- Home

- »

- Communications Infrastructure

- »

-

Software Defined Data Center Market, Industry Report, 2033GVR Report cover

![Software Defined Data Center Market Size, Share, & Trends Report]()

Software Defined Data Center Market (2025 - 2033) Size, Share, & Trends Analysis By Component (Solution, Services), By Type, By Deployment, By Enterprise Size, By End Use, By Region, And Segment Forecasts

Market Size, 2024

$72.3BMarket Estimate, 2026

$88.0BMarket Forecast, 2033

$736.0BCAGR, 2025–2033

30.4%Software Defined Data Center Market Summary

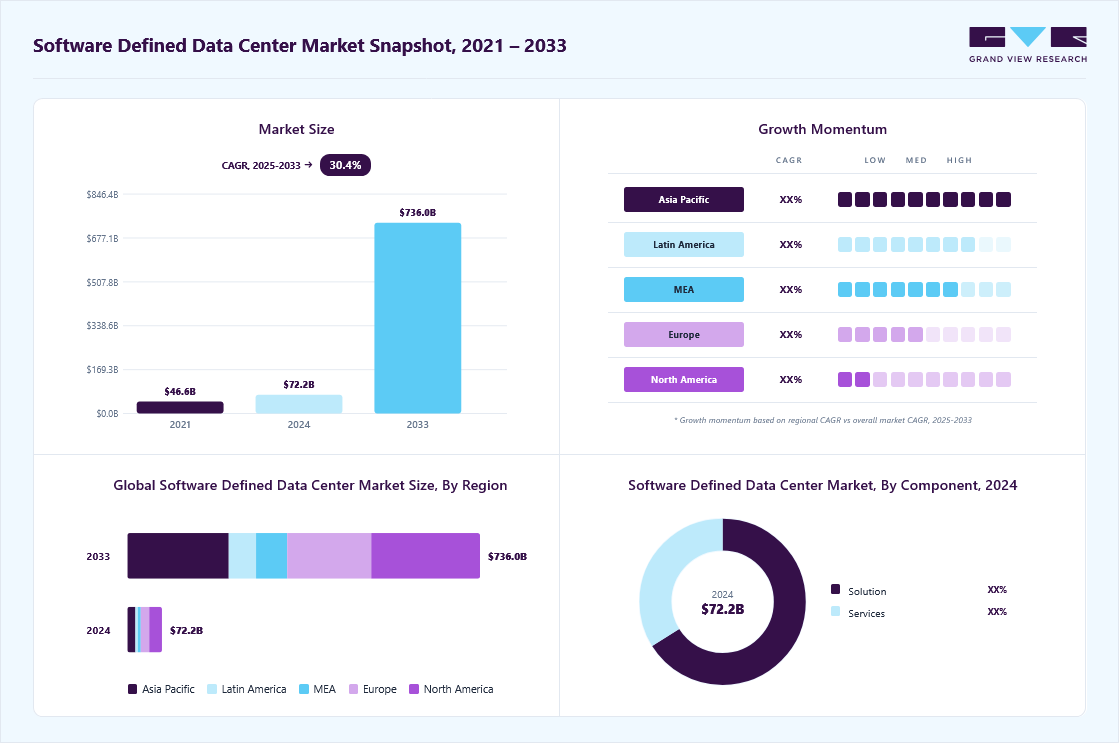

The global software defined data center market size was estimated at USD 72.29 billion in 2024 and is projected to reach USD 736.00 billion by 2033, growing at a CAGR of 30.4% from 2025 to 2033 due to increasing demand for scalable and agile IT infrastructure to support digital transformation initiatives.

Key Market Trends & Insights

- North America software defined data center dominated the global market with the largest revenue share of 40.2% in 2024.

- The software defined data center industry in the U.S. is expected to grow significantly over the forecast period.

- By component, solution led the market and held the largest revenue share of 66.0% in 2024.

- By type, the software-defined compute (SDC) segment held the dominant position in the market and accounted for the largest revenue share in 2024.

- By end use, the IT and telecom segment is expected to grow at the fastest CAGR from 2025 to 2033.

