- Home

- »

- Renewable Chemicals

- »

-

Hydrocolloids Market Size, Share, Growth Report, 2026-2033GVR Report cover

![Hydrocolloids Market (2026 - 2033)Report]()

Hydrocolloids Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Gelatin, Xanthan Gum, Carrageenan, Alginates, Pectin, Guar Gum, Gum Arabic, Carboxymethyl Cellulose, Agar), By Function, By Application (Food & Beverages), By Region, And Segment Forecasts

Market Size, 2025

$13.6BMarket Estimate, 2026

$14.4BMarket Forecast, 2033

$20.4BCAGR, 2026–2033

5.0%Hydrocolloids Market Summary

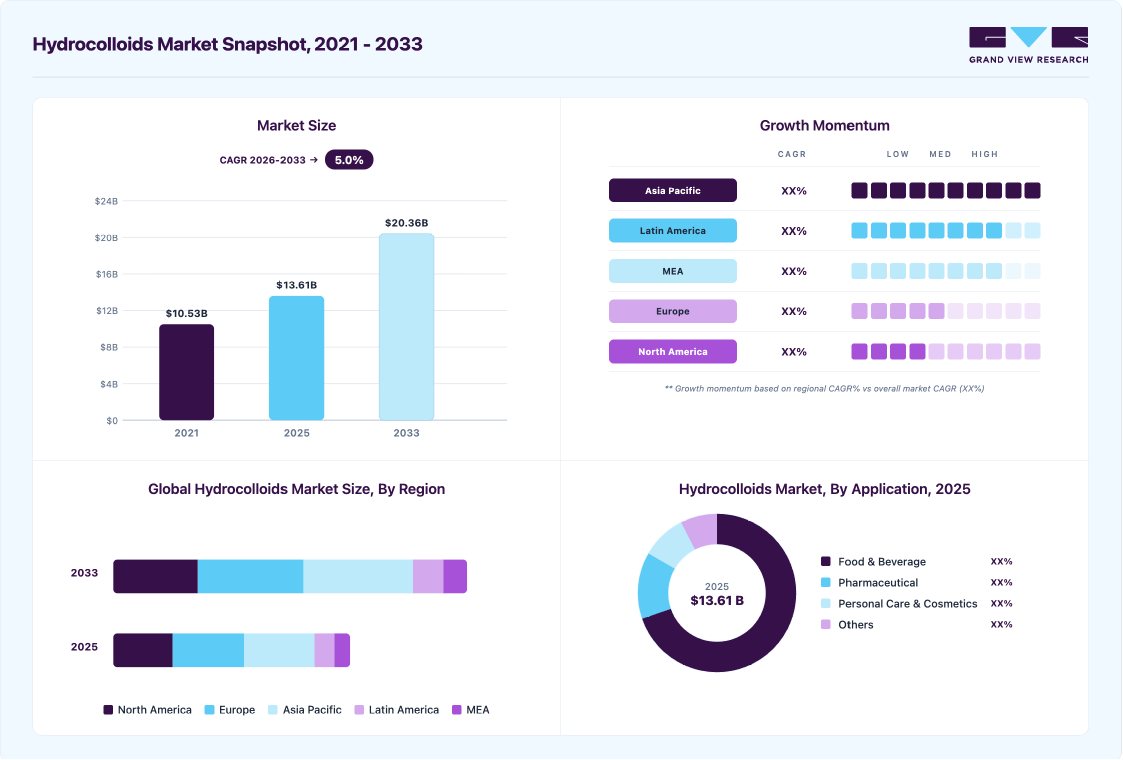

The global hydrocolloids market size was valued at USD 13.6 billion in 2025 and is projected to grow from USD 14.4 billion in 2026 to USD 20.4 billion by 2033, at a CAGR of 5.0% from 2026 to 2033. The Europe held the largest share of 30.2% of the global market in 2025, driven by rising demand for functional and clean-label ingredients across food, beverage, pharmaceutical, and personal care applications. Increasing consumption of processed and convenience foods, coupled with the need for improved texture, stability, and shelf life, is accelerating adoption, while ongoing formulation innovation and sustainable sourcing further support market growth.

Key Market Trends & Insights

- By product: Gelatin segment holds a largest market revenue share of 34.9% in 2025.

- By function: Gelling function dominates the market with share of 48.2% in 2025.

- By application: Food & beverage segment held the largest share of 69.7% in 2025.

Regional Highlights

- Largest regional market: Europe (30.2% revenue share, 2025)

- Fastest-growing regional market: Asia pacific (highest CAGR, 2026-2033)

- By country: The Germany led the Europe market in 2025.

