- Home

- »

- HVAC & Construction

- »

-

Digital Shipyard Market Size And Share Report, 2026-2033GVR Report cover

![Digital Shipyard Market (2026 - 2033)Report]()

Digital Shipyard Market (2026 - 2033)

Size, Share & Trends Analysis Report By Solution (Hardware, Software, Services), By Shipyard Type (Commercial, Military), By Capacity, By Technology (AR/VR, Digital Twin, AI & Big Data Analytics, HPC), By Region, And Segment Forecasts

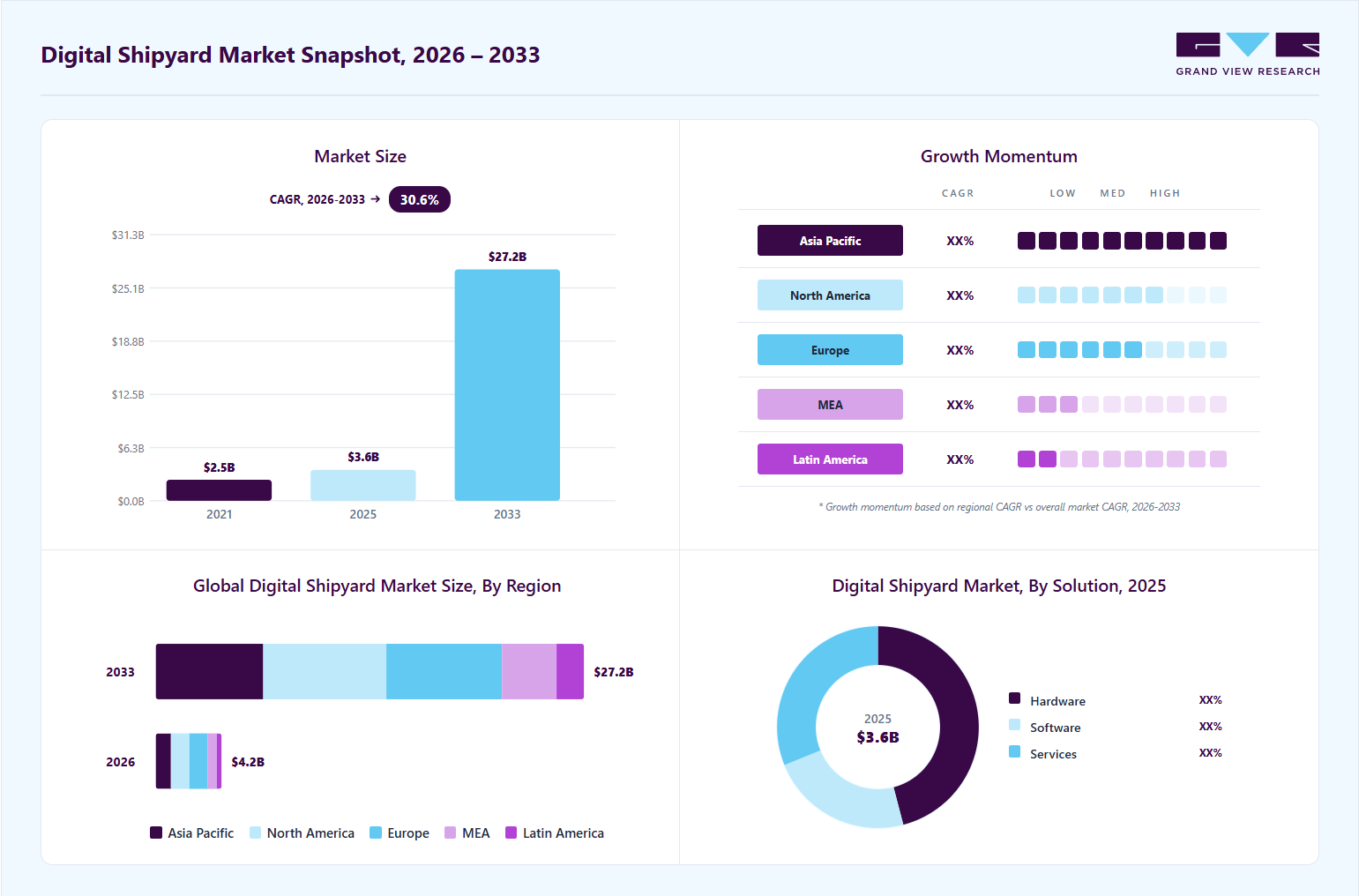

Market Size, 2025

$3.6BMarket Estimate, 2026

$4.2BMarket Forecast, 2033

$27.2BCAGR, 2026–2033

30.6%Digital Shipyard Market Summary

The global digital shipyard market size was valued at USD 3.6 billion in 2025 and is projected to grow from USD 4.2 billion in 2026 to USD 27.2 billion by 2033, at a CAGR of 30.6% from 2026 to 2033. North America accounted for a 28.2% share of the overall market in 2025. The rapid growth of the global digital shipyard market is primarily driven by increasing naval modernization programs, rising adoption of Industry 4.0 technologies across shipbuilding facilities, and growing investments in smart maritime infrastructure.

Key Market Trends & Insights

- By solution: Hardware segment held the largest market share of 45.9% in 2025.

- By shipyard Type: Commercial segment held the largest market share in 2025.

- By capacity: Medium segment held the largest market share in 2025.

- By technology: AI & big data analytics segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (28.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 3.6 Billion

- Estimated market size in 2026: USD 4.2 Billion

- Projected market size by 2033: USD 27.2 Billion

- CAGR (2026-2033): 30.6%

Shipbuilders and defense contractors are increasingly integrating advanced digital technologies such as artificial intelligence, digital twins, additive manufacturing, IoT-enabled monitoring systems, and high-performance computing to improve operational efficiency, reduce production timelines, and enhance lifecycle management of vessels. In addition, the increasing demand for autonomous vessels, predictive maintenance capabilities, and real-time shipyard analytics is further accelerating global market expansion.

The IIoT enables the integration of physical machinery and assets with digital systems, allowing shipyards to collect and analyze real-time data. This data-driven approach enhances operational efficiency, improves decision-making, and enables predictive maintenance, ultimately leading to cost savings and improved productivity.

Furthermore, factors such as the rising interest in connected and autonomous ships fuel the industry's demand for digital shipyard solutions. These solutions enable shipyards to integrate advanced technologies such as sensors, connectivity, automation, and artificial intelligence (AI) into vessels. Connected and autonomous ships offer improved safety, reduced fuel consumption, optimized navigation, and enhanced operational efficiency. Autonomous ships, also called crewless ships, are outfitted with software and hardware that allows them to operate without the intervention of humans. These ships use sensors, automated navigation systems, propulsion and auxiliary systems, GPS trackers, and other components. These components allow the ship to make decisions based on its surroundings.

