- Home

- »

- Network Security

- »

-

Hardware Security Modules Market, Industry Report, 2033GVR Report cover

![Hardware Security Modules Market Size, Share & Trends Report]()

Hardware Security Modules Market (2026 - 2033) Size, Share & Trends Analysis Report By Type (LAN-based, PCIE-based, USB-based, Cloud-based), By Deployment, By Application (Payment Processing, Authentication, PKI Management, Database Encryption), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$1.8BMarket Estimate, 2026

$2.3BMarket Forecast, 2033

$4.0BCAGR, 2026–2033

14.0%Hardware Security Modules Market Summary

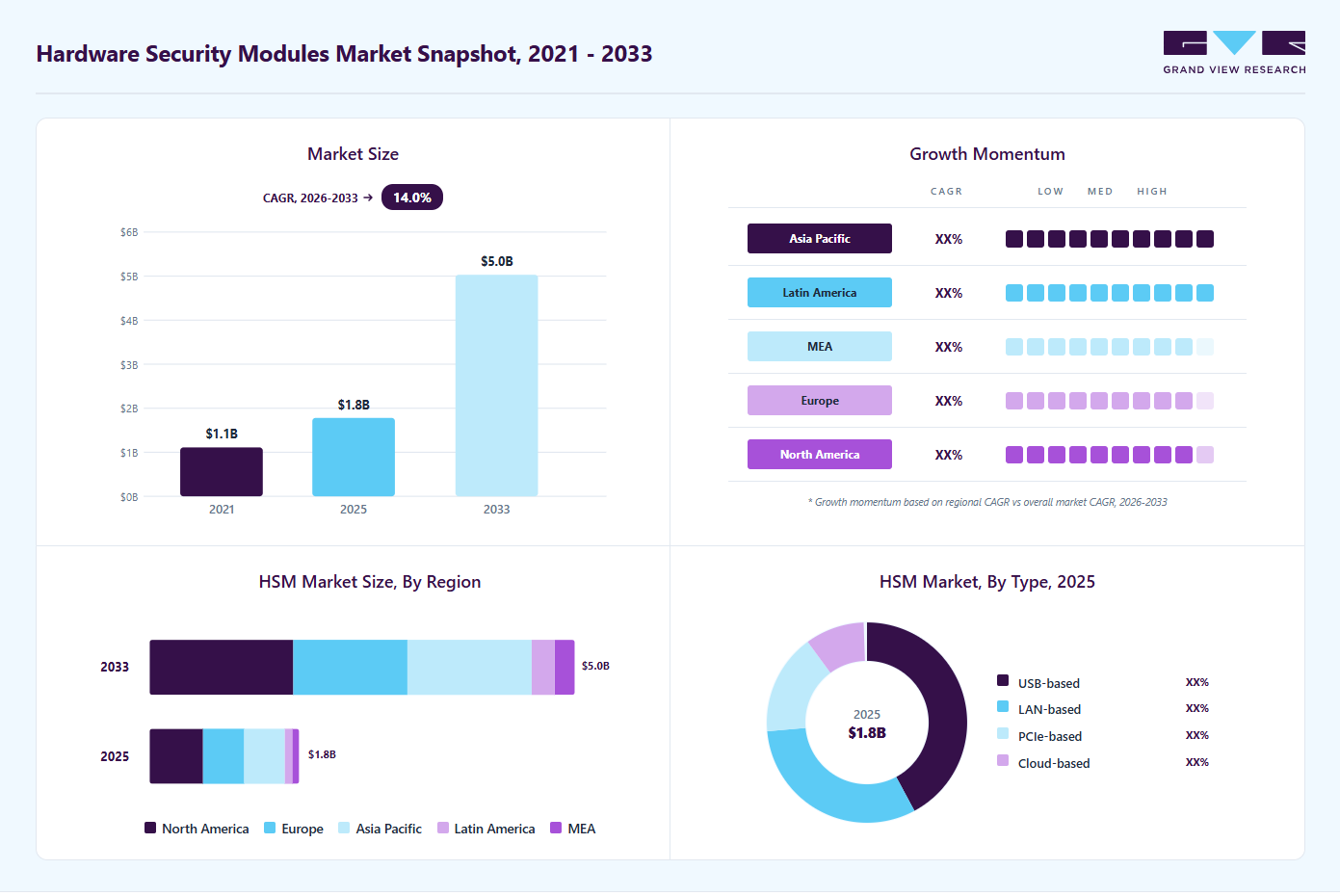

The global hardware security modules market size was valued at USD 1.8 billion in 2025 and is projected to grow from USD 2.3 billion in 2026 to USD 5.0 billion by 2033, at a CAGR of 14.0% from 2026 to 2033. The market in North America dominated with a revenue share of 56.4% in 2025. The market is a critical segment of the cybersecurity and data protection industry, focused on providing highly secure, tamper-resistant hardware devices that manage and safeguard cryptographic keys.

