- Home

- »

- Advanced Interior Materials

- »

-

Copper Scrap Market Size & Share, Industry Report, 2033GVR Report cover

![Copper Scrap Market Size, Share & Trends Report]()

Copper Scrap Market (2026 - 2033) Size, Share & Trends Analysis Report By Feed Material (Old Scrap, New Scrap), By Grade (Bare Bright, #1 Copper, #2 Copper), By Application, By Region, And Segment Forecasts

Market Size, 2025

$39.6BMarket Estimate, 2026

$42.4BMarket Forecast, 2033

$78.9BCAGR, 2026–2033

9.3%Copper Scrap Market Summary

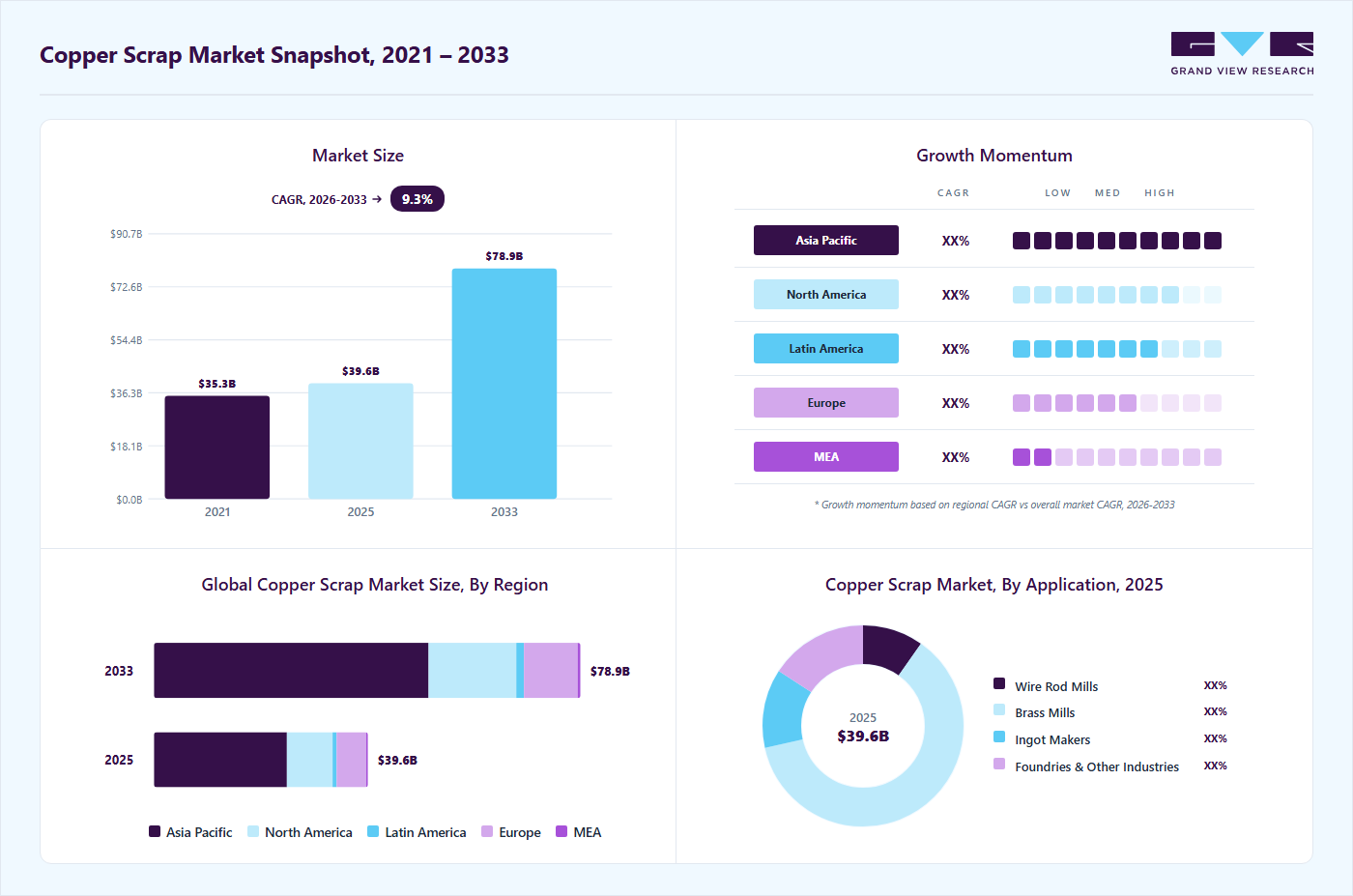

The global copper scrap market size was valued at USD 39.6 billion in 2025 and is projected to grow from USD 42.4 billion in 2026 to USD 78.9 billion by 2033, at a CAGR of 9.3% from 2026 to 2033. The Asia Pacific copper scrap market held the largest share of 49.0% of the global market in 2025. The market growth is primarily driven by the rising emphasis on metal recycling and circular economy practices, as industries increasingly utilize recycled copper to reduce production costs and energy consumption compared to primary copper extraction.

Key Market Trends & Insights

- By feed material: New scrap segment accounted for the largest market revenue share of 84.0% in 2025.

- By grade: #2 scrap segment accounted for the largest revenue share in 2025.

- By application: Ingot makers segment is projected to register the fastest CAGR of 11.3% during the forecast period.

Regional Highlights

- Largest regional market: Asia Pacific (49.0% revenue share, 2025)

- By country: The China copper scrap market held a substantial market share in Asia Pacific in 2025.

Market Size & Forecast

- Market size in 2025: USD 39.6 Billion

- Estimated market size in 2026: USD 42.4 Billion

- Projected market size by 2033: USD 78.9 Billion

- CAGR (2026-2033): 9.3%

In addition, growing demand from electrical and electronics manufacturing, construction, renewable energy infrastructure, and electric vehicles (EVs) is further driving the use of copper scrap as a sustainable raw material.The market is increasingly driven by the growing emphasis on sustainability and circular-economy initiatives across the metals and manufacturing industries. Recycling copper significantly reduces energy consumption and greenhouse gas emissions compared to primary copper extraction, making it a preferred raw material for producers seeking to lower their environmental footprint. Governments and regulatory bodies across major economies are also encouraging metal recycling through stricter environmental policies, waste management regulations, and sustainability targets. As industries such as construction, electronics, and renewable energy expand, the demand for recycled copper is rising, supporting the development of efficient scrap collection, processing, and reuse systems worldwide.

