- Home

- »

- Automotive & Transportation

- »

-

Stacker Crane Market Size, Share, Growth Report, 2026-2033GVR Report cover

![Stacker Crane Market (2026 - 2033)Report]()

Stacker Crane Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type, By Operation (Semi-automatic, Automatic), By End Use (Consumer Goods, Pharmaceutical, Automotive), By Region, And Segment Forecasts

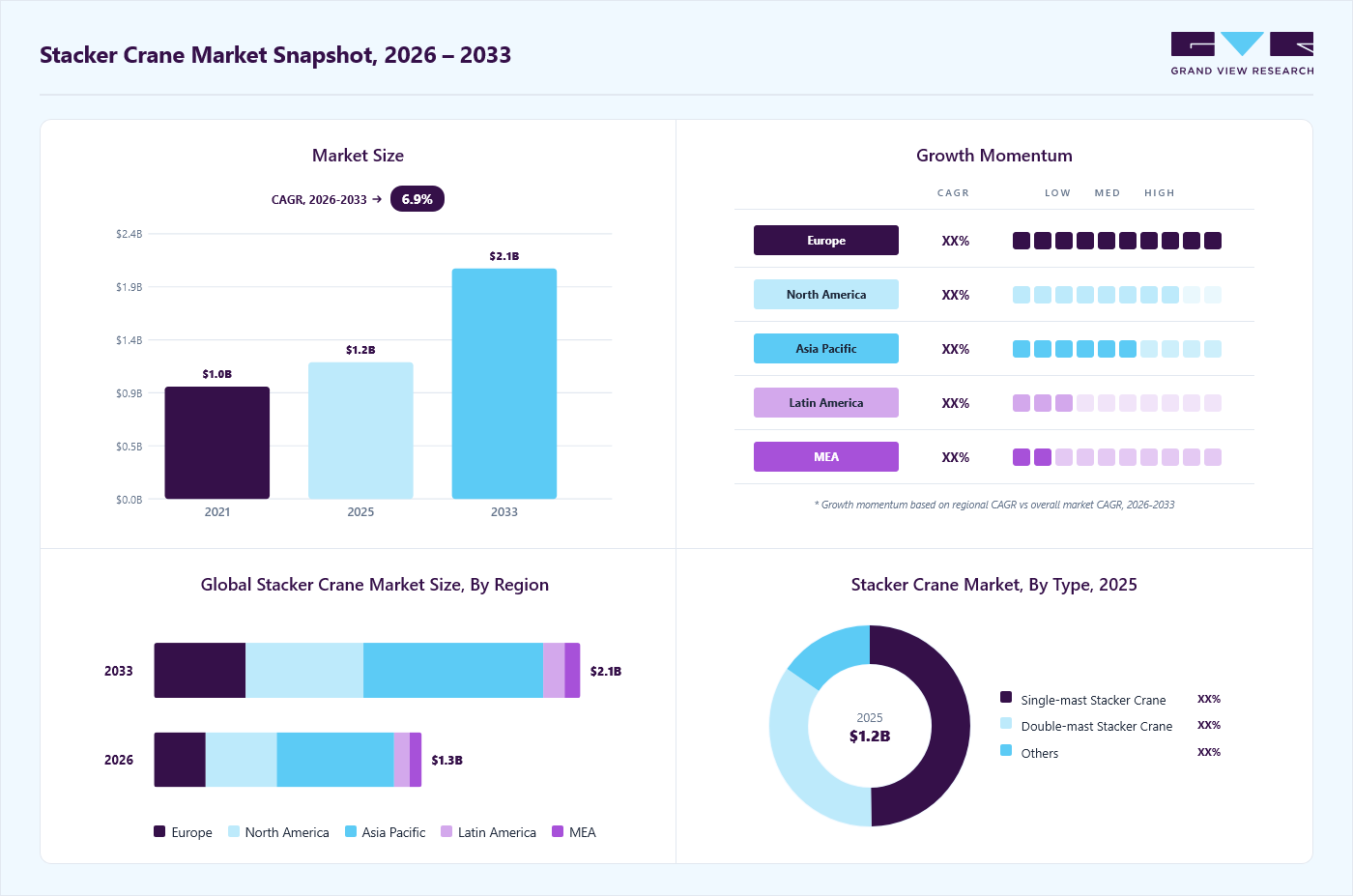

Market Size, 2025

$1.2BMarket Estimate, 2026

$1.3BMarket Forecast, 2033

$2.1BCAGR, 2026–2033

6.9%Stacker Crane Market Size & Trends

The global stacker crane market size was estimated at USD 1.2 billion in 2025 and is projected to grow from USD 1.3 billion in 2026 to USD 2.1 billion by 2033, at a CAGR of 6.9% from 2026 to 2033. Asia Pacific dominated the global market with the largest revenue share of 44.0% in 2025. The growing need for efficient storage and retrieval systems in warehouses and logistics operations is a major driving factor behind the growth of the market.

Key Market Trends & Insights

- By type: Single-mast stacker crane segment dominated the market, with a revenue share of 49.7% in 2025.

- By operations: Semi-automatic segment held the largest market share of 60.4% in 2025.

- By end use: Automotive segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (44.0% revenue share, 2025)

- Fastest-growing regional market: Europe (highest CAGR, 2026-2033)

- By country: The India is the fastest growing country in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.2 Billion

- Estimated market size in 2026: USD 1.3 Billion

- Projected market size by 2033: USD 2.1 Billion

- CAGR (2026-2033): 6.9%

Various industries are increasingly adopting automated solutions such as stacker cranes to optimize their supply chain, enhance productivity, and reduce labor costs. In addition, rapidly growing e-commerce and manufacturing industry across the globe and rising technological advancements in stacker cranes are further expected to boost the growth of the stacker crane market. As industries across the globe are increasingly adopting smart manufacturing practices, stacker cranes equipped with advanced sensors, Artificial Intelligence (AI), and Internet of Things (IoT) connectivity are becoming essential. These innovations enable real-time data collection and analysis, enhancing operational efficiency, reducing labor costs, and minimizing errors. Several companies are streamlining their supply chains and improving inventory management, making stacker cranes a critical investment for businesses looking to remain competitive in a rapidly evolving landscape. Thus, the rise of Industry 4.0 and automation is significantly contributing to the growth of the market.The rapid growth of the e-commerce sector is increasing the demand for efficient warehousing solutions, such as stacker cranes. Owing to the increasing consumer demand for faster delivery and enhanced service, warehouses are focusing on adopting stacker cranes to optimize their operations. Stacker cranes enable high-density storage and quick retrieval of products, making them vital in e-commerce fulfillment centers. As online shopping continues to expand, businesses are increasingly investing in automated storage solutions to meet the demands of their customers, thereby driving the growth of the stacker crane market.

