- Home

- »

- Biotechnology

- »

-

RNA Analysis Market Size And Share Report, 2026-2033GVR Report cover

![RNA Report]()

RNA Analysis Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Kits & Reagents, Services, Instruments), By Technology (qPCR, Microarray, Sequencing), By Application, By End Use, By Region, And Segment Forecasts

Market Size, 2025

$9.2BMarket Estimate, 2026

$9.9BMarket Forecast, 2033

$23.6BCAGR, 2026–2033

13.3%RNA Analysis Market Summary

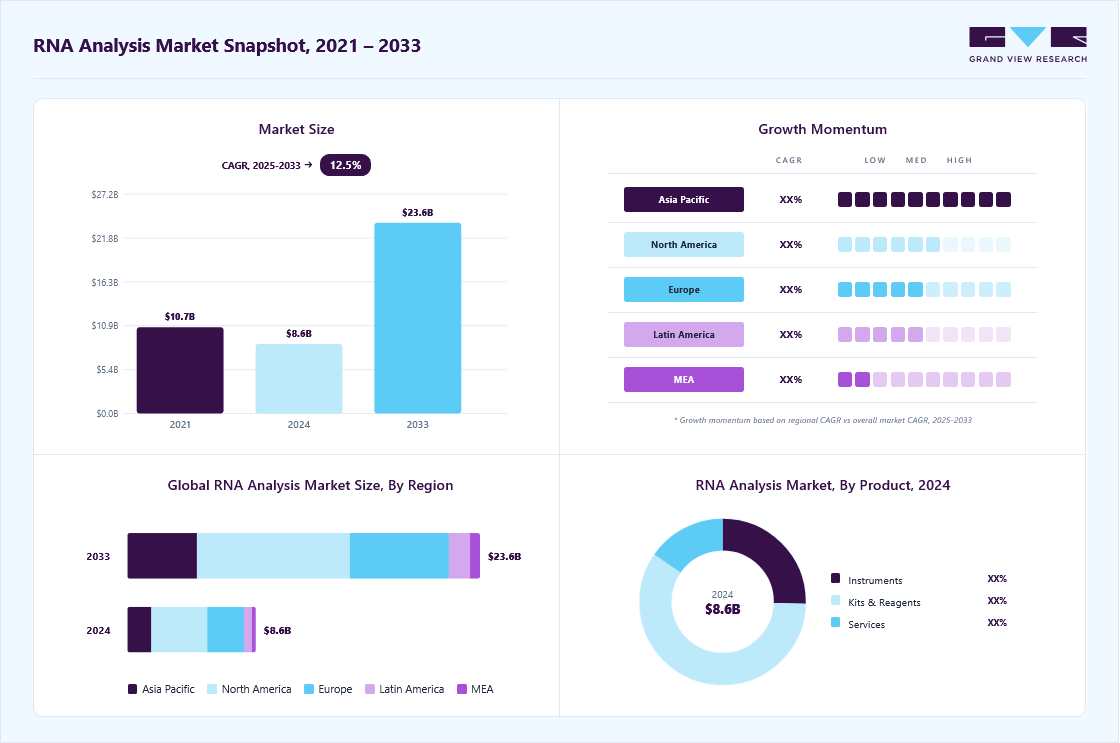

The global RNA analysis market size was valued at USD 9.2 billion in 2025 and is projected to grow from USD 9.9 billion in 2026 to USD 23.6 billion by 2033, at a CAGR of 13.3% from 2026 to 2033. The market in North America dominated with a revenue share of 43.6% in 2025. This growth is driven by the rising demand for transcriptomic studies in precision medicine, advancements in next-generation sequencing (NGS) technologies, and increasing applications of RNA biomarkers in disease diagnostics and drug discovery

Key Market Trends & Insights

- By product: Kits & reagents segment held the largest market share of 59.5% in 2025.

- By technology: Real time-PCR (qPCR) segment held the largest market share of 43.4% in 2025.

- By end use: Government institutes & academic centers segment held the largest market share of 32.0% in 2025.

- By application: Infectious diseases and pathogenesis segment held the largest market share of 18.1% in 2025.

