- Home

- »

- Next Generation Technologies

- »

-

Distribution Automation Market Size, Industry Report, 2030GVR Report cover

![Distribution Automation Market Size, Share & Trends Report]()

Distribution Automation Market (2025 - 2030) Size, Share & Trends Analysis Report By Type (Wired, Wireless), By Application (Private Utility, Public Utility), By Component (Software, Hardware, Services), By End-use (Industrial), By Region, And Segment Forecasts

Market Size, 2024

$18,833.4MMarket Estimate, 2026

$21,316.3MMarket Forecast, 2030

$41,721.3MCAGR, 2025–2030

14.4%Distribution Automation Market Summary

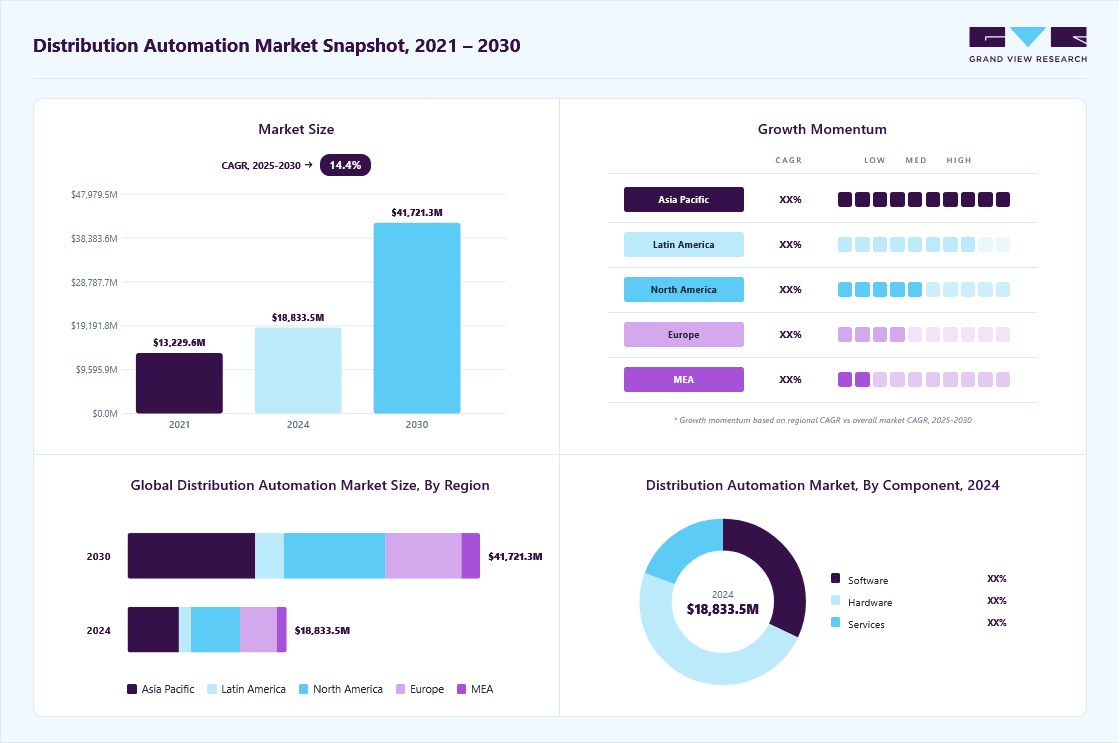

The global distribution automation market size was estimated at USD 18,833.4 million in 2024 and is projected to reach USD 41,721.3 million by 2030, growing at a CAGR of 14.4% from 2025 to 2030. The market growth is primarily driven by the increasing demand for reliable and uninterrupted power supply, coupled with the modernization of aging grid infrastructure.

Key Market Trends & Insights

- North America accounted for a significant market share of over 30% in 2024.

- The U.S. distribution automation market is expected to grow at a CAGR of over 12% from 2025 to 2030.

- Based on type, the wired segment dominated the market with a market share of over 58% in 2024.

- Based on application, the public utility segment accounted for the largest market share in 2024.