Market Size & Forecast

- Market size in 2025: USD 13.6 Billion

- Estimated market size in 2026: USD 14.4 Billion

- Projected market size by 2033: USD 20.4 Billion

- CAGR (2026-2033): 5.0%

Growth in the hydrocolloids market is further supported by technological advancements in extraction, fermentation, and formulation processes, which are improving product consistency, functionality, and cost efficiency. Enhanced production technologies enable suppliers to develop tailored, high-performance hydrocolloid solutions, supporting wider adoption across diverse industrial applications.")

The hydrocolloids market presents a strong opportunity through the rising adoption of plant-based and alternative protein products, where hydrocolloids play a critical role in replicating texture, mouthfeel, and stability. Increasing consumer preference for vegan and sustainable foods is encouraging manufacturers to invest in innovative hydrocolloid solutions, opening new growth avenues across global markets.

Market Dynamics

The global hydrocolloids market is witnessing significant growth on the back of rising demand for convenience foods among health-conscious consumers. Hydrocolloids find applications in various industries such as oil, food, and pharmaceuticals. The extensive range of functions performed by hydrocolloids in the food industry is a key driver of the market. The primary function that contributes to the widespread use of hydrocolloids in the food industry is their ability to bind water and enhance the properties of food ingredients. Increasing demand for healthy food products is likely to translate into an increasing demand for hydrocolloids, thereby fueling the growth of the global hydrocolloids market.

Today, a majority of the consumers are increasingly preferring healthy and nutritious food items. Rising consumer preference for natural ingredients and the varied applications of hydrocolloids, which involve extensive research & development and innovation in the food &beverage industry, are the reasons for the uptick in the demand for hydrocolloids. In pharmaceuticals industry, hydrocolloids are used for the preservation of parenteral drugs.

The green ammonia market faces challenges due to the high capital investment required for electrolyzers, renewable power integration, storage facilities, and transportation infrastructure. Compared to conventional ammonia production, green ammonia manufacturing involves higher operational and production costs, which impact large-scale commercial adoption. Also, limited renewable energy availability and underdeveloped hydrogen infrastructure in several regions continue to restrict market expansion.

According to the International Energy Agency and the International Renewable Energy Agency, the cost competitiveness of green hydrogen and ammonia remains strongly dependent on affordable renewable electricity and infrastructure development. These economic and infrastructure-related limitations are slowing commercialization and broader adoption of green ammonia projects globally.

Market Concentration & Characteristics

The hydrocolloids market is moderately consolidated, with a limited number of multinational players accounting for a significant share of global revenue due to their strong R&D capabilities, diversified product portfolios, and established relationships with large food and pharmaceutical manufacturers. These companies benefit from economies of scale, global distribution networks, and regulatory expertise, creating high entry barriers for new participants.

Market characteristics are defined by application-specific customization, raw material dependency, and compliance with stringent quality standards. Demand is largely driven by functional performance, consistency, and clean-label compatibility, while innovation, sustainable sourcing, and formulation support play a critical role in differentiation and long-term competitiveness.

Product Insights

The gelatin segment holds a largest market revenue share of 34.9% in 2025, supported by its broad application range and multifunctional performance. Strong demand from food and pharmaceutical industries, along with gelatin’s proven gelling strength, stability, and compatibility with existing formulations, continues to drive its widespread adoption and reinforce its market dominance.

Xanthan gum is significant growing segment with CAGR of 5.0% from forecast period, driven by xanthan gum’s high functional efficiency, cost-effectiveness, and wide applicability across food, beverages, and industrial uses. Its stability under varied processing conditions and strong alignment with clean-label and gluten-free formulations continue to support rising demand.

Function Insights

The gelling function dominates the hydrocolloids market with revenue share of 48.2% in 2025, due to its critical role in providing structure, texture, and mouthfeel across a wide range of food and beverage applications, including confectionery, dairy, desserts, and processed foods. Strong demand for texture consistency, product differentiation, and extended shelf life in mass-produced foods continues to drive high consumption of gelling hydrocolloids. In addition, their ability to replace fat and improve sensory attributes supports sustained adoption by large-scale food manufacturers.

The stabilizing function is the fastest-growing segment with revenue CAGR of 6.2% from forecast period, supported by rising demand for complex formulations requiring emulsion stability, uniform dispersion, and longer shelf life. Growth in ready-to-drink beverages, plant-based alternatives, sauces, and functional foods is accelerating the use of stabilizing hydrocolloids to maintain product quality during processing and storage. Increasing focus on clean-label and performance-driven formulations further strengthens demand for advanced stabilizing solutions.

Application Insights

The food & beverages application segment dominates the hydrocolloids market with revenue share of 69.7% in 2025, supported by extensive use of hydrocolloids for texture enhancement, stabilization, shelf-life improvement, and moisture control across processed foods and beverages. Growing demand for clean-label, plant-based, and convenience food products further reinforces the segment’s leading position.