Key Market Trends & Insights

- By type: The USB-based segment accounted for the largest revenue share of 42.4% in 2025.

- By end use: The BFSI segment accounted for the largest share in 2025.

- By deployment: The on-premise segment accounted for the largest share in 2025.

Regional Highlights

- Largest regional market: North America (56.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The hardware security modules industry in the U.S. held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.8 Billion

- Estimated market size in 2026: USD 2.3 Billion

- Projected market size by 2033: USD 5.0 Billion

- CAGR (2026-2033): 14.0%

These modules are widely used to perform encryption, decryption, digital signing, and authentication in a secure environment, helping protect against unauthorized access and cyber threats. As organizations increasingly adopt digital transformation, cloud computing, and online financial transactions, the demand for robust cryptographic security solutions such as HSMs continues to grow significantly across industries, including banking, government, healthcare, and IT & telecommunications.The market is witnessing strong growth driven by rising concerns over data breaches, stringent regulatory compliance requirements, and the rapid expansion of digital payment ecosystems. Within emerging economies, the Brazil hardware security modules (HSM) market is gaining traction, supported by the country’s expanding fintech sector, increasing digital banking penetration, and growing adoption of secure payment infrastructures such as PIX, which is driving demand for advanced cryptographic security solutions. Regulations such as GDPR, PCI DSS, and other data protection frameworks are compelling enterprises to adopt advanced key management solutions, thereby boosting HSM adoption.

")

Additionally, the growing adoption of cloud-based services and hybrid IT infrastructures has increased the need for cloud-compatible, scalable HSM solutions, enabling organizations to secure sensitive workloads both on-premises and in virtual environments. Further, North America dominates the HSM market due to the early adoption of advanced cybersecurity technologies, the strong presence of key vendors, and strict regulatory enforcement. Europe follows closely, supported by stringent data privacy laws and increasing investments in digital identity protection. Meanwhile, the Asia-Pacific is emerging as the fastest-growing region, fueled by rapid digitalization, expansion of fintech services, and increasing cybersecurity investments in countries such as China and India. Latin America and the Middle East & Africa are also experiencing steady growth as organizations in these regions enhance their security infrastructure.

Consequently, the hardware security modules market is expected to expand steadily as enterprises prioritize zero-trust security architectures and secure key management becomes central to enterprise cybersecurity strategies. The integration of HSMs with cloud services, blockchain applications, and IoT ecosystems is further expected to create new growth opportunities. Key players are also focusing on developing flexible deployment models, including as-a-service offerings, to cater to evolving enterprise needs, making HSMs an essential component of modern digital security frameworks.

Market Dynamics

The rapid growth of digital payments and fintech ecosystems is significantly driving demand for Hardware Security Modules (HSMs) across the BFSI sector. Increasing adoption of online banking, mobile wallets, contactless payments, UPI transactions, real-time payment systems, and digital currencies has created a strong need for secure cryptographic infrastructure to protect sensitive financial data and authenticate transactions. HSMs play a critical role in securely generating, storing, and managing encryption keys used in payment processing, PIN authentication, tokenization, and digital signatures. Financial institutions and payment processors rely on HSMs to comply with stringent regulatory standards such as PCI DSS while ensuring secure and uninterrupted transaction processing. Additionally, the emergence of Central Bank Digital Currencies (CBDCs), open banking frameworks, and blockchain-based financial services is further accelerating HSM adoption. As cyberattacks targeting financial networks continue to rise, organizations are increasingly investing in advanced HSM solutions to strengthen fraud prevention, data integrity, and customer trust in digital financial ecosystems.

The hardware security modules (HSM) market faces challenges due to the high costs associated with deployment, maintenance, and integration of advanced cryptographic infrastructure. Implementing HSM solutions often requires significant investment in specialized hardware, secure facilities, compliance certifications, and skilled cybersecurity professionals capable of managing encryption keys and cryptographic operations. Additionally, integrating HSMs with existing legacy IT systems, cloud platforms, payment networks, and enterprise security architectures can be technically complex and time-consuming. Small and medium-sized enterprises (SMEs) often struggle with budget constraints and limited in-house expertise, slowing adoption rates. Operational complexities related to scalability, performance optimization, and regulatory compliance further add to deployment challenges. Moreover, organizations must continuously update cryptographic systems to address evolving cybersecurity threats and changing compliance standards, increasing long-term operational burdens. These factors collectively restrain broader market penetration, particularly among cost-sensitive organizations and businesses with limited cybersecurity infrastructure maturity.

