- Home

- »

- HVAC & Construction

- »

-

Data Center Access Control Market Size Report, 2026-2033GVR Report cover

![Data Center Access Control Market Size, Share & Trends Report]()

Data Center Access Control Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Component, Hardware, Software, Services), By Control (Card-Based Access Control, Biometric Access Control), By Application, By Data Center, By Region, And Segment Forecasts

Market Size, 2025

$1.6BMarket Estimate, 2026

$1.7BMarket Forecast, 2033

$3.4BCAGR, 2026–2033

10.3%Data Center Access Control Market Summary

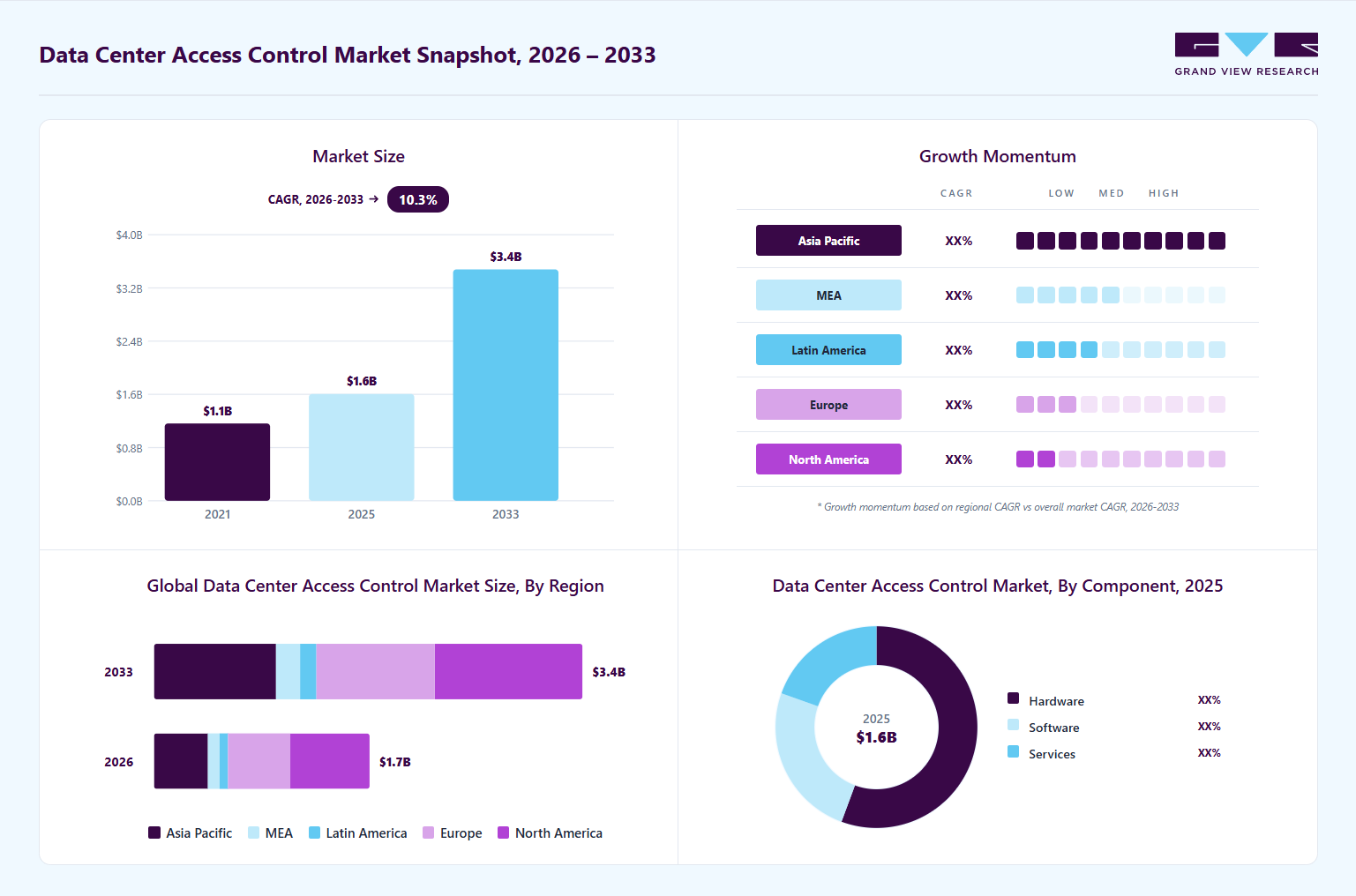

The global data center access control market size was valued at USD 1.59 billion in 2025 and is projected to grow from USD 1.73 billion in 2026 to USD 3.44 billion by 2033, at a CAGR of 10.3% from 2026 to 2033. North America dominated the global market with the largest revenue share of 37.1% in 2025. The rapid expansion of hyperscale and colocation data centers worldwide has significantly accelerated the demand for advanced access control solutions.

Key Market Trends & Insights

- The data center access control industry in the U.S. is expected to grow significantly over the forecast period.

- By component, hardware segment led the market and held the largest revenue share of 55.6% in 2025.

- By control, the card-based access control segment held the dominant position in the market and accounted for the largest revenue share in 2025.

- By application, the rack & cabinet-level security segment is expected to grow at the fastest CAGR from 2026 to 2033.

Market Size & Forecast

- 2025 Market Size: USD 1.59 Billion

- 2033 Projected Market Size: USD 3.44 Billion

- CAGR (2026-2033): 10.3%

- North America: Largest market in 2025

Cloud service providers, telecom operators, financial institutions, healthcare organizations, and government agencies increasingly require robust physical security systems to protect sensitive digital infrastructure and ensure compliance with regulatory standards such as ISO 27001, SOC 2, HIPAA, PCI DSS, and GDPR. The rapid expansion of hyperscale data centers is significantly driving demand for advanced access control solutions. Major cloud providers and AI infrastructure companies are investing heavily in large-scale facilities to support cloud computing, artificial intelligence, machine learning, and big data workloads. These hyperscale campuses store massive volumes of sensitive information and house highly valuable computing infrastructure, including AI servers and GPU clusters. As a result, operators require robust physical security systems to prevent unauthorized access, insider threats, sabotage, and data breaches. Advanced technologies such as biometric authentication, mobile credentials, intelligent surveillance integration, and multi-factor authentication are increasingly being deployed to secure facilities, critical rooms, and rack-level infrastructure within hyperscale data center environments.")

