- Home

- »

- Advanced Interior Materials

- »

-

Copper In Data Centers Market Size Report, 2026-2033GVR Report cover

![Copper In Data Centers Market (2026 - 2033)Report]()

Copper In Data Centers Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (Power Infrastructure, Cooling Systems, Networking & IT Infrastructure), By Type (Hyperscale, Colocation, Edge), By Region, And Segment Forecasts

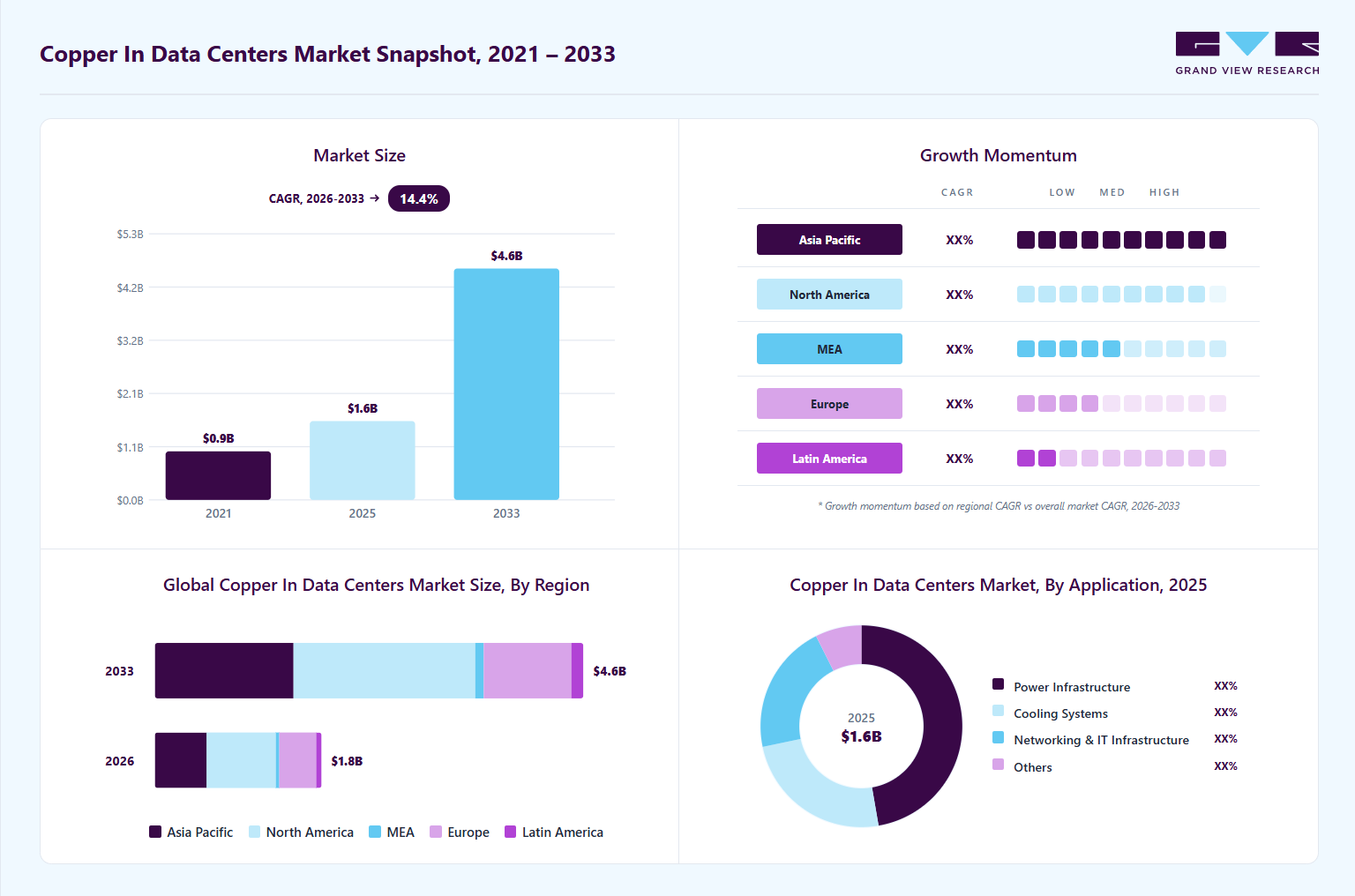

Market Size, 2025

$1.6BMarket Estimate, 2026

$1.8BMarket Forecast, 2033

$4.6BCAGR, 2026–2033

14.4%Copper In Data Centers Market Summary

The global copper in data centers market size was valued at USD 1.6 billion in 2025 and is projected to grow from USD 1.8 billion in 2026 to USD 4.6 billion by 2033, at a CAGR of 14.4% from 2026 to 2033. The market in North America dominated with a revenue share of 41.4% in 2025.

