- Home

- »

- Advanced Interior Materials

- »

-

Low-E Glass Market Size, Share & Trends Report 2026-2033GVR Report cover

![Low-E Glass Market (2026 - 2033)Report]()

Low-E Glass Market (2026 - 2033)

Size, Share & Trends Analysis Report By Coating (Hard, Soft), By Glazing (Single, Double, Triple), By End-use (Building & Construction, Aerospace, Automotive), By Region (North America, Europe, Asia Pacific), And Segment Forecasts

Market Size, 2025

$15.3BMarket Estimate, 2026

$16.6BMarket Forecast, 2033

$28.4BCAGR, 2026–2033

8.0%Low-E Glass Market Summary

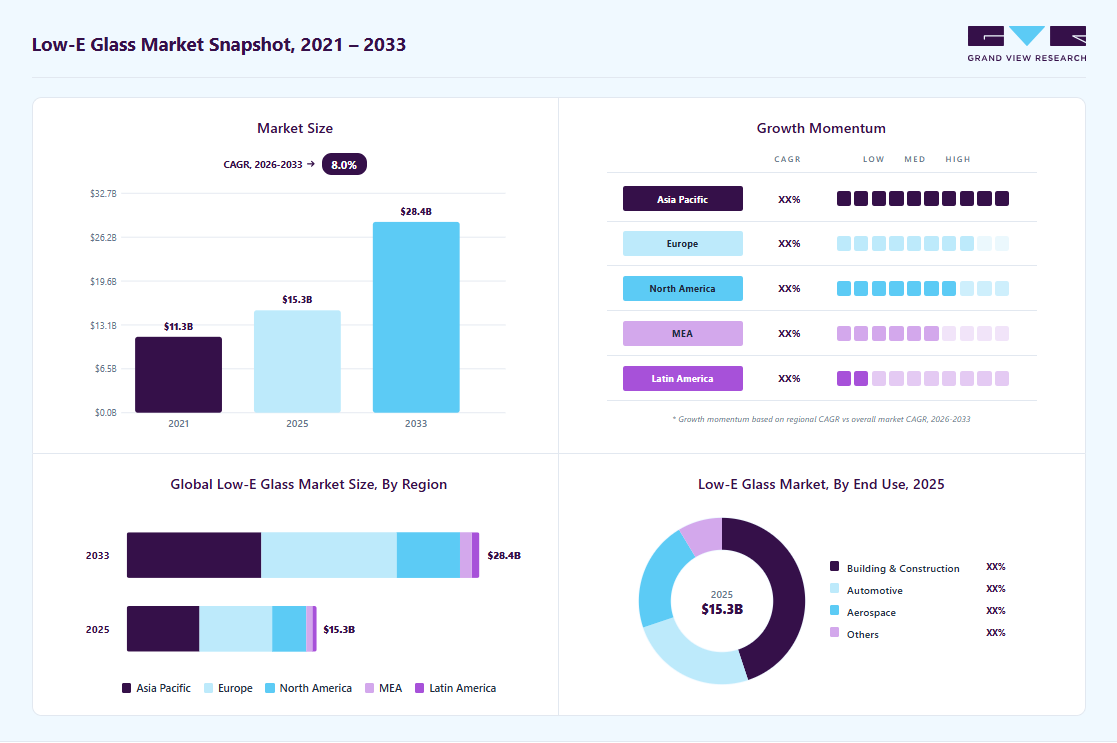

The global low-e glass market size was valued at USD 15.3 billion in 2025 and is projected to grow from USD 16.6 billion in 2026 to USD 28.4 billion by 2033, at a CAGR of 8.0% from 2026 to 2033. The Europe market held the largest share of 38.0% of the global market in 2025. The market is being strongly driven by rising global demand for energy-efficient buildings.

Key Market Trends & Insights

- By coating: The soft held the revenue share of over 68.0% in 2025.

- By glazing: The double glazing held the revenue share of 58.0% in 2025.