")

Technological advancements are also playing a crucial role in shaping the global copper scrap market. Innovations in sorting, separation, and refining technologies have improved the efficiency and purity levels of recycled copper, enabling manufacturers to utilize scrap metal in high-performance applications without compromising quality. Automated sorting systems, sensor-based technologies, and advanced metallurgical processes are helping recyclers recover higher volumes of usable copper from complex waste streams such as electronic scrap and industrial residues. These technological improvements are enhancing operational efficiency, reducing material losses, and strengthening the overall supply chain for recycled copper, thereby supporting long-term market growth.

Drivers, Opportunities & Restraints

The increasing global focus on sustainability and resource efficiency is a major driver of the copper scrap market, as recycled copper requires significantly less energy than primary copper production and reduces greenhouse gas emissions. Industries such as construction, electrical equipment, renewable energy, and electric vehicles are increasingly using recycled copper to secure a stable supply of raw materials while meeting environmental targets. For instance, on 24 September 2025, the German metals producer Aurubis announced the ramp-up of its USD 800 million copper recycling facility in Richmond, U.S., designed to process around 180,000 metric tons of complex copper scrap annually, reflecting the rising industrial demand for recycled copper feedstock.

Advancements in recycling and metal recovery technologies are creating significant opportunities for the copper scrap market by enabling efficient extraction of copper from complex waste streams such as electronic scrap and industrial residues. Improved metallurgical techniques, automated sorting systems, and environmentally friendly chemical processes are helping recyclers recover higher volumes of high-purity copper. A notable example occurred in February 2026, when researchers at IIT Madras developed a green solvent-based method to recover copper from electronic waste using biodegradable compounds, offering a safer and more sustainable alternative to traditional acid-based recycling processes.

