- Home

- »

- Advanced Interior Materials

- »

-

Metal Forging Market Size, Share & Trends Report 2026-2033GVR Report cover

![Metal Forging Market (2026 - 2033)Report]()

Metal Forging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Raw Material (Carbon Steel, Alloy Steel, Aluminum, Magnesium), By Application (Automotive, Transportation, Aerospace, Oil & Gas, Construction, Agriculture), By Region, And Segment Forecasts

Market Size, 2025

$85.9BMarket Estimate, 2026

$93.8BMarket Forecast, 2033

$158.8BCAGR, 2026–2033

7.8%Metal Forging Market Summary

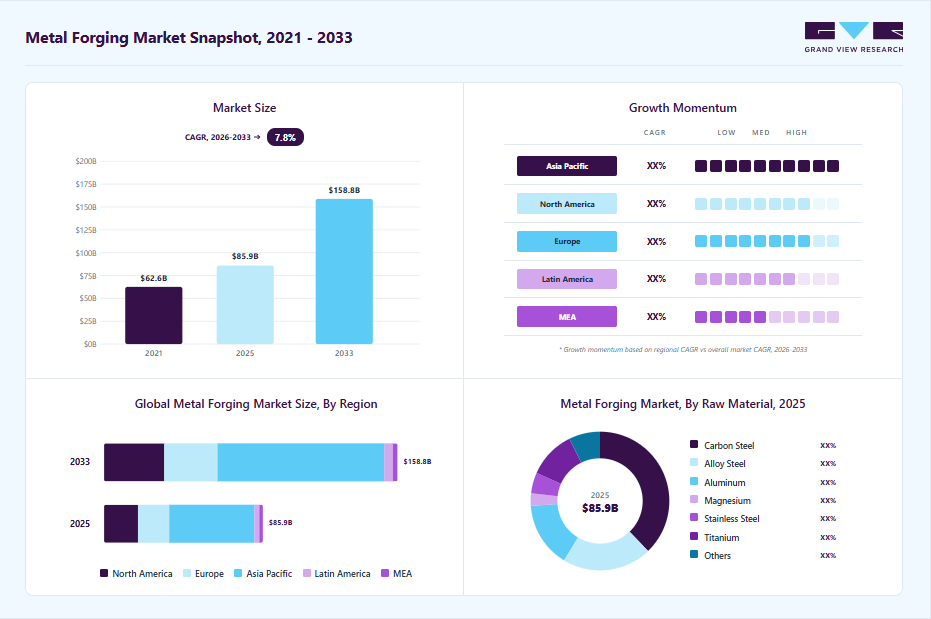

The global metal forging market size was valued at USD 85.9 billion in 2025 and is projected to grow from USD 93.8 billion in 2026 to USD 158.8 billion by 2033, at a CAGR of 7.8% from 2026 to 2033. The Asia Pacific held the largest share of 53.0% of the global market in 2025. The industry is expected to witness steady growth, supported by its essential role in producing high-strength and high-reliability components across key end use industries such as automotive, aerospace, oil and gas, and heavy equipment.

Key Market Trends & Insights

- By raw material: Carbon steel held the largest market share of over 37.0% in 2025.

- By application: The automotive segment accounted for the largest market share of over 52.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (53.0% revenue share, 2025).

- By country: China held the largest regional market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 85.9 Billion

- Estimated market size in 2026: USD 93.8 Billion

- Projected market size by 2033: USD 158.8 Billion

- CAGR (2026-2033): 7.8%

Forging processes enhance mechanical properties, including fatigue resistance, grain structure alignment, and overall durability, making them highly suitable for critical applications where performance and safety are paramount. Growth in industrialization and infrastructure development, particularly in emerging economies, continues to drive demand for forged components in construction equipment, railways, and energy systems. In addition, the increasing focus on product quality and lifecycle performance is reinforcing the adoption of forging over alternative manufacturing methods.")

