- Home

- »

- Next Generation Technologies

- »

-

Mobile Artificial Intelligence Market Size Report, 2026-2033GVR Report cover

![Mobile Artificial Intelligence Market (2026 - 2033)Report]()

Mobile Artificial Intelligence Market (2026 - 2033)

Size, Share & Trends Analysis Report By Technology Node (7 nm, 10 nm, 20-28 nm), By Application (Smartphones, Cameras, Drones, Automobile, Robotics, AR/VR), By Region, And Segment Forecasts

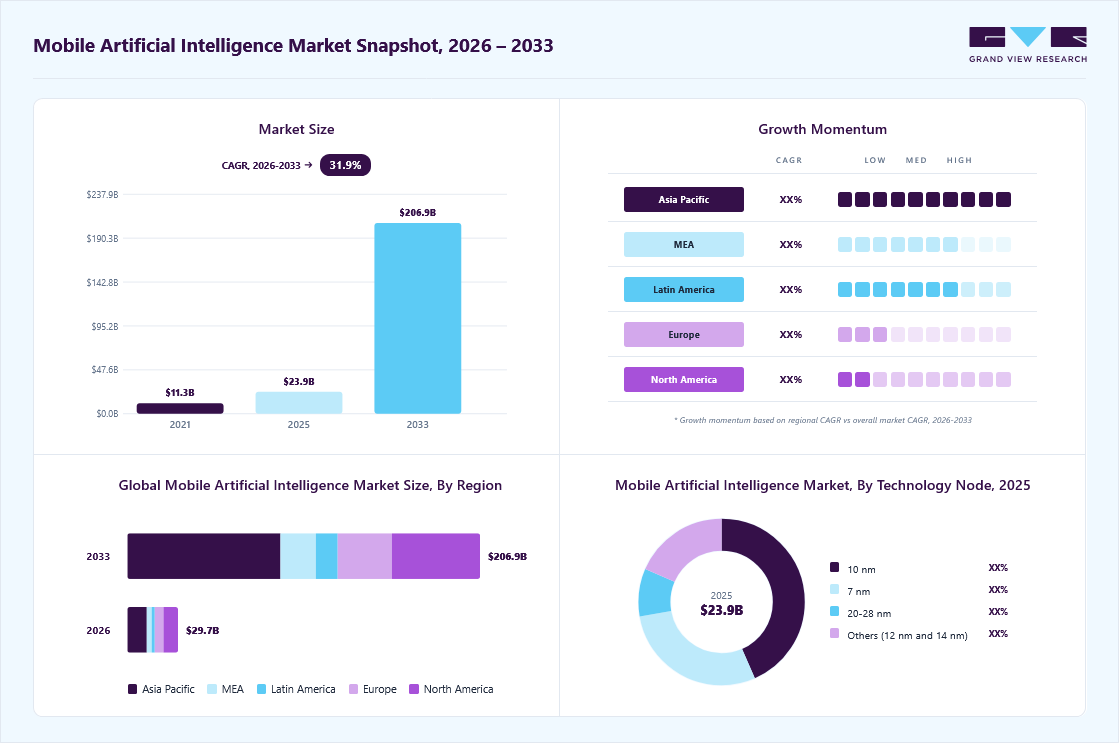

Market Size, 2025

$23.8BMarket Estimate, 2026

$29.7BMarket Forecast, 2033

$206.9BCAGR, 2026–2033

31.9%Mobile Artificial Intelligence Market Summary

The global mobile artificial intelligence market size was valued at USD 23.8 billion in 2025 and is projected to grow from USD 29.7 billion in 2026 to USD 206.9 billion by 2033, at a CAGR of 31.9% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 37.6% in 2025. The global mobile artificial intelligence market is experiencing strong growth, driven by increasing adoption of AI-enabled smartphones, rising demand for on-device processing, advancements in edge AI technologies, and growing integration of generative AI features across mobile applications and devices.

Key Market Trends & Insights

- By Technology Node: 10 nm segment held a significant 43.4% revenue share in 2025.