The increasing adoption of biometric and touchless authentication technologies will help market growth in the coming years. Solutions such as facial recognition, iris scanning, palm vein recognition, and mobile credentials are gradually replacing traditional card-based systems due to their higher security and operational efficiency. These technologies help reduce risks associated with lost, stolen, or shared access cards while providing stronger identity verification and faster authentication. In addition, organizations are increasingly prioritizing contactless access solutions to support workplace modernization, improve user convenience, and enhance security management. Growing investments in hyperscale, colocation, and AI-driven data centers are further accelerating the deployment of advanced touchless access control systems worldwide.

Market Dynamics

The growing adoption of edge computing is creating significant opportunities for Data Center Access control providers. Unlike traditional centralized data centers, edge facilities are typically deployed across multiple remote, distributed, or unmanned locations to support low-latency applications, 5G networks, IoT devices, and real-time data processing. Managing physical security across these geographically dispersed sites is becoming increasingly complex, driving demand for advanced cloud-managed access control systems. Technologies such as mobile credentials, biometric authentication, AI-powered surveillance, and centralized monitoring platforms enable operators to remotely manage and secure edge infrastructure efficiently. These solutions provide real-time visibility, automated threat detection, and remote access management without requiring continuous on-site personnel. As edge computing deployments continue to expand globally, the need for scalable, intelligent, and remotely managed physical security solutions is expected to grow substantially.

Cybersecurity vulnerabilities associated with connected access control systems are becoming a major concern for data center operators. Modern access control platforms are increasingly integrated with cloud infrastructure, mobile applications, IoT devices, and centralized monitoring systems to improve operational efficiency and remote management. However, these interconnected systems can become potential targets for cyberattacks, unauthorized remote access, credential theft, and identity spoofing if not properly secured. A breach in access control infrastructure can compromise both physical and digital security within critical data center environments. As a result, organizations must invest heavily in cybersecurity measures, such as encryption, secure authentication protocols, network protection, and continuous monitoring, alongside physical security systems, thereby increasing overall operational complexity and implementation costs.