Regional Highlights

- Largest regional market: North America (43.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 9.2 Billion

- Estimated market size in 2026: USD 9.9 Billion

- Projected market size by 2033: USD 23.6 Billion

- CAGR (2026-2033): 13.3%

")

Advances in sequencing technologiesRapid technological advancements in RNA sequencing have been a major catalyst for the growth of the RNA analysis market. Next-generation sequencing (NGS) platforms have revolutionized transcriptomics by enabling high-throughput, accurate, and cost-effective analysis of RNA molecules across multiple samples simultaneously. These technologies allow researchers to explore gene expression patterns in unprecedented detail, uncover novel RNA variants, and gain insights into complex cellular processes.

Moreover, continuous improvements in sequencing speed, accuracy, and data output have made RNA analysis more accessible and scalable for pharmaceutical, biotechnology, and academic research applications. High-throughput transcriptomics platforms currently facilitate large-scale studies that were earlier time- and cost-prohibitive, thus allowing a more in-depth consideration of disease mechanisms and biomarker discovery. Hence, adopting advanced sequencing technologies drives sustained demand for RNA analysis solutions across various research and clinical applications, placing the market for substantial growth.

Drug development and vaccine research

The research activities of the pharmaceutical industry and biotechnological sectors are increasingly relying upon RNA analysis, and hence, the market is witnessing substantial growth. RNA profiling has enabled researchers to understand cellular processes more deeply, identify novel drug action targets, and study disease pathways with high precision. This becomes extremely important in areas such as oncology, infectious diseases, and rare genetic disorders, where such knowledge of gene expression patterns could significantly speed up bringing the most appropriate therapeutics into existence.

RNA therapeutics, including mRNA vaccines and RNAi therapeutics, generate increased demand. The commercial success of mRNA vaccines during the past viral pandemics paved the way for the RNA platforms to garner increased interest from commercial and government bodies. High-throughput RNA sequencing, in combination with state-of-the-art bioinformatics tools, is increasingly utilized to expedite vaccine development, monitor immune response, and identify possible safety concerns. Pharmaceutical companies and biotechnology firms, thus, working on RNA analysis, are improving their capabilities and promoting continuous growth while creating long-term opportunities in the global RNA analysis market.

Market Dynamics

The RNA analysis market is witnessing strong growth, driven by rising demand for high-resolution molecular profiling in research, clinical diagnostics, and biopharmaceutical applications. Increasing adoption of RNA sequencing and transcriptomic tools in oncology, immunology, infectious diseases, and personalized medicine is accelerating market expansion, along with a growing focus on biomarker discovery and companion diagnostics. Moreover, advancements in next-generation sequencing, single-cell RNA analysis, and bioinformatics, coupled with rising investments in genomics research and the development of RNA-based therapeutics such as mRNA vaccines and RNAi drugs, are expected to sustain market growth over the forecast period.

The growing adoption of transcriptomics in personalized and precision cancer medicine is expected to drive growth in the RNA analysis market. RNA analysis technologies, including RNA sequencing and transcriptome profiling, are increasingly used to assess gene expression patterns, identify cancer-specific biomarkers, and characterize tumor heterogeneity. These capabilities support the development of targeted therapies and personalized treatment strategies for oncology patients.

In addition, the increasing prevalence of cancer and rising focus on precision oncology are accelerating investments in advanced transcriptomic research and molecular diagnostics. Pharmaceutical and biotechnology companies, along with research institutions, are increasingly adopting RNA analysis tools to improve biomarker discovery, treatment selection, and therapeutic response monitoring, thereby contributing to market growth. For instance, in January 2025, Illumina, Inc. collaborated with NVIDIA to advance AI-powered multiomic and transcriptomic data analysis platforms to improve the interpretation of large-scale RNA sequencing datasets for drug discovery and clinical research, further strengthening the integration of AI into RNA analysis workflows in precision medicine.

The high cost of advanced RNA sequencing instruments and associated consumables is a key factor restraining the growth of the RNA analysis market. Technologies such as next-generation sequencing (NGS), single-cell RNA sequencing, and other high-throughput transcriptomic platforms require substantial capital investment in sophisticated sequencing systems, specialized reagents, sample preparation kits, and advanced bioinformatics infrastructure. These technologies also require continuous upgrades and integration with high-performance computing systems, further increasing end users' overall operational expenses.