- Based on component, the hardware segment accounted for the largest market share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 18,833.4 Million

- 2030 Projected Market Size: USD 41,721.3 Million

- CAGR (2025-2030): 14.4%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Advancements in smart grid technologies and the integration of IoT, artificial intelligence, and cloud-based solutions are enabling utilities to enhance operational efficiency and reduce outage durations. Government mandates focused on energy efficiency, grid reliability, and carbon emission reductions are also accelerating the adoption of automation systems in power distribution. The growing penetration of distributed energy resources (DERs) such as solar and wind is reshaping the landscape of utility operations. These factors contribute to the robust growth of the distribution automation industry.

The availability of advanced communication technologies and smart grid infrastructure is significantly influencing the growth of the distribution automation industry. Utilities now have access to a wide range of automation solutions such as feeder automation, voltage regulation, automated switching, and real-time fault detection, allowing them to enhance the reliability and efficiency of power distribution networks. This flexibility enables energy providers to reduce downtime, improve load management, and respond quickly to outages, thereby strengthening the overall distribution automation industry.

In addition, the growing emphasis on energy efficiency and grid modernization is propelling the distribution automation market forward. Governments and regulatory bodies are introducing supportive policies and funding initiatives aimed at upgrading aging grid infrastructure and improving power quality. These mandates are pushing utilities to adopt automation systems that can monitor, control, and optimize energy flow in real time, contributing to significant operational cost savings and improved sustainability.

Furthermore, the rapid adoption of IoT, artificial intelligence (AI), and advanced metering infrastructure (AMI) is reshaping the distribution automation landscape. Utilities investing in connected devices and cloud-based platforms, operators can now gather granular insights into energy consumption and network performance. This integration of digital technologies enables predictive maintenance, enhanced fault diagnosis, and improved decision-making capabilities.

Moreover, the rise in renewable energy integration, such as solar and wind, into distribution networks presents valuable opportunities for automated control systems. Distributed energy resources (DERs) become more prevalent as distribution automation systems play a critical role in managing load fluctuations and ensuring grid stability. This increasing need for responsive, flexible grid solutions is expected to remain a key driver of the distribution automation market expansion.

Type Insights

The wired segment dominated the market with a market share of over 58% in 2024, primarily due to its proven reliability, stability, and security in grid automation applications. The use of wired systems, such as fiber optics and copper cables, ensures high-speed data transmission with minimal signal interference, making them the preferred choice for critical, large-scale infrastructure. These attributes are essential for utility providers aiming to maintain consistent and secure communication networks, thereby reinforcing the segment's dominance in the distribution automation market.

The wireless segment is expected to witness a significant CAGR of over 16% from 2025 to 2030. This growth is attributed to the increasing demand for flexible, scalable, and easily deployable communication solutions in the energy sector. The adoption of advanced wireless technologies such as 5G is enabling seamless real-time data transmission across geographically dispersed infrastructure without the constraints of traditional wiring. Utilities and industries prioritize smart grid development and remote monitoring, and the shift toward agile and cost-efficient wireless communication systems is accelerating. This trend is further fueled by the need for enhanced operational efficiency, reduced installation complexity, and greater adaptability in dynamic environments, positioning wireless connectivity as a key segment of the distribution automation industry.

Application Insights

The public utility segment accounted for the largest market share in 2024. This growth is primarily driven by the increasing demand for reliable, resilient, and intelligent power distribution systems. Public utilities are rapidly modernizing outdated grid infrastructure by adopting advanced automation technologies, such as smart meters, sensors, and automated switches, to enhance grid visibility and responsiveness. Government mandates, regulatory support, and funding for grid modernization initiatives are further accelerating adoption across the public utility sector, making it a significant contributor to market growth.

The private utility segment is expected to witness the highest CAGR from 2025 to 2030, owing to substantial investments in advanced grid modernization technologies and intelligent distribution automation systems. There is a need to enhance operational efficiency, reduce outage durations, and meet sustainability goals. These organizations often operate across vast networks and require robust automation solutions to manage peak loads, integrate renewable energy sources, and optimize energy distribution. The increased reliance on distribution automation to improve service reliability, reduce operational costs, and enhance customer satisfaction drives the dominance of the private utility segment in the market.

