- Home

- »

- Plastics, Polymers & Resins

- »

-

Flexible Foam Market Size And Share Report, 2026-2033GVR Report cover

![Flexible Foam Market (2026 - 2033)Report]()

Flexible Foam Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type, By Application (Furniture & Bedding, Transportation, Packaging, Building & Construction), By Region (North America, Europe, Asia Pacific, Central & South America, MEA), Segment Forecasts

Market Size, 2025

$41.7BMarket Estimate, 2026

$44.1BMarket Forecast, 2033

$66.4BCAGR, 2026–2033

6.0%Flexible Foam Market Summary

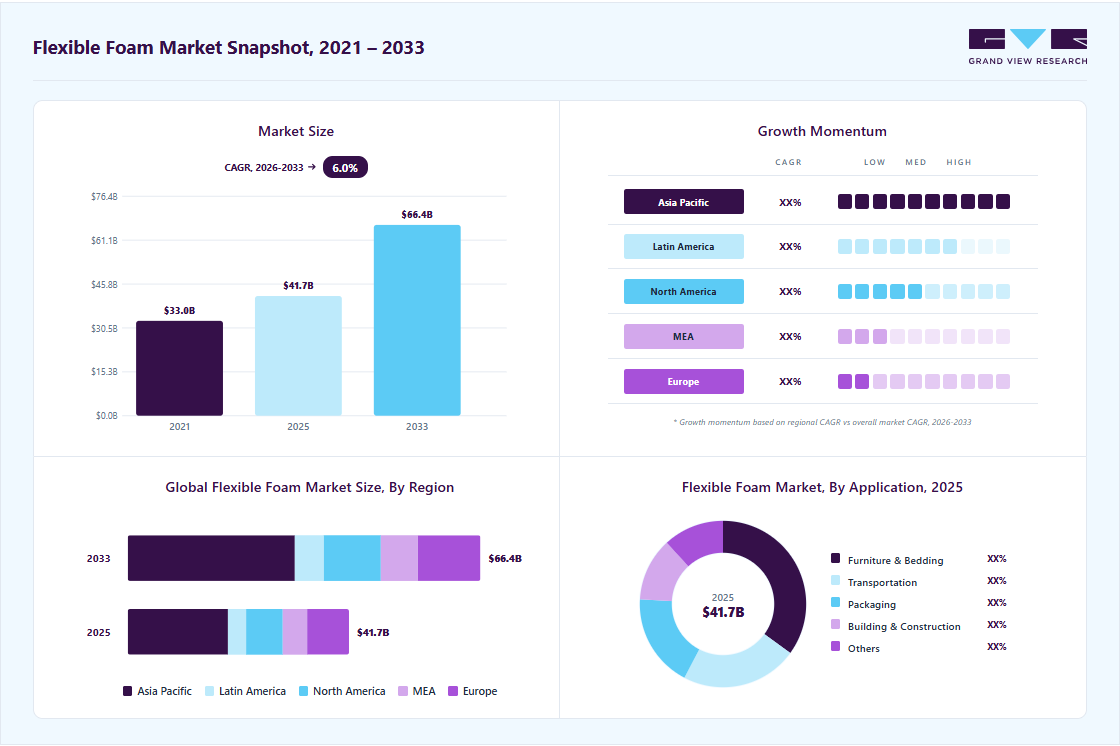

The global flexible foam market size was valued at USD 41.7 billion in 2025 and is projected to grow from USD 44.1 billion in 2026 to USD 66.4 billion by 2033, at a CAGR of 6.0% from 2026 to 2033. Asia Pacific held the largest revenue share of 45.3% of the global market in 2025. Rising urbanization and residential construction are driving demand for affordable comfort materials in mattresses, sofas, and home furnishings.

Key Market Trends & Insights

- By type: Polyurethane (PU) segment held the largest market share of 57.9% in 2025.

- By application: Furniture & bedding segment held the largest market share of 35.1% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (45.3% market share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR of 6.6% from 2026-2033)

- By country: China held held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 41.7 Billion

- Estimated market size in 2026: USD 44.1 Billion

- Projected market size by 2033: USD 66.4 Billion

- CAGR (2026-2033): 6.0%

Flexible foams offer a cost-effective balance of durability, comfort, and design flexibility, making them a preferred choice for mass-market housing and lifestyle products. The market is shifting from volume-driven growth to a more differentiated expansion led by premium comfort applications and sustainability-aware product lines. New uses in protective packaging and thermal insulation are complementing mature demand in furniture and automotive.

")

Consolidation among mid-sized converters and strategic vertical integration by polyol producers are increasing. Overall growth remains positive but uneven across regions, with Asia Pacific leading expansion while developed markets focus on higher-value formulations.