In addition, recurring costs such as instrument maintenance, software licensing, data storage, and skilled personnel requirements significantly add to the total cost of ownership. This cost burden is particularly challenging for small and mid-sized research laboratories, academic institutes, and healthcare facilities, especially in developing and price-sensitive economies. As a result, limited affordability and budget constraints may slow down the global adoption of advanced RNA analysis technologies, thereby restraining overall market penetration.

Market Concentration & Characteristics

The RNA analysis industry is characterized by a high degree of innovation, driven by rapid advancements in sequencing technologies, bioinformatics tools, and RNA-based therapeutics. More accurate, high-throughput, and economical gene expression analysis is made possible by ongoing advancements in single-cell and next-generation RNA sequencing systems. Faster biomarker discovery and applications in personalized medicine are made possible by AI and machine learning advancements, which also improve the interpretation of complex transcriptome data. Creating revolutionary RNA-based therapeutics, such as mRNA vaccines and RNA interference (RNAi) treatments, also leads to large investments in state-of-the-art analytical tools, which support the market's inventive environment and promote steady growth in both the clinical and research sectors.

The RNA analysis industry has witnessed a moderate to high mergers and acquisitions, indicative of businesses' strategic attempts to broaden their product lines, technological prowess, and worldwide presence. Major firms actively pursue collaborations and acquisitions to access cutting-edge sequencing technology, bioinformatics tools, and specialist RNA analysis solutions. For instance, in August 2023, Danaher, a U.S.-based medical tool supplier, acquired British biotech firm Abcam for USD 5.7 billion. Abcam became a standalone entity within Danaher's Life Sciences division. Abcam emerged as a separate business inside the Life Sciences division of Danaher.

Regulatory frameworks are crucial in shaping the RNA analysis industry, influencing research and clinical applications. Stringent guidelines governing the use of genetic and transcriptomic data, clinical trials, and RNA-based therapeutics ensure the safety, efficacy, and ethical use of RNA technologies. For those involved in developing and commercializing RNA diagnostics and therapeutics, it is critical to comply with the requirements of various national regulatory agencies (for example, the FDA, EMA, and other regional regulatory authorities). Although sometimes seen as a burden and a delay in getting products to market, regulation ultimately supports innovation, as firms move forward with the required and adopt even higher standards for quality, must conduct extensive verification testing, and report transparently. Overall, regulation increases market confidence, protects end users, and supports developing, marketing, and disseminating safe and efficacious RNA products.

Continuous product expansion is a significant growth driver in the RNA analysis industry, mainly because companies are working towards addressing the broad and changing needs of research and clinical uses. Leading companies are developing and selling new RNA sequencing kits, reagents, consumables, and integrated analysis platforms with improved sensitivity, throughput, and accuracy.

Geographic expansion is a key growth driver in the RNA analysis industry, as companies increasingly seek to establish a presence in emerging markets alongside established regions like North America and Europe. Expanding into Asia-Pacific, Latin America, and the Middle East allows market players to tap into growing research initiatives, rising healthcare infrastructure investments, and increasing adoption of advanced genomic technologies. By broadening their geographic footprint, companies can capture new revenue streams, strengthen brand recognition, and respond more effectively to regional demands, driving sustained market growth.

Analyst Perspective

The RNA analysis market is expected to witness strong growth, driven by the expanding adoption of transcriptomics in precision medicine, oncology, infectious disease research, and biomarker discovery. Increasing use of RNA sequencing, RT-PCR, and gene expression profiling is enabling deeper insights into disease mechanisms and accelerating the development of targeted therapeutics. Growing investments in genomic research, rising prevalence of chronic diseases, and advancements in high-throughput sequencing and bioinformatics tools are further supporting market expansion. In addition, the shift toward personalized healthcare and continuous innovation in RNA analysis platforms is expected to strengthen demand for advanced, accurate, and scalable solutions across research and clinical applications.