Market Concentration & Characteristics

The hardware security modules (HSM) market is moderately concentrated, with a combination of established cybersecurity vendors, encryption technology providers, and specialized cryptographic hardware companies leading the competitive landscape. Major players such as Thales Group, IBM Corporation, Entrust Corporation, Utimaco, and Futurex hold significant market share due to their strong cryptographic expertise, extensive compliance certifications, global enterprise customer base, and integrated security portfolios. These vendors offer a broad range of HSM solutions including payment HSMs, general-purpose HSMs, cloud HSMs, and key management platforms, creating substantial entry barriers for new participants due to stringent regulatory standards, certification requirements such as FIPS 140-2/3 and Common Criteria, and the highly sensitive nature of cryptographic infrastructure.

In terms of market characteristics, the industry is highly security-centric, compliance-driven, and innovation-intensive, with strong focus on cloud security, post-quantum cryptography readiness, secure digital payments, and hybrid cloud key management. Demand is primarily driven by rising cyber threats, increasing adoption of digital banking and e-commerce, expansion of cloud computing environments, and growing regulatory requirements for data protection and encryption. The market is also characterized by long enterprise procurement cycles, high integration complexity, and strong customer retention due to deep integration with critical IT infrastructure, payment systems, and identity management frameworks. Additionally, the growing adoption of HSM-as-a-Service (HSMaaS), confidential computing, blockchain security, and zero-trust cybersecurity architectures is accelerating innovation and intensifying competition among vendors globally.Type Insights

The USB-based segment accounted for the largest share of 42.4% in the hardware security modules market in 2025 due to its strong alignment with modern enterprise requirements for portability, cost efficiency, and hardware-level encryption security. Organizations are adopting flexible IT environments that demand secure data handling across endpoints, remote operations, and hybrid cloud infrastructures, where traditional rack-mounted or network-attached HSMs are often less practical. Also, the growing emphasis on plug-and-play security solutions and software-independent encryption devices is further accelerating adoption by reducing system complexity, minimizing dependency on host software, and mitigating risks such as malware and keylogging attacks. Recent trends also indicate rising demand for compact, high-performance encrypted USB devices that support secure authentication and FIPS-grade protection. These solutions are gaining traction across industries such as banking, healthcare, defense, and digital forensics, where secure mobility of sensitive data is critical. For instance, in May 2023, Apricorn launched the Aegis NVX, a hardware-encrypted USB storage device offering read/write speeds up to 1,000 MB/s with onboard authentication and AES-XTS encryption, designed to enable secure data protection without requiring host-installed software. This development reflects the broader market shift toward fast, portable, and highly secure USB-based encryption solutions. Consequently, the dominance of this segment is expected to continue as enterprises increasingly prioritize scalable, user-friendly, and robust cryptographic solutions that support distributed IT architectures and real-time data protection needs.

The cloud-based segment is expected to grow at the fastest CAGR from 2026 to 2033 due to the rapid shift of enterprises toward cloud-native architectures, increasing adoption of hybrid and multi-cloud environments, and the rising need for on-demand cryptographic key management without heavy hardware dependency. Organizations are facing challenges related to “secret sprawl,” API security, and distributed workloads across containers, Kubernetes, and serverless platforms, which is driving demand for cloud-delivered HSMs that offer centralized control, automation, and elastic scalability while maintaining high levels of compliance and security. In addition, the growing focus on zero-trust security models and regulatory requirements for data protection is pushing enterprises to integrate HSM functionality directly into cloud security stacks to ensure secure key generation, storage, and rotation across dynamic digital environments. For instance, in November 2025, Crypto4A introduced QxVault, a next-generation secrets management platform that integrates a FIPS 140-3 Level 3 hardware security module directly into a cloud-ready vault, enabling organizations to manage cryptographic keys, credentials, and API secrets with built-in hardware-backed security while supporting both on-premises and private cloud deployments. This development reflects vendors' efforts to embed hardware-grade security into cloud platforms to eliminate complexity and improve agility in managing sensitive cryptographic operations across distributed infrastructures. Consequently, the cloud-based segment is projected to witness the fastest growth as enterprises increasingly prioritize flexible, software-defined security models that combine the strength of hardware encryption with the scalability and accessibility of cloud environments.

