets of consolidation at the high end of the value chain. The advanced segment, including LiDAR systems, AI-enabled vision processors, and high-precision CMOS sensors, is dominated by a limited number of global players due to high R&D requirements, strong intellectual property barriers, and automotive-grade performance standards. These factors create a more consolidated structure among leading semiconductor and imaging technology companies.

However, the broader market for industrial cameras, machine vision systems, and edge vision devices remains highly fragmented. This is driven by numerous regional vendors and startups offering customized solutions across industries such as manufacturing, retail, healthcare, and security. The diversity of applications and rapid innovation cycles continue to support a wide supplier base, preventing strong consolidation at the overall market level.

Processor Insights

The Graphics Processing Units (GPUs) segment led the market in 2025, accounting for over 28.6% of global revenue, primarily driven by the increasing demand for high-performance computing and real-time data processing capabilities. GPUs enable parallel processing, which is critical for computer vision tasks such as image recognition, object detection, and 3D modeling. The growing adoption of artificial intelligence (AI) and deep learning algorithms across industries such as automotive, healthcare, robotics, and surveillance further fuels GPU demand. Moreover, advancements in GPU architecture, energy efficiency, and integration with edge computing devices enhance processing speed and accuracy. The surge in demand for autonomous systems, smart devices, and AI-enabled analytics continues to act as a significant growth catalyst for this segment.

The Application-Specific Integrated Circuits (ASICs)/Vision Processing Units (VPUs) segment is expected to grow the fastest over the forecast period, driven by increasing demand for high-performance, energy-efficient processing in AI and edge devices. ASICs and VPUs offer customized, low-power solutions optimized for computer vision workloads, enabling real-time image and video analysis in various sectors such as autonomous vehicles, robotics, and smart surveillance. Growing adoption of AI-driven applications, including facial recognition, object detection, and augmented reality, further fuels market growth. Moreover, rising investments in edge computing and demand for miniaturized, low-latency devices encourage manufacturers to deploy ASICs and VPUs. The combination of enhanced processing speed, reduced power consumption, and scalability positions this segment as a key enabler of next-generation computer vision solutions.

Imaging Device Insights

The 3D cameras & stereo vision cameras segment accounted for the largest market share in 2025, driven by several factors, including industrial automation and robotics increasingly relying on 3D cameras for precise quality control, assembly, and robotic guidance across industries such as automotive, electronics, and packaging. Advances in AI and deep learning enhance stereo vision systems, enabling real-time object recognition and inspection in complex environments. Consumer electronics and AR/VR applications benefit from stereo cameras for accurate depth perception, improving gaming, simulation, and medical imaging experiences. Moreover, autonomous vehicles and robotics leverage stereo vision for navigation and obstacle detection, collectively boosting demand and innovation in the computer vision hardware sector.

The 2D cameras segment has supported broader computer vision market adoption by providing a cost-efficient entry point for imaging-based automation. It has enabled wider deployment of machine vision systems across manufacturing, logistics, and security environments. The segment has helped standardize inspection and monitoring processes by integrating with existing workflows. It has also increased accessibility for organizations that do not require complex depth-based imaging solutions. Overall, it has strengthened baseline demand for computer vision hardware by enabling scalable and reliable visual inspection capabilities.

Sensor Insights

The CMOS/CCD sensors segment accounted for the largest market share in 2025, supported by their pivotal role in delivering high-quality image capture across diverse applications. CMOS sensors are increasingly preferred for their low power consumption, faster processing speeds, and cost-effectiveness, making them suitable for smartphones, consumer electronics, and automotive vision systems. Meanwhile, CCD sensors remain vital in applications that demand superior image clarity and low-light performance, such as medical imaging, industrial inspection, and scientific research. Growing adoption of automation, machine vision, and AI-driven imaging solutions further accelerates demand for these sensors, as industries require precise, reliable, and scalable imaging technologies to enhance efficiency and decision-making.