")

Moreover, the significance of utilizing a digital twin in the shipyard industry is its potential to transform shipbuilding and maintenance procedures. A digital twin is a virtual replica of a ship or shipyard continuously updated with real-time data. Shipyards can develop advanced 3D models and simulations by employing digital twins, enabling more precise planning and design. This aids in identifying potential issues and streamlining ship construction processes, resulting in cost and time savings. In addition, digital twins comprehensively understand ship and equipment performance in real-time. This facilitates continuous monitoring and optimization of operations, ensuring optimal efficiency and performance throughout the ship's lifespan.

Software companies continuously enhance their products to fortify them against potential hacking attempts. Within the maritime sector, shipyards and ship operators store vast repositories of sensitive data on their IT platforms, including information about ships and components. Consequently, these entities face elevated vulnerability to cyberattacks, which could result in substantial financial losses. The growing adoption of digitalization also raises the specter of cyber threats and cybercrimes aimed at stealing critical operational data from ships, posing a threat to national security. Addressing these cyber risks necessitates deploying sophisticated cybersecurity solutions, which demands increased investments from software companies. As a result, the maritime industry has recognized the imperative of safeguarding against cyber threats and risks.

The focus on sustainable shipbuilding is a significant driver of growth in the digital shipyard market, primarily due to increasing regulatory pressures, rising costs of resources, and growing environmental concerns. Digital shipyards leverage advanced technologies such as digital twins, IoT, and AI-driven analytics to reduce emissions, conserve materials, and promote energy efficiency, which aligns with the sustainability goals of the modern maritime industry.

The need for efficiency and cost reduction is a critical factor driving the growth of the global digital shipyard market. Digital technologies enhance operational efficiency and reduce overall costs, making shipyards more competitive and adaptable in a challenging economic landscape. Automation technologies, such as robotic process automation (RPA) and AI, streamline shipyard processes by taking over repetitive tasks and improving workflow organization. This automation reduces labor costs and shortens production times, enhancing overall productivity. Digital shipyards can also allocate resources more effectively, ensuring that every phase of the shipbuilding process operates at peak efficiency, which in turn lowers operational costs.