Market Concentration & Characteristics

The data center access control market is moderately to highly concentrated, with a limited number of global physical security providers, access management software vendors, and integrated infrastructure companies dominating the competitive landscape. Major players possess strong competitive advantages due to their extensive product portfolios, long-standing relationships with hyperscale cloud providers and colocation operators, global service capabilities, and expertise in integrating physical security with digital infrastructure management systems. These companies typically offer comprehensive solutions that combine biometric authentication, access control hardware, Physical Identity and Access Management (PIAM) software, intelligent surveillance integration, visitor management systems, and centralized monitoring platforms. High entry barriers exist because of strict compliance requirements, cybersecurity standards, integration complexity, and the need for proven reliability in mission-critical data center environments.

In terms of market characteristics, the industry is highly security-driven and technology-intensive, with increasing emphasis on biometric authentication, touchless access technologies, AI-powered monitoring, cloud-based access management, and rack-level security solutions. Demand is primarily driven by the rapid expansion of hyperscale and colocation data centers, rising investments in AI and high-performance computing (HPC) infrastructure, growing concerns about insider threats, and increasing regulatory requirements for physical security and audit compliance. Furthermore, the market is characterized by high system integration requirements, long deployment and procurement cycles, continuous software upgrades, and strong interoperability needs between access control, surveillance, and cybersecurity systems. Operators also prioritize scalable, centralized security management platforms that can secure geographically distributed edge and multi-tenant facilities. Due to the critical nature of physical security in data centers, customers typically maintain long-term relationships with trusted vendors, resulting in high customer retention rates and relatively low switching behavior once security infrastructure is deployed.

Component Insights

The hardware segment dominated the market and accounted for the revenue share of 55.6% in 2025. The rapid growth of artificial intelligence workloads and high-performance GPU infrastructure is significantly increasing demand for advanced physical security hardware in data centers. AI training clusters and GPU-intensive facilities contain extremely valuable computing assets that require enhanced protection against unauthorized access, theft, and operational disruption. As a result, operators are increasingly deploying intelligent rack- and cabinet-level security solutions, such as electronic locks, biometric authentication devices, cabinet monitoring sensors, and real-time access-tracking systems. These technologies help ensure granular access control and improve auditability for sensitive AI infrastructure. Additionally, hyperscale cloud providers and colocation operators are investing in advanced hardware security systems to support compliance requirements and strengthen protection for mission-critical AI and HPC environments.

The software segment is anticipated to grow at the fastest CAGR during the forecast period. Organizations are increasingly adopting cloud-based access control platforms because they enable centralized management of multiple data center sites through a single interface. These solutions improve scalability by allowing operators to easily add new facilities without major infrastructure changes. They also support remote administration, enabling security teams to monitor and control access from anywhere. Continuous software updates enhance security and functionality without downtime. Additionally, real-time monitoring and alerts improve incident response times, while integration with IoT and identity systems strengthens overall visibility and control across distributed, multi-tenant data center environments.

Control Insights

The card-based access control segment dominated the market and accounted for the largest revenue share in 2025. Colocation data centers serve multiple customers within the same facility, making strict access segregation essential. Card-based access control is widely used because it enables tenant-specific permissions and zoning across shared infrastructure. Each client, contractor, or operator is issued a unique card that defines where they can enter, such as cages, suites, or shared technical areas. This ensures secure separation between tenants while still allowing efficient facility operations. The system is easy to manage, scalable for large user bases, and supports quick updates when access rights change or contracts are modified.

The mobile credential access control segment is expected to grow at a significant CAGR during the forecast period. Rising adoption of smartphone-based authentication is driven by the shift toward mobile-first security in data centers. Mobile credentials replace physical access cards by using smartphones as secure digital tokens. High smartphone penetration among employees, contractors, and vendors supports fast deployment. This approach improves convenience by eliminating badge management while reducing operational overhead. It also enhances security through encrypted credentials and device-based authentication, making access control more efficient, flexible, and scalable for modern data center environments.