- By application: Smartphones segment led the market with the largest revenue share of 35.7% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (37.6% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 23.8 Billion

- Estimated market size in 2026: USD 29.7 Billion

- Projected market size by 2033: USD 206.9 Billion

- CAGR (2026-2033): 31.9%

The vast expansion in connectivity with the rollout of 5G and the IoT enables organizations and individuals to collect more real-world data in real-time. This data can be used to improve AI systems further so that they become increasingly sophisticated and capable. These technologies can produce a powerful virtuous circle to generate massive socio-economic benefits. The emerging use of drones is rising quickly for several reasons, including more venture capital financing, demand for drone-generated data for commercial uses, and quickening technology development. Artificial intelligence (AI) is projected to fuel the next generation of drones, enabling them to function autonomously and make choices without human supervision. Drones are cameras and sensors that send information to tiny circuits in vision processing units (VPUs). A drone's VPU processor and sophisticated algorithms are applied.")

Moreover, the mobile Artificial Intelligence (AI) industry growth is driven by ongoing advancements in semiconductor technologies and innovations in AI chip architectures that improve processing speeds, energy efficiency, and scalability. The rising adoption of edge computing accelerates demand for compact, low-power AI hardware capable of real-time data processing closer to data sources, such as in autonomous vehicles, smart devices, and industrial automation. In addition, increasing cloud adoption and expanding AI-as-a-service platforms require powerful AI hardware infrastructure to support large-scale training and inference workloads.

Furthermore, growing internet penetration, smart city initiatives, and the proliferation of IoT devices generating vast amounts of data requiring AI-driven analytics are influencing future market expansion. Major technology players continue to invest heavily in research and development to create energy-efficient AI 7 nm and neuromorphic chips that mimic brain functions for cognitive tasks. With regulatory support and increasing AI adoption across sectors, these developments sustain the AI hardware market’s growth.

Market Dynamics

The global Mobile Artificial Intelligence market is experiencing strong growth due to the increasing integration of AI capabilities into smartphones and mobile applications. Mobile AI is enhancing user experiences through intelligent features such as voice recognition, image processing, and personalized recommendations. The market is benefiting from advancements in mobile computing power and AI algorithms. However, concerns related to data privacy and device performance remain important considerations. Ongoing technological developments are expected to support continued market expansion over the forecast period.

Continuous advancements in mobile processors are enabling smartphones and other mobile devices to handle increasingly complex artificial intelligence workloads. Leading semiconductor companies are integrating specialized neural processing units (NPUs), graphics accelerators, and AI engines into modern chipsets to improve computational efficiency. These enhancements allow devices to process tasks such as image recognition, speech processing, language translation, and predictive analytics directly on the device. As a result, mobile systems are achieving lower latency, improved responsiveness, and reduced reliance on cloud-based infrastructure, which improves overall user experience.

Dedicated AI chipsets are further accelerating the adoption of mobile AI by optimizing performance for machine learning workloads while maintaining energy efficiency. These chipsets are designed to handle parallel processing requirements of AI models, enabling faster inference and real-time decision-making. Improved architecture design helps balance processing power with thermal control and battery consumption, which is critical for mobile environments. In addition, the increasing availability of AI-enabled processors across mid-range and premium smartphones is expanding market penetration. This trend is expected to continue as AI models become more complex and demand for edge-based intelligence increases across consumer and enterprise applications.

High computational and power limitations in mobile devices act as a key constraint for the mobile artificial intelligence market. Advanced AI models require substantial processing capability, memory bandwidth, and real-time computation, which can strain compact mobile hardware. Despite ongoing improvements in chipsets, executing complex AI workloads on-device can impact performance stability and limit the execution of high-intensity applications such as computer vision and real-time analytics. This creates a need for lightweight and optimized AI models, which may reduce overall functionality and accuracy compared to full-scale systems.

Battery consumption and thermal management limitations further restrict the deployment of advanced mobile AI solutions. Continuous AI processing can lead to rapid power drain, reducing device uptime and user convenience, particularly in smartphones and wearables. At the same time, limited cooling capacity in slim device designs increases the risk of overheating, resulting in performance throttling to protect hardware. These constraints, along with memory and storage limitations in lower-end devices, restrict widespread adoption of advanced AI capabilities across all mobile device categories.