The evolving automotive sector remains a significant contributor to market demand, particularly with the transition toward electric vehicles. While the shift reduces demand for traditional internal combustion engine components, it creates new opportunities for forged products in structural and safety-related applications such as chassis systems, suspension components, and transmission parts. Furthermore, regulatory pressure related to emissions and fuel efficiency is encouraging the use of lightweight forged materials such as aluminum and magnesium. The aerospace industry also supports market growth through consistent demand for high-performance forged components used in aircraft engines and structural assemblies, where precision and material integrity are critical.

Technological advancements are playing a crucial role in enhancing the efficiency and competitiveness of the metal forging industry. The adoption of automation, robotics, and digital manufacturing technologies is improving production accuracy, cuts operational costs, and enabling real-time quality control. Advanced forging techniques, including precision forging and closed-die forging, are increasingly used to manufacture complex components with minimal material waste.

In November 2024, Schilling Forge, a precision forging supplier based in Syracuse, New York, expanded its operational capabilities by installing a new electrically heated Gasbarre car-bottom furnace, increasing its annealing capacity by 67% to better serve high-precision medical applications such as surgical and dental tools. In addition, the integration of simulation tools and data-driven optimization is reducing design cycles and improving production planning. Sustainability initiatives, including energy-efficient equipment and metal recycling practices, are also gaining importance as manufacturers align with environmental regulations and corporate sustainability goals.

Drivers, Opportunities & Restraints

The metal forging market is primarily driven by the growing demand for high-strength and lightweight components across industries such as automotive, aerospace, construction, and power generation. Increasing vehicle production, particularly in emerging economies, has significantly boosted the consumption of forged parts used in engines, transmissions, and structural components. In addition, the aerospace sector’s focus on safety, performance, and fuel efficiency continues to support the use of forged metals, which offer superior mechanical properties compared to cast or machined parts. Rapid industrialization and infrastructure development across the Asia Pacific further contribute to market expansion.

Significant opportunities exist in the adoption of advanced forging technologies and the shift toward electric vehicles and renewable energy systems. The increasing penetration of electric vehicles is creating demand for specialized forged components such as lightweight shafts, gears, and structural parts. Moreover, advancements in precision forging, automation, and digital manufacturing are improving production efficiency and reducing material waste, enabling manufacturers to cater to high-performance applications. The growing focus on sustainability and recycling of metals also presents opportunities for forging companies to align with environmental regulations and enhance cost efficiency.

However, the market faces certain restraints, including high initial capital investment and fluctuating raw material prices. The establishment of forging facilities requires substantial investment in machinery, tooling, and energy, which can be a barrier for new entrants. Moreover, volatility in the prices of raw materials such as steel and aluminum can impact profit margins and overall production costs.

Raw Material Insights

Carbon steel segment held the revenue share of over 37% in 2025, the carbon steel is the most extensively utilized raw material in the metal forging industry due to its optimal balance of mechanical strength, ductility, and cost efficiency. It is widely deployed across open-die and closed-die forging processes to manufacture high-load, fatigue-resistant components such as crankshafts, connecting rods, gears, shafts, and fasteners. The material’s broad carbon content range allows manufacturers to tailor properties from high ductility in low-carbon grades to superior hardness and wear resistance in high-carbon grades, making it suitable for diverse end-use industries, including automotive, construction, oil & gas, and industrial machinery.

Aluminum is a key material segment in the metal forging industry, primarily driven by its lightweight characteristics, high strength-to-weight ratio, and excellent corrosion resistance. It is extensively used in forging applications where weight reduction without compromising structural integrity is critical, particularly in automotive, aerospace, and transportation sectors. Forged aluminum components such as suspension parts, wheels, aircraft structural elements, and engine components offer superior mechanical performance along with improved fuel efficiency and emission reduction benefits.

Application Insights

Automotive held the revenue share of over 52.0% in 2025. The rapid expansion of electric vehicle production is a major factor accelerating growth in the automotive segment of the metal forging market. Global EV sales surpassed 20 million units in 2025, reflecting a strong shift toward electrified mobility. This transition introduces entirely new vehicle architectures that rely on highly specialized components, many of which are best produced through forging. Unlike internal combustion engine vehicles, EVs require parts such as motor rotors, inverter housings, and battery enclosures that must endure intense thermal fluctuations and mechanical stress.