The LiDAR sensors segment is expected to grow at the highest CAGR during the forecast period, driven by rising demand for high-precision 3D mapping, depth sensing, and object detection. In the automotive sector, increasing adoption of LiDAR in advanced driver-assistance systems (ADAS) and autonomous vehicles is a key driver, as it enables accurate perception in complex environments. Moreover, industries such as robotics, industrial automation, construction, and agriculture are leveraging LiDAR for navigation, obstacle detection, and real-time spatial analysis. The expanding use in smart cities, drones, and augmented reality applications further accelerates adoption. Continuous advancements in miniaturization, cost reduction, and sensor integration strengthen the segment’s role in enhancing computer vision capabilities across diverse applications.

Memory & Storage Units Insights

The high-speed DRAM segment accounted for the largest market revenue share in 2025. The segment serves an essential function in the market by enabling fast data processing and memory access required for real-time image and video analysis. As computer vision applications in autonomous vehicles, robotics, industrial automation, and healthcare demand higher frame rates and lower latency, the need for high-speed DRAM intensifies. The growing deployment of AI-powered vision systems requires substantial memory bandwidth to efficiently handle massive datasets and deep learning workloads. Moreover, the surge in edge computing accelerates adoption, as devices must locally process visual data with high efficiency. Advancements in DRAM technology, including GDDR6 and HBM, further fuel adoption by supporting energy-efficient, high-performance vision hardware.

The graphics memory segment is expected to grow at the highest CAGR during the forecast period, primarily driven by the rising demand for high-performance computing and real-time image processing across industries such as automotive, healthcare, consumer electronics, and industrial automation. Graphics memory, particularly GDDR and HBM, plays a critical role in enabling fast data transfer, high bandwidth, and low latency, which are essential for advanced vision tasks like object recognition, 3D reconstruction, and AI-driven analytics. The proliferation of autonomous vehicles, augmented/virtual reality applications, and edge AI devices further fuels demand, as these technologies require robust memory solutions for handling large datasets and complex algorithms. Moreover, advancements in GPU architectures and increasing adoption of cloud-based vision solutions are accelerating growth in this segment.

Networking Module Insights

The wired segment accounted for the largest market revenue share in 2025, primarily due to the increasing need for high-speed, reliable, and low-latency data transmission in applications such as industrial automation, smart manufacturing, and intelligent transportation systems. Ethernet-based connectivity is widely adopted in machine vision systems for real-time data transfer between cameras, processors, and storage devices, ensuring seamless integration in Industry 4.0 environments. Moreover, the rising demand for high-resolution imaging and multi-camera setups underscores the need for robust wired networking solutions capable of handling large data volumes. Growing adoption in healthcare imaging, surveillance, and automotive ADAS systems further accelerates the market growth for wired connectivity modules.

The wireless segment is anticipated to grow at the highest CAGR during the forecast period. The segment plays a crucial role in the market by enabling seamless data transfer, real-time image processing, and device interoperability across diverse applications. Growing demand for connected devices across industries such as automotive, healthcare, manufacturing, and smart cities is driving the adoption of advanced wireless technologies, including Wi-Fi 6, 5G, and Bluetooth Low Energy (BLE). These modules support low-latency, high-bandwidth communication essential for autonomous vehicles, robotics, and IoT-enabled surveillance systems. Moreover, the growing integration of AI-powered vision solutions into edge devices underscores the need for efficient connectivity, thereby enhancing scalability, remote monitoring, and operational efficiency, thereby boosting market growth for wireless networking and connectivity modules.

Regional Insights

Asia Pacific dominated the computer vision hardware industry, accounting for over 37.7% of revenue in 2025. This dominance is supported by strong manufacturing activity and widespread adoption of large-scale automation. Expansion of electronics production and industrial robotics further strengthens demand for computer vision systems. Continuous investments in smart factories and advanced inspection technologies also strengthen the region’s market position. Increasing adoption of AI-driven vision solutions across industrial applications further reinforces regional demand.