")

Furthermore, innovations such as improved control systems, enhanced safety features, and integration with warehouse management systems are driving the adoption of stacker cranes. Advanced robotics and AI-driven algorithms optimize the performance and functionality of stacker cranes, allowing for more precise handling of goods. As technology evolves, stacker cranes are becoming more versatile and capable of adapting to the specific needs of various industries, driving widespread adoption across sectors. Thus, rising technological advancements in stacker cranes are expected to contribute to the growth of the market.

High capital investment and maintenance complexity could hamper the growth of the market.The significant initial investment needed for stacker crane installation remains a barrier to their adoption, especially for smaller businesses with budget limitations. In addition, the complexity of stacker cranes requires careful maintenance; even occasional breakdowns or malfunctions can disrupt operations, resulting in delays and higher operational costs. Furthermore, stacker cranes are vulnerable to single points of failure. When one crane breaks down, it can make the entire aisle's inventory inaccessible, disrupting order fulfillment and halting warehouse operations, thereby hindering the market’s growth.

Market Dynamics

Advancements in automation technologies, warehouse management systems (WMS), artificial intelligence, machine vision, IoT connectivity, and autonomous control systems are significantly enhancing the efficiency, accuracy, speed, and operational reliability of stacker cranes across warehousing, e-commerce, automotive, food & beverage, and manufacturing industries. The integration of real-time monitoring, predictive maintenance, and data analytics platforms further improves inventory management, space utilization, throughput, and overall warehouse productivity. However, high initial capital investment, complex installation requirements, infrastructure modification costs, and the need for skilled workforce and system integration expertise increase deployment expenses and pose challenges for small and medium-sized enterprises. Meanwhile, the rapid growth of e-commerce, increasing adoption of automated storage and retrieval systems (AS/RS), rising labor costs, expanding cold chain logistics infrastructure, and ongoing Industry 4.0 initiatives are creating opportunities for manufacturers to develop intelligent, energy-efficient, high-speed, and scalable stacker crane solutions tailored to modern automated warehouse environments.