Market Dynamics

Shipyards worldwide are increasingly adopting automation technologies and smart manufacturing systems to improve production efficiency and reduce vessel construction timelines. The integration of robotics, AI-driven production management, automated welding systems, and real-time operational monitoring is enabling shipbuilders to streamline complex manufacturing processes while improving precision and reducing human error. These technologies are becoming critical as commercial and defense shipbuilding projects grow larger and more technologically sophisticated.

In addition, digital production platforms are improving coordination between engineering, procurement, fabrication, and maintenance teams. Shipbuilders are leveraging integrated digital workflows to minimize operational bottlenecks, optimize workforce utilization, and enhance project visibility across vessel construction lifecycles. The growing pressure to improve delivery schedules and reduce operational costs is significantly accelerating adoption of advanced digital shipyard solutions globally.

The increasing digitalization of shipyard operations is exposing maritime infrastructure to growing cybersecurity risks, which remains a significant challenge for market growth. Shipyards and ship operators manage large volumes of sensitive operational, engineering, and defense-related data, making them attractive targets for cyberattacks. The integration of connected systems, IoT-enabled devices, and cloud-based operational platforms increases vulnerability to ransomware, data breaches, and operational disruptions. As a result, shipbuilders are required to invest heavily in cybersecurity infrastructure and continuous software protection measures.

Additionally, the high capital investment associated with upgrading legacy shipyard infrastructure continues to limit technology adoption among small and medium-sized shipyards. Implementing AI platforms, digital twins, industrial IoT systems, and advanced analytics environments requires significant financial and technical resources. Integration challenges with outdated operational systems and workforce retraining requirements further increase deployment complexity and implementation costs.

The rapid development of autonomous vessels and connected maritime ecosystems is creating substantial growth opportunities for the digital shipyard market. Autonomous ships require advanced simulation platforms, predictive maintenance systems, digital navigation technologies, and AI-enabled operational management solutions throughout the vessel development lifecycle. This is increasing demand for advanced digital shipyard technologies capable of supporting intelligent shipbuilding and lifecycle optimization.

Furthermore, the growing focus on sustainable shipbuilding and green maritime operations is generating new opportunities for digital transformation across global shipyards. Digital twin technology, AI-driven analytics, and IoT-enabled monitoring systems help shipbuilders optimize energy usage, reduce material waste, and improve emissions management during vessel construction and maintenance. Rising environmental regulations and investments in smart port infrastructure are expected to further accelerate demand for advanced digital shipyard solutions over the forecast period.

Market Concentration & Characteristics

The digital shipyard market is moderately fragmented, with the presence of global industrial technology providers, defense contractors, maritime software companies, and specialized shipyard automation vendors competing across commercial and military shipbuilding sectors. Major companies maintain strong market positions through integrated digital manufacturing platforms, strategic partnerships, and advanced engineering capabilities. The market is also witnessing growing participation from emerging technology firms specializing in AI-enabled analytics, digital twin solutions, and industrial automation technologies.

The market is characterized by rapid technological innovation, increasing integration of cloud-native shipyard management systems, and rising adoption of predictive analytics and automation platforms. Companies are focusing on enhancing real-time operational visibility, digital collaboration capabilities, and intelligent production management systems to improve shipbuilding efficiency and reduce project delivery timelines. Strategic investments in cybersecurity, smart manufacturing infrastructure, and connected maritime ecosystems are further shaping competitive dynamics across the industry.

Solution Insights

The hardware segment accounted for the largest market share of 45.9% in 2025. The ongoing advancements in hardware technologies, including sensors, the Industrial Internet of Things (IIoT), and edge computing devices, are driving the integration of hardware components in the digital shipyard sector. These progressions empower real-time data collection and enable seamless network connectivity and integration with digital twin systems. Notably, these hardware components are pivotal for establishing connections between digital twin models and the tangible assets in the digital shipyard industry.