The power generation segment continues to be a major driver of the metal forging market due to the rapid scale-up of renewable energy capacity worldwide. According to the IEA Renewables 2024 Electricity report, global annual renewable capacity additions are projected to increase from 666 GW in 2024 to nearly 935 GW by 2030. Solar PV and wind alone are expected to account for about 95% of these additions, primarily due to their lower generation costs compared to both fossil fuel and other non-fossil alternatives, along with continued policy support. This large-scale expansion directly drives demand for forged components such as turbine shafts, flanges, and structural rings used in wind and solar infrastructure.

Regional Insights

Asia Pacific metal forging market accounted for the largest revenue share of over 53.0% in 2025. The Asia Pacific region represents one of the most dynamic growth hubs for metal forging, driven by rapid expansion in renewable energy, particularly in wind and solar power. Countries such as China and India are aggressively increasing their installed renewable capacity, with China alone exceeding 400 GW of wind power capacity and continuing to lead global additions. This large-scale deployment is generating strong demand for forged components such as turbine shafts, bearing rings, flanges, and gear systems that are essential for high-capacity wind turbines. In parallel, rising investments in solar energy and grid infrastructure upgrades across the region are further supporting demand for forged products used in power transmission and distribution equipment.

North America Metal Forging Market Trends

The North American market is currently experiencing a robust period of growth, primarily fueled by the accelerating transition to EVs and the revitalization of the automotive supply chain. Forged components are indispensable for EVs because they provide the high-strength, lightweight properties necessary to offset heavy battery packs and improve driving range. As of 2026, manufacturers in the U.S., Canada, and Mexico are increasingly utilizing advanced aluminum and titanium alloys for critical parts such as suspension arms, steering knuckles, and motor housings. This shift is bolstered by the USMCA (United States-Mexico-Canada Agreement) trade provisions, which mandate high regional content and North American-sourced steel and aluminum, incentivizing domestic forging facilities to scale up production.

U.S. Metal Forging Market Trends

The US market is being propelled by robust demand from the aerospace and defense sectors, which are seeing unprecedented levels of investment. The recently authorized nearly USD 900 billion FY2026 National Defense Authorization Act (NDAA) explicitly identifies castings and forgings as priority components for national security, creating a multi-year business opportunity rather than a series of short-term contracts. This funding ensures predictable volume for manufacturers producing everything from submarine structural forgings to aircraft landing gear and propulsion systems. Concurrently, the aerospace industry's need for lightweight, high-strength alloys is driving investment in precision forging technologies to meet the stringent requirements of modern aircraft and spacecraft, with the growing number of global flyers further fueling this demand.

Europe Metal Forging Market Trends

In Europe, the market is undergoing a structural transformation driven by the EU's Green Deal and the "Circular Economy" initiative. As of 2026, forgers are facing intense pressure to decarbonize, leading to a widespread shift from traditional blast furnaces to Electric Arc Furnaces (EAF) and the adoption of high-quality recycled scrap. This transition is being accelerated by the full implementation of the Carbon Border Adjustment Mechanism (CBAM) in January 2026, which effectively places a carbon price on imported steel and aluminum.

Latin America Metal Forging Market Trends

Latin America’s metal forging market is witnessing steady expansion, driven by rising oil and gas activity, strong mining output, and increasing renewable energy investments across major economies such as Brazil, Argentina, Chile, and Peru. Brazil remains the primary growth engine, with its offshore energy sector reaching a historic milestone in 2025 as total oil and natural gas production climbed to 4.89 million barrels of oil equivalent per day, marking a 13.3% increase compared to 2024. Pre salt reserves now contribute close to 80% of this output, highlighting the growing importance of deepwater exploration.