The increasing adoption of automated storage and retrieval systems and smart warehouse technologies is significantly driving demand for advanced stacker cranes across logistics, e-commerce, manufacturing, automotive, food & beverage, and cold chain industries. Modern stacker cranes equipped with intelligent control systems, machine vision, IoT connectivity, and automated navigation capabilities enable faster material movement, higher storage density, improved inventory accuracy, and reduced labor dependency. These next-generation solutions offer enhanced operational efficiency, high-speed handling, and reliable performance, making them essential components of modern automated warehouses and distribution centers.

The market is also witnessing growing integration of artificial intelligence, predictive analytics, and digital warehouse management platforms. AI-enabled monitoring systems facilitate real-time equipment tracking, predictive maintenance, route optimization, and performance analytics, helping warehouse operators minimize downtime, improve throughput, and reduce operating costs. Additionally, the adoption of cloud-based warehouse management systems (WMS) and industrial IoT technologies is enabling seamless communication between stacker cranes, conveyors, robotics, and inventory management platforms.

The deployment of stacker crane systems requires substantial capital investment in automated storage and retrieval systems, warehouse infrastructure, software platforms, control systems, and supporting material handling equipment. The high upfront costs associated with procurement, installation, customization, and commissioning often limit adoption among small and medium-sized enterprises (SMEs), particularly in cost-sensitive industries and developing markets. Additionally, warehouse operators must invest in facility modifications, specialized racking systems, and advanced warehouse management software, further increasing total ownership costs.

The market also faces challenges related to complex system integration and implementation processes. Stacker cranes must operate seamlessly with warehouse management systems, warehouse control systems (WCS), conveyors, robotics, sensors, and enterprise resource planning (ERP) platforms. Ensuring compatibility across multiple technologies and vendors often requires extensive engineering expertise, prolonged deployment timelines, and additional integration expenses. Any operational disruption during implementation can affect warehouse productivity and inventory management efficiency.

The rapid growth of e-commerce, omnichannel retailing, and global distribution networks is creating significant opportunities for stacker crane manufacturers worldwide. Increasing order volumes, rising consumer expectations for faster deliveries, and the need for efficient inventory management are driving investments in automated warehouses and distribution centers. Stacker cranes play a critical role in maximizing storage capacity, improving order-picking efficiency, and enabling high-throughput operations, making them an essential component of next-generation logistics infrastructure.

The market is also benefiting from the expansion of cold chain logistics and temperature-controlled storage facilities across food & beverage, pharmaceuticals, healthcare, and biotechnology sectors. As demand for refrigerated and frozen storage increases, warehouse operators are increasingly adopting automated storage and retrieval systems equipped with stacker cranes to enhance operational efficiency, reduce labor exposure in extreme environments, and ensure accurate inventory handling. This trend is generating substantial opportunities for manufacturers to develop specialized stacker crane solutions designed for cold storage and high-bay warehouse applications.

Analyst Perspective

The growing adoption of warehouse automation, automated storage and retrieval systems, e-commerce fulfillment infrastructure, and smart logistics solutions is driving strong growth in the stacker crane market. Industries are increasingly deploying stacker cranes to enhance storage density, improve inventory accuracy, optimize material flow, and reduce labor dependency across warehouses and distribution centers. Advances in automation technologies, artificial intelligence, machine vision, IoT connectivity, and warehouse management systems are improving operational efficiency, throughput, reliability, and energy performance across a wide range of material handling applications. Ongoing innovation in autonomous material handling, predictive maintenance, digital twin technology, and intelligent warehouse orchestration platforms is expanding the adoption of stacker cranes across e-commerce, retail, automotive, pharmaceutical, manufacturing, and cold chain logistics sectors. However, high initial capital investment, complex system integration requirements, lengthy implementation timelines, and the need for specialized technical expertise remain significant challenges, particularly for small and medium-sized enterprises. The market is expected to grow steadily as organizations continue to invest in warehouse modernization, supply chain digitalization, Industry 4.0 initiatives, and highly automated storage and distribution infrastructure to improve operational efficiency and meet evolving customer fulfillment requirements.