Application Insights

The facility entry control segment dominated the market and accounted for the largest revenue share in 2025 due to increasing pressure for complying with security and audit regulations. Standards such as ISO 27001, SOC 2, and other industry-specific frameworks require strict monitoring of who enters and exits secure areas. Facility entry systems help organizations meet these requirements by maintaining detailed, time-stamped access logs and audit trails. These records support compliance reporting, internal audits, and external inspections. They also assist in incident investigations by providing traceability of physical access events. This ensures accountability, transparency, and adherence to global security governance standards.

The rack & cabinet level security segment is expected to grow at a significant CAGR over the forecast period, driven by the rising value density of IT equipment. Modern AI and GPU-intensive data centers pack extremely expensive hardware into each rack, significantly increasing the financial and operational risk of unauthorized access. Even a single rack may contain high-value compute, storage, and networking components. This makes granular protection essential to prevent theft, tampering, or sabotage. Rack-level security systems such as smart locks, access logs, and remote monitoring ensure only authorized personnel can access specific equipment, enhancing asset protection and operational integrity.

Data Center Insights

The hyperscale data centers segment dominated the market, accounting for the largest revenue share in 2025. These facilities span large campuses and employ thousands of staff, contractors, and vendors who require controlled and secure entry. Managing such high volumes of users necessitates automated, role-based access systems that can efficiently grant or restrict permissions across multiple zones. Advanced solutions streamline onboarding and offboarding while ensuring consistent security enforcement. They also reduce manual workload for security teams and improve operational efficiency, while maintaining strict control over sensitive infrastructure and critical data center areas.

The HPC & edge data centers segment is expected to grow at a significant CAGR over the forecast period. High-Performance Computing (HPC) environments process highly sensitive, mission-critical workloads across sectors such as defense, scientific research, and financial modeling. Because these systems manage valuable intellectual property and classified data, strict physical access control is essential. Unauthorized access could lead to data breaches, system disruption, or intellectual theft. As a result, HPC facilities adopt advanced security measures like biometrics, multi-factor authentication, and restricted zone-based access to ensure only authorized personnel can interact with critical computing infrastructure.

Regional Insights

The North America data center access control industry dominated the global market with the largest revenue share of 37.1% in 2025. The rapid expansion of hyperscale data centers in North America is significantly driving demand for advanced access control systems. These large facilities, operated by leading cloud providers, house thousands of employees, contractors, and vendors who require secure, efficient access management. To maintain strict security across vast campuses, operators deploy scalable systems with biometric authentication, role-based permissions, and real-time monitoring. This ensures controlled movement across multiple zones while maintaining operational efficiency and minimizing security risks.

U.S. Data Center Access Control Market Trends

The data center access control industry in the U.S. is expected to grow significantly at a CAGR of 9.1% from 2026 to 2033, due to the strong presence of cloud and technology giants in the U.S. These companies continuously invest in highly secure and scalable infrastructure to support global digital services. This increases demand for integrated access control systems that enable centralized management across multiple facilities. Automation and Zero Trust security frameworks further enhance adoption by ensuring continuous identity verification, least-privilege access, and seamless coordination between physical and digital security environments.

Europe Data Center Access Control Market Trends

The data center access control industry in Europe is anticipated to register considerable growth from 2026 to 2033. Europe’s strict regulatory environment, including GDPR and ISO 27001, drives strong demand for advanced data center access control systems. Organizations must ensure secure identity verification, continuous monitoring, and detailed audit trails of physical access. These capabilities support compliance, enhance accountability, and reduce the risk of unauthorized access to critical infrastructure.

The UK data center access control industry is expected to grow rapidly in the coming years. The UK enforces strong cybersecurity and data protection standards, including UK GDPR and industry-specific regulations. These require detailed access logging, identity verification, and continuous monitoring of physical access points.

The data center access control industry in Germany held a substantial market share in 2025. Germany’s leadership in Industry 4.0 and industrial digitalization drives strong demand for secure data center infrastructure. Manufacturing and enterprise organizations rely on data centers to store sensitive operational, engineering, and production data. This increases the need for robust access control systems that ensure only authorized personnel can access critical digital assets.