Component Insights

The hardware segment accounted for the largest market share in 2024. The rising deployment of intelligent electronic devices, remote terminal units, smart sensors, and advanced switchgear drives demand for robust hardware infrastructure that supports real-time monitoring and control. The rapid integration of renewable energy sources into the grid is necessitating hardware upgrades to manage bidirectional power flow and improve system resilience. The shift toward smart substations and the increasing need for grid modernization across developing and developed regions are expected to contribute significantly to the growth of hardware in this segment.

The software segment is expected to witness the highest CAGR from 2025 to 2030, owing to the rising need for real-time monitoring and intelligent decision-making in power distribution networks. Distribution grids become increasingly complex with the integration of renewable energy sources, electric vehicles, and decentralized generation, and the demand for smart grid management software has surged. Utilities are adopting advanced software platforms to enhance grid reliability, optimize load balancing, and ensure efficient fault detection and response. The platforms enable predictive maintenance, remote operations, and data-driven insights, thereby critical in modernizing distribution systems and driving segmental growth.

End-use Insights

The industrial segment accounted for the largest market share in 2024, driven by the increasing demand for automation, energy efficiency, and real-time monitoring. The integration of Industry 4.0 technologies, including IoT, AI, and machine learning, is further accelerating the deployment of smart grids and automated substations within industrial facilities. The rising emphasis on sustainability, carbon footprint reduction, and compliance with environmental regulations is pushing industries to adopt intelligent energy management systems, thereby driving segmental growth.

The commercial segment is expected to witness the highest CAGR from 2025 to 2030, as organizations across retail, logistics, and facility management increasingly adopt advanced distribution automation technologies. The surge in e-commerce, omnichannel retailing, and smart infrastructure drives demand for intelligent grid solutions that ensure uninterrupted power supply, real-time monitoring, and efficient load management. Commercial operations grow more energy-intensive, the need for automated, scalable, and cost-effective energy distribution becomes critical. These solutions are pivotal in achieving sustainability goals and ensuring resilience in dynamic commercial environments.

Regional Insights

North America accounted for the significant market share of over 30% in 2024, primarily driven by the region’s advanced grid infrastructure and widespread deployment of smart grid technologies. The increasing need to reduce transmission and distribution losses, combined with rising investments in grid modernization programs such as the U.S. Department of Energy’s Grid Modernization Initiative, is significantly boosting market growth. The presence of leading technology providers and utilities actively embracing digital transformation is fostering innovation and accelerating the deployment of distribution automation solutions across the region.

U.S. Distribution Automation Market Trends

The U.S. distribution automation market is expected to grow at a CAGR of over 12% from 2025 to 2030, driven by the country’s accelerated grid modernization initiatives and focus on enhancing energy efficiency across utility networks. Federal and state-level investments in smart grid infrastructure, along with favorable regulatory frameworks such as the Infrastructure Investment and Jobs Act, are playing a critical role in driving automation across distribution systems. The U.S. is also witnessing a surge in renewable energy integration, which necessitates distribution networks to maintain grid stability. These factors collectively position the U.S. as a leading market for adopting distribution automation solutions.

Europe Distribution Automation Market Trends

The Europe distribution automation is expected to grow at a CAGR of over 12% from 2025 to 2030. In Europe, the distribution automation market is propelled by the growing integration of electric vehicles (EVs) and the expansion of EV charging infrastructure. The rising adoption of distributed energy resources, such as rooftop solar and community wind projects, is increasing the need for dynamic grid balancing and localized automation technologies. Public-private partnerships and cross-border energy cooperation under EU frameworks are enhancing investment flows into smart grid technologies, thereby supporting the continued growth of the distribution automation industry.

The UK distribution automation market is expected to grow significantly in the coming years. The country’s ambitious climate targets and commitment to achieving net-zero emissions by 2050 are accelerating investments in smart grid technologies and automation systems. Government-led initiatives such as the Smart Systems and Flexibility Plan promote the deployment of intelligent infrastructure to modernize the electricity network. The UK's strong regulatory framework and focus on energy resilience further support the growth of the distribution automation market.