Product Insights

Based on product, the kits & reagents segment held the largest revenue share of over 59.5% in 2025. Rising requirements for high-quality reagents and kits, coupled with the repeated usage of reagents and media in transcriptome studies, drive the growth of this segment. High-quality reagents and kits deliver unmatched efficiency and strong performance, ensuring reliable and reproducible sequencing outcomes at a minimal cost.

The services segment is expected to grow at the fastest CAGR from 2026 to 2033. Growing R&D activities in the pharmaceutical sector and increasing government investments in life science research are expected to raise the demand for RNA analysis services. Several companies, such as Eurofins Scientific, Genewiz, and QIAGEN, offer various RNA analysis services, including mRNA sequencing, transcriptome profiling, and end-to-end solutions such as RNA sample preparation, library construction, sequencing, and data analysis. Availability of various services is expected to boost the market in the coming years.

Technology Insights

Based on technology, the real time-PCR (qPCR) segment held the largest revenue share of over 43.4% in 2025. The high share was attributed to the wide usage of PCR for COVID-19 diagnostics across the globe. The qPCR technology is highly sensitive & quantitative, and one of the most suitable methods for interrogating a comparatively small number of transcripts in a broad set of samples. PCR offers relatively high-sensitivity detection of SARS-CoV-2, evaluation of viral RNA in various clinical samples, detection of SARS-CoV-2 mutations, and evaluation of anti-SARS-CoV-2 drugs.

The sequencing segment is anticipated to witness the fastest CAGR throughout the forecast period, owing to advancements in next-generation and SMRT sequencing technology. The presence of several companies providing single-cell RNA sequencing services and the advent of bioinformatics algorithms are also driving the market. Furthermore, increasing scientific awareness and decreasing costs of sequencing technologies are expected to fuel the segment over the forecast period.

Application Insights

Based on application, the infectious diseases and pathogenesis segment held the largest revenue share of over 18.1% in 2025, and it is expected to grow with the fastest CAGR over the forecast period. The identification of susceptible cells is crucial for understanding the pathogenic mechanism. Hence, there is increasing adoption of scRNA-sequencing to provide information about cell types susceptible to infection. Next-generation sequencing transforms the approach to infectious diseases, pathogenesis, and treating individuals. Various methodologies have been developed for measuring gene expression and biomarkers to make their translation into clinical practice more feasible.

The epigenetics segment is expected to grow significantly from 2026 to 2033, as the pharmaceutical importance of understanding epigenetics for studying disease prognosis and epidemiology is gradually increasing, as the pharmaceutical importance of understanding epigenetics for studying disease prognosis and epidemiology is gradually increasing. In addition, molecular dynamics will also become a versatile tool to complement experimental investigations of RNA structural dynamics to provide opportunities for expanding the field and maximizing gains from the molecular dynamics simulations, without any further methodological advances. As epigenetic modifications such as DNA methylation and histone modifications can alter the binding of transcription factors and other regulatory proteins, epigenetic analyses for understanding gene expression are expected to be highly demanded soon.

End Use Insights

Based on end use, the government institutes & academic centers segment held the largest revenue share of over 32.0% in 2025. The rising adoption rate of high-throughput technologies for the effective process of RNA analysis by government institutes and academic centers drives the segment growth. Increasing applications of transcriptomics technologies in drug discovery propel the demand in the pharmaceutical and biotechnological industries. Similarly, drug discovery research contributes to the market, followed by clinical diagnostics. For instance, in April 2021, researchers developed TORNADO-seq, an RNA sequencing-based drug discovery platform to monitor the expression of the large gene for a detailed study of organoid cellular phenotypes.

The Contract Research Organizations (CROs) segment is expected to grow at the fastest CAGR over the forecast period. Strategic activities by key market players support the segment growth. For instance, in Jan 2022, 10x Genomics announced the expansion of its 10x Certified Service Provider Network to incorporate three leading CROs. The CROs will partner with 10x Genomics to support leading biopharmaceutical companies seeking the advantage of 10x Genomics’ single-cell and spatial technologies to accelerate drug development and power novel therapeutic findings. The three CROs chosen for the 10x Genomics program are Azenta Life Sciences, Q2 Solutions, and CellCarta.