Deployment Insights

The on-premise segment dominated the hardware security modules industry in 2025 due to the strong requirement for full control over cryptographic keys, strict regulatory compliance, and data sovereignty needs across highly sensitive industries. Organizations in these sectors prefer on-premise HSMs because they ensure that encryption keys never leave internal data centers, significantly reducing exposure to external threats, third-party risks, and jurisdictional uncertainties. This deployment model also aligns with stringent compliance frameworks that mandate physical and logical control over cryptographic assets, making it the most trusted option for mission-critical workloads. In addition, enterprises continue to maintain legacy security architectures and hybrid transition strategies, where on-premise HSMs act as the root-of-trust for identity, authentication, and key management while cloud adoption gradually scales. For instance, in December 2025, Crypto4A’s sovereign and post-quantum-ready solutions highlight the growing emphasis on maintaining cryptographic sovereignty, with its QxVault platform and related deployments designed to support both cloud and on-premise environments while ensuring full control over secrets, credentials, and cryptographic keys within organizational boundaries. Consequently, the on-premise segment remained dominant in 2025 as organizations balanced growing digital transformation with uncompromising security, compliance, and sovereignty requirements, ensuring that sensitive cryptographic operations remain securely managed within internal infrastructure.

The cloud segment is expected to grow at a significant CAGR from 2026 to 2033 due to the rapid acceleration of cloud-first digital transformation strategies, where enterprises are migrating critical workloads, applications, and data infrastructures to public, private, and hybrid cloud environments, creating strong demand for cloud-native cryptographic key management and scalable hardware-backed security services. Organizations are prioritizing flexible, on-demand security models such as HSM-as-a-Service and cloud-integrated HSMs because they eliminate the need for heavy upfront infrastructure investment, reduce operational complexity, and enable seamless integration with DevOps pipelines, containerized applications, and multi-cloud ecosystems. Additionally, the rise of zero-trust architectures, API-driven ecosystems, and distributed computing environments is further driving the need for centralized, automated, and highly scalable key management solutions that cloud-based HSM platforms are uniquely positioned to deliver. For instance, in January 2025, Fortanix highlighted in its research that modern enterprises are adopting software-defined, cloud-integrated HSM solutions that combine traditional hardware-grade security with cloud-scale agility, enabling organizations to secure sensitive data, cryptographic keys, and workloads across hybrid and multi-cloud environments. This trend demonstrates that cloud-based HSMs are evolving beyond standalone hardware appliances into fully integrated security services embedded within cloud infrastructures, supporting real-time encryption, key lifecycle automation, and secure application development at scale. Subsequently, the cloud segment is expected to witness strong growth as enterprises increasingly demand scalable, flexible, and future-ready security architectures that align with modern cloud-native operating models.

Application Insights

The payment processing segment accounted for the largest revenue share in 2025 in the hardware security modules market, driven by its critical role in securing highly sensitive financial transactions, including card authentication, PIN verification, encryption, tokenization, and cryptographic key management, which are essential to ensuring secure and compliant digital payment ecosystems. The rapid expansion of digital banking, contactless payments, real-time settlement systems, and cross-border e-commerce has increased transaction volumes, thereby driving strong demand for HSMs that comply with stringent standards such as PCI DSS, EMV, and PCI PIN, as financial institutions and payment service providers prioritize robust infrastructure to prevent fraud and data breaches. Additionally, the increasing migration of payment workloads to cloud environments is further strengthening the need for scalable, hardware-backed cryptographic services that can support high-throughput transaction processing. For instance, in June 2023, AWS introduced Payment Cryptography, a fully managed service that enables organizations to move payment processing operations to the cloud while leveraging HSM-backed cryptographic operations for secure key management, encryption, and transaction processing through scalable APIs. This development highlights the industry shift toward cloud-enabled, HSM-backed payment security solutions that combine scalability with strong cryptographic protection. In conclusion, the payment processing segment continues to dominate the market as it remains fundamental to global financial operations, driven by rising digital payment adoption, evolving regulatory requirements, and the increasing need for secure, high-volume transaction processing across modern financial ecosystems.

The IoT security segment is expected to grow at a significant CAGR from 2026 to 2033 due to the rapid expansion of connected devices across industries such as smart manufacturing, healthcare, automotive, energy, and smart cities, which has increased the attack surface and created strong demand for hardware-backed cryptographic protection to secure device identity, authentication, firmware updates, and data communication across highly distributed environments. The rising frequency of IoT-targeted cyberattacks, combined with the fact that many IoT endpoints have limited built-in security capabilities, is further pushing enterprises to adopt HSM-enabled solutions for secure key management, encryption, and device trust establishment. In addition, increasing regulatory focus on IoT security standards and the adoption of zero-trust architectures are accelerating investments in scalable, hardware-rooted security frameworks that can support massive device fleets while ensuring compliance and operational resilience. For instance, in July 2025, Asimily enhanced its IoT security platform by introducing advanced password management and automated device patching capabilities, enabling organizations to more effectively secure and update large-scale IoT deployments and reduce vulnerabilities arising from unmanaged or outdated devices, reflecting the growing industry emphasis on continuous protection and lifecycle security for IoT ecosystems, where weak credentials and unpatched firmware remain major attack vectors. This development highlights that vendors are expanding IoT security solutions to address operational complexity and security gaps across heterogeneous device environments, reinforcing the need for integrated, scalable security frameworks supported by hardware-level cryptographic controls. Consequently, the IoT security segment is projected to grow rapidly over the forecast period as organizations increasingly prioritize securing billions of connected endpoints, ensuring device authenticity, and protecting real-time data flows in highly dynamic, decentralized digital infrastructures.