One of the major restraints on the copper scrap market is volatility in scrap availability and in global copper supply chains. Fluctuations in primary copper production, trade flows, and scrap collection rates can lead to inconsistent feedstock supply for recyclers, affecting operational efficiency and pricing stability. In addition, rising competition among recyclers and smelters for high-quality scrap can increase procurement costs. For instance, on 26 September 2025, JX Advanced Metals announced plans to expand its recycled-materials processing capacity due to the tightening supply of recyclable feedstock and declining margins in traditional smelting operations, highlighting the challenges of securing stable scrap inputs.

Feed Material Insights

The new scrap segment accounted for the largest revenue share in 2025, primarily due to its consistent quality, high copper purity, and direct availability from manufacturing and industrial processes such as metal fabrication, wire production, and machining operations. New scrap, also known as prompt scrap, requires minimal processing before being reintroduced into the production cycle, making it a preferred raw material for smelters and refiners. Its reliable supply from industrial activities and lower contamination levels support its dominant share in the copper scrap market.

Old scrap segment is expected to witness the fastest growth during the forecast period, driven by increasing recovery of copper from end-of-life products such as electrical wiring, electronic equipment, construction materials, and automotive components. The growing emphasis on urban mining, expansion of electronic waste recycling programs, and rising investments in advanced scrap-sorting and recovery technologies are improving the efficiency of extracting copper from obsolete products. As global sustainability initiatives strengthen and recycling infrastructure expands, the collection and processing of old scrap are anticipated to increase significantly, supporting its rapid market growth.

Grade Insights

The #2 scrap segment accounted for the largest revenue share in 2025, primarily due to its wide availability and extensive use in recycling operations. This grade includes copper with slight impurities, such as solder, paint, or coatings, and is commonly sourced from construction waste, plumbing materials, and electrical components. Despite requiring additional refining compared to higher-purity grades, its abundant supply and lower procurement cost make it a preferred feedstock for smelters and secondary copper producers, thereby supporting its dominant share in the global copper scrap market.

Bare bright scrap segment is expected to register the fastest CAGR during the forecast period, driven by its superior purity level, typically above 99% copper content, which allows it to be directly reused in high-quality electrical and industrial applications. The increasing demand for high-conductivity copper in power transmission systems, electronics manufacturing, and renewable energy infrastructure is encouraging recyclers and manufacturers to prioritize high-grade scrap such as bare bright copper. As industries focus on improving material efficiency and reducing refining costs, the demand for premium scrap grades is expected to grow steadily in the coming years.

Application Insights

The brass mills segment accounted for the largest revenue share in 2025, primarily due to the extensive use of recycled copper in the production of brass alloys used across plumbing fixtures, industrial components, electrical fittings, and decorative applications. Brass mills rely heavily on copper scrap as a cost-effective raw material for manufacturing sheets, rods, and tubes of consistent quality. The strong demand for brass products in construction, manufacturing, and consumer goods industries has driven large-scale copper scrap consumption by brass mills, contributing to the dominant market share.

Ingot makers segment is expected to register the fastest CAGR during the forecast period, driven by rising demand for recycled copper ingots as feedstock for secondary metal production and foundry operations. The increasing emphasis on sustainable metal production and the growing availability of scrap materials are encouraging smelters and recyclers to expand ingot manufacturing capacity. Moreover, copper ingots are widely used in downstream industries such as electrical equipment, automotive components, and machinery manufacturing, furthering the growth of the ingot maker segment.

Regional Insights

North America copper scrap marketis driven by robust recycling infrastructure, rising demand for secondary copper in manufacturing, and expanding sustainability initiatives across the region. The presence of established scrap collection networks and advanced recycling facilities supports efficient recovery and processing of copper scrap. Rising investments in renewable energy systems, electric vehicle manufacturing, and power grid modernization are also increasing the demand for recycled copper. Additionally, stringent environmental regulations encouraging metal recycling and resource efficiency are further supporting the growth of the copper scrap market across North America.

U.S. Copper Scrap Market Trends

The U.S. accounts for the largest share of the market in North America, driven by its well-developed recycling ecosystem and high copper consumption across industries such as construction, electrical equipment, and electronics manufacturing. The country generates a substantial volume of copper scrap from industrial production and end-of-life products, including electrical wiring, appliances, and automotive components. Growing investments in infrastructure upgrades, expansion of renewable energy installations, and increasing adoption of electric vehicles are driving demand for recycled copper, strengthening the copper scrap market in the U.S.