Market Dynamics

The flexible foam market is being driven by increasing consumption of lightweight, cushioning, and energy-absorbing materials across furniture, bedding, automotive, packaging, construction, and consumer goods applications. Flexible foams are widely preferred because they provide comfort, durability, thermal insulation, vibration control, and design flexibility while maintaining relatively low weight and cost efficiency. Growth in residential construction, automotive production, and consumer lifestyle spending continues to support broad-based market expansion.

Furniture and bedding applications remain among the largest contributors to market demand. Flexible polyurethane foams are extensively used in mattresses, sofas, seating systems, and cushions due to their resilience, softness, and long-term performance. Rising consumer preference for premium comfort products, ergonomic furniture, and advanced sleep solutions is increasing demand for high-performance foam formulations with enhanced support, breathability, and durability characteristics. This trend is particularly strong in urbanizing and middle-income economies.

One of the key restraints affecting the flexible foam market is volatility in petrochemical-based raw materials such as polyols and isocyanates. Production economics are highly dependent on crude oil and energy market conditions, making foam pricing sensitive to feedstock cost fluctuations. Variability in raw material availability and transportation costs can create margin pressure for manufacturers and complicate procurement planning for downstream converters and end users.

Market Concentration & Characteristics

The market growth stage is moderate, and growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as BASF SE, Dow Inc., Covestro AG, Huntsman Corporation, Armacell International S.A., Recticel N.V., Rogers Corporation, Zotefoams plc, FXI Holdings, Inc., Future Foam, Inc., and others play a significant role in shaping the market dynamics. These leading players often drive innovation within the market, introducing new products, technologies, and types to meet the evolving demands of the industry.

Innovation in foam dressings is focused on multifunctional performance improvements that meet clinical and logistical needs. New formulations combine higher absorption capacity, controlled moisture vapor transmission, and integrated antimicrobial chemistries to reduce infection risk while supporting faster wound healing. Manufacturers are also prioritizing thinner profiles and improved conformability to broaden use across body sites and outpatient care. Advances in bio-based polyols and production controls are enabling these gains while addressing regulatory and sustainability requirements.

Substitutes to flexible polyurethane foam range from natural latex and viscoelastic memory foams to engineered polyolefin foams such as EPP and EPE, depending on application requirements. In seating and bedding, latex offers durability and natural credentials, though at a higher cost. For industrial cushioning and packaging, molded polyolefins provide superior recyclability and lighter weight. These alternatives pressure pricing and innovation in the recticel market, forcing suppliers to differentiate on performance, certification, and circularity.

Type Insights

Polyurethane (PU) dominated the market across all type segments in terms of revenue, accounting for a 57.85% market share in 2025, and is forecasted to grow at a 5.9% CAGR from 2026 to 2033. The polyurethane value chain is benefitting from demand for high-performance thermal and acoustic insulation, particularly in HVAC, refrigeration, and specialised industrial sealing. Manufacturers of flexible PU are improving formulation stability and fire performance to meet tighter building codes while controlling density and resilience for comfort applications. These technical advances increase PU uptake where rigid foams underperform. This dynamic is reinforcing investment in downstream converting capacity and supporting growth in the flexible elastomeric foam market.

The polypropylene (PP) segment is anticipated to grow at a substantial CAGR of 7.1% through the forecast period. Automotive lightweighting and packaging requirements are driving the adoption of expanded polypropylene, as PP foams combine low density with excellent impact resistance and recyclability. OEMs and tier suppliers increasingly specify EPP for energy-absorbing components, interior structural parts, and reusable packaging inserts to cut vehicle mass and simplify end-of-life sorting. Process improvements that lower cycle times and expand part sizes are widening PP foam's use and nudging procurement away from heavier, harder-to-recycle polymers, despite price competition from commodity resins. This trend closely aligns with demand tracked in the flexible polyurethane foam market.

Application Insights

Furniture & bedding dominated the market across the application segmentation in terms of revenue, accounting for a 35.02% market share in 2025, and is forecast to grow at a 6.1% CAGR from 2026 to 2033. Rising consumer expenditure on sleep quality and the shift to online mattress retail are accelerating demand for engineered polyurethane cushioning with controlled support profiles. Compressed-pack supply chains favour flexible PU because it ships efficiently and recovers resilience after unpacking. Mattress brands are investing in grade differentiation and eco-certifications to capture premium segments, thereby increasing demand for technical foam. Replacement cycles and hospitality refurbishment projects add reliable volume, sustaining market growth in polyurethane through both value and volume channels.