End-use Insights

The BFSI segment accounted for the largest revenue share in 2025, due to its heavy reliance on high-assurance cryptographic protection, strict regulatory compliance requirements, and large-scale digital transaction processing needs, as financial institutions continuously handle sensitive customer data, payment credentials, and interbank transactions that must be secured against fraud, breaches, and cyberattacks. The sector’s rapid digital transformation, including the expansion of online banking, mobile payments, fintech platforms, and real-time settlement systems, has significantly increased the demand for robust HSM solutions that ensure secure key management, encryption, authentication, and digital signing across financial ecosystems. In addition, stringent global regulations such as PCI DSS, GDPR, and other financial data protection frameworks compel BFSI organizations to adopt certified and tamper-resistant hardware security infrastructure to maintain trust, ensure compliance, and safeguard critical financial operations. For instance, in February 2026, Fireblocks partnered with Thales to improve security for digital assets. This shows that banks and financial institutions are adopting advanced HSM-based solutions to better protect digital asset storage, manage transactions, and secure cryptographic keys. It also reflects the growing need in the BFSI sector for strong, reliable systems that can support both traditional banking services and newer digital asset technologies.. Consequently, BFSI continues to dominate the HSM market as it remains the most security-sensitive vertical, driven by continuous innovation in digital payments, rising cyber threats targeting financial systems, and the sector’s non-negotiable requirement for trusted cryptographic infrastructure to protect global financial transactions.

The retail and consumer products segment is expected to grow at the fastest CAGR in the hardware security modules (HSM) market due to the rapid expansion of digital commerce, omnichannel retailing, and data-driven customer engagement models, which are generating massive volumes of sensitive consumer and transaction data that require strong cryptographic protection. Retailers are adopting e-commerce platforms, mobile shopping applications, and digital payment systems, which depend on secure key management, encryption, and authentication to protect payment information, customer identities, and loyalty program data from rising cyber threats. In addition, the growing adoption of cloud-based retail infrastructure, APIs, and third-party integrations is increasing exposure to data breaches, prompting organizations to invest in HSM-enabled security solutions that ensure secure transactions, tokenize payment data, and comply with regulations such as PCI DSS and global data protection laws. The rise of personalized retail experiences powered by AI and analytics is further amplifying the need for secure data handling across distributed systems, driving demand for scalable and automated cryptographic security frameworks. Consequently, the retail and consumer products segment is expected to register the fastest growth as organizations prioritize secure digital payment processing, enhanced customer data protection, and scalable security architectures that can support rapidly expanding e-commerce ecosystems and evolving consumer expectations.

Regional Insights

The North America hardware security modules market held the largest share of the global industry due to strong adoption of advanced cryptographic security infrastructure across BFSI, government, and technology sectors, where enterprises are rapidly deploying HSMs to support secure digital payment processing, cloud migration, and identity management systems. The region is witnessing high demand for FIPS-certified HSMs driven by stringent regulatory frameworks such as PCI DSS, HIPAA, and federal cybersecurity mandates that require secure key generation, encryption, and tamper-resistant hardware to protect sensitive data. Additionally, the widespread integration of cloud-based HSM services across hyperscale cloud providers and fintech ecosystems is accelerating deployment, as organizations shift toward hybrid and multi-cloud environments while maintaining strict security and compliance standards. Another key trend is the increasing use of HSMs in digital identity, authentication, and zero-trust architectures, particularly in financial services and government digital transformation initiatives, where secure cryptographic key management is essential for large-scale secure transactions and data protection.

U.S. Hardware Security Modules Market Trends

The hardware security modules industry in the U.S. is expected to grow significantly from 2026 to 2033, driven by the rapid expansion of cloud computing, the increasing adoption of zero-trust security architectures, and the rising demand for advanced cryptographic key management across the BFSI, government, and technology sectors. Organizations in the U.S. are increasingly deploying HSMs to secure digital payment systems, protect sensitive enterprise data, and enable secure authentication in highly distributed hybrid and multi-cloud environments, where cybersecurity threats are becoming more sophisticated and frequent. In addition, stringent regulatory requirements such as PCI DSS, HIPAA, and federal cybersecurity standards are driving enterprises to invest in FIPS-certified HSM solutions to ensure compliance, data integrity, and secure encryption of critical workloads. The growing focus on digital identity protection, API security, and secure software development practices is further accelerating HSM adoption across enterprises undergoing large-scale digital transformation.