Market Size & Forecast

- 2024 Market Size: USD 72.29 Billion

- 2033 Projected Market Size: USD 736.00 Billion

- CAGR (2025-2033): 30.4%

- North America: Largest market in 2024

- Asia Pacific: Fastest-growing market

Enterprises across industries are shifting from traditional data centers to software-defined environments to improve automation, reduce hardware dependency, and increase resource utilization. With cloud computing, AI/ML workloads, and big data analytics requiring highly flexible and programmable infrastructure, software defined data center (SDDC) solutions are becoming vital. Moreover, organizations are adopting DevOps and continuous delivery models that rely on dynamic provisioning of compute, storage, and networking resources, capabilities that are native to SDDC frameworks. The rapid proliferation of edge computing and hybrid cloud strategies, which require a consistent and centralized approach to managing distributed IT environments, contributes to market growth. SDDCs offer seamless integration across public and private cloud platforms by abstracting hardware components and managing them via software-defined policies. This enables organizations to manage workloads across on-premises and cloud environments with better control, security, and visibility. Moreover, advancements in virtualization technologies and the adoption of containerized applications using Kubernetes and Docker further support the demand for SDDC architectures.")

Cybersecurity and compliance pressures are also propelling the SDDC market forward. Software-defined infrastructures offer enhanced automation and orchestration capabilities that improve disaster recovery, fault tolerance, and policy enforcement. This is crucial in regulated industries such as finance, healthcare, and government, where data integrity and access control are mission-critical. Gigamon’s 2025 Hybrid Cloud Security Survey reveals breach rates have jumped to 55%, up 17% year-over-year, as AI-generated attacks increasingly strain hybrid cloud environments. The study surveyed over 1,000 IT and security leaders across six countries.

In addition, the emergence of AI-driven monitoring tools within SDDC platforms allows for proactive infrastructure management, helping reduce downtime and operational costs. As organizations look to future-proof their IT ecosystems, SDDC's ability to deliver agility, automation, and operational efficiency will continue to fuel its adoption globally.

Component Insights

The solution segment dominated the market and accounted for the revenue share of 66.0% in 2024, driven by the rising need for agile, scalable, and cost-effective IT infrastructure to support modern digital transformation initiatives. Enterprises are increasingly adopting SDDC solutions to automate data center operations, enhance resource utilization, and reduce reliance on hardware-centric environments. The surge in hybrid cloud deployments, growing demand for unified management of computing, storage, and networking through software, and rising security concerns are further fueling adoption.

The service segment is anticipated to grow at the highest CAGR during the forecast period due to the increasing complexity of deploying and managing software-defined environments. This complexity drives demand for specialized consulting, integration, and support services. Organizations often lack the in-house expertise required to design and implement SDDC architectures efficiently, prompting them to rely on third-party service providers.

Type Insights

The software-defined compute (SDC) segment dominated the market and accounted for the largest revenue share in 2024, driven by the need for flexible and policy-driven allocation of computing resources across virtualized environments. As businesses scale workloads across on-premises and multi-cloud platforms, SDC enables seamless workload portability, dynamic provisioning, and improved performance efficiency. The increasing adoption of containerized applications, DevOps practices, and microservices architecture also propels demand for SDC to support rapid deployment and scalability.

The software-defined networking (SDN) segment is expected to grow significantly during the forecast period due to the growing need for intelligent, programmable, and agile network infrastructure that can adapt to dynamic workload requirements. As enterprises embrace distributed applications and real-time data processing, SDN facilitates granular traffic control, automated provisioning, and improved network visibility, enhancing overall efficiency and security. The rising frequency of cyber threats and east-west traffic within data centers is also encouraging the adoption of SDN for its centralized policy enforcement and micro-segmentation capabilities.

Deployment Insights

The public systems segment dominated the market and accounted for the largest revenue share in 2024, driven by the increasing preference of enterprises and SMEs for cost-effective, scalable, and on-demand infrastructure offered by public cloud providers. This model significantly reduces capital expenditure and eliminates the need to maintain physical data centers, making it attractive for businesses seeking faster time-to-market and global reach. The expansion of public cloud ecosystems with native SDDC offerings, coupled with improved regulatory compliance capabilities and high service availability, is further encouraging adoption.

The hybrid segment is expected to grow at a significant CAGR during the forecast period as organizations seek to balance control, performance, and flexibility by combining on-premises infrastructure with public cloud resources. This model supports data sovereignty, legacy system integration, and customized workload placement, which are critical for regulated industries and large enterprises. The rise of data-intensive and latency-sensitive applications also drives demand for hybrid environments that allow localized processing while leveraging cloud scalability.