Distribution automation market in Germany is fueled by the country’s commitment to grid modernization and energy transition. Germany advances toward its Energiewende goals, there is a strong push to adopt intelligent grid technologies that can efficiently manage decentralized energy generation and storage. The rising demand for smart substations, real-time monitoring systems, and predictive maintenance tools is further boosting automation adoption in the power distribution sector.

Asia Pacific Distribution Automation Market Trends

Asia Pacific distribution automation is expected to grow at a CAGR of over 16% from 2025 to 2030, driven by increasing investments in urban expansion and rising energy consumption. The growing penetration of renewable energy sources such as solar and wind requires advanced automation systems to manage grid stability and intermittent power generation. Funding for digital infrastructure is accelerating the adoption of intelligent substations and advanced metering systems, making APAC a key growth hub for distribution automation technologies.

The Japan distribution automation market is gaining traction, fueled by the nation’s advanced infrastructure and strong industrial base. The push toward decarbonization and the integration of renewable energy sources such as solar and wind is further encouraging investment in intelligent distribution networks. Japan’s leadership in IoT and sensor technologies also enables the implementation of real-time monitoring and automated control systems, fostering continued growth in the distribution automation market.

Distribution automation market in China is rapidly expanding. China’s accelerated urbanization and government initiatives to modernize the power grid are significant drivers of the distribution automation market. The country’s strong emphasis on smart grid deployment is accelerating the adoption of advanced automation technologies across utilities. China’s commitment to reducing carbon emissions and integrating renewable energy sources fosters demand for intelligent distribution automation solutions that enhance grid reliability and flexibility, driving market growth.

Key Distribution Automation Company Insights

Some of the key players operating in the market include Schneider Electric SE and Siemens AG among others

-

Schneider Electric SE is a global leader in energy management and automation, offering a wide array of solutions that contribute significantly to the distribution automation market. The company provides advanced smart grid technologies, real-time monitoring systems, and grid optimization tools. Its flagship EcoStruxure™ Grid platform leverages IoT, AI, and analytics to enhance the reliability, safety, and efficiency of power distribution networks across various industries. Schneider Electric's commitment to innovation, digital transformation, and sustainability makes it a key player in the distribution automation market.

-

Siemens AG is a global technology powerhouse specializing in smart infrastructure and energy automation solutions. In the distribution automation market, Siemens plays a crucial role through its comprehensive offerings, including grid automation systems, SCADA, remote terminal units (RTUs), and digital substations. The company’s solutions enable utility providers to modernize distribution networks, minimize outages, and improve operational control. Siemens AG’s emphasis on innovation, sustainability, and scalable grid solutions solidifies its position as a key player in the distribution automation market.

Trilliant Holdings Inc. and NARI Technology Co., Ltd. are some of the emerging market participants in the distribution automation market.

-

Trilliant Holdings Inc. is an emerging provider of smart communication platforms and solutions tailored for the distribution automation market. The company specializes in scalable, secure, and interoperable technologies that enable utility companies to modernize their grid infrastructure and enhance operational efficiency. Integrating advanced metering infrastructure (AMI), IoT, and data analytics, Trilliant supports seamless energy distribution and network reliability. Its expanding presence across North America, Europe, and Asia makes it a promising player in the evolving distribution automation landscape.

-

NARI Technology Co., Ltd., is rapidly gaining recognition in the distribution automation market. The company focuses on delivering intelligent solutions for grid automation, energy management, and protection systems. Leveraging advanced technologies such as AI, big data, and digital control, NARI helps optimize power distribution and improve grid stability. Backed by China’s national grid modernization initiatives, the company is expanding its domestic leadership to international markets, making it a strong emerging player in this sector.

Key Distribution Automation Companies:

The following are the leading companies in the distribution automation market. These companies collectively hold the largest market share and dictate industry trends.

- Schneider Electric SE

- Toshiba Corporation.

- Mitsubishi Electric Corporation

- Schweitzer Engineering Laboratories, Inc.