Asia Pacific Data Center Access Control Market Trends

The data center access control industry in the Asia Pacific held a significant share in the global market in 2025. Rapid cloud adoption and digital transformation across China, India, and Japan are accelerating demand for secure data centers. As enterprises migrate to cloud and hybrid environments, investments in modern infrastructure increase. This drives adoption of integrated, scalable access control solutions to ensure secure, centralized, and efficient physical access management.

The Japan data center access control industry is expected to grow rapidly in the coming years. Japan’s leadership in AI, robotics, and automation is transforming data center operations. Intelligent access control systems are increasingly used to enable real-time monitoring, automated identity verification, and predictive security analytics. These technologies reduce human intervention, improve accuracy, and enhance response speed. As a result, data centers are becoming more efficient and secure, with advanced systems ensuring seamless, automated, and highly reliable physical access management for critical infrastructure environments.

The data center access control industry in China held a substantial market share in 2025. China’s rapid expansion of hyperscale, colocation, and enterprise data centers is fueling strong demand for advanced access control systems. As facilities scale to support the digital economy, security requirements increase significantly. These systems help protect high-density infrastructure by ensuring controlled, authenticated, and monitored physical access across critical data center environments.

Key Data Center Access Control Company Insights

Key players operating in the data center access control industry are Johnson Controls International plc, Honeywell International Inc., Siemens AG, Schneider Electric SE, and Robert Bosch GmbH. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In March 2026, Johnson Controls showcased next-generation access control and video security solutions at ISC West 2026, emphasizing tighter integration between access control, video surveillance, and incident management platforms. The updates include enhancements to software platforms like C•CURE IQ, Kantech EntraPass, and exacqVision, alongside improved interoperability, AI-driven analytics, and cloud-ready architectures. The solutions aim to deliver faster deployment, improved real-time monitoring, and centralized security management for enterprise and mission-critical environments such as data centers.

-

In March 2026, Honeywell announced the launch of an AI-driven, cloud-based video and access control solution in collaboration with Rhombus that integrates physical security systems into a unified platform. The solution combines access control, video management, and AI analytics to deliver real-time monitoring, automated threat detection, and centralized security management across facilities. The partnership also strengthens interoperability and supports faster adoption of integrated security ecosystems in modern buildings and data center environments.

-

In July 2025, Allegion plc announced the acquisition of Gatewise Incorporated, a provider of smart access control solutions across the U.S. This reflects a broader industry shift toward software-driven, integrated security ecosystems in the physical access control market. The move strengthens its portfolio beyond hardware locks into cloud-based and mobile-enabled access platforms, aligning with demand from modern enterprises and data centers.

Key Data Center Access Control Companies

The following key companies have been profiled for this study on the data center access control market.

-

Allegion plc

-

Avigilon Corporation

-

Axis Communications AB

-

Brivo Systems LLC

-

Gallagher Group Limited

-

Genetec Inc.

-

HID Global Corporation

-

Honeywell International Inc.

-

Johnson Controls International plc

-

Nedap N.V.

-

Robert Bosch GmbH

-

Schneider Electric SE

-

Siemens AG

-

Suprema Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Johnson Controls; Honeywell; Schneider Electric; Bosch Security Systems; Allegion; Siemens

- Expanding from traditional physical security into integrated, software-driven access control platforms (cloud + on-prem hybrid models).

- Developing AI-enabled security ecosystems combining access control, video surveillance, identity management, and DCIM integration.

- Strengthening subscription-based and SaaS models for centralized multi-site access management across enterprise and hyperscale data centers.

- Strong global installed base in enterprise buildings and mission-critical infrastructure.

- Deep integration capabilities with HVAC, power, fire safety, and building management systems.

- Established compliance readiness (ISO 27001, SOC 2 alignment) and proven reliability in high-security environments.

- Legacy hardware-centric portfolios can slow transition to fully cloud-native architectures.

- High dependency on large enterprise contracts may limit flexibility in fast-growing edge and mid-market deployments.

- Integration complexity across legacy systems can increase deployment time and cost.

Emerging Players: Brivo; HID Global; Suprema

- Focus on cloud-native access control platforms with mobile credentials and remote management capabilities.

- Rapid innovation in AI-based access analytics, facial recognition, and touchless authentication systems.