The packaging segment is expected to expand at a robust 7.2% CAGR over the forecast period. E-commerce expansion and higher shipments of electronics and fragile goods are boosting demand for tailored foam cushioning that reduces transit damage and returns. Flexible foam inserts offer predictable shock mitigation, light weight, and reusable life-cycles that improve logistics economics for retailers and shippers. At the same time, regulatory and retailer sustainability targets are forcing formulators to improve recyclability and reduce film use around foam inserts. These commercial and regulatory pressures are underpinning measurable growth in the flexible foam packaging market.

Regional Insights

The Asia Pacific flexible foam industry held the largest share, accounting for 45.25% of the revenue in 2025, and is expected to grow at the fastest CAGR of 6.6% over the forecast period. Urbanization and industrial expansion are underpinning robust demand for flexible foam across the Asia Pacific. Rapid housing development and rising consumer spending on furniture and mattresses are expanding volume consumption. The automotive sector’s recovery is driving increased demand for seat and interior foam. Local converters are investing in capacity to serve growth and reduce import dependency. Competitive raw material supply in the region supports cost-effective production and attracts global manufacturers seeking scale and proximity to key end-use markets.

China Flexible Foam Market Trends

The flexible foam market in China is expanding due to robust infrastructure and consumer market growth. The nation’s sizable furniture and bedding industry is upgrading products with higher-performance foams. Automotive foam consumption is increasing in tandem with vehicle production and electrification. Domestic polyurethane producers are scaling up capacity and shifting toward higher-value grades to reduce reliance on imports. The government's emphasis on manufacturing modernization and sustainability is encouraging the adoption of efficient production technologies and localized innovation, strengthening China’s competitive position in the global flexible foam supply chain.

North America Flexible Foam Market Trends

The flexible foam market in North America is growing due to the growth in furniture, bedding, and automotive seating. Premiumization in home comfort products is elevating the usage of advanced memory and high-resilience foams. Investments in energy-efficient building retrofits support insulation-related flexible foam applications. Supply chain nearshoring is strengthening domestic converting capacity and reducing lead times. Regulatory emphasis on safety standards and material traceability is also prompting formulators to innovate, adding value in the market.

The U.S. flexible foam market is supported by rising renovation activity and healthy new housing starts. Mattress and upholstered furniture upgrades are fueling technical foam uptake with enhanced comfort profiles. Automotive production growth is prompting tier suppliers to expand their domestic foam cutting and molding operations. E-commerce-driven packaging applications add incremental demand for protective cushioning. Stringent fire safety and indoor air quality norms are encouraging higher-specification formulations to satisfy building and consumer product standards.

Europe Flexible Foam Market Trends

The flexible foam market in Europe is shaped by stringent environmental and fire-safety regulations, which are boosting interest in melamine-based foams for insulation and acoustic control. Renovation cycles in commercial and residential buildings emphasise energy efficiency, expanding market share for low-emission products. Growth in electric vehicle production increases demand for lightweight, thermally stable interior components. Circular economy policies are accelerating investments in recycling and bio-based feedstocks, creating a competitive advantage for compliant manufacturers in the flexible melamine foam market.

Key Flexible Foam Company Insights

The flexible foam industry is highly competitive, with several key players dominating the landscape. Major companies include BASF SE, Dow Inc., Covestro AG, Huntsman Corporation, Armacell International S.A., Recticel N.V., Rogers Corporation, Zotefoams plc, FXI Holdings, Inc., and Future Foam, Inc. The flexible foam industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Flexible Foam Companies:

The following key companies have been profiled for this study on the flexible foam market.

- BASF SE

- Dow Inc.

- Covestro AG

- Huntsman Corporation

- Armacell International S.A.

- Recticel N.V.

- Rogers Corporation

- Zotefoams plc

- FXI Holdings, Inc.

- Future Foam, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: BASF SE, Dow Inc., Covestro AG

- Broad flexible foam portfolios across bedding, furniture, automotive, insulation, packaging, and industrial applications.

- Strong integration across polyurethane chemistry, specialty materials, and downstream foam processing technologies.

- Continuous investment in low-emission, bio-based, and recyclable foam solutions.

- Large-scale manufacturing and global supply capabilities improve operational reliability.

- Advanced R&D infrastructure supports the development of high-performance and sustainable foam technologies.

- Strong technical expertise across multiple end-use industries.

- High exposure to petrochemical feedstock and energy price volatility.

- Significant compliance and sustainability-related investment requirements.

- Dependence on cyclical industries such as automotive and furniture affects revenue stability.

Emerging Players: Zotefoams plc, FXI Holdings, Inc., Future Foam, Inc.

- Focus on specialized foam applications, including comfort solutions, protective packaging, acoustic insulation, and engineered foam products.

- Flexible manufacturing operations supporting customized formulations and mid-scale production requirements.

- Regional market expansion and customer-focused product development strategies.

- Faster responsiveness to customer-specific requirements and application customization.