Type Insights

Based on type, the single-mast stacker crane segment led the market with the largest revenue share of 49.7% in 2025. Single mast stacker cranes are gaining traction due to their cost-effectiveness and versatility in various applications. These cranes are typically lighter and less expensive than their double mast counterparts, making them an attractive option for small to medium-sized businesses with limited budgets. Their compact design allows for easy maneuverability in narrower aisles, optimizing space utilization in warehouses. In addition, their ability to handle a range of goods, from pallets to smaller items, makes them suitable for diverse industries, driving their growth in the market.

The double-mast stacker crane segment is projected to witness significant growth from 2026 to 2033. The growth of the double-mast stacker crane segment can be attributed to their enhanced lifting capacity and stability. These cranes can handle heavier loads and reach greater heights compared to single mast models, which is particularly beneficial for warehouses with tall racking systems. In addition, double-mast stacker cranes can seamlessly integrate with warehouse management systems, allowing for real-time inventory tracking and improved data management. This integration enhances operational visibility and supports better decision-making regarding inventory control, thereby driving the segment’s growth.

Operation Insights

Based on operation, the semi-automatic segment led the market with the largest revenue share of 60.4% in 2025. Semi-automatic stacker cranes are increasingly gaining traction as they effectively balance the benefits of manual operation with the efficiencies of full automation. These cranes offer operators greater control while helping with lifting and moving tasks, making them suitable for warehouses that require a mix of human oversight and machine efficiency. This hybrid approach allows businesses to optimize labor resources without significant upfront investment in fully automated systems. Thus, the increasing adoption of semi-automatic stacker cranes by industries that handle varied inventory types and volumes to enhance productivity and reduce operational costs is boosting the segment’s growth.

The automatic segment is projected to witness significant growth from 2026 to 2033. Automatic stacker cranes are experiencing significant growth due to their ability to streamline operations and reduce labor costs. Fully automated systems integrate advanced technologies such as AI, sensors, and real-time data analytics, allowing for efficient, error-free handling of goods. These cranes can operate continuously without human intervention, making them ideal for high-throughput environments, such as e-commerce fulfillment centers and large-scale warehouses. In addition, their capability to minimize operational downtime and enhance safety through reduced human involvement makes them a key investment for companies looking to stay competitive in a rapidly evolving market, thereby driving segment growth.

End Use Insights

Based on end use, the consumer goods segment led the market with the largest revenue share of 34.9% in 2025. The increasing demand for efficient warehousing and distribution systems in the consumer goods sector is the major driving factor behind the segment’s growth. Several consumer goods companies are investing in automated storage solutions to handle the high volume of goods and meet consumer expectations for rapid delivery. Stacker cranes facilitate high-density storage, allowing businesses to maximize their warehouse space and streamline order fulfillment processes. Furthermore, the versatility of stacker cranes makes them suitable for a wide range of products, from packaged goods to bulk items, further enhancing their appeal in this dynamic industry, thereby boosting the segment’s growth.

The automotive vehicles segment is projected to witness significant growth from 2026 to 2033. The need for efficient material handling in automotive manufacturing and assembly processes can be attributed to the segment’s growth. Automotive manufacturers are increasingly adopting automated solutions to optimize their supply chains and improve production efficiency. Stacker cranes play a crucial role in managing heavy components and parts, ensuring that they are stored and retrieved with precision. The automotive sector is shifting towards more complex production methods, such as just-in-time manufacturing and greater customization. This drives the demand for advanced stacker crane systems that can manage diverse load types and sizes.

Regional Insights

Asia Pacific dominated the global stacker crane market with the largest revenue share of 44.0% in 2025. India is the fastest growing country in the Aisa Pacific stacker crane market. The growth of the market is driven by the region's expanding manufacturing and logistics sectors. As countries such as China and India continue to industrialize, the demand for efficient material handling solutions is increasing. In addition, the rise of e-commerce in the region is also encouraging companies to invest in automated storage systems to enhance order fulfillment capabilities. Furthermore, government initiatives aimed at modernizing infrastructure and promoting automation are contributing to the growth of stacker cranes.