Enterprise Size Insights

The large enterprise segment dominated the market and accounted for the largest revenue share in 2024, fueled by the need for centralized management of vast and complex IT infrastructures that span multiple locations and business units. These organizations prioritize digital transformation and operational efficiency, which SDDC enables through policy-driven automation, reduced manual intervention, and improved resource optimization. Large enterprises also benefit from the enhanced scalability and interoperability, which supports rapid expansion and integration of emerging technologies.

The SMEs segment is expected to grow at a significant CAGR during the forecast period due to the increasing availability of affordable, scalable, and easy-to-deploy SDDC solutions tailored for smaller IT environments. SMEs are embracing SDDC to overcome IT staff and budget limitations while enhancing agility, uptime, and application performance. Adopting cloud-native technologies and SaaS models enables SMEs to access enterprise-grade infrastructure capabilities without large capital investment.

End Use Insights

The IT and telecom segment dominated the market and accounted for the largest revenue share in 2024, driven by continuous demand for high-speed data processing, ultra-low latency, and scalable infrastructure to support services such as 5G, IoT, and cloud computing. Telecom operators leverage SDDC to virtualize network functions (NFV), streamline service delivery, and reduce operational complexity. In the IT industry, SDDC supports rapid innovation cycles and agile development environments by enabling programmable infrastructure and automated provisioning.

The healthcare segment is expected to grow at a significant CAGR over the forecast period as medical institutions increasingly adopt digital health records, telemedicine, and AI-driven diagnostics, all requiring secure, scalable, and high-performance IT infrastructure. SDDC enables healthcare providers to efficiently manage large volumes of sensitive patient data while ensuring regulatory compliance with standards such as HIPAA. The ability to quickly scale computing resources to support imaging, genomics, and real-time analytics is particularly valuable in clinical environments.

Regional Insights

North America dominated the global market with the largest revenue share of 40.2% in 2024, driven by the region’s early adoption of cloud-native architectures, the dominance of hyperscale data center providers, and the rapid integration of AI and analytics in enterprise infrastructure. The presence of leading technology vendors and aggressive investments in 5G and edge computing infrastructure have accelerated the shift toward software-defined environments.

U.S. Software Defined Data Center Market Trends

The software defined data center market in the U.S. is expected to grow significantly at a CAGR of 27.4% from 2025 to 2033, due to the growing demand for automation in IT operations (AIOps). Autonomous data center management is a key growth driver. Enterprises are increasingly leveraging AI and machine learning to optimize data center performance, reduce human intervention, and enable predictive maintenance capabilities that align directly with the principles of SDDC.

Europe Software Defined Data Center Market Trends

The software defined data center market in Europe is anticipated to register considerable growth from 2025 to 2033, as the drive toward green and energy-efficient data centers is significantly influencing the adoption of SDDC. Environmental sustainability policies under the EU Green Deal are pushing enterprises to consolidate resources, minimize hardware usage, and improve energy efficiency, benefits provided by software-defined infrastructure.

The UK software defined data center market is expected to grow rapidly in the coming years, owing to rising demand for digital resiliency in the financial services, insurance, and healthcare sectors. Moreover, the growing reliance on private 5G networks and edge computing in manufacturing and logistics is fueling the adoption of SDDC platforms that can orchestrate resources at the network edge.

The software defined data center market in Germany held a substantial market share in 2024 due to the strong adoption of Industry 4.0 standards and the country's emphasis on high-performance computing (HPC) in the automotive and engineering sectors. The need for ultra-reliable, secure, and software-driven infrastructure to manage real-time data across manufacturing floors encourages SDDC deployment.

Asia Pacific Software Defined Data Center Industry Trends

The software defined data center market in Asia Pacific is anticipated to grow at the highest CAGR of 33.4% during the forecast period due to rapid urbanization, rising internet penetration, and the boom in e-commerce and fintech ecosystems. Emerging economies such as India, Indonesia, and Vietnam are investing heavily in digital infrastructure to support their growing digital economies.

Japan software defined data center market is expected to grow rapidly in the coming years, driven by accelerated cloud migration strategies among traditional enterprises, particularly in the banking and manufacturing sectors. The push for automation in the face of a declining IT workforce and the need for business continuity during natural disasters is motivating companies to shift to programmable and resilient data center infrastructure.