- By end-use: The building & construction segment held the revenue share of over 44.0% in 2025.

Regional Highlights

- Largest regional market: Europe (38.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 15.3 Billion

- Estimated market size in 2026: USD 16.6 Billion

- Projected market size by 2033: USD 28.4 Billion

- CAGR (2026-2033): 8.0%

Low-E (low-emissivity) glass features a microscopically thin metallic coating that reflects infrared and UV light while allowing visible light to pass through. This regulates indoor temperatures by keeping heat inside during winter and blocking solar heat in summer, significantly improving energy efficiency. Low-e glass reduces heat transfer, which lowers heating and cooling loads in residential and commercial spaces. As electricity prices rise and building owners focus more on lifecycle cost savings, developers are increasingly specifying low-e glazing in new construction and renovation projects. This makes it a preferred material in modern façade systems and insulated window units.")

Stringent building energy codes and green construction policies are another major growth catalyst. Governments across regions are tightening standards for thermal insulation, carbon emissions, and overall building performance. Regulations tied to net-zero and zero-emission buildings are encouraging widespread adoption of advanced glazing products, especially in Europe, North America, and fast-growing Asian markets. These policy shifts are creating steady replacement demand in retrofit projects as well.

Rapid urbanization and infrastructure development are further accelerating market growth. Expanding cities, commercial complexes, airports, hospitals, and premium residential projects increasingly require high-performance glass solutions for thermal comfort and natural light optimization. Emerging economies such as India, China, and Southeast Asian countries are seeing strong uptake due to growing awareness of sustainable building materials and rising construction activity.

The automotive industry is also supporting demand for low-e glass, particularly with the rise of electric vehicles and premium passenger cars. Automakers are using advanced glazing to improve cabin comfort, reduce solar heat gain, and enhance energy efficiency by lowering air-conditioning load. In electric vehicles, this directly supports battery efficiency and driving range, making low-e coatings increasingly valuable in side windows, windshields, and sunroofs.

Drivers, Opportunities & Restraints

The market is primarily driven by rising demand for energy-efficient buildings and stricter thermal performance standards in residential and commercial construction. Governments across major economies are enforcing green building codes and carbon reduction targets, which is increasing the adoption of insulated glazing and coated glass solutions. Growing urbanization, rising electricity costs, and higher consumer awareness about indoor comfort are further supporting demand.

The market has strong growth opportunities in green retrofitting projects, smart buildings, and emerging economies where construction activity is expanding rapidly. Increasing demand for premium façades, energy-saving windows, and sustainable infrastructure in countries such as India, China, and Southeast Asia is creating new avenues for manufacturers. Technological advancements such as double-silver and triple-silver coatings, more effective solar control, and smart glazing integration are also expected to widen application scope in both buildings and vehicles.

High initial installation costs compared to conventional glass remain a key restraint, especially in price-sensitive markets. The market also faces challenges from raw material price volatility, energy-intensive manufacturing processes, and supply chain disruptions affecting coated glass production. In some developing regions, limited awareness, lack of skilled installation, and lower enforcement of energy codes may slow adoption. Competition from alternative glazing technologies can also affect market penetration.

Coating Insights

Soft held the revenue share of over 68.0% in 2025. The soft coat low-e glass, typically produced through magnetron sputtering, offers lower emissivity and improved heat reflection, making it highly effective in reducing indoor heating and cooling loads. As building energy codes become stricter and developers prioritize high-performance façades, insulated windows, and curtain wall systems, demand for soft-coated glass continues to rise across residential and commercial construction.

The hard coat segment is gaining traction due to its durability, scratch resistance, and ease of handling during transportation and installation. Unlike soft-coated glass, hard coated low-e glass is manufactured through pyrolytic coating directly during the float glass process, creating a robust surface that can withstand harsher environmental conditions. This makes it particularly suitable for monolithic applications, storm windows, and cost-sensitive projects where long-term durability and lower maintenance are important. Its ability to provide basic thermal insulation at a relatively lower cost is supporting steady demand in residential and light commercial construction.