Regional Insights

North America dominated the RNA analysis market with the largest revenue share of 43.6% in 2025, due to established pharmaceutical and biotechnology companies, strong research infrastructure, and a large investment in genomic and transcriptomic analysis. The region benefits from widespread adoption of next-generation sequencing (NGS) technologies, a high concentration of academic and clinical research institutions, and strong government and private funding initiatives supporting RNA-based studies and therapeutics.

U.S. RNA Analysis Market Trends

The RNA analysis market in the U.S. held the largest share in the North America region in 2025. The U.S. dominates the global RNA analysis market due to its advanced research infrastructure, high biotechnology and pharmaceutical companies concentration, and significant public and private funding for genomic studies. Widespread adoption of next-generation sequencing (NGS) and single-cell RNA sequencing technologies, combined with the success of RNA-based therapeutics, continues to strengthen the U.S. market.

Europe RNA Analysis Market Trends

Europe held a significant share in the RNA analysis market, driven by robust research activities, favorable regulatory support, and increasing collaborations between academic institutions and biotechnology firms. Countries such as Germany, the United Kingdom, and France stand out as key players in the region due to their advanced research infrastructure, strong governmental initiatives to support precision medicine, and high uptake of next-generation sequencing (NGS) technologies. The presence of leading pharmaceutical and biotech companies and participation in clinical trials and RNA-based therapeutic development further support the market.

The UK RNA analysis market benefits from advanced research infrastructure, government-backed genomic projects, and collaborations between academic institutions and biotechnology firms. The country’s focus on clinical trials, RNA therapeutics, and personalized medicine supports steady growth in RNA analysis adoption.

The Germany RNA analysis market remains a primary European market for RNA analysis, backed by strong research academic programs, established biotechnology and pharmaceutical industries, and government-supported initiatives for precision medicine. Investing in translational research and clinical applications of RNA technologies in Germany continues to create demand for a reliable sequencing platform or an appropriate bioinformatics tool.

Asia Pacific RNA Analysis Market Trends

The Asia Pacific region is expected to grow at the fastest CAGR of 14.4% from 2026 to 2033. The Japanese government and non-government organizations highly support the growth of biotechnology research in the country and provide funds for research in medicine and life sciences. This encourages researchers to explore the transcriptomics space actively. Furthermore, increasing focus on APAC countries, owing to the low-cost manufacturing service, is expected to provide growth opportunities for the manufacturers. In addition, strategic activities, such as partnerships, will further augment the growth of this region. For instance, in January 2020, Genetron Holdings Ltd. entered into a strategic partnership agreement with Thermo Fisher Scientific to expand its precision cancer monitoring and diagnosis in China’s public hospitals.

The China RNA analysis market is emerging as one of the fastest-growing RNA analysis markets due to increasing research investments, expanding healthcare infrastructure, and rising adoption of next-generation sequencing technologies. Government initiatives promoting genomics and precision medicine and collaborations with global biotech companies are further boosting market demand.

The Japan RNA analysis market is a leading market in Asia, driven by significant investments in biotechnology, active government support for genomic research, and adoption of advanced RNA sequencing technologies. Pharmaceutical research and the development of RNA-based therapeutics are key growth factors in the country.

Middle East & Africa RNA Analysis Market Trends

The MEA region is gradually emerging as a growth market for RNA analysis, supported by increasing government investment in healthcare research and rising awareness of personalized medicine. Countries like Kuwait, the UAE, and Saudi Arabia are expanding their research infrastructure and forming collaborations with international biotech and pharmaceutical firms. Although adoption rates are lower compared to North America and Europe, growing clinical research initiatives, improving laboratory facilities, and an increasing focus on rare genetic disorders drive steady market growth in this region.

Kuwait is gradually entering the RNA analysis market, supported by government funding in healthcare research and partnerships with international biotechnology firms. The country is focused on improving laboratory infrastructure and expanding clinical research initiatives, contributing to moderate market growth in the MEA region.

Key RNA Analysis Company Insights

The RNA analysis industry features some established competitors through broad portfolios, partnerships, and ongoing investments in research and development. Key sector players such as Agilent Technologies, F. Hoffmann-La Roche, Illumina, QIAGEN, and Thermo Fisher Scientific hold substantial market share in RNA analysis markets by offering advanced RNA sequencing systems, sample preparation or kits, high-throughput analysis platforms, and the ability to enter the RNA analysis markets with bioinformatics and distribution networks that lead to global reach.