The expansion of edge AI and on-device processing presents a significant opportunity for the mobile artificial intelligence market. Increasing shift toward decentralized computing enables smartphones and mobile devices to process data locally, reducing latency and improving real-time responsiveness. This approach also enhances user privacy, as sensitive data does not need to be transmitted to cloud servers for processing. Growing availability of AI-optimized chipsets and efficient neural processing units is supporting broader deployment of advanced AI capabilities across mobile devices.

Rising demand for generative AI, intelligent assistants, and context-aware applications is further creating new growth avenues. Mobile AI is increasingly being integrated into applications such as healthcare monitoring, financial services, gaming, and augmented reality experiences. As AI models become more efficient and adaptable to low-power environments, adoption across mid-range and budget smartphones is expected to increase, expanding the addressable market significantly.

Market Concentration & Characteristics

The mobile artificial intelligence market exhibits a towards concentrated structure, primarily driven by strong control over core enabling technologies. The hardware layer remains the most concentrated part of the ecosystem due to high barriers related to chip design complexity, advanced processing unit integration, and manufacturing constraints. A limited number of global Technology Node providers control the majority of AI compute capability embedded in smartphones. This concentration is further reinforced by vertical integration across hardware, operating systems, and AI processing frameworks in premium device ecosystems. High R&D requirements, specialized semiconductor expertise, and dependence on advanced fabrication ecosystems restrict new entrants.

At the ecosystem and application layers, the market shows moderate fragmentation while still retaining an overall concentrated structure. Platform-level AI frameworks embedded in major mobile operating systems create centralized distribution of AI capabilities across devices, limiting full fragmentation. However, differentiation at the device manufacturer level and application layer introduces variability in features, user experience, and deployment intensity. Lower and mid-tier device categories, along with region-specific implementations, contribute to a broader spread of solution providers. Despite this dispersion, dependence on core AI hardware and platform ecosystems ensures that control remains indirectly concentrated.

Analyst Perspective

The Mobile Artificial Intelligence market is experiencing strong growth driven by increasing integration of AI capabilities into smartphones, tablets, wearables, and other connected devices. Advancements in AI-enabled processors, neural processing units (NPUs), and on-device machine learning are improving user experiences through features such as voice assistants, image recognition, predictive analytics, and real-time language processing. Growing demand for personalized services, enhanced security, and edge computing capabilities is encouraging technology providers and device manufacturers to expand their AI offerings.

Technology Node Insights

Based on technology node, the 7 nm segment led the market with the largest revenue share of 43.4% in 2025. This can be attributed to the technology’s optimal balance between performance, power efficiency, and cost-effectiveness. Semiconductor manufacturers have refined 10 nm fabrication processes, enabling the production of AI chips that deliver substantial computational power while maintaining manageable thermal output and battery consumption. This makes 10 nm chips highly suitable for a wide range of mobile devices, including smartphones and tablets, which require efficient on-device AI processing for applications such as voice recognition, image processing, and real-time data analytics. The maturity of this node size also ensures higher yields and lower production costs, encouraging widespread adoption by device manufacturers.

The 7 nm segment is predicted to experience the fastest CAGR during the forecast period, due to the increasing demand for enhanced AI capabilities in mobile devices. This technology node supports higher transistor density, which translates into greater processing power and improved energy efficiency, two important factors for AI workloads on mobile platforms. The transition toward 7 nm chips aligns with the evolving requirements of next-generation smartphones, AR/VR devices, and edge computing applications, where real-time AI inference and low latency are essential. Additionally, the adoption of 7 nm technology enables manufacturers to integrate more sophisticated neural processing units (NPUs) and AI 7 nm, facilitating advanced functionalities such as natural language processing, augmented reality enhancements, and intelligent camera systems.

Application Insights

Based on application, the smartphones segment led the market with the largest revenue share of 35.7% in 2025. This dominance is driven by the ubiquity of smartphones as primary computing devices and their increasing reliance on AI to enhance user experiences. AI integration in smartphones supports various functionalities, including voice assistants, facial recognition, computational photography, and personalized content delivery. The constant evolution of AI chipsets tailored for mobile platforms enables manufacturers to embed powerful AI capabilities without compromising battery life or device form factor. Moreover, the global proliferation of smartphones, particularly in emerging markets, sustains strong demand for AI-enabled devices.