The software defined data center market in Chinaheld a substantial market share in 2024, due to the government initiatives such as the New Infrastructure plan and heavy investments in AI, big data, and smart manufacturing, which are propelling the demand for next-generation data center solutions, including SDDC. The country’s growing domestic cloud market, dominated by players like Alibaba Cloud and Huawei Cloud, is integrating SDDC to offer agile, customizable infrastructure services to enterprises.

Key Software Defined Data Center Company Insights

Key players operating in the software defined data center industry are VMware, Inc., Microsoft, IBM Corporation, Hewlett-Packard Enterprise Development LP, and Dell Inc. The companies focus on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In May 2025, Hewlett-Packard Enterprise Development LP expanded its HPE Aruba Networking portfolio by launching the Aruba CX 10K distributed services switches. Featuring integrated AMD Pensando DPUs, the switches offload network and security tasks from CPUs, freeing up compute resources for intensive AI workloads. This enhancement aims to boost efficiency and scalability in modern data center environments.

-

In April 2025, through strategic collaboration, Dell Inc. launched its PowerFlex software-defined storage solution integrated with the Nutanix Cloud Platform (NCP) and Nutanix Cloud Infrastructure (NCI). The partnership between Dell and Nutanix was announced last year; the joint solution is now commercially available. Dell Inc. aims to support NCP and Nutanix’s native hypervisor, AHV, in a scalable, two-tiered architecture, bringing increased flexibility and performance to enterprise hybrid cloud deployments.

Key Software Defined Data Center Companies:

The following are the leading companies in the software defined data center market. These companies collectively hold the largest market share and dictate industry trends.

- Cisco Systems Inc.

- Citrix Systems, Inc.

- Dell Software Inc.

- Hewlett-Packard Enterprise Development LP

- IBM Corporation

- Microsoft

- NEC Corporation

- Oracle

- SAP SE

- VMware, Inc.

Software Defined Data Center Market Report Scope

Report Attribute

Details

Market size in 2025

USD 88.04 billion

Revenue forecast in 2033

USD 736.00 billion

Growth rate

CAGR of 30.4% from 2025 to 2033

Actual data

2021 - 2024

Forecast period

2025 - 2033

Report updated

July 2025

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, type, deployment, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Cisco Systems Inc.; Citrix Systems, Inc.; Dell Software Inc.; Hewlett-Packard Enterprise Development LP; IBM Corporation; Microsoft; NEC Corporation; Oracle; SAP SE; VMware, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Software Defined Data Center Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global software defined data center market report based on component, type, deployment, enterprise size, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solution

-

Services

-

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Software-Defined Compute (SDC)

-

Software-Defined Networking (SDN)

-

Software-Defined Storage (SDS)

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Public

-

Private

-

Hybrid

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

SMEs

-

Large Enterprises

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT and Telecom

-

Government

-

Healthcare

-

Manufacturing

-

Retail and E-commerce

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global software defined data center market size was estimated at USD 72.29 billion in 2024 and is expected to reach USD 88.04 billion in 2025.

The global software defined data center market is expected to grow at a compound annual growth rate of 30.4% from 2025 to 2033 to reach USD 736.00 billion by 2033.

The solution segment accounted for the largest market share of 66.0% in 2024. The growth of the solution segment includes the rising need for agile, scalable, and cost-effective IT infrastructure to support modern digital transformation initiatives. Enterprises are increasingly adopting SDDC solutions to automate data center operations, enhance resource utilization, and reduce reliance on hardware-centric environments.

Some key players operating in the software defined data center market include Cisco Systems Inc., Citrix Systems, Inc., Dell Inc., Hewlett Packard Enterprise Development LP, IBM Corporation, Microsoft, NEC Corporation, Oracle, SAP SE, VMware, Inc.

The Software Defined Data Center (SDDC) market is experiencing significant growth driven by the increasing demand for scalable and agile IT infrastructure to support digital transformation initiatives. Enterprises across industries are shifting from traditional data centers to software-defined environments to improve automation, reduce hardware dependency, and increase resource utilization.

About the Author(s)

Communications Infrastructure Research Team

Technology · Communications InfrastructureThis report was authored by the communications infrastructure research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the communications infrastructure segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.