End-use Insights

Building & construction segment held the revenue share of over 44.0% in 2025. The building and construction industry is responding to the rising demand for energy-efficient and sustainable building materials. These glasses play a critical role in reducing heat transfer, improving indoor temperature regulation, and lowering HVAC energy consumption in residential, commercial, and institutional buildings. With increasing urbanization, infrastructure development, and rising focus on green building certifications, developers are increasingly incorporating low-e glazing in windows, façades, skylights, and curtain wall systems.

The automotive segment is anticipated to register the fastest CAGR over the forecast period. Low-e glass reduces solar heat gain inside vehicles by reflecting infrared radiation while maintaining visible light transmission. This lowers the need for excessive air conditioning, improving passenger comfort and reducing energy consumption, especially in regions with hot climates.

Glazing Insights

Double glazing held the revenue share of 58.0% in 2025. The double-glazed low-e glass units reduce heat loss in winter and minimize solar heat gain in summer, helping lower energy consumption for heating and cooling. As residential and commercial buildings increasingly focus on reducing utility costs and meeting green building standards, double glazing has become a widely adopted solution in both new construction and renovation projects.

The single glazing segment continues to see demand in cost-sensitive applications where basic thermal performance and affordability are key priorities. In certain residential buildings, interior partitions, secondary structures, and mild-climate regions, single glazed low-e glass offers an economical way to improve energy efficiency over conventional clear glass. Its lower upfront cost, lighter weight, and simpler installation make it attractive for budget-conscious builders and retrofit projects.

Regional Insights

Europe held over 38.0% revenue share of the global low-e glass market, driven primarily by stringent energy efficiency regulations and decarbonization targets across the region. The EU’s push toward lower building emissions, stricter thermal insulation standards, and renovation mandates for aging residential and commercial stock are accelerating the adoption of high-performance glazing solutions. Low-e glass reduce heating losses during winter and minimizes solar heat gain in summer, making it an essential material for compliance with green building certifications and energy codes.

Asia Pacific Low-E Glass Market Trends

Asia Pacific is a major growth engine for the market due to rapid urbanization, large-scale infrastructure investments, and rising demand for energy-efficient buildings. Countries such as China, India, Japan, and Southeast Asian nations are witnessing strong residential and commercial construction activity, which is increasing the use of advanced glazing solutions to improve insulation and indoor comfort.

North America Low-E Glass Market Trends

North America’s market is being strongly driven by stringent energy efficiency regulations, green building standards, and a rising focus on reducing heating and cooling costs in residential and commercial buildings. Building codes across the U.S. and Canada increasingly emphasize thermal insulation, window performance, and carbon reduction, which is accelerating the use of low-e coated glazing in new construction and retrofit projects.

U.S. Low-E Glass Market Trends

The U.S. market is being driven primarily by stricter energy efficiency standards in residential and commercial construction. Federal and state level building codes increasingly emphasize thermal insulation, reduced HVAC loads, and lower carbon emissions, which is accelerating the use of low-e coated windows, curtain walls, and façades. In addition, the large stock of aging buildings across the country is creating strong retrofit demand, as homeowners and commercial property owners seek to improve energy performance and lower long term utility costs.

Latin America Low-E Glass Market Trends

Latin America’s market is being driven by rising urbanization, expanding residential construction, and growing investments in commercial infrastructure across countries such as Brazil, Mexico, and Chile. As cities continue to modernize, developers are increasingly adopting energy-efficient building materials to improve indoor comfort and reduce cooling costs in warm climates. Low-e glass is gaining traction in windows, façades, and curtain wall systems due to its ability to control solar heat gain while maintaining natural light transmission, making it well suited for the region’s climate conditions.