North America Stacker Crane Market Trends

The North America stacker crane market is expected to witness notable growth from 2026 to 2033. The strong presence of advanced logistics and warehousing infrastructure across the region can be attributed to the growth of the market. In addition, the presence of major e-commerce and retail companies and the rapid growth of the automotive industry further fuel the adoption of stacker cranes in the region.

U.S. Stacker Crane Market Trends

The U.S. stacker crane market is expected to grow at a significant CAGR from 2026 to 2033. There is a growing trend towards automation in warehouses, with stacker cranes playing a crucial role in enhancing operational efficiency. These systems enable faster storage and retrieval processes, reduce labor costs, and improve inventory management accuracy. In addition, technological advancements in stacker cranes, such as integration with warehouse management systems and improved navigational capabilities are further propelling the market's growth in the country.

Europe Stacker Crane Market Trends

The Europe stacker crane market is expected to grow at the highest CAGR from 2026 to 2033. Increasing investments in smart manufacturing and automation technologies are driving demand for stacker cranes across the region. Furthermore, the growing trend of e-commerce and increased focus on logistics optimization are further supporting the adoption of stacker cranes across various sectors.

Key Stacker Crane Company Insights

The market players are focusing on numerous strategic initiatives, such as new product development, agreements, and partnerships & collaborations to acquire a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In December 2022, PSA Antwerp (PSAA), a Belgian terminal operator entered into an agreement with Austrian crane manufacturer Kuenz and global technology leader ABB Ltd., specializing in electrification and automation, to acquire 14 automated stacking cranes for its Europa Terminal. These advanced cranes would enable PSAA to increase the terminal's capacity by 40% while significantly advancing its sustainability goals by cutting total carbon emissions per handled container by over 50%.

-

In October 2020, Stoecklin Logistics, a provider of innovative supply chain solutions, launched a line of dynamic MASTer Stacker Cranes. These cranes are designed with moving speeds and high acceleration, enhanced energy efficiency, and modular construction that significantly boosts performance and availability. The models feature greater standardization across various cranes and load capacities, simpler and quicker wheels and hoists, shorter assembly and manufacturing times, lighter construction, and improved access to components for easier maintenance.

Key Stacker Crane Companies:

The following key companies have been profiled for this study on the stacker crane market.

-

Mecalu, S.A.

-

American Crane & Equipment Corporation

-

ME-JAN d.o.o.

-

Daifuku Co. Ltd.

-

Jungheinrich AG

-

Mitsubishi Logisnext Americas Inc.

-

Demag Cranes & Components GmbH

-

Kardex

-

Alstef Group

-

ATS Group

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Daifuku Co. Ltd., Jungheinrich AG, Kardex, Mitsubishi Logisnext Americas Inc.)

- Focus on developing high-performance automated storage and retrieval systems, intelligent stacker cranes, warehouse automation software, and integrated material handling solutions.

- Continuous investment in automation technologies, AI-enabled warehouse management systems, robotics integration, digital twins, and Industry 4.0 capabilities.

- Strong global presence, extensive project execution capabilities, comprehensive product portfolios, and long-standing relationships with logistics providers, manufacturers, and e-commerce companies.

- Proven expertise in delivering turnkey warehouse automation solutions, advanced engineering capabilities, and strong after-sales support infrastructure.

- High operational and development costs associated with large-scale automation projects.

- Longer sales cycles due to complex project approvals, customization requirements, and capital-intensive customer investments.

Emerging Players (American Crane & Equipment Corporation, ME-JAN d.o.o., Alstef Group, ATS Group)

- Focus on specialized stacker crane solutions, modular automation systems, warehouse modernization projects, and industry-specific applications.

- Emphasis on flexible system configurations, customized engineering, and cost-effective automation solutions for mid-sized facilities.

- Greater agility in responding to customer-specific requirements and evolving warehouse automation trends.

- Faster implementation timelines, flexible customization options, and competitive pricing strategies.

- Limited global presence, smaller project execution capabilities, and lower financial resources compared to industry leaders.

- Narrower product portfolios and reduced ability to provide end-to-end warehouse automation solutions.