Asia Pacific Hardware Security Modules Market Trends

The hardware security modules industry in the Asia Pacific region is expected to grow at the fastest CAGR during the forecast period, due to rapid digital transformation across emerging economies, strong expansion of cloud computing, and fintech ecosystems. The growth is also attributed to the increasing adoption of digital payment platforms across countries such as China, India, and Japan, including the growing South Korean market, which is being driven by advanced digital banking infrastructure and strong national cybersecurity initiatives. The region is witnessing a surge in cybersecurity investments as enterprises modernize IT infrastructure and shift toward hybrid and multi-cloud environments, creating strong demand for hardware-backed cryptographic security to protect sensitive data, digital identities, and financial transactions. In addition, rising government initiatives focused on data protection regulations, digital economy development, and secure digital identity frameworks are further accelerating the deployment of HSM solutions across the BFSI, telecom, and public sectors. The rapid growth of e-commerce, IoT deployments, and mobile-first business models is also increasing the need for scalable key management and encryption solutions, making the Asia Pacific the most dynamic and fastest-growing regional market for HSM adoption.

The China hardware security modules industry held a significant share in 2025 due to the rapid expansion of its digital economy, strong adoption of cloud computing, and large-scale deployment of secure payment and identity infrastructure across banking, government, and enterprise sectors. The country’s increasing focus on cybersecurity regulations, data localization requirements, and digital sovereignty has significantly driven demand for hardware-based cryptographic solutions to secure sensitive financial data, critical infrastructure, and cross-border digital transactions. In addition, the rapid growth of e-commerce platforms, fintech innovation, and mobile payment ecosystems, such as digital wallets, has further accelerated the need for secure key management and encryption technologies. The rising adoption of cloud-native architectures and enterprise digital transformation initiatives across industries has also supported sustained demand for HSM solutions, making China one of the key contributors to the Asia Pacific HSM market in 2025.

The hardware security modules industry in Japan is expected to grow at a significant CAGR from 2026 to 2033, due to accelerating digital transformation across enterprises, rising adoption of cloud computing, and increasing deployment of advanced cybersecurity frameworks to protect sensitive financial, industrial, and government data. Japan’s strong focus on data protection, regulatory compliance, and secure digital infrastructure is driving organizations to adopt hardware-based cryptographic solutions for secure key management, encryption, and authentication across hybrid and multi-cloud environments. In addition, the expansion of digital payment systems, IoT-enabled manufacturing (Industry 4.0), and smart city initiatives is increasing the need for high-assurance security solutions that can protect connected devices and real-time data flows. The growing emphasis on zero-trust security architectures and the modernization of legacy IT systems across sectors such as BFSI, telecommunications, and automotive are further driving sustained demand for HSM solutions, supporting strong market growth throughout the forecast period.

The India hardware security modules industry is witnessing strong growth driven by rapid digital transformation, expanding cloud adoption, and the large-scale rise of digital payment ecosystems across banking, fintech, and e-commerce sectors. Increasing cybersecurity threats and data breaches are pushing enterprises to adopt hardware-based cryptographic solutions for secure key management, encryption, and authentication, particularly in highly regulated industries such as BFSI and government. In addition, government-led initiatives such as Digital India, Aadhaar-enabled services, and the expansion of digital public infrastructure are significantly increasing the demand for secure identity verification and transaction processing systems. The rapid growth of cloud computing, IoT deployments, and hybrid IT environments is further accelerating the need for scalable and tamper-resistant HSM solutions that can secure sensitive data across distributed networks.

Europe Hardware Security Modules Market Trends

The hardware security modules industry in Europe is growing at a significant CAGR from 2026 to 2033, due to increasing regulatory pressure for data privacy and cybersecurity compliance, particularly under frameworks such as GDPR, eIDAS, and evolving EU cybersecurity directives that require strong encryption, secure key management, and tamper-resistant hardware for protecting sensitive data. Within the region, Spain is also witnessing steady growth, driven by rising digital banking adoption, increasing cloud migration among enterprises, and expanding government-led digital identity and cybersecurity initiatives. Organizations across BFSI, government, healthcare, and industrial sectors are rapidly adopting HSM solutions to secure digital identities, financial transactions, and critical infrastructure as cyber threats continue to rise in sophistication and frequency. In addition, the accelerated adoption of cloud computing, hybrid IT architectures, and digital payment systems is driving demand for scalable and compliant cryptographic infrastructure that ensures data sovereignty and secure cross-border data processing within the region. The growing focus on digital identity frameworks, secure authentication systems, and zero-trust security models is further supporting sustained HSM adoption across enterprises undergoing large-scale digital transformation.