The services segment is expected to emerge at the fastest CAGR from 2026 to 2033. As the global fleet of ships continues to grow, there is a constant need for ship maintenance and repair services. The services segment within the market caters to this demand by providing specialized services such as ship repair, retrofitting, and maintenance. The need to keep ships in optimal condition and comply with regulations drives the demand for these services. As shipyards increasingly adopt advanced technologies, they require specialized consulting services to tailor these solutions to their unique operational needs. Service providers offer expertise in assessing shipyard processes, integrating digital tools such as IoT, AI, and digital twin technologies, and ensuring that these solutions align with the client’s goals for efficiency and sustainability.

Shipyard Type Insights

The commercial segment held the largest market share in 2025. The growth influences the commercial shipyard segment in maritime trade. As global trade continues to expand, demand for new commercial ships and the maintenance and repair of existing ones is increasing. For instance, in April 2022, Wärtsilä introduced virtual and augmented reality simulation solutions that leverage the latest AR and VR technologies. These solutions create immersive environments that simulate real-life shipboard operations, improving learning retention, job performance, and team collaboration. Such innovation drives the need for such services that can optimize shipbuilding and maintenance processes.

The military segment is expected to grow at the fastest CAGR during the forecast period. The allocation of defense budgets plays a crucial role in driving the military shipyard segment. Governments invest in digital shipyard services to optimize defense spending, improve shipbuilding capabilities, and extend the lifespan of existing naval assets. The demand for digital shipyard services within the military segment is influenced by the availability of defense funding and the strategic priorities of nations. For instance, in December 2022, the government of India intends to provide cash subsidies, tax reductions, and other incentives to support its shipbuilding sector. This move aims to alleviate the impact of elevated freight rates on the country's manufacturers. The proposed measures include offering subsidies to facilitate the construction of at least 50 new vessels and granting the shipbuilding industry "infrastructure status," which would help secure financing from banks.

Capacity Insights

The large segment dominated the market in 2025 and is expected to grow at the fastest CAGR during the forecast period. Large-scale shipyards possess greater financial capabilities and operational requirements for advanced automation systems, AI-driven production management, and digital engineering platforms. These facilities are increasingly deploying integrated smart manufacturing ecosystems to manage highly complex vessel construction projects and improve operational scalability.

The medium segment also held a significant share of the market in 2025. Medium-sized shipyards are gradually adopting modular digital solutions and cloud-based operational systems to improve competitiveness and optimize production efficiency. Increasing availability of scalable digital platforms is encouraging broader adoption among medium-capacity shipbuilding facilities.

Technology Insights

AI & big data analytics dominated the market in 2025 and are projected to maintain strong growth throughout the forecast period. AI-driven analytics platforms enable shipyards to improve predictive maintenance capabilities, optimize production workflows, analyze operational data, and enhance decision-making efficiency. Growing adoption of intelligent automation and real-time operational analytics is significantly accelerating demand for AI-enabled shipyard technologies.

Digital Twin technology is expected to grow at the fastest CAGR during the forecast period. Digital twin platforms are increasingly being deployed to simulate vessel performance, monitor shipyard assets, optimize maintenance schedules, and improve engineering collaboration. Integration of digital twins with IoT sensors and AI analytics is further strengthening their adoption across commercial and military shipbuilding operations.

Regional Insights

North America digital shipyard market accounted for the largest revenue share of 28.2% in the global digital shipyard market in 2025. The region’s dominance is primarily attributed to rising defense modernization investments, increasing adoption of advanced manufacturing technologies, and the strong presence of major naval shipbuilding companies. Government support for smart manufacturing initiatives and the growing deployment of AI-driven shipyard automation systems are further driving regional market growth.

U.S. Digital Shipyard Market Trends

The U.S. market held a dominant position in North America in 2025. Increasing naval fleet modernization initiatives, rising adoption of digital engineering technologies, and growing investments in autonomous maritime systems are accelerating market demand. Major defense contractors and commercial shipbuilders are increasingly implementing digital twin systems, industrial IoT platforms, and AI-enabled predictive maintenance technologies to improve operational efficiency and reduce production risks.

Europe Digital Shipyard Market Trends

Europe is witnessing steady market growth driven by increasing investments in sustainable maritime technologies, smart port infrastructure, and naval modernization programs. European shipbuilders are focusing heavily on digital manufacturing systems that improve fuel efficiency, operational sustainability, and vessel lifecycle management capabilities. Strong regulatory focus on emissions reduction and green shipping initiatives is further supporting adoption of advanced digital shipyard technologies across the region.