By offering cutting-edge solutions and customized RNA analysis services that meet the changing needs of academic institutions, pharmaceutical companies, and clinical research organizations, businesses like Eurofins Scientific, Merck KGaA, Bio-Rad Laboratories, Pacific Bioscience of California, Affymetrix, Danaher, and Promega are growing their footprint. These services include RNA-based biomarker discovery platforms, transcriptomic profiling, and single-cell RNA sequencing.

Prominent companies keep strengthening their position in the market by fusing state-of-the-art technology with extensive service offerings and calculated expansion plans. These companies have cemented their market leadership by meeting the growing need for accurate RNA profiling in precision medicine, drug discovery, infectious disease research, and RNA-based therapeutics. As the adoption of RNA sequencing technologies picks up speed, the competitive landscape is being shaped more and more by dedication to innovation, accessibility, and data accuracy. These factors are essential for the advancement of clinical and research applications.

The market for RNA analysis is dynamically interacting with new developments and well-established knowledge. Competition is getting more intense due to strategic alliances, mergers and acquisitions, and advancements in data interpretation and sequencing efficiency. In this quickly changing industry, businesses that successfully combine technological innovation with customer-focused solutions will be well-positioned to create long-term value and support the expansion of transcriptomics, personalized medicine, and RNA-based therapeutic development.

Key RNA Analysis Companies:

The following are the leading companies in the RNA analysis market. These companies collectively hold the largest market share and dictate industry trends.

- Agilent Technologies, Inc.

- F. Hoffmann-La Roche AG

- Illumina, Inc.

- QIAGEN

- Thermo Fisher Scientific, Inc.

- Eurofins Scientific

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- Pacific Bioscience of California, Inc.

- Affymetrix, Inc.

- Danaher

- Promega

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Merck KGaA, Thermo Fisher Scientific, Bio-Rad Laboratories, Agilent Technologies, etc.)

- Invest heavily in next-generation sequencing (NGS), transcriptomics platforms, and automation-driven RNA analysis technologies to support precision medicine and drug discovery.

- Deep integration with pharmaceutical, biotechnology, and academic research ecosystems enabling high recurring demand and platform stickiness.

- High dependence on research funding cycles and pharmaceutical R&D investment trends.

Emerging Players (Pacific Biosciences of California, Inc., Affymetrix, Inc., Promega)

- Focus on specialized RNA sequencing technologies and microarray-based gene expression profiling solutions for research and clinical applications.

- Strong technological differentiation in long-read sequencing (PacBio) and legacy microarray-based expression platforms (Affymetrix).

- Higher vulnerability to displacement by advanced NGS and multi-omics platforms from major competitors.

Recent Developments

- In April 2026, Alida Biosciences launched its EpiPlex Tri-Mod service, enabling simultaneous profiling of three key mRNA modifications. The service enhanced RNA analysis capabilities by supporting more comprehensive transcriptomic studies and improving the understanding of epitranscriptomic regulation in research applications.

RNA Analysis Market Report Scope

Report Attribute

Details

Market size in 2025

USD 9.2 billion

Estimated market size in 2026

USD 9.9 billion

Projected market size by 2040

USD 23.6 billion

Growth rate

CAGR of 13.3% from 2026 to 2040

Historical data

2021 - 2025

Forecast period

2026 - 2040

Quantitative units

Revenue in USD million, and CAGR from 2026 to 2040

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, technology, application, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S., Canada, Mexico, UK, Germany, France, Italy, Spain, Norway, Denmark, Sweden, China, Japan, India, South Korea, Australia, Thailand, Brazil, Argentina, Saudi Arabia, South Africa, UAE, and Kuwait

Key companies profiled

Agilent Technologies, Inc.; F. Hoffmann-La Roche AG; Illumina, Inc.; QIAGEN; Thermo Fisher Scientific, Inc.; Eurofins Scientific; Merck KGaA; Bio-Rad Laboratories, Inc.; Pacific Bioscience of California, Inc.; Affymetrix, Inc.; Danaher; Promega

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global RNA Analysis Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For the purpose of this report, Grand View Research has segmented the global RNA analysis market on the basis of product, technology, application, end use, and region.