The UK hardware security modules industryis expected to grow rapidly in the coming years, supported by increasing adoption of cloud computing, rising demand for secure digital payment systems, and the expansion of cybersecurity frameworks across financial services, government, and enterprise sectors. The growing shift toward digital banking, fintech innovation, and real-time payment processing is driving strong demand for hardware-based cryptographic solutions to secure sensitive financial data, manage encryption keys, and ensure compliance with stringent regulatory standards such as GDPR and PCI DSS. In addition, the UK’s focus on strengthening national cybersecurity infrastructure, including zero-trust architectures and secure identity management systems, is further accelerating the deployment of HSM solutions. The rising integration of HSMs into hybrid cloud environments and digital transformation initiatives across industries is also contributing to sustained market growth.

The hardware security modules industry in Germanyheld a significant market share in 2025, driven by strong industrial digitization, stringent data protection regulations, and widespread adoption of secure cryptographic infrastructure across BFSI, automotive, manufacturing, and government sectors. The country’s strict compliance environment under GDPR and national cybersecurity frameworks has significantly increased the need for hardware-based key management, encryption, and authentication solutions to secure sensitive enterprise and industrial data. In addition, Germany’s leadership in Industry 4.0 initiatives and smart manufacturing has accelerated the deployment of HSMs to protect IoT-enabled systems, connected production environments, and industrial control networks. The rapid shift toward cloud computing, hybrid IT environments, and digital identity systems is further strengthening demand for secure and scalable cryptographic solutions, supporting the country’s strong position in the European HSM market in 2025.

Key Hardware Security Modules Company Insights

Some of the key companies operating in the market include Amazon Web Services (AWS), Atos SE, Cavium (Marvell Technology), and Crypto4A Technologies, among others. These companies are some of the leading participants in the hardware security modules market.

-

In April 2026, BTQ Technologies partnered with Daou Data to develop hardware-rooted post-quantum cryptography solutions for securing South Korea’s payment infrastructure, focusing on strengthening payment gateways and networks against future quantum computing threats.

-

In April 2026, Sectigo launched Private PQC, a new feature in its certificate management platform that allows enterprises to test and manage post-quantum cryptography (PQC) certificates within existing workflows without requiring new infrastructure or tools.

Key Hardware Security Modules Companies:

The following key companies have been profiled for this study on the hardware security modules market.

- Amazon Web Services (AWS)

- Atos SE

- Cavium (Marvell Technology)

- Crypto4A Technologies

- Entrust Corporation

- Futurex

- Google LLC

- Hewlett Packard Enterprise (HPE)

- IBM Corporation

- Ledger

- Micro Focus

- Microsoft Corporation

- Securosys SA

- Thales Group

- Utimaco GmbH

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Thales Group; IBM; Entrust; Utimaco; Futurex

- Expanding from traditional on-premise HSM appliances toward cloud-native HSM and HSM-as-a-Service (HSMaaS) platforms integrated with multi-cloud environments.

- Strengthening portfolios through partnerships with hyperscalers, payment processors, and cybersecurity vendors to support enterprise encryption and zero-trust architectures.

- Investing heavily in post-quantum cryptography (PQC), confidential computing, and crypto-agility capabilities to prepare for future cybersecurity threats.

- Strong global enterprise relationships with banks, governments, cloud providers, and telecom operators create high customer retention and long-term contracts.

- Extensive compliance certifications such as FIPS 140-3, PCI DSS, Common Criteria, and eIDAS provide strong credibility and regulatory trust.

- Proven capability to manage mission-critical cryptographic operations for high-volume payment processing, digital identity, and cloud security workloads.

- Legacy HSM architectures may create integration complexity with modern cloud-native and DevSecOps environments.

- High deployment, maintenance, and compliance costs can limit adoption among SMEs and mid-market enterprises.

- Longer product development cycles and complex procurement structures may slow innovation compared to agile cybersecurity startups.

Emerging Players: Yubico; Fortanix; Crypto4A; Sepior; Unbound Security

- Developing lightweight, cloud-first cryptographic platforms designed for hybrid cloud, containers, and Kubernetes-based environments.

- Leveraging technologies such as multi-party computation (MPC), confidential computing, and decentralized key management to reduce dependence on traditional hardware appliances.

- Focusing on niche high-growth use cases including digital asset custody, blockchain security, API security, and quantum-safe encryption.

- Faster deployment of innovative features such as SaaS-based key management, API-driven encryption, and automated certificate lifecycle management.