Key Market Trends & Insights

- By application: Power infrastructure segment held the largest market share of 47.3% in 2025.

- By type: Hyperscale segment held the largest market share of 51.7% in 2025.

Regional Highlights

- Largest regional market: North America (41.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 1.6 Billion

- Estimated market size in 2026: USD 1.8 Billion

- Projected market size by 2033: USD 4.6 Billion

- CAGR (2026-2033): 14.4%

This market is experiencing significant growth, driven by the rapid expansion of hyperscale and colocation data centers, increasing deployment of AI-focused computing infrastructure, and rising demand for high-performance cloud services globally. Technological advancements in hyperscale computing, artificial intelligence (AI), and high-density server architecture are significantly transforming the market. The growing adoption of liquid cooling technologies, direct-to-chip cooling systems, and high-efficiency power distribution architectures is further increasing copper utilization, as copper offers superior thermal and electrical conductivity. The increasing adoption of edge computing infrastructure, 5G-enabled data processing facilities, and modular data center architectures is driving demand for compact, high-performance connectivity systems across networking and power management applications.")

Sustainability and energy efficiency initiatives are becoming key strategic priorities across the market as operators seek to reduce carbon emissions, improve power utilization effectiveness (PUE), and support long-term environmental targets. Copper plays a critical role in enabling energy-efficient electrical transmission and thermal management systems within data centers due to its high conductivity, recyclability, and durability. The increasing deployment of renewable energy-powered facilities, advanced cooling systems, and smart power distribution architectures is supporting greater adoption of copper-intensive infrastructure designed to minimize energy losses and improve operational reliability.

Market Dynamics

The rapid expansion of hyperscale data centers, artificial intelligence (AI) infrastructure, and cloud computing platforms is a major market driver, as copper remains a critical material in power transmission, cooling systems, networking infrastructure, and electrical distribution applications. In addition, copper-intensive thermal management systems are increasingly deployed in AI-ready facilities due to rising rack power density and the growing adoption of GPU clusters for machine learning, generative AI, and high-performance computing applications.

The rapid increase in cloud service adoption, edge computing deployment, 5G infrastructure expansion, and hyperscale facility investments is significantly increasing demand for advanced copper-based electrical infrastructure globally. Growing investments in AI data centers and colocation facilities are further driving market growth, as demand for efficient power management, low-latency connectivity, and high-performance cooling systems continues to grow. The increasing focus on energy-efficient digital infrastructure, renewable-powered data centers, and intelligent power distribution technologies is expanding the use of specialty copper components across modern data center ecosystems.

Copper price volatility and high infrastructure deployment costs remain major restraints affecting the market. Fluctuations in global copper prices, mining supply disruptions, geopolitical uncertainties, and refining capacity constraints significantly impact the cost structure of manufacturers supplying cables, busbars, connectors, cooling systems, and electrical infrastructure components to data center operators. Since refined copper is a primary input across power distribution and networking systems, instability in copper pricing directly affects infrastructure procurement costs and overall project economics for hyperscale and colocation facilities.

Application Insights

The power infrastructure segment accounted for the largest revenue share of 47.3% in 2025, driven by extensive use of copper in transformers, switchgear systems, power distribution units (PDUs), busbars, backup power systems, and electrical cabling infrastructure in data centers. Modern hyperscale and colocation facilities require highly reliable and energy-efficient power architectures capable of supporting high-density AI workloads and uninterrupted operations. The growing expansion of hyperscale campuses and increasing rack power density are significantly increasing demand for copper-intensive power transmission and electrical distribution systems across global data center developments.

The cooling systems segment is projected to expand at the fastest CAGR of 16.3% during the forecast period, owing to the rising adoption of liquid-cooling technologies, direct-to-chip cooling systems, and advanced thermal management infrastructure in AI-ready and high-performance computing facilities. The increasing deployment of GPU-intensive AI clusters is generating substantially higher heat loads, driving demand for copper-based heat exchangers, cooling pipes, and thermal-conductivity components. In addition, the shift toward energy-efficient cooling architectures and sustainable data center operations is expected to further strengthen copper demand across next-generation cooling infrastructure applications.