Key Metal Forging Company Insights

Some of the key players operating in the market include Arconic Inc., Bharat Forge Limited, and others

-

Arconic Inc. operates as a specialized manufacturer of aluminum-based engineered products, catering to industries such as aerospace, automotive, and construction. The company’s business model is centered on producing high-performance, lightweight metal solutions for structural and architectural applications. It was previously known as Arconic Rolled Products Corporation and was renamed Arconic Corporation in 2020 following corporate restructuring.

-

Bharat Forge Limited represents a fully integrated forging specialist with a strong global footprint across automotive, industrial, aerospace, and defense sectors. As part of the Kalyani Group, the company has evolved into a high-volume and high-precision forging manufacturer with diversified end-market exposure. The company’s strength lies in its extensive forging portfolio, which includes crankshafts, connecting rods, chassis components, oil & gas forgings, and aerospace-grade parts such as landing gear components.

Key Metal Forging Companies:

The following key companies have been profiled for this study on the metal forging market

- Arconic Inc.

- Allegheny Technologies Incorporated

- Bharat Forge Limited

- Bruck GmbH

- China First Heavy Industries Co., Ltd.

- ELLWOOD Group, Inc.

- Jiangyin Hengrun Heavy Industries Co., Ltd.

- Nippon Steel Corporation

- Precision Castparts Corp.

- Larsen & Toubro Limited

Recent Development

-

In July 2025, Bharat Forge Limited completed the acquisition of AAM India Manufacturing, strengthening its automotive forging capacity and expanding its manufacturing footprint in India. This move enhances its position in drivetrain and component manufacturing.

-

In June 2025, ATI Inc. expanded its production focus on high-performance titanium and nickel-based alloys to meet growing aerospace forging demand, particularly for jet engines and structural applications.

Metal Forging Report Scope

Report Attribute

Details

Market Definition

The market size represents the total annual consumption of forged metal components across end-use industries such as automotive, construction, aerospace, energy, etc.

Market size in 2025

USD 85.9 billion

Estimated market size in 2026

USD 93.8 billion

Projected market size by 2033

USD 158.8 billion

Growth rate

CAGR of 7.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue & volume forecast, competitive landscape, growth factors, and trends

Segments covered

Raw material, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; Italy; France; Spain; China; India; Japan; South Korea

Key companies profiled

Arconic Inc.; Allegheny Technologies Incorporated; Bharat Forge Limited; Bruck GmbH; China First Heavy Industries Co., Ltd.; ELLWOOD Group, Inc.; Jiangyin Hengrun Heavy Industries Co., Ltd.; Nippon Steel Corporation; Precision Castparts Corp.; Larsen & Toubro Limited

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Metal Forging Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global metal forging market report based on raw material, application, and region.

-

Raw Material Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Carbon Steel

-

Alloy steel

-

Aluminum

-

Magnesium

-

Stainless Steel

-

Titanium

-

Others

-

-

Application Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

Automotive

-

Transportation

-

Aerospace

-

Oil & Gas

-

Construction

-

Agriculture

-

Power Generation

-

Marine

-

Others

-

-

Regional Outlook (Revenue, USD Million; Volume, Kilotons; 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

Italy

-

France

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Middle East & Africa

-

Frequently Asked Questions About This Report

Asia Pacific dominated the market with the largest revenue share of over 53.0% in 2025.

The global metal forging market size was valued at USD 85.9 billion in 2025 and is estimated at USD 93.8 billion for 2026.

The global metal forging market is expected to grow at a CAGR of 7.8% from 2026 to 2033, reaching USD 158.8 billion by 2033.

The carbon steel segment led with a market revenue share of over 37.0% in 2025.

The automotive segment held the largest revenue share of over 52.0% in 2025.

Some of the key players operating in the metal forging market include Arconic Inc.; Allegheny Technologies Incorporated; Bharat Forge Limited; Bruck GmbH; China First Heavy Industries Co., Ltd.; ELLWOOD Group, Inc.; Jiangyin Hengrun Heavy Industries Co., Ltd.; Nippon Steel Corporation; Precision Castparts Corp.; and Larsen & Toubro Limited.

Key factors driving the metal forging market include growing demand for high-strength and lightweight components across automotive, aerospace, construction, and power generation industries.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.