The AR/VR segment is anticipated to grow at the fastest CAGR during the forecast period, reflecting the rising interest in immersive technologies across various sectors. AI plays a pivotal role in AR/VR devices by enabling real-time environment mapping, object recognition, gesture tracking, and adaptive content rendering. These capabilities are essential for delivering seamless and interactive user experiences in gaming, education, healthcare, and enterprise applications. The ongoing advancements in AI algorithms and hardware, 7 nm optimized for AR/VR, contribute to enhanced device performance and reduced latency. Additionally, increasing investments from technology companies and startups in AR/VR innovation, coupled with expanding consumer adoption, support the rapid growth trajectory of this segment.

Regional Insights

North America mobile artificial intelligence (AI) industry held a revenue share of over 28% in 2024. This can be attributed to the region’s well-established technology ecosystem, presence of major semiconductor and software companies, and substantial investments in AI research and development. The United States, in particular, benefits from a robust innovation infrastructure, including world-class universities, government funding programs, and a vibrant startup culture focused on AI advancements. Additionally, high consumer awareness and early adoption of AI-powered mobile devices contribute to strong market demand.

U.S. Mobile Artificial Intelligence (AI) Market Trends

The U.S. mobile artificial intelligence (AI) industry is expected to grow significantly in 2024, driven by extensive investments in AI chip design, expansion of data center capacity, and widespread AI adoption across finance, defense, and healthcare industries. Leading technology firms focus on developing energy-efficient 10 nm and 7 nm chips tailored to AI workloads, enhancing performance and reducing operational costs. Federal funding programs and strategic collaborations between academia and industry foster innovation and accelerate deployment.

Europe Mobile Artificial Intelligence (AI) Market Trends

The mobile artificial intelligence (AI) industry in Europe is expected to grow significantly over the forecast period, supported by a combination of regulatory emphasis on data privacy, investments in AI startups, and growing adoption of AI-enabled mobile technologies. The European Union’s focus on ethical AI development and stringent data protection regulations drives innovation that balances technological advancement with user trust. Key industries such as automotive, telecommunications, and healthcare are integrating mobile AI solutions to enhance connectivity, safety, and service delivery.

Asia Pacific Mobile Artificial Intelligence (AI) Market Trends

Asia Pacific dominated the mobile artificial intelligence market with the largest revenue share of 37.6% in 2025, driven by rapid smartphone adoption, expanding digital infrastructure, and supportive government policies. Countries like China, India, Japan, and South Korea lead in both manufacturing and consumption of AI-enabled mobile devices.

China Mobile Artificial Intelligence Market Trends

The mobile artificial intelligence market in the China held the largest share in the Asia Pacific region in 2025. The region’s large and tech-savvy population drives demand for AI-powered applications such as voice assistants, mobile payments, and personalized content. Additionally, government initiatives promoting AI innovation, smart cities, and digital transformation create a conducive environment for market expansion.

Key Mobile Artificial Intelligence Company Insights

Some key companies in the mobile artificial intelligence (AI) industry are IBM Corporation, Intel Corporation, NVIDIA Corporation, and Microsoft.

-

NVIDIA Corporation develops advanced GPUs and AI solutions to accelerate machine learning, deep learning, and data analytics workloads. Its technology node portfolio includes architectures such as the Blackwell series, which focus on improving computational efficiency and energy performance for AI training and inference. NVIDIA supports a comprehensive ecosystem that combines hardware, software frameworks, and collaborations with cloud providers and enterprises to facilitate AI deployment across sectors, including healthcare, finance, and autonomous systems.

-

Intel Corporation offers diverse AI solutions, including CPUs, GPUs, and specialized AI accelerators tailored for various workloads from edge devices to large-scale data centers. Recent technology nodes such as the Intel Arc Pro GPUs and Gaudi 3 AI accelerators emphasize energy efficiency and scalability for AI inference and training tasks. Intel integrates hardware development with open software platforms and ecosystem partnerships, enabling efficient AI application deployment. The company focuses on advancing AI-optimized processors and new architectures that support applications across cloud services, professional computing, and edge environments.