The pharmaceutical segment is the fastest growing segment with revenue CAGR of 5.7% during forecast period, driven by increasing use of hydrocolloids as excipients, binders, controlled-release agents, and stabilizers in solid and liquid dosage forms. Rising global healthcare spending, expanding generic drug production, and growth in nutraceuticals and functional supplements are accelerating demand. Moreover, the shift toward patient-centric formulations, including liquid and modified-release products, is strengthening adoption of high-purity hydrocolloids in pharmaceutical applications.

Regional Insights

Europe dominated the hydrocolloid market with revenue share of 30.2% in 2025, is supported by strict quality and food safety regulations and a strong shift toward natural, plant-based, and sustainable ingredients. A mature food processing sector and growing pharmaceutical usage are reinforcing steady demand for texture-enhancing and stabilizing solutions across the region.

Germany Hydrocolloids Market Trends

Germany’s hydrocolloids market is driven by its well-established food processing and pharmaceutical industries and a strong focus on quality, traceability, and sustainability. Regulatory compliance and advanced manufacturing standards are encouraging consistent demand for specialty hydrocolloid solutions.

North America Hydrocolloids Market Trends

The hydrocolloids market in North America is driven by sustained demand from the food, beverage, and pharmaceutical industries, supported by advanced processing capabilities and continuous product innovation. Strong emphasis on clean-label formulations and functional ingredients, combined with well-established regulatory frameworks, continues to encourage adoption across high-value applications.

The U.S. market benefits from strong consumer demand for functional, clean-label, and plant-based food products, alongside continuous innovation by ingredient manufacturers. A mature regulatory environment and high R&D investment continue to support adoption in premium food and pharmaceutical applications.

Asia Pacific Hydrocolloids Market Trends

Asia Pacific represents a high-growth region for the hydrocolloids market, fueled by rapid expansion of food processing industries, rising urban consumption, and increasing availability of key raw materials such as seaweed and guar. Growing disposable incomes and evolving dietary patterns are further accelerating market penetration across multiple end-use sectors.

China’s hydrocolloids market growth is underpinned by its large-scale food manufacturing base and strong domestic availability of raw materials. Upgrading food safety standards and increasing use of hydrocolloids in pharmaceutical and personal care formulations are reinforcing long-term market expansion.

Middle East & Africa Hydrocolloids Market Trends

The hydrocolloids market in the Middle East & Africa is gradually gaining momentum due to investments in food manufacturing infrastructure and rising demand for packaged and processed foods. Increasing awareness of product quality, shelf stability, and health attributes is supporting wider use of hydrocolloids in food, beverage, and personal care applications.

Latin America Hydrocolloids Market Trends

Latin America’s hydrocolloids market is expanding on the back of growth in processed food and beverage production and a rising preference for clean-label ingredients. Improving regulatory standards and increasing urbanization in key economies are further contributing to steady demand for functional food ingredients.

Key Hydrocolloids Company Insights

DuPont maintains a strong position in the global hydrocolloids market through its portfolio of functional ingredients such as pectin and gellan gum, serving food, beverage, pharmaceutical, and industrial applications. The company leverages advanced R&D and biotechnology expertise to improve texture, stability, and formulation efficiency, while focusing on clean-label solutions and sustainable production to address evolving customer and regulatory requirements.

Palsgaard A/S is a specialized ingredient supplier offering hydrocolloid-based stabilizing and texturizing solutions primarily for food applications including bakery, dairy, sauces, and dressings. The company emphasizes plant-based and sustainable ingredient systems, supported by strong application know-how and customer-centric formulation support, aligning its offerings with clean-label trends and global food industry standards.

Key Hydrocolloids Companies:

The following key companies have been profiled for this study on the hydrocolloids market.

- DuPont

- Palsgaard

- Nexira

- Ingredion, Incorporated

- Kerry

- BASF

- Ashland

- Glanbia Nutritionals

- Darling Ingredients, Inc.

- Tate & Lyle Plc

- Cargill, Incorporated

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: CP Kelco U.S. Inc.; Ingredion Incorporated; BASF SE; Cargill, Incorporated

- Market participants such as Cargill Incorporated, and CP Kelco are integrated across the value chain, where the company produces hydrocolloids and uses them for developing end-use products.

- The companies are aiming at backward integrated I.e., is internally producing raw materials to reduce cost.

- The global hydrocolloids market is fragmented in nature with numerous market participants. However, a limited number of big multinational companies possess the caliber of bringing innovations into the global market.