Key Low-E Glass Company Insights

Some of the key players operating in the market include AGC Inc., Central Glass Co., Ltd., and others

-

AGC Inc. is a flat glass manufacturer with a strong presence across architectural, automotive, and specialty glass applications. The company has built a broad global footprint through advanced float glass production, coating technologies, and energy-efficient glazing systems. AGC offers a wide portfolio, including Planibel Low-E, Sunergy, Energy Select, and Thermobel insulating glass systems. These products are designed to improve thermal insulation, reduce solar heat gain, and support energy-saving building designs.

-

Central Glass Co., Ltd. is a Japanese manufacturer with diversified operations across architectural glass, chemicals, and electronic materials. The company has established a strong reputation in Japan and other Asian markets for supplying quality flat glass products used in residential, commercial, and industrial applications. Central Glass offers energy-efficient products such as Pairlex Heat Guard and Eco-Glass, which are designed to enhance thermal insulation, reduce indoor heat loss, and improve occupant comfort.

Key Low-E Glass Companies:

The following key companies have been profiled for this study on the low-e glass market.

- AGC Inc.

- Central Glass Co. Ltd.

- CEVITAL GROUP

- China Glass Holding, Ltd.

- Euroglas

- Fuyao Glass Industry Group Co., Ltd.

- Guardian Industries

- Nippon Sheet Glass Co., Ltd.

- Saint-Gobain

- SCHOTT AG

Recent Development

-

In January 2026, Vitro Architectural Glass announced the launch of Solarban Champane low-e glass, an innovative product featuring a breakthrough coating that delivers warm-neutral champagne tones with superior solar control and energy efficiency, unlike traditional tinted glass.

Low-E Glass Market Report Scope

Report Attribute

Details

Market Definition

The scope includes the consumption of low-e glass in various applications.

Market size in 2025

USD 15.3 billion

Estimated market size in 2026

USD 16.6 billion

Projected market size by 2033

USD 28.4 billion

Growth rate

CAGR of 8.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, competitive landscape, growth factors, and trends

Segments covered

Coating, glazing, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; Italy; Russia; China; India; Japan; South Korea; Brazil; Saudi Arabia; UAE

Key companies profiled

AGC Inc.; Central Glass Co. Ltd.; CEVITAL GROUP; China Glass Holding, Ltd.; Euroglas; Fuyao Glass Industry Group Co., Ltd.; Guardian Industries; Nippon Sheet Glass Co., Ltd.; Saint-Gobain; SCHOTT AG

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Low-E Glass Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global low-e glass market report based on coating, glazing, end-use, and region.

-

Coating Outlook (Revenue, USD Million; Volume; Kilotons, 2021 - 2033)

-

Hard

-

Soft

-

-

Glazing Outlook (Revenue, USD Million; Volume; Kilotons, 2021 - 2033)

-

Single Glazing

-

Double Glazing

-

Triple Glazing

-

-

End-use Outlook (Revenue, USD Million; Volume; Kilotons, 2021 - 2033)

-

Building & Construction

-

Aerospace

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Million; Volume; Kilotons, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

Italy

-

France

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

Soft segment led with a 68.0% revenue share in 2025.

Double glazing held the revenue share of 58.0% in 2025.

Building & construction segment held the highest market share (over 44.0%) in 2025, while automotive is the fastest-growing segment.

Key factors include the rising demand for energy efficient glazing solutions in residential, commercial, and automotive applications, supported by stricter building energy codes, green construction initiatives, and increasing consumer preference for thermal comfort.

The global low-e glass market size was estimated at USD 15.3 billion in 2025 and is expected to reach USD 16.6 billion in 2026.

The global low-e glass market is expected to grow at a compound annual growth rate of 8.0% from 2026 to 2033 to reach USD 28.4 billion by 2033.

Europe market held the largest share of 38.0% in 2025.

Some of the key players of the global low-e glass market are AGC Inc., Central Glass Co. Ltd., CEVITAL GROUP, China Glass Holding, Ltd., Euroglas, Fuyao Glass Industry Group Co., Ltd., Guardian Industries, Nippon Sheet Glass Co., Ltd., Saint-Gobain, SCHOTT AG, and others.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.