- Eaton.

- ABB

- Itron Inc.

- S&C Electric Company

- Siemens

- Xylem.

- Trilliant Holdings Inc.

- NARI Technology Co., Ltd

Recent Developments

-

In May 2025, Toshiba International Corporation announced the launch of its new Toshiba 3000 SP Series Uninterruptible Power System (UPS), designed specifically for the U.S. and global edge data centers, IT, and commercial markets. The new single-phase modular and scalable UPS offers unmatched reliability and efficiency for mission-critical applications. This innovation supports the growing demand for stable power distribution in highly automated environments, aligning with the expanding needs of distribution automation systems in data-intensive and real-time operational settings.

-

In March 2025, Eaton announced a breakthrough AI-powered innovation aimed at strengthening wildfire prevention efforts within utility distribution systems. The new Eaton HiZ Protect™ solution addresses the long-standing challenge of accurately detecting and mitigating high-impedance (HiZ) faults on distribution lines. By enabling faster, more accurate fault detection and automatic de-energization, the technology significantly enhances grid reliability and safety. This advancement reinforces Eaton’s leadership in the distribution automation market and its commitment to building intelligent, resilient, and fire-safe grid infrastructure.

-

In February 2025, Schneider Electric announced a major expansion of its manufacturing footprint in India. The expansion supports Schneider Electric’s commitment to accelerating India’s digitalization and sustainability efforts through advanced energy management and industrial automation technologies The company showcased cutting-edge solutions tailored to enable digital grids, IoT-enabled distributed energy resources, and smart buildings, aligning with the growing demand for distribution automation in India’s rapidly evolving power sector.

Distribution Automation Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 21,316.3 million

Revenue forecast in 2030

USD 41,721.3 million

Growth rate

CAGR of 14.4% from 2025 to 2030

Base year for estimation

2024

Historical data

2018 - 2023

Forecast period

2025 - 2030

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2030

Report product

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, application, components, end-use, region

Region scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Schneider Electric SE; Toshiba Corporation.; Mitsubishi Electric Corporation; Schweitzer Engineering Laboratories, Inc.; Eaton.; ABB; Itron Inc.; S&C Electric Company; Siemens; Xylem.; Trilliant Holdings Inc.; NARI Technology Co., Ltd

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Distribution Automation Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the distribution automation market report based on type, application, components, end use, and region:

-

Type Outlook (Revenue, USD Million, 2018 - 2030)

-

Wired

-

Wireless

-

-

Application Outlook (Revenue, USD Million, 2018 - 2030)

-

Private Utility

-

Public Utility

-

-

Component Outlook (Revenue, USD Million, 2018 - 2030)

-

Software

-

Hardware

-

Services

-

-

End-use Outlook (Revenue, USD Million, 2018 - 2030)

-

Industrial

-

Commercial

-

Residential

-

-

Regional Outlook (Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global distribution automation market was estimated at USD 18.83 billion in 2024 and is expected to reach USD 21.32 billion in 2025.

The global distribution automation market is expected to grow at a compound annual growth rate of 14.4% from 2025 to 2030 to reach USD 41.72 billion by 2030.

The Asia Pacific distribution automation market accounts for the largest market share. The market growth is driven by urban expansion, rising energy consumption, and the integration of renewable energy sources. Investments in digital infrastructure are accelerating the adoption of intelligent substations and advanced metering systems to enhance grid stability and efficiency.

The key players in the distribution automation market are Schneider Electric SE, Toshiba Corporation., Mitsubishi Electric Corporation, Schweitzer Engineering Laboratories, Inc., Eaton., ABB, Itron Inc., S&C Electric Company, Siemens, Xylem., Trilliant Holdings Inc., and NARI Technology Co., Ltd

The key players in the distribution automation market are Schneider Electric SE, Toshiba Corporation., Mitsubishi Electric Corporation, Schweitzer Engineering Laboratories, Inc., Eaton., ABB, Itron Inc., S&C Electric Company, Siemens, Xylem., Trilliant Holdings Inc., and NARI Technology Co., Ltd

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.