- Hydrocolloid being a niche product, the market faces limited consumer awareness due to which it is difficult for the producers to position their product on a wide scope as per the consumer requirement

Emerging Players: Glanbia Nutritionals; Ashland Inc.; DSM; ADM

- Companies are adopting backward as well as frontwards integration in order to ensure a consistent supply of raw materials and reduce logistic and operational costs

- The players in the market tend to compete on the quality and price owing to availability of Hydrocolloid products at a comparatively reasonable cost.

- The manufacturers are more inclined to use conventional ingredient to manufacture their products due to which the innovation sector in the hydrocolloid market has been facing problem, leading to slower growth rate of the industry.

Recent Developments

-

On June 20, 2024, Tate & Lyle completed the $1.8 billion acquisition of CP Kelco on 15 November 2024, bringing a leading producer of pectin and specialty gums into its portfolio to strengthen its global speciality food and beverage ingredient solutions and enhance capabilities across sweetening, mouthfeel and fortification categories.

Hydrocolloids Market Report Scope

Report Attribute

Details

Market size in 2025

USD 13.6 billion

Estimated market size in 2026

USD 14.4 billion

Projected market size by 2033

USD 20.4 billion

Growth rate

CAGR of 5.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, function, application, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

DuPont; Palsgaard; Nexira; Ingredion, Incorporated; Kerry; BASF; Ashland; Glanbia Nutritionals; Darling Ingredients, Inc.; Tate & Lyle Plc; Cargill, Incorporated

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Hydrocolloids Market Report Segmentation

This report forecasts volume & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global hydrocolloids market report based on product, function, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Gelatin

-

Xanthan Gum

-

Carrageenan

-

Alginates

-

Pectin

-

Guar Gum

-

Gum Arabic

-

Carboxymethyl Cellulose

-

Agar

-

Locust Bean Gum

-

-

Function Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Thickening

-

Gelling

-

Stabilizing

-

Other Functions

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Food & Beverages

-

Pharmaceutical

-

Personal Care & Cosmetics

-

Other Applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Trade Analysis

Comprehensive assessment of international trade for xanthan gum and related hydrocolloids using product-specific HS codes. Study includes export-import volumes, leading supplier countries, trade balance evaluation, customs trends, and demand movement across food, oilfield, pharmaceutical, and industrial applications.

Deliver clarity on global supply concentration, dependency on key exporting nations, and evolving trade dynamics. Assist stakeholders in procurement optimization, supplier diversification, and regional sourcing strategy development.

Regional Segmentation

In-depth breakdown of different hydrocolloid product demand and consumption trends across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, including country-level evaluation of major end-use sectors and growth intensity.

Highlight the most commercially attractive regions and uncover regional demand variations by application. Support market prioritization, distribution planning, and expansion strategy formulation.

Pricing Trend Analysis

Evaluation of historical and current xanthan gum, guar gum, etc. pricing patterns considering corn prices, fermentation costs, energy expenses, freight movements, and supply-demand fluctuations across major producing and consuming regions.

Support better pricing visibility and cost forecasting for manufacturers, distributors, and buyers. Enable informed purchasing decisions and identification of factors influencing margin fluctuations and market stability.

Frequently Asked Questions About This Report

Europe dominated with a 30.2% revenue share in 2025.

Asia pacific is the fastest-growing region over the forecast period.

The gelling function segment led with a 48.2% revenue share in 2025, while stabilizing function is the fastest-growing function.

The food & beverage segment dominated the market with a revenue share of 69.7% in 2025, while pharmaceutical is the fastest-growing application.

Key players include DuPont; Palsgaard; Nexira; Ingredion, Incorporated; Kerry; BASF; Ashland; Glanbia Nutritionals; Darling Ingredients, Inc.; Tate & Lyle Plc; Cargill, Incorporated.

The market is driven by rising demand for functional and clean-label ingredients across food, beverage, pharmaceutical, and personal care applications. Increasing consumption of processed and convenience foods, coupled with the need for improved texture, stability, and shelf life, is accelerating adoption, while ongoing formulation innovation and sustainable sourcing further support market growth.

The gelatin segment holds a largest market revenue share of 34.9% in 2025, supported by its broad application range and multifunctional performance. Strong demand from food and pharmaceutical industries, along with gelatin’s proven gelling strength, stability, and compatibility with existing formulations, continues to drive its widespread adoption and reinforce its market dominance.

The global hydrocolloids market size was valued at USD 13.6 billion in 2025 and is estimated at USD 14.4 billion for 2026.

The global hydrocolloids market is expected to grow at a CAGR of 5.0% from 2026 to 2033, reaching USD 20.4 billion by 2033.

About the Author(s)

Renewable Chemicals Research Team

Specialty & Chemicals · Renewable ChemicalsThis report was authored by the renewable chemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the renewable chemicals segment of the specialty & chemicals industry. All findings are based on proprietary specialty & chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.