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Instruments

-

Kits & Reagents

-

miRNA & siRNA

-

Reverse Transcriptases & RT-PCR

-

RNA Extraction & Purification

-

RNA Interference

-

Others

-

-

Services

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Real Time-PCR (qPCR)

-

Microarray

-

Sequencing

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Construction of RNA expression atlas

-

Epigenetics

-

Infectious diseases and pathogenesis

-

Alternative RNA splicing

-

RNA structure and molecular dynamics

-

Development and delivery of RNA therapeutics

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Government Institutes & Academic Centers

-

Pharmaceutical & Biotechnology Companies

-

Contract research Organizations (CROs)

-

Hospitals & Clinics

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

The RNA analysis market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each RNA analysis segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment- Product

Revenue Capture Definition

Instruments

Revenue generated from analytical and molecular biology equipment used to detect, quantify, and characterize RNA molecules across research and clinical workflows. This includes platforms supporting transcript quantification, gene expression profiling, and RNA quality assessment used in genomics, diagnostics, and therapeutic development.

Kits & Reagents

This segment captures income from consumable solutions used throughout RNA analysis workflows, including miRNA and siRNA-based assay kits for gene regulation studies, reverse transcriptases and RT-PCR reagents for cDNA synthesis and amplification, RNA extraction and purification kits for isolating high-quality RNA, RNA interference reagents for gene silencing studies, and other specialized molecular biology consumables supporting transcriptomic research and clinical applications.

Services

Market value in this category stems from outsourced RNA analysis offerings provided by specialized laboratories and service providers, including RNA sequencing, expression profiling, bioinformatics analysis, and transcriptomic data interpretation services used by research institutions, biotech firms, and pharmaceutical companies.

Segment - Technology

Revenue Capture Definition

Real-Time PCR (qPCR)

Revenue derived from quantitative PCR-based RNA analysis technologies used for precise measurement of gene expression levels, biomarker validation, pathogen detection, and clinical diagnostics across research and healthcare settings.

Microarray

This segment reflects income from hybridization-based RNA profiling platforms used for large-scale gene expression analysis, comparative transcriptomics, and biomarker discovery applications in biomedical research.

Sequencing

Market value is generated from next-generation sequencing and related transcriptomic technologies used for comprehensive RNA profiling, including gene expression analysis, RNA-Seq studies, splice variant detection, and advanced molecular characterization.

Others

Includes revenue from emerging or specialized RNA analysis technologies not classified under major platforms, such as novel digital PCR systems, hybrid analytical methods, and advanced transcriptomic profiling tools.

Segment - Application

Revenue Capture Definition

Construction of RNA Expression Atlas

Revenue originates from RNA analysis applications focused on building comprehensive gene expression databases across tissues, diseases, and developmental stages to support systems biology and functional genomics research.

Epigenetics

This segment captures income from RNA analysis used to study gene regulation mechanisms influenced by epigenetic modifications, including RNA-mediated chromatin interactions and regulatory RNA functions.

Infectious Diseases & Pathogenesis

Market value stems from RNA-based studies used to identify pathogens, analyze host-pathogen interactions, and understand disease mechanisms in viral, bacterial, and emerging infectious diseases.

Alternative RNA Splicing

Revenue generated from applications analyzing RNA splicing variations and transcript isoforms to understand gene diversity, disease mechanisms, and regulatory complexity in biological systems.

RNA Structure & Molecular Dynamics

This segment reflects earnings from RNA analysis focused on secondary and tertiary RNA structure characterization and molecular behavior studies critical for functional genomics and drug design.

Development & Delivery of RNA Therapeutics

Income arises from RNA analysis applications supporting the design, optimization, and evaluation of RNA-based therapeutics such as mRNA vaccines, siRNA therapies, and antisense oligonucleotide drugs.

Others

Includes revenue from RNA analysis applications across microbiome research, biomarker discovery, agricultural genomics, and other emerging transcriptomic fields.

Segment - End Use

Revenue Capture Definition

Government Institutes & Academic Centers

Revenue generated from RNA analysis technologies used by universities, public research organizations, and government-funded laboratories engaged in fundamental and applied transcriptomic research.