Europe Copper Scrap Market Trends

Europe holds a significant market position, supported by strict environmental policies, circular-economy initiatives, and well-established recycling systems across countries such as Germany, Italy, and the UK. The region has been actively promoting sustainable resource management and reducing reliance on primary raw materials, thereby increasing the use of recycled metals in manufacturing. Additionally, strong demand from industries such as automotive, electrical equipment, and renewable energy infrastructure is driving the recycling and reuse of copper scrap across Europe.

Asia Pacific Copper Scrap Market Trends

Asia Pacific dominates the market with the largest revenue share of 62.1% in 2025 due to rapid industrialization, expanding manufacturing activities, and high copper consumption in countries such as China, India, Japan, and South Korea. The region has many copper processing and recycling facilities that utilize scrap as a key raw material for cost-efficient production. Growing investments in infrastructure development, power transmission networks, electronics manufacturing, and electric vehicle production are further increasing the demand for recycled copper, making the Asia Pacific the largest and fastest-growing regional market.

Latin America Copper Scrap Market Trends

Latin America is gradually expanding due to the growth of recycling industries and increasing awareness of sustainable resource management. Countries such as Brazil, Mexico, and Chile are witnessing rising demand for recycled copper in manufacturing and construction applications. Additionally, improvements in waste collection systems and the expansion of metal recycling facilities are supporting the recovery and reuse of copper scrap across the region, contributing to steady market growth.

Middle East & Africa Copper Scrap Market Trends

The Middle East & Africa market is experiencing moderate growth, supported by increasing infrastructure development, urbanization, and industrial expansion in countries such as the UAE, Saudi Arabia, and South Africa. The growing construction sector and rising investments in power generation and transmission projects are creating demand for copper-based materials, including recycled copper. Furthermore, gradual improvements in recycling infrastructure and government initiatives promoting waste management and resource efficiency are expected to support the development of the scrap copper market in the region.

Key Copper Scrap Company Insights

Some of the key players operating in the market include Aurubis AG, Sims Limited, and others.

-

Aurubis AG is a Germany-based global copper producer and recycler founded in 1866, operating across integrated metal processing and recycling segments with a significant presence in the global copper scrap market. The company processes complex copper scrap, electronic waste, and other recyclable materials to produce high-purity copper cathodes, copper rods, and specialty copper products used in electrical, construction, automotive, and renewable energy applications. Aurubis focuses on advanced metallurgical technologies, sustainable metal recovery, and circular economy initiatives to improve resource efficiency and reduce environmental impact. With major recycling and smelting facilities in Europe and North America, the company serves customers across global industrial supply chains.

-

Sims Limited is an Australia-based global metal recycling company founded in 1917, specializing in ferrous and non-ferrous scrap recycling, including copper scrap processing and trading. The company collects, processes, and supplies recycled metals used in steelmaking, manufacturing, electronics, and infrastructure industries. Sims Limited emphasizes sustainable resource management by recovering valuable metals from industrial scrap, end-of-life products, and electronic waste. Through its extensive network of recycling facilities, processing yards, and logistics operations across North America, Europe, and the Asia Pacific, the company plays a key role in supplying high-quality recycled copper to global manufacturing markets.

-

Schnitzer Steel Industries, Inc. is a U.S.-based metals recycling and manufacturing company founded in 1906, engaged in the collection, processing, and recycling of ferrous and non-ferrous scrap metals, including copper scrap. The company operates numerous recycling facilities that recover copper from industrial waste, obsolete equipment, and end-of-life products, supplying recycled metals to smelters, foundries, and manufacturers. Schnitzer Steel focuses on environmentally responsible recycling practices and efficient material recovery to support sustainable metal production. With a strong presence across North America and established export networks serving Asia and other international markets, the company plays an important role in the global copper scrap supply chain.

Key Copper Scrap Companies:

The following key companies have been profiled for this study on the copper scrap market.

- Aurubis AG

- Commercial Metals Company

- David J. Joseph Company

- European Metal Recycling Ltd.

- Glencore plc

- HKS Metals

- Kuusakoski Group

- OmniSource Corporation

- Schnitzer Steel Industries, Inc.