Key Mobile Artificial Intelligence Companies

The following key companies have been profiled for this study on the mobile artificial intelligence market.

-

Qualcomm Inc

-

Nvidia Corporation

-

Intel Corporation

-

IBM Corporation

-

Microsoft

-

Apple Inc

-

Huawei (Hisilicon)

-

Google LLC

-

Mediatek

-

Samsung

-

Cerebras Systems

-

Graphcore

-

Cambricon Technology

-

Shanghai Thinkforce Electronic Technology Co., Ltd (Thinkforce)

-

Deephi Tech

-

Sambanova Systems

-

Rockchip (Fuzhou Rockchip Electronics Co., Ltd.)

-

Thinci

-

Kneron

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Qualcomm Inc., Nvidia Corporation, Intel Corporation, IBM Corporation

- Focus on bundled services, large-scale infrastructure, and long-term content contracts to retain subscribers and maintain market share.

- Strong brand presence, large subscriber base, and extensive bundled service ecosystems supported by premium content rights and advanced infrastructure.

- High operating costs, slower adaptability to changing consumer preferences, and dependency on traditional subscription models.

Emerging Players: Cerebras Systems, Graphcore, Cambricon Technology, Shanghai Thinkforce Electronic Technology Co., Ltd. (Thinkforce)

- Focus on cost-efficient models, flexible pricing, and targeted expansion to grow subscriber base and improve competitiveness.

- Lower pricing, flexible service offerings, and agility in adopting digital-first and niche content strategies to attract targeted customer groups.

- Limited scale, weaker content portfolios, and lower bargaining power with content providers and infrastructure partners.

Recent Developments

-

In May 2025, Anthropic announced the rollout of a voice interaction mode for Claude, its widely used AI chatbot, to all mobile app users. Currently in beta, this new feature supports English voice input and is available across all subscription tiers, including the free plan. The introduction of voice mode aims to enhance user accessibility and engagement by enabling more natural, conversational interactions with the AI, reflecting ongoing advancements in conversational AI technologies.

-

In March 2025, Samsung articulated its strategic vision to deliver an integrated AI companion across the Galaxy ecosystem, emphasizing the launch of the Galaxy S25 series and the expansion of AI-driven functionalities to the new A series, as well as to health and smart home applications. The company showcased significant advancements in Galaxy AI and comprehensive software solutions designed to empower network operators, enabling them to fully leverage AI technologies for enhanced connectivity, user experience, and operational efficiency.

-

In February 2025, Mistral, a French startup recognized for its pioneering role in European AI development, launched Le Chat, an AI chatbot application available on both iOS and Android platforms. The app leverages advanced natural language processing technologies to provide users with interactive and intelligent conversational experiences. This release underscores Mistral’s commitment to expanding accessible AI tools and strengthening its position within the competitive AI landscape in Europe.

Mobile Artificial Intelligence Market Report Scope

Report Attribute

Details

Market size in 2025

USD 23.8 billion

Estimated market size in 2026

USD 29.7 billion

Projected market size by 2033

USD 206.9 billion

Growth rate

CAGR of 31.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Technology node, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; Australia; South Korea; Brazil; KSA; UAE; South Africa

Key companies profiled

Qualcomm Inc; Nvidia Corporation; Intel Corporation; IBM Corporation; Microsoft; Apple Inc; Huawei (Hisilicon); Google LLC; Mediatek; Samsung; Cerebras Systems; Graphcore; Cambricon Technology Node; Shanghai Thinkforce Electronic Technology Node Co., Ltd (Thinkforce); Deephi Tech; Sambanova Systems; Rockchip (Fuzhou Rockchip Electronics Co., Ltd.); Thinci; Kneron

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Mobile Artificial Intelligence Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global mobile Artificial Intelligence (AI) market report based on technology node, application, and region:

-

Technology Node Outlook (Revenue, USD Million, 2021 - 2033)

-

7 nm

-

10 nm

-

20-28 nm

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Smartphones

-

Cameras

-

Drones

-

Automobile

-

Robotics

-

AR/VR

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

UAE

-

KSA

-

South Africa

-

-

Research Methodology

The mobile artificial intelligence market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each mobile artificial intelligence segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Technology Node

Revenue capture definition

7 nm

Revenue generated from semiconductor devices manufactured using the 7 nm process node, offering high transistor density and power efficiency.