China Computer Vision Hardware Market Trends

The computer vision hardware market in China is characterized by strong adoption across industrial automation and manufacturing environments. Demand is supported by large-scale deployment of smart factory initiatives and robotics integration. The market benefits from a well-established electronics and semiconductor manufacturing base. The increasing use of AI-enabled inspection and quality control systems is expanding their application scope.

Europe Computer Vision Hardware Market Trends

The computer vision hardware market in Europe is expected to grow over the forecast period, driven by strong industrial and automotive automation in Germany and the UK. Demand for smart cameras, sensors, and AI chips supports applications such as inspection and autonomous driving. EU initiatives such as EuroHPC and InvestAI are strengthening computing infrastructure for vision workloads. Rising adoption of edge computing enables real-time analytics across industries.

North America Computer Vision Hardware Market Trends

The computer vision hardware market in North America is driven by strong adoption across manufacturing, logistics, and security applications. The region benefits from advanced technological infrastructure and early integration of AI-enabled imaging systems. High demand for automation in the automotive and industrial sectors supports the deployment of smart cameras and sensors. Significant R&D investment by technology companies accelerates innovation in imaging hardware.

Key Computer Vision Hardware Company Insights

Some key companies in the computer vision hardware industry are Google LLC and Digimarc Corporation.

-

Google LLC is expanding its presence in the computer vision hardware ecosystem through AI-integrated imaging and edge-processing solutions. The company focuses on enhancing visual intelligence capabilities across cloud and device-based platforms. Its development efforts support applications such as object detection, image recognition, and real-time analytics. Integration of AI chips and optimized hardware-software frameworks strengthens performance efficiency.

-

Digimarc Corporation is developing computer vision technologies focused on digital watermarking and automated identification systems. The company enables machine-readable content recognition across packaging, retail, and logistics environments. Its solutions support real-time product authentication and tracking through imaging systems. Advancements in pattern recognition and embedded digital codes enhance scanning accuracy.

Key Computer Vision Hardware Companies:

The following key companies have been profiled for this study on the computer vision hardware market.

-

Cognex Corporation

-

KEYENCE CORPORATION

-

Intel Corporation

-

NVIDIA Corporation

-

Ambarella International LP

-

Basler AG

-

Sony Semiconductor Solutions Corporation

-

Teledyne Vision Solutions

-

ViTrox Corporation

-

Zivid

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Cognex Corporation; KEYENCE CORPORATION; Intel Corporation; NVIDIA Corporation

- Focus on integrated hardware, software, and AI-based vision systems

- Target large-scale industrial automation and inspection applications

- Invest heavily in R&D to improve accuracy and system performance

- Maintain strong global distribution and enterprise partnerships

- Strong brand presence and established customer base

- Broad product portfolios across vision hardware and software

- Advanced R&D capabilities and proven reliability

- Deep integration within industrial automation ecosystems

- High product and operational costs

- Slower adaptation to rapid technology shifts

- Complex product portfolios affect agility

- Longer development and deployment cycles

- Dependence on established industrial demand cycles

Emerging Players: Ambarella International LP; ViTrox Corporation; Zivid

- Focus on innovative imaging and next-generation vision technologies

- Target niche applications such as robotics and smart devices

- Use agile development for faster product upgrades and customization

- Strong focus on innovation and next-generation imaging

- Faster product development and customization capability

- Competitive pricing for specialized solutions

- Flexibility in addressing niche and new use cases

- Limited global presence and distribution scale

- Lower brand recognition in enterprise markets

- Restricted R&D and financial resources

- Narrow product portfolios focused on niche use cases

Recent Developments

-

In August 2025, EssilorLuxottica, an eyewear and optical products provider, acquired Automation & Robotics, a designer and manufacturer of automated systems used for optical lens quality control, serving both large-scale production facilities and prescription laboratories. The company applies proprietary optical metrology technologies to support lens manufacturers in implementing digital processes across production workflows.