- Targeting SMEs, colocation providers, and edge data centers with faster deployment and lower upfront costs.

- High agility and faster product innovation cycles compared to legacy providers.

- Strong user experience with mobile-first access control and easy scalability.

- Ability to integrate seamlessly with modern cloud ecosystems and identity platforms.

- Limited penetration in large hyperscale and government-grade critical infrastructure projects.

- Smaller global service networks compared to established multinational vendors.

- Dependence on third-party integrations for full-stack data center infrastructure solutions.

Data Center Access Control Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.59 billion

Market size in 2026

USD 1.73 billion

Revenue forecast in 2033

USD 3.44 billion

Growth rate

CAGR of 10.3% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, control, application, data center, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Allegion plc; Avigilon Corporation; Axis Communications AB; Brivo Systems LLC; Gallagher Group Limited; Genetec Inc.; HID Global Corporation; Honeywell International Inc.; Johnson Controls International plc; Nedap N.V.; Robert Bosch GmbH; Schneider Electric SE; Siemens AG; Suprema Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Data Center Access Control Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global data center access control market report based on component, control, application, data center and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Control Outlook (Revenue, USD Billion, 2021 - 2033)

-

Card-Based Access Control

-

Biometric Access Control

-

Mobile Credential Access Control

-

PIN/Keypad-Based Access Control

-

Others

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Perimeter Security

-

Facility Entry Control

-

Critical Room Security

-

Rack & Cabinet-Level Security

-

-

Data Center Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hyperscale Data Centers

-

Colocation Data Centers

-

Enterprise Data Centers

-

HPC & Edge Data Centers

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customization

This report has been delivered with the following in-depth customizations

Client Request

Customization Delivered

Value Adds

Hyperscale & AI-driven access control opportunity mapping

Evaluated demand for advanced access control systems across hyperscale, AI, and HPC data center environments

Assessed shift toward zero-trust physical security, biometric authentication, mobile credentials, and rack-level security systems

Analyzed security architecture evolution across perimeter, facility entry, and cabinet-level control layers

Identified high-growth access control deployment zones within AI and hyperscale campuses

Supported security technology investment prioritization

Highlighted emerging threats including insider risk, tailgating, and multi-tenant vulnerabilities

Regional and infrastructure maturity assessment for data center access security

Analyzed adoption maturity across Asia Pacific and emerging regions

Evaluated infrastructure readiness across hyperscale campuses, colocation hubs, edge facilities, and enterprise data centers

Assessed regulatory impact on access control adoption (GDPR, SOC 2, ISO 27001, and local cybersecurity laws)

Highlighted region-specific growth drivers and compliance pressures

Enabled strategic prioritization of expansion markets

Identified infrastructure segments with highest security upgrade demand

Vendor ecosystem and competitive positioning analysis

Benchmarking of leading access control providers across integrated security platforms, software innovators, and hardware specialists

Assessment of partnerships between security vendors, cloud providers, and data center operators

Evaluation of integration trends with DCIM, IAM, and cybersecurity ecosystems

Identified consolidation trends toward integrated security platforms

Supported go-to-market strategy and partnership development

Highlighted competitive gaps in cloud-native and AI-driven access control solutions

Frequently Asked Questions About This Report

The global data center access control market size was estimated at USD 1.59 billion in 2025 and is expected to reach USD 1.73 billion in 2026.

The global data center access control market is expected to grow at a compound annual growth rate of 10.3% from 2026 to 2033 to reach USD 3.44 billion by 2033.

The hardware segment dominated the market and accounted for the revenue share of 55.6% in 2025. The rapid growth of artificial intelligence workloads and high-performance GPU infrastructure is significantly increasing demand for advanced physical security hardware in data centers.

Some key players operating in the data center access control market include Allegion plc, Avigilon Corporation, Axis Communications AB, Brivo Systems LLC, Gallagher Group Limited, Genetec Inc., HID Global Corporation, Honeywell International Inc., Johnson Controls International plc, Nedap N.V., Robert Bosch GmbH, Schneider Electric SE, Siemens AG, Suprema Inc.

The rapid expansion of hyperscale and colocation data centers worldwide has significantly accelerated the demand for advanced access control solutions.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.