Stacker Crane Market Report Scope

Report Attribute

Details

Market size in 2025

USD 1.2 billion

Estimated market size in 2026

USD 1.3 billion

Projected market size by 2033

USD 2.1 billion

Growth rate

CAGR of 6.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, operation, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; U.K.; Germany; France; Italy China; Japan; India; Australia; South Korea; Australia; Brazil; Kingdom of Kingdom of Saudi Arabia (KSA); UAE; South Africa

Key companies profiled

Mecalu, S.A., American Crane & Equipment Corporation, ME-JAN d.o.o., Daifuku Co. Ltd., Jungheinrich AG, Mitsubishi Logisnext Americas Inc., Demag Cranes & Components GmbH, Kardex

Alstef Group, ATS Group

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Stacker Crane Market Report Segmentation

The report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global stacker crane market based on type, operation, end use, and region.

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Single-mast Stacker Crane

-

Double-mast Stacker Crane

-

Others

-

-

Operation Outlook (Revenue, USD Million, 2021 - 2033)

-

Semi-automatic

-

Automatic

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer Goods

-

E-commerce/Retail and Wholesale

-

Pharmaceutical

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Kingdom of Saudi Arabia

-

South Africa

-

-

Research Methodology

The stacker crane market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each stacker crane segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Type

Revenue Capture Definition

Single-mast Stacker Crane

This segment captures revenue generated from single-mast stacker cranes designed for light- to medium-duty automated storage and retrieval operations. These systems are widely used in warehouses, distribution centers, retail logistics facilities, and manufacturing plants where moderate load capacities, high maneuverability, and cost-effective automation solutions are required.

Double-mast Stacker Crane

This segment includes revenue derived from double-mast stacker cranes engineered for heavy-duty material handling and high-load storage applications. These cranes are commonly deployed in high-bay warehouses, automotive facilities, cold storage warehouses, and industrial manufacturing environments where enhanced stability, higher lifting capacities, and greater operational reliability are essential.

Others

This segment captures revenue generated from specialized stacker crane configurations, including multi-mast, mini-load, shuttle-integrated, custom-engineered, and application-specific stacker crane systems designed to address unique storage, retrieval, and material handling requirements across various industries.

Segment- Operation

Revenue Capture Definition

Semi-Automatic

This segment captures revenue generated from semi-automatic stacker cranes that combine automated movement and positioning functions with manual operator intervention for certain tasks. These systems are widely utilized in warehouses and industrial facilities seeking improved efficiency while maintaining operational flexibility and lower automation investment costs.

Automatic

This segment includes revenue derived from fully automated stacker cranes capable of performing storage, retrieval, transportation, and inventory handling operations with minimal human intervention. These systems are increasingly adopted in advanced warehouses, distribution centers, e-commerce fulfillment facilities, and smart factories to enhance productivity, accuracy, throughput, and operational efficiency.

Segment- End use

Revenue Capture Definition

Consumer Goods

This segment captures revenue generated from stacker cranes deployed in consumer goods manufacturing and warehousing facilities for automated storage, inventory management, order fulfillment, and material handling operations. These systems help improve warehouse efficiency, optimize storage capacity, and streamline supply chain operations.

E-commerce/Retail and Wholesale

This segment includes revenue derived from stacker cranes utilized in e-commerce fulfillment centers, retail distribution hubs, and wholesale warehouses. These systems support high-volume order processing, rapid inventory movement, automated picking operations, and efficient storage management to meet increasing customer demand and delivery expectations.

Pharmaceutical

This segment captures revenue generated from stacker cranes used in pharmaceutical manufacturing plants, medical supply warehouses, and temperature-controlled storage facilities. These solutions facilitate accurate inventory tracking, regulatory compliance, product traceability, and efficient handling of sensitive pharmaceutical products and healthcare supplies.

Automotive

This segment includes revenue derived from stacker cranes deployed in automotive manufacturing facilities, spare parts warehouses, and component distribution centers. These systems support automated storage and retrieval of vehicle components, raw materials, finished goods, and spare parts while improving production logistics and warehouse productivity.

Others

This segment captures revenue generated from stacker crane applications across food & beverage, logistics, cold chain storage, chemicals, electronics, aerospace, industrial manufacturing, and other sectors requiring automated material handling and high-density storage solutions.