-

In June 2025, Snap Inc., a technology and social media company, announced the launch of a standalone, AI-powered ‘Specs’, smart glasses that operate without a smartphone tether. Packing proprietary visual AI plus integrations with OpenAI, Google Gemini, and DeepSeek, this new product is a major push into computer-vision-enabled wearables.

-

In September 2024, EssilorLuxottica, an eyewear and optical products provider, extended its partnership with Meta, a technology company, through a new long-term agreement to continue collaboration into the next decade on the development of multi-generational smart eyewear. The two companies collaborated earlier and introduced two generations of Ray-Ban-branded smart glasses, which introduced wearable devices into the consumer market.

Computer Vision Hardware Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 16.9 billion

Market size value in 2026

USD 20.1 billion

Revenue forecast in 2033

USD 71.1 billion

Growth rate

CAGR of 19.8% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Processor, imaging device, sensor, memory & storage units, networking module, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Cognex Corporation; KEYENCE CORPORATION; Intel Corporation; NVIDIA Corporation; Ambarella International LP; Basler AG; Sony Semiconductor Solutions Corporation; Teledyne Vision Solutions; ViTrox Corporation; Zivid

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Computer Vision Hardware Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global computer vision hardware market report based on processor, imaging device, sensor, memory & storage units, networking module, and region:

-

Processor Outlook (Revenue, USD Billion, 2021 - 2033)

-

Graphics Processing Units (GPUs)

-

Central Processing Units (CPUs)

-

Field-Programmable Gate Arrays (FPGAs)

-

Application-Specific Integrated Circuits (ASICs)/ VPUs (Vision Processing Units)

-

Others

-

-

Imaging Device Outlook (Revenue, USD Billion, 2021 - 2033)

-

2D Cameras

-

3D Cameras & Stereo Vision

-

Infrared / Thermal Cameras

-

Others

-

-

Sensor Outlook (Revenue, USD Billion, 2021 - 2033)

-

CMOS / CCD Sensors

-

LiDAR Sensors

-

Depth & Proximity Sensors

-

Others

-

-

Memory & Storage Units Outlook (Revenue, USD Billion, 2021 - 2033)

-

High-speed DRAM

-

Flash and SSD storage

-

Graphics Memory

-

Others

-

-

Networking Module Outlook (Revenue, USD Billion, 2021 - 2033)

-

Wired

-

Wireless

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

KSA

-

South Africa

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

Some key players operating in the computer vision hardware market include Cognex Corporation; KEYENCE CORPORATION; Intel Corporation; NVIDIA Corporation; Ambarella International LP; Basler AG ; Sony Semiconductor Solutions Corporation; Teledyne Vision Solutions; ViTrox Corporation ; and Zivid.

Key factors that are driving the computer vision hardware market growth include the proliferation of AI & deep learning, expansion of industry 4.0 & Automation, surge in autonomous vehicles & ADAS.

The 3D Cameras & Stereo Vision Cameras segment captured a prominent 33.2% revenue share in 2025 and is also the fastest-growing segment.

CMOS/CCD Sensors accounted for the largest share at 36.9% in 2025, while LiDAR Sensors represented the fastest-growing segment.

High-speed DRAM captured a prominent revenue share of 27.2% in 2025, while Graphics Memory is the fastest-growing segment.

The global computer vision hardware market size was estimated at USD 16.9 billion in 2025 and is expected to reach USD 20.1 billion in 2026.

The global computer vision hardware market is expected to grow at a compound annual growth rate of 19.8% from 2026 to 2033 to reach USD 71.1 billion by 2033.

Asia Pacific dominated the computer vision hardware market with a share of 37.7% in 2025. This is attributable to strong semiconductor manufacturing, rapid automation adoption, and large investments in AI-driven imaging and robotics infrastructure.

The GPUs (Graphics Processing Units) segment held a prominent revenue share of 28.6% in 2025, while ASICs / VPUs (Vision Processing Units) is the fastest-growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.