Type Insights

The hyperscale segment accounted for the largest revenue share of 51.7% in 2025, owing to the rapid expansion of large-scale cloud computing infrastructure and AI-driven data processing facilities globally. Hyperscale data centers require extensive copper-intensive electrical systems, including high-capacity power cables, transformers, switchgear, busbars, structured cable networks, and advanced grounding infrastructure to support massive computing workloads and uninterrupted power delivery. Major cloud service providers such as Amazon Web Services, Microsoft, and Google continue investing heavily in hyperscale campuses across North America, Europe, and the Asia Pacific, significantly driving copper consumption across digital infrastructure ecosystems.

The edge data center segment is projected to register the fastest CAGR of 18.3% over the forecast period, driven by increasing demand for low-latency computing, real-time data processing, IoT connectivity, and 5G-enabled digital services. Edge facilities require localized power distribution systems, high-speed networking infrastructure, and compact cooling architectures, all of which rely heavily on copper-based components and connectivity. Growing deployment of edge infrastructure across smart cities, autonomous mobility networks, industrial automation, and telecom applications is expected to further accelerate demand for copper-intensive electrical and networking solutions globally.

Regional Insights

North America held the largest global revenue share of 41.4% in the copper in data centers market in 2025. North America represents the largest regional market for copper consumption in data center applications, driven by extensive hyperscale and AI infrastructure deployment across the U.S. and Canada. The region benefits from the strong presence of major cloud service providers such as Amazon Web Services, Microsoft, Google, and Meta Platforms, which continue to invest in high-density AI-ready facilities that require significant copper usage for power distribution, liquid cooling systems, and structured cabling.

U.S. Copper In Data Centers Market Trends

The copper in data centers market in the U.S. dominates North America owing to its leadership in hyperscale cloud infrastructure, AI computing investments, and colocation capacity expansion. Northern Virginia remains the world’s largest data center hub, while states such as Texas, Arizona, Ohio, and Georgia are witnessing substantial investments in AI-oriented data center campuses. Companies including Digital Realty, Equinix, and CyrusOne are expanding high-capacity facilities requiring extensive copper wiring, grounding systems, and power infrastructure.

Asia Pacific Copper In Data Centers Market Trends

The copper in data centers market in the Asia Pacific is the fastest-growing regional market due to rapid digitalization, cloud adoption, AI infrastructure expansion, and increasing colocation investments across China, India, Japan, Singapore, and Southeast Asia. China remains a major contributor, driven by strong hyperscale development and government-backed digital infrastructure initiatives, while India is emerging as a key growth market, supported by rising internet penetration and cloud investments. The region is witnessing strong demand for copper power cables, structured cabling systems, and thermal management infrastructure as high-density computing environments become more prevalent.

Europe Copper In Data Centers Market Trends

The copper in data centers market in Europe is supported by increasing investments in sustainable digital infrastructure, cloud computing, and regional data sovereignty initiatives. Countries including Germany, the UK, France, the Netherlands, and Ireland are major contributors to regional data center capacity additions. The region emphasizes energy-efficient infrastructure and low-carbon electrification, which drive demand for advanced copper cabling and power management solutions.

Latin America Copper In Data Centers Market Trends

The copper in data centers market in Latin America is experiencing gradual growth, driven by rising cloud infrastructure investments and increasing colocation demand in countries such as Brazil, Mexico, and Chile. Global cloud providers are increasing regional infrastructure investments to improve latency and data localization capabilities. The expansion of interconnected digital infrastructure and the increasing adoption of advanced power and cooling systems are driving higher copper demand for electrical wiring, networking cables, and backup power infrastructure in regional facilities.

Middle East & Africa Copper In Data Centers Market Trends

The copper in data centers market in MEA is growing steadily due to increased investments in smart city initiatives, digital transformation programs, and regional expansion of cloud infrastructure. Countries including the UAE, Saudi Arabia, and South Africa are emerging as important markets for hyperscale and colocation data center developments. Government-led digital economy initiatives and rising adoption of AI and cloud computing technologies are accelerating investments in modern data center infrastructure.