10 nm

Revenue derived from semiconductor products fabricated on the 10 nm technology node, supporting enhanced performance and reduced power consumption.

20-28 nm

Revenue generated from chips produced using 20 nm to 28 nm process technologies, widely utilized across consumer, industrial, and automotive applications.

Others

Revenue attributed to semiconductor devices manufactured on 12 nm and 14 nm process nodes, balancing performance, cost efficiency, and production scalability.

Segment - Application

Revenue capture definition

Commercial

Revenue generated from semiconductor solutions deployed across commercial facilities, enterprises, data centers, and business infrastructure applications.

Residential

Revenue derived from semiconductor products used in household electronics, smart home devices, and consumer-focused residential applications.

Estimation Model

Layer Name

Key Question

Description

Device & Installed Base Layer

Who creates demand for Mobile Artificial Intelligence solutions?

Identify the installed base of smartphones, tablets, wearables, and other connected mobile devices capable of supporting AI-enabled functionalities. This layer establishes the overall addressable market for mobile AI technologies.

AI-Enabled Device Adoption Layer

Which devices actively utilize Mobile Artificial Intelligence capabilities?

Filter the total device base based on AI-enabled processors, neural processing units (NPUs), operating system compatibility, and user adoption of AI-driven features. This layer represents the active deployment base for Mobile Artificial Intelligence.

Application & Service Utilization Layer

How are Mobile Artificial Intelligence capabilities used?

Estimate adoption across applications such as virtual assistants, image recognition, voice processing, predictive text, mobile commerce, personalized recommendations, security authentication, and augmented reality experiences.

Revenue Capture Layer

How is revenue generated within the Mobile Artificial Intelligence ecosystem?

Calculate revenue generated from AI-enabled smartphones and devices, AI chipsets, software platforms, cloud-based AI services, application subscriptions, licensing, and enterprise mobile AI solutions.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Objective

Custom Research Modules Delivered

Strategic Value / Business Impact

Market Entry & Expansion Assessment

Regional demand sizing and forecasting

Mobile AI adoption and penetration analysis

Competitive landscape benchmarking

Technology ecosystem assessment

Identified high-growth market opportunities

Supported go-to-market strategy development

Highlighted investment priorities and risks

Enabled data-driven expansion planning

Product Positioning & Competitive Intelligence

AI chipset and platform benchmarking

Feature and performance comparison

Product portfolio assessment

Competitor strategy evaluation

Improved product differentiation strategy

Identified technology gaps and opportunities

Enhanced competitive positioning

Supported product roadmap planning

Technology & Innovation Assessment

Emerging AI technology trend analysis

AI processor and NPU innovation tracking

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

The global mobile artificial intelligence market size was estimated at USD 23.8 billion in 2025 and is expected to reach USD 29.7 billion in 2026 in 2026.

The global mobile artificial intelligence market is expected to grow at a compound annual growth rate of 31.9% from 2026 to 2033 to reach USD 206.9 billion by 2033.

Asia Pacific dominated the mobile artificial intelligence (AI) market with a share of over 37.6% in 2025. This is attributable to the prevalence of large number of market players in the countries from the region.

Some key players operating in the mobile artificial intelligence market include Qualcomm, Nvidia, Intel, IBM, Microsoft, Apple, Huawei (Hisilicon), Alphabet (Google), Mediatek, Samsung, Shanghai Thinkforce Electronic Technology Co., Ltd (Thinkforce), Sambanova Systems, Rockchip (Fuzhou Rockchip Electronics Co., Ltd.)

Key factors that are driving the market growth include prominent innovation of AI in smartphones, increase in demand for AI-capable processors, and substantial investments in AI technology

The 7 nm segment accounted for the largest share at 43.4% in 2025, while the 10 nm segment is the fastest-growing.

The smartphones segment accounted for the largest share at 35.7% in 2025, while the AR/VR segment is the fastest-growing.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.