- Greater operational flexibility compared with large multinational competitors.

- Strong specialization in selected foam technologies and niche applications.

- Smaller global manufacturing and distribution footprint.

- Limited economies of scale compared with diversified multinational producers.

- Higher dependence on selected regional markets and end-use sectors.

Recent Developments

-

In June 2025, Armacell inaugurated a new ArmaGel XG aerogel insulation manufacturing facility in Pune, India, adding roughly 1 million square metres per year of capacity to serve equipment insulation and engineered-foam demand across South Asia.

-

In April 2024, Huntsman launched its SHOKLESS polyurethane systems for EV battery potting and fixation, introducing a family of low-to-high density foams designed to improve mechanical protection, thermal insulation, and vibration damping at module and pack level.

Flexible Foam Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 41.7 billion

Estimated Market size in 2026

USD 44.1 billion

Projected Market size by 2033

USD 66.4 billion

Growth rate

CAGR of 6.0% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Report Segmentation

Type, application, region

Regional scope

North America; Europe; Asia Pacific; CSA; MEA

Country Scope

U.S.; Canada; Mexico; Germany; UK; Italy; France; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

BASF SE; Dow Inc.; Covestro AG; Huntsman Corporation; Armacell International S.A.; Recticel N.V.; Rogers Corporation; Zotefoams plc; FXI Holdings, Inc.; Future Foam, Inc.

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Flexible Foam Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global flexible foam market report based on type, application, and region:

-

Type Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Polyurethane (PU)

-

Polyethylene (PE)

-

Polypropylene (PP)

-

Ethylene-Vinyl Acetate (EVA)

-

Latex

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Furniture & Bedding

-

Transportation

-

Packaging

-

Building & Construction

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

France

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Benchmarking

Conducted detailed benchmarking analysis of key flexible foam manufacturers based on product portfolio strength, production capacity, regional presence, technology capabilities, sustainability initiatives, end-use penetration, and strategic developments. The assessment compared company positioning across bedding, furniture, automotive, packaging, insulation, and industrial foam applications.

Supported competitive intelligence and strategic positioning analysis. Identified technology differentiation, capability gaps, and regional competitive strengths among market participants. Improved understanding of product specialization and customer alignment across end-use industries. Enabled informed sourcing, partnership, and expansion planning decisions.

Opportunity Assessment

Assessed growth opportunities across premium bedding products, automotive lightweighting, acoustic insulation systems, sustainable packaging, furniture applications, and recyclable foam technologies. The study evaluated emerging consumer trends, regional demand shifts, sustainability-driven material adoption, and innovation activity across high-value foam applications.

Supported long-term growth strategy and product portfolio prioritization. Identified high-potential application segments and emerging revenue opportunities. Improved visibility into sustainability-focused demand trends and premium comfort product adoption. Enabled targeted investment and commercialization planning.

Pricing Analysis

Delivered pricing analysis for flexible polyurethane foams, specialty foam materials, and engineered foam products across major regions. The analysis examined polyol and isocyanate cost trends, production economics, energy price impacts, regional pricing variations, import-export pricing structures, and logistics-related cost influences affecting market pricing dynamics.

Supported procurement optimization and pricing strategy development. Improved understanding of raw material cost exposure and regional pricing behavior. Assisted in supplier comparison, margin management, and feedstock risk assessment. Enabled better response to petrochemical price volatility and changing production economics.

Frequently Asked Questions About This Report

The global flexible foam market size was estimated at USD 41.7 billion in 2025 and is expected to reach USD 44.1 billion in 2026.

Asia Pacific dominated with a 45.3% market share in 2025.

Asia Pacific is the fastest-growing region over the forecast period, expanding at a CAGR of 6.6%.

The polyurethane (PU) segment led the market with a 57.9% share in 2025, while the polypropylene (PP) segment is expected to grow at a CAGR of 7.1% over the forecast period.

The global flexible foam market is expected to grow at a compound annual growth rate of 6.0% from 2026 to 2033 to reach USD 66.4 billion by 2033.

Furniture & bedding dominated the market across the application segmentation in terms of revenue, accounting for a 35.0% market share in 2025, and is forecast to grow at a 6.1% CAGR from 2026 to 2033.

Some key players operating in the flexible foam market include BASF SE, Dow Inc., Covestro AG, Huntsman Corporation, Armacell International S.A., Recticel N.V., Rogers Corporation, Zotefoams plc, FXI Holdings, Inc., and Future Foam, Inc.

Rising urbanization and residential construction are driving demand for affordable comfort materials in mattresses, sofas, and home furnishings. Flexible foams offer a cost-effective balance of durability, comfort, and design flexibility, making them a preferred choice for mass-market housing and lifestyle products.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.