Key Copper In Data Centers Company Insights

Some of the key players operating in the market include Prysmian Group, Nexans, and others.

-

Prysmian Group is an Italy-based cable manufacturing company founded in 1879 and headquartered in Milan, Italy. The company specializes in power transmission cables, telecom cables, optical fiber systems, and copper-based structured cabling solutions used across energy, industrial, and digital infrastructure applications. They are a major supplier of copper power cables, copper conductors, and structured cabling systems for hyperscale and colocation data centers. The company is recognized for its global manufacturing footprint, advanced cable engineering capabilities, and strong presence in high-performance electrical and communication infrastructure markets.

-

Nexans is a France-based electrification and cable manufacturing company founded in 2000 and headquartered in Paris, France. The company specializes in copper and fiber-optic cable systems, electrification solutions, and advanced wiring infrastructure for energy, industrial, telecommunications, and data center applications. Nexans supplies copper conductors, structured copper cabling systems, and electrical distribution components used in hyperscale and enterprise data center facilities.

-

Southwire Company is a U.S.-based wire and cable manufacturer founded in 1950 and headquartered in Carrollton, Georgia. The company manufactures copper and aluminum wire products, power cables, building wire systems, and electrical components used in utility, industrial, construction, and data center applications. It supplies copper building wire, grounding systems, and power distribution cables used in data center electrical infrastructure and backup power systems.

Key Copper In Data Centers Companies

The following key companies have been profiled for this study on the copper in data centers market.

-

Furukawa Electric Co., Ltd.

-

Hubbell Incorporated

-

Legrand

-

LS Cable & System

-

Nexans

-

nVent Electric plc

-

Panduit Corporation

-

Prysmian Group

-

Southwire Company

-

Sumitomo Electric Industries Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Furukawa Electric Co., Ltd., Legrand, LS Cable & System, Nexans, Prysmian Group, Southwire Company, Sumitomo Electric Industries, Ltd.

- Mature participants primarily focus on large-scale cable manufacturing, vertically integrated copper processing, advanced electrification technologies, and long-term supply partnerships with hyperscale, industrial, and utility customers.

- These companies are increasingly investing in high-performance structured cabling systems, energy-efficient power infrastructure, AI-ready data center connectivity solutions, and sustainable manufacturing technologies to strengthen their position in high-growth digital infrastructure applications.

- Established companies benefit from strong global manufacturing footprints, integrated supply chains, extensive distribution networks, advanced electrical engineering expertise, and high-volume production capabilities.

- Their ability to deliver reliable copper-intensive power cables, busbar systems, and structured connectivity infrastructure for hyperscale and colocation facilities enables strong long-term relationships with cloud providers, EPC contractors, and data center operators globally.

- Despite their strong market position, mature companies face challenges including volatile copper prices, rising energy and logistics costs, high capital investment requirements, and strict environmental regulations associated with cable manufacturing and metal processing.

- In addition, supply chain disruptions, geopolitical uncertainties, and increasing pricing pressure from regional manufacturers may affect operational profitability and long-term expansion strategies.

Emerging Players: Hubbell Incorporated, nVent Electric plc, Panduit Corporation

- Emerging market participants are focusing on specialized electrical infrastructure systems, intelligent power management solutions, structured cabling technologies, and high-performance grounding and connectivity products for modern data center facilities.

- These companies emphasize product innovation, modular infrastructure solutions, operational flexibility, and strategic collaborations with data center developers and infrastructure integrators to expand their presence in high-growth digital infrastructure applications.

- Emerging companies benefit from strong specialization in niche electrical infrastructure applications, faster product customization, and targeted innovation strategies that support evolving hyperscale and edge data center requirements.

- Their focused expertise in grounding systems, rack-level power distribution, connectivity infrastructure, and intelligent monitoring technologies enables rapid adaptation to changing customer requirements and AI-driven infrastructure trends.

- Emerging participants face limitations related to a comparatively smaller global manufacturing scale, lower vertical integration in copper processing, dependence on external raw material suppliers, and relatively narrower international distribution networks compared with those of large multinational cable manufacturers.

- In addition, intense competition from established electrification companies and fluctuations in copper prices may limit long-term margin expansion and opportunities for large-scale infrastructure penetration.