Germany digital shipyard market remains a major hub for advanced shipbuilding engineering and maritime automation technologies. German shipyards are increasingly integrating robotics, AI-enabled analytics, and digital simulation platforms to improve vessel design accuracy and manufacturing efficiency. The country’s strong industrial automation ecosystem continues to support digital shipyard innovation.

The UK digital shipyard market is benefiting from growing naval defense investments and increasing adoption of digitally integrated maritime manufacturing systems. Expansion of offshore renewable energy infrastructure and smart maritime logistics projects is further contributing to demand for advanced digital shipyard technologies.

Asia Pacific Digital Shipyard Market Trends

Asia Pacific is expected to grow at the fastest CAGR of 32.4% during the forecast period. The region’s growth is primarily driven by expanding shipbuilding activities, rising maritime trade volumes, increasing defense modernization programs, and strong government support for industrial digitalization initiatives. Countries such as China, Japan, South Korea, and India are rapidly investing in smart manufacturing infrastructure and advanced shipyard automation systems.

The China digital shipyard market remains one of the largest shipbuilding hubs globally and is aggressively investing in intelligent manufacturing technologies across commercial and naval shipyards. Government-backed industrial modernization initiatives and increasing focus on autonomous shipping technologies are significantly accelerating adoption of digital shipyard platforms.

The Japan digital shipyard market growth is driven by advanced engineering capabilities, strong maritime technology expertise, and increasing adoption of AI-enabled manufacturing systems. Japanese shipbuilders are prioritizing digital automation and predictive maintenance technologies to maintain competitiveness in global shipbuilding markets.

The India digital shipyard market is emerging as a significant growth market due to rising investments in naval modernization, domestic shipbuilding expansion, and smart port development initiatives. Government programs promoting indigenous defense manufacturing and maritime infrastructure modernization are encouraging broader adoption of digital shipyard technologies across the country.

Key Digital Shipyard Company Insights

Some of the leading players in the digital shipyard industry include SAP, Wärtsilä, BAE Systems, Dassault Systèmes, and AVEVA Group Limited, among others. These companies provide advanced digital shipyard technologies and solutions spanning digital twin platforms, AI-enabled analytics, industrial IoT infrastructure, smart manufacturing systems, cloud-based engineering software, and connected maritime operations platforms. Their offerings support a broad range of applications across commercial shipbuilding, naval defense modernization, offshore engineering, autonomous vessel development, and smart port infrastructure. Market participants are increasingly focusing on automation, predictive maintenance, operational intelligence, and cybersecurity capabilities to improve shipyard productivity and vessel lifecycle management.

-

BAE Systems plays a significant role in naval digital shipbuilding and defense modernization programs. The company leverages advanced digital engineering, model-based systems engineering, and intelligent manufacturing technologies to support the design and production of complex naval vessels and submarines. BAE Systems focuses heavily on digital twin integration, cybersecurity protection, and AI-enabled operational systems to improve production efficiency, mission readiness, and lifecycle sustainment capabilities for defense fleets.

-

AVEVA Group Limited specializes in industrial software and engineering information management solutions for maritime and heavy industrial sectors. The company provides digital asset performance management systems, industrial IoT platforms, and operational intelligence software that enable shipyards to improve project execution, predictive maintenance, and process optimization. AVEVA’s cloud-enabled engineering and visualization solutions support real-time monitoring and data-driven decision-making across vessel construction and maintenance operations.

Key Digital Shipyard Companies

The following key companies have been profiled for this study on the digital shipyard market

-

SAP

-

Wärtsilä

-

BAE Systems

-

Dassault Systèmes

-

AVEVA Group Limited

-

Siemens

-

Accenture

-

Hexagon AB

-

Inmarsat Global Limited

-

DAMEN SHIPYARDS GROUP

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: SAP; Siemens; Dassault Systèmes; Accenture; Wärtsilä; BAE Systems

- Focus on expanding digital shipyard ecosystems through AI, IoT, cloud computing, and automation technologies.

- Invest in strategic partnerships, naval modernization programs, and smart manufacturing solutions.

- Strong global presence, advanced digital engineering capabilities, and extensive enterprise customer networks.

- Broad portfolios covering digital twins, analytics, automation, and connected maritime operations.

- High implementation and integration costs.

- Longer deployment timelines due to complex operational structures and legacy system integration challenges.

Emerging Players: AVEVA Group Limited; Hexagon AB; Inmarsat Global Limited; Damen Shipyards Group

- Focus on digital twins, smart asset management, connected vessel technologies, and maritime analytics platforms.