- Agile product architectures enable easier integration with DevOps pipelines, cloud-native applications, and modern identity platforms.

- Strong specialization in emerging security domains such as cryptocurrency infrastructure, zero-trust security, and post-quantum readiness.

- Limited global support infrastructure and smaller enterprise sales networks can restrict expansion into large regulated industries.

- Lower brand recognition and fewer compliance certifications compared to established HSM vendors may impact trust among government and BFSI customers.

- High dependence on emerging technology adoption trends and venture-backed funding may create concerns around long-term scalability and stability.

Hardware Security Modules Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.8 billion

Estimated market size in 2026

USD 2.01 billion

Projected market size by 2033

USD 5.03 billion

Growth rate

CAGR of 14.0% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Type, deployment, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Amazon Web Services (AWS); Atos SE; Cavium (Marvell Technology); Crypto4A Technologies; Entrust Corporation; Futurex; Google LLC; Hewlett Packard Enterprise (HPE); IBM Corporation; Ledger; Micro Focus; Microsoft Corporation; Securosys SA; Thales Group; Utimaco GmbH

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Hardware Security Modules Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global hardware security modules market report based on type, deployment, application, end-use, and region.

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

LAN-based

-

PCIE-based

-

USB-based

-

Cloud-based

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

On-Premises

-

Cloud

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Payment Processing

-

Authentication

-

Public Key Infrastructure (PKI) Management

-

Database Encryption

-

IoT Security

-

Others

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Government

-

Healthcare and Life Sciences

-

Retail and Consumer Products

-

Technology and Communication

-

Industrial and Manufacturing

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

HSM adoption opportunity assessment for a cybersecurity infrastructure provider

- Assessment of Hardware Security Module (HSM) demand across BFSI, cloud service providers, government, healthcare, and telecom sectors.

- Analysis of adoption trends for payment HSMs, cloud HSMs, and general-purpose HSM solutions.

- Benchmarking of key vendors, certification standards, deployment models, and pricing strategies.

- Identified high-growth application areas such as digital payments, cloud encryption, and PKI management.

- Supported product positioning for cloud-native and hybrid HSM solutions.

- Highlighted key growth drivers, restraints, and regulatory compliance requirements.

HSM market entry and competitive benchmarking for a cloud security vendor

- Analysis of regional cybersecurity spending and encryption infrastructure investments.

- Evaluation of certification requirements including FIPS 140-3, PCI DSS, GDPR, and Common Criteria.

- Assessment of cloud adoption trends, hybrid IT environments, and confidential computing requirements.

- Identified attractive regional opportunities across Middle East & Africa.

- Supported GTM and channel partnership strategies for enterprise and cloud ecosystems.

- Enabled strategic expansion into digital banking, sovereign cloud, and zero-trust security markets.

Customized cross-segmentation analysis for HSM market by deployment type and end use industry

- Conducted cross-segmentation analysis by deployment model and end-user industry.

- Evaluated adoption trends across on-premise HSM and cloud HSM.

- Identified high-adoption use cases driving enterprise encryption investments.

- Highlighted sectors with strongest demand including BFSI, automotive and public sector organizations.

- Supported strategic understanding of security modernization trends across industries.

Frequently Asked Questions About This Report

Some key players operating in the hardware security modules market include Alfresco Software, Inc., Box, Inc., DocuWare Corporation, Hyland Software, Inc. International Business Machines Corporation, Laserfiche, M-Files Corporation, Microsoft, OpenText Corporation, and Oracle.

The hardware security modules (HSM) market is driven by several key factors, reflecting the increasing emphasis on robust cybersecurity measures across industries. The growing incidences of data breaches and cyber-attacks have heightened the need for advanced security solutions, prompting organizations to adopt HSMs for their superior encryption and key management capabilities.

Asia Pacific is the fastest-growing region over the forecast period.

The global hardware security modules market size was estimated at USD 1.8 billion in 2025 and is expected to reach USD 2.0 billion in 2026

North America dominated the hardware security modules market with a market share of 35.7% in 2025. The hardware security modules (HSM) market in North America is experiencing robust growth, driven by the region's strong emphasis on cybersecurity and stringent regulatory requirements. The increasing adoption of advanced technologies such as cloud computing, IoT, and digital payments necessitates enhanced security measures, fostering the demand for HSMs.

USB-based segment accounted for the largest revenue share of 42.4% in 2025, while cloud-based segment is the fastest-growing segment.

The payment processing segment accounted for the largest revenue share in 2025.

The global hardware security modules market is expected to grow at a compound annual growth rate of 14.0% from 2026 to 2033 to reach USD 5.0 billion by 2033

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.