Recent Developments

-

In February 2026, Nexans announced a framework agreement valued at approximately USD 650 million with Enedis to support the modernization and expansion of France’s medium-voltage power network. The agreement includes investments to increase low-carbon cable manufacturing capacity across Europe. The development is significant for the market as expanding electrical grid infrastructure and medium-voltage cable production directly support rising power transmission requirements associated with hyperscale and AI-driven data center facilities, which require extensive copper-based power distribution systems.

-

In March 2026, Southwire Company announced a strategic investment in Verdigris Technologies, an AI-native electrical intelligence company specializing in AI-scale data center infrastructure and advanced power delivery optimization systems. The investment highlights Southwire’s focus on next-generation electrical infrastructure solutions supporting high-density AI and hyperscale data centers. The development is relevant to the market because AI-focused facilities require significantly higher copper usage across power cables, busbars, grounding systems, and electrical monitoring infrastructure to manage elevated rack power density and energy loads.

Copper In Data Centers Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.6 billion

Estimated market size in 2026

USD 1.8 billion

Projected market size by 2033

USD 4.6 billion

Growth rate

CAGR of 14.4% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, Volume in Kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, competitive landscape, growth factors, and trends

Segments covered

Application, type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S., Canada; Mexico; Germany; France; UK; Netherlands; China; India; Japan; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Furukawa Electric Co., Ltd.; Hubbell Incorporated; Legrand; LS Cable & System; Nexans; nVent Electric plc; Panduit Corporation; Prysmian Group; Southwire Company; Sumitomo Electric Industries, Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Copper In Data Centers Market Report Segmentation

This report forecasts global, country, and regional revenue and volume growth and analyzes the latest trends in each sub-segment from 2021 to 2033. For this study, Grand View Research has segmented the global copper in data centers market report based on application, type, and region:

-

Application Outlook (Revenue, USD Million; Volume in Kilotons; 2021 - 2033)

-

Power Infrastructure

-

Cooling Systems

-

Networking & IT Infrastructure

-

Others

-

-

Type Outlook (Revenue, USD Million; Volume in Kilotons; 2021 - 2033)

-

Hyperscale

-

Colocation

-

Enterprise

-

Edge

-

Others

-

-

Regional Outlook (Revenue, USD Million; Volume in Kilotons; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Netherlands

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed country- and region-level analysis covering hyperscale expansion, colocation investments, AI infrastructure deployment, cloud computing adoption, power infrastructure development, and copper consumption trends across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Helps clients identify high-growth regional markets, evaluate infrastructure investment trends, optimize geographic expansion strategies, and assess region-specific digital infrastructure opportunities and supply chain risks.

Pricing Analysis

Comprehensive assessment of copper pricing trends, cable and component pricing structures, raw material cost fluctuations, regional price variations, and the impact of copper price volatility on data center infrastructure investments.

Enables clients to evaluate procurement risks, optimize sourcing strategies, forecast infrastructure costs, and assess the impact of raw material pricing on long-term profitability and project economics.

Opportunity Assessment

Identification of high-growth opportunities across hyperscale data centers, AI infrastructure, liquid cooling systems, edge computing facilities, high-density networking infrastructure, and renewable-powered digital infrastructure projects. Includes analysis of emerging demand trends, investment hotspots, technology adoption, and future infrastructure expansion potential.

Enables clients to prioritize high-growth application segments, evaluate future revenue opportunities, align investment strategies with evolving digital infrastructure trends, and identify emerging areas of copper demand across next-generation data center ecosystems.

Frequently Asked Questions About This Report

The global copper in data centers market size was valued at USD 1.6 billion in 2025 and is estimated at USD 1.8 billion for 2026.

The global copper in data centers market is expected to grow at a CAGR of 14.4% from 2026 to 2033, reaching USD 4.6 billion by 2033.

North America dominated with a 41.4% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Furukawa Electric Co., Ltd.; Hubbell Incorporated; Legrand; LS Cable & System; Nexans; nVent Electric plc; Panduit Corporation; Prysmian Group; Southwire Company; Sumitomo Electric Industries, Ltd.

The global copper in data centers market is primarily driven by the rapid expansion of hyperscale and AI-focused data centers, increasing cloud computing adoption, and rising investments in high-density digital infrastructure globally.

The power infrastructure segment led with a 47.3% revenue share in 2025, while the cooling systems segment is the fastest-growing.

The hyperscale segment led with a 51.7% revenue share in 2025, while the edge data center segment is the fastest-growing.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.