- Expand through cloud-based solutions, technology partnerships, and smart shipbuilding initiatives.

- Strong specialization in industrial software, operational intelligence, and maritime connectivity solutions.

- Flexible and scalable digital platforms supporting smart shipyard operations.

- Smaller global customer reach compared to established market leaders.

- Intense competition from large integrated technology and industrial solution providers.

Recent Developments

-

In May 2026, Wärtsilä joined the EU-funded H4PERION consortium, where data from real-world demonstrations will feed into a digital twin model to support long-term learning and future design work for zero-carbon shipping, reinforcing its relevance to digital shipyard innovation.

-

In October 2025, SAP unveiled SAP Supply Chain Orchestration, an AI-centric solution built to detect disruptions early, analyze risk in context, and trigger AI-driven actions across planning, logistics, procurement, and manufacturing.

Digital Shipyard Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 3.6 Billion

Estimated market size in 2026

USD 4.2 billion

Estimated market size in 2026

USD 27.2 billion

Growth rate

CAGR of 30.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Solution, shipyard type, capacity, technology, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

SAP; Wärtsilä; BAE Systems; Dassault Systèmes; AVEVA Group Limited; Siemens; Accenture; Hexagon AB; Inmarsat Global Limited; DAMEN SHIPYARDS GROUP

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Digital Shipyard Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global digital shipyard market report based on solution, shipyard type, capacity, technology, and region.

-

Solution Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hardware

-

Software

-

Services

-

-

Shipyard Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Commercial

-

Military

-

-

Capacity Outlook (Revenue, USD Billion, 2021 - 2033)

-

Small

-

Medium

-

Large

-

-

Technology Outlook (Revenue, USD Billion, 2021 - 2033)

-

AR/ VR

-

Digital Twin

-

Additive Manufacturing

-

AI & Big Data Analytics

-

High performance Computing (HPC)

-

Blockchain

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Naval Shipyard Digital Transformation Assessment

Evaluation of AI-enabled shipyard automation systems

Analysis of digital twin integration for vessel lifecycle management

Assessment of predictive maintenance and smart manufacturing capabilities

Identified operational efficiency improvement opportunities

Supported modernization strategy for naval shipbuilding facilities

Commercial Shipbuilding Market Analysis

Analysis of commercial vessel production trends and smart shipyard adoption

Benchmarking of connected manufacturing platforms and automation technologies

Evaluation of cloud-based shipyard management systems

Supported investment planning for digital infrastructure

Identified high-growth commercial shipbuilding opportunities

Digital Twin & Predictive Maintenance Strategy

Assessment of vessel simulation and real-time asset monitoring platforms

Analysis of predictive maintenance software capabilities

Benchmarking of lifecycle management technologies

Assessment of vessel simulation and real-time asset monitoring platforms

Analysis of predictive maintenance software capabilities

Benchmarking of lifecycle management technologies

Frequently Asked Questions About This Report

The global digital shipyard market size was estimated at USD 3.6 billion in 2025 and is expected to reach USD 4.2 billion in 2026.

The global digital shipyard market is expected to grow at a compound annual growth rate of 30.6% from 2026 to 2033 to reach USD 27.2 billion by 2033.

Some of the key player include SAP, Wartsila, BAE Systems, Dassault Systemes, AVEVA, Siemens Digital Industries Software, Accenture, Hexagon, Inmarsat Plc., and Damen Shipyards Group.

Digital twin adoption has been fueled by the industry's rapid growth and the demand for cutting-edge technology. Furthermore, factors such as the rising interest in connected and autonomous ships fuel the industry's demand for digital shipyard solutions. These solutions enable shipyards to integrate advanced technologies such as sensors, connectivity, automation, and artificial intelligence (AI) into vessels.

North America dominated with a 28.2% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The commercial segment held the largest revenue share in 2025, while the military segment is the fastest-growing.

The medium segment held the largest revenue share in 2025, while the large segment is the fastest-growing.

The hardware segment dominated the overall market, gaining a market share of over 45.9% in 2025. The ongoing advancements in hardware technologies, such as encompassing sensors, the Industrial Internet of Things (IIoT), and edge computing devices, propel the integration of hardware components in the digital shipyard sector. These progressions empower real-time data collection and enable seamless network connectivity and integration with digital twin systems.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.