- Sims Limited

Recent Developments

-

In September 2025, Aurubis AG commenced production at its new USD 800 million copper recycling facility in Richmond, Georgia, U.S., designed to process up to 180,000 metric tons of complex copper scrap annually. The plant converts materials such as cables, printed circuit boards, and other secondary feedstock into approximately 70,000 tons of blister copper per year, strengthening North America’s copper recycling capacity and supporting the regional circular metals economy.

-

In May 2024, Sims Limited announced the expansion of its non-ferrous metal recycling operations in the U.S., aimed at increasing the recovery and processing of high-value metals such as copper and aluminum from end-of-life products and industrial scrap. The expansion focuses on advancing sorting and processing technologies to improve recovery rates and support the growing demand for recycled metals in manufacturing and infrastructure sectors.

-

In March 2024, Schnitzer Steel Industries, Inc. (now operating as Radius Recycling) announced investments to upgrade several of its North American recycling facilities with advanced metal recovery technologies. The upgrades are intended to improve the processing efficiency of ferrous and non-ferrous scraps, including copper, enabling the company to increase recycled metal output while supporting sustainable material supply for domestic and international metal manufacturing industries.

Copper Scrap Market Report Scope

Report Attribute

Details

Market definition

The market scope is limited to processed scrap, specifically copper content generated from various sources, including copper-based scrap and non-copper-based scrap.

Market size in 2025

USD 39.6 billion

Estimated market size in 2026

USD 42.4 billion

Projected market size by 2033

USD 78.9 billion

Growth rate

CAGR of 9.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Feed material, grade, application, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; Italy; Belgium; Spain; China; India; Japan; Brazil; South Africa

Key companies profiled

Aurubis AG; Commercial Metals Company; David J. Joseph Company; European Metal Recycling Ltd.; Glencore plc; HKS Metals; Kuusakoski Group; OmniSource Corporation; Schnitzer Steel Industries, Inc.; Sims Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Copper Scrap Market Report Segmentation

This report forecasts revenue and volume growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global copper scrap market based on feed material, grade, application, and region.

-

Feed Material Outlook (Revenue, USD Million; Volume, Kilotons, 2021 - 2033)

-

Old Scrap

-

New Scrap

-

-

Grade Outlook (Revenue, USD Million; Volume, Kilotons, 2021 - 2033)

-

Bare Bright

-

#1 Copper Scrap

-

#2 Copper Scrap

-

Other Grades

-

-

Application Outlook (Revenue, USD Million; Volume, Kilotons, 2021 - 2033)

-

Wire Rod Mills

-

Brass Mills

-

Ingots Makers

-

Other Applications

-

-

Regional Outlook (Revenue, USD Million; Volume, Kilotons, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

Belgium

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

-

Latin America

-

Brazil

-

-

Middle East and Africa

-

South Africa

-

-

Frequently Asked Questions About This Report

The global copper scrap market size was valued at USD 39.6 billion in 2025 and is estimated at USD 42.4 billion for 2026.

The global copper scrap market is expected to grow at a CAGR of 9.3% from 2026 to 2033, reaching USD 78.9 billion by 2033.

The brass mills segment held the largest revenue share in 2025, while the ingot makers segment is projected to register the fastest growth, expanding at a CAGR of 11.3% during the forecast period, driven by increasing demand for recycled copper feedstock in secondary metal production and cost-efficient smelting operations.

Key players include Aurubis AG; Commercial Metals Company; David J. Joseph Company; European Metal Recycling Ltd.; Glencore plc; HKS Metals; Kuusakoski Group; OmniSource Corporation; Schnitzer Steel Industries, Inc.; Sims Limited.

The copper scrap market is driven by rising demand for recycled copper in electrical equipment, construction, and electronics manufacturing industries. The increasing focus on sustainability, energy efficiency, and circular-economy practices is further accelerating the adoption of recycled copper as a cost-effective alternative to primary copper.

Asia Pacific dominated with a 49.0% revenue share in 2025.

The new scrap segment led with a 84.0% revenue share in 2025, while old scrap is the fastest-growing material.

The #2 scrap segment held the largest revenue share in 2025, while bare bright scrap is the fastest-growing grade.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.