Estimation Model

Layer Name

Key Question

Description

Installed Warehouse & Storage Infrastructure Layer

Where are stacker cranes used and what drives demand?

Establish the total potential demand base by identifying stacker crane deployment across automated warehouses, distribution centers, e-commerce fulfillment centers, manufacturing facilities, cold storage warehouses, pharmaceutical storage facilities, automotive plants, and other high-density storage environments requiring automated material handling solutions.

Addressable Automation Market Layer

Which facilities can realistically adopt stacker crane solutions?

Refine the total storage infrastructure base into the realistically serviceable market by considering factors such as warehouse size, automation readiness, storage density requirements, labor costs, capital investment capacity, facility layout compatibility, technological maturity, and regional adoption of automated storage and retrieval systems.

Stacker Crane Procurement Layer

Who is actively purchasing, expanding, or upgrading stacker crane systems?

Estimate annual demand generation by analyzing new warehouse construction, expansion of distribution centers, e-commerce fulfillment investments, industrial automation projects, warehouse modernization initiatives, replacement cycles of existing equipment, cold chain infrastructure development, and Industry 4.0 adoption across key end-use industries.

Revenue Layer

How is revenue generated from stacker crane sales?

Revenue is generated through the sale of stacker cranes across various types (single-mast, double-mast, and specialized systems), automation levels (semi-automatic and automatic), and end-use industries. Market revenue is calculated by considering unit shipments, system configurations, load capacity specifications, automation features, software and control system integration, installation and commissioning services, regional pricing variations, and value chain margins across manufacturers, system integrators, and solution providers.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Stacker Crane Market Assessment

Structured evaluation of market dynamics including key drivers, restraints, opportunities, and industry trends across the stacker crane value chain.

Assessment of technology evolution across automated storage and retrieval systems, warehouse automation, AI-enabled material handling, and IoT-integrated warehouse management solutions.

Clear visibility into market growth drivers and adoption barriers.

Strategic input for market entry, expansion planning, and investment decisions.

End-Use and Application Insights

Analysis of demand distribution across consumer goods, e-commerce/retail & wholesale, pharmaceutical, automotive, and other end-use sectors.

Evaluation of evolving industry requirements related to warehouse automation, inventory optimization, order fulfillment efficiency, cold chain logistics, and smart warehousing initiatives.

Identification of high-growth and high-value application segments.

Support for targeted product development and go-to-market strategies.

Technology and Competitive Landscape Review

Benchmarking of key stacker crane technologies including single-mast, double-mast, semi-automatic, and fully automatic systems.

Analysis of major players' innovation strategies, automation capabilities, product differentiation, software integration expertise, and regional market presence.

Competitive intelligence for technology positioning and portfolio optimization.

Guidance for R&D prioritization, partnership evaluation, and long-term growth planning.

Frequently Asked Questions About This Report

Some key players operating in the stacker crane market include Mecalux, S.A., American Crane & Equipment Corporation, ME-JAN d.o.o., Daifuku Co., Ltd., Jungheinrich AG, Mitsubishi Logisnext Americas Inc., Demag Cranes & Components GmbH, Kardex, Alstef Group, and ATS Group.

Key factors that are driving the market growth include the growing need for efficient storage and retrieval systems in warehouses and logistics operations and the rapidly growing e-commerce and manufacturing industry across the globe.

Double-mast Stacker Crane witnessed the high CAGR of 8.3% in the stacker crane market.

The semi-Automatic segment dominated the operation segment in the stacker crane market with a share of 60.4% in 2025.

The global stacker crane market size was estimated at USD 1.2 billion in 2025 and is expected to reach USD 1.3 billion in 2026.

The global stacker crane market is expected to grow at a compound annual growth rate of 6.9% from 2026 to 203 to reach USD 2.1 billion by 2033.

Asia Pacific dominated the stacker crane market with a share of 44.0% in 2025. The growth of the market is driven by the region's expanding manufacturing and logistics sectors.

The China country dominated the Asia Pacific stacker crane market with a share of 41.1% in 2025.

The U.S. witnessed accounted for high share of 67.7% in the North America stacker crane market in 2025.

About the Author(s)

Automotive & Transportation Research Team

Technology · Automotive & TransportationThis report was authored by the automotive & transportation research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the automotive & transportation segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.