Pharmaceutical & Biotechnology Companies

This segment captures income from RNA analysis solutions utilized in drug discovery, target validation, biomarker identification, and RNA-based therapeutic development by pharma and biotech firms.

Hospitals & Clinics

Market value stems from clinical adoption of RNA analysis for disease diagnosis, patient stratification, infectious disease detection, and personalized medicine applications in healthcare settings.

Contract Research Organizations (CROs)

Revenue originates from outsourced RNA analysis services provided by CROs supporting pharmaceutical, biotech, and academic clients in transcriptomic research, clinical trials, and molecular diagnostics workflows.

Estimation Model

Top-Down

Parent Market

Segmentation

Validation

Forecasting

Commodity Flow Analysis

Parent Market & Penetration-Based Analysis

Country-Level Segment Share Modeling

Data Triangulation & Validation Model

Forecasting & CAGR Modeling

Market size was estimated by analyzing revenues generated by key RNA analysis product manufacturers, including providers of instruments, kits & reagents, consumables, and software solutions. Data were sourced from company annual reports, investor presentations, product portfolios, and premium industry databases. Revenue contributions from private and emerging players were assessed through secondary research and validated through primary interviews to derive the overall market value.

The RNA analysis market was evaluated within the broader biotechnology market. The adoption of RNA analysis technologies across genomics research, transcriptomics, drug discovery, oncology research, infectious disease research, and precision medicine was analyzed, along with research funding trends and clinical adoption rates, to estimate the addressable market and segment-level opportunities.

Market shares for product type, technology (RNA sequencing, RT-PCR, microarrays), application, and end-use segments were derived using country-specific biotechnology R&D expenditure, genomic research activity, clinical trial density, healthcare infrastructure, and academic research output. Weighted-average calculations were used to determine regional and global segment distributions.

Market estimates were validated through triangulation of secondary research, primary interviews, company-level revenue assessments, publication trends in genomics research, and end-user adoption patterns to ensure consistency and accuracy across all market segments and geographies.

Market forecasts were developed using historical growth in transcriptomics research, expansion of precision medicine, increasing adoption of RNA sequencing technologies, rising oncology research activity, and growing investments in biotechnology infrastructure. Regression-based analysis and trend modeling were applied to project future market growth and CAGR.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-Segmentation Analysis for RNA Analysis Market (Product × Technology × Application × End Use)

Detailed multi-layered cross-tabulation across key RNA analysis segments including instruments, kits & reagents (miRNA, siRNA, RT-PCR, RNA extraction & purification), and services mapped against technologies such as qPCR, microarray, next-generation sequencing (NGS) and applications including infectious diseases, RNA therapeutics, epigenetics, and transcriptome profiling across end-use segments like pharma & biotech, academic & research institutes, CROs, and hospitals/clinics.

Enables identification of high-growth transcriptomics workflows, reveals shifts in technology adoption, highlights untapped application niches (RNA therapeutics, precision oncology), and supports portfolio prioritization across RNA workflows and consumables ecosystems.

Competitive Intelligence & Benchmarking for RNA Analysis Ecosystem

Comprehensive benchmarking of key players (e.g., Illumina, Thermo Fisher Scientific, QIAGEN, Bio-Rad, Roche, Agilent, PacBio, Merck KGaA, Eurofins) across NGS platforms, PCR systems, RNA kits, reagents, sequencing services, bioinformatics tools, pricing strategies, R&D intensity, partnerships, and M&A activity.

Helps clients evaluate technology leadership vs. consumables dominance, identify competitive white spaces in RNA sample prep and bioinformatics, assess vertical integration opportunities (sample-to-insight workflows), and refine market-entry and differentiation strategies for transcriptomics tools.

Regional Demand, Clinical Adoption & Investment Opportunity Assessment

Region-wise and country-level analysis across North America, Europe, Asia Pacific, Latin America, and MEA, focusing on research funding intensity, genomic infrastructure, adoption of NGS-based RNA sequencing, clinical diagnostics penetration, biotech ecosystem maturity, and regulatory landscape (FDA/EMA/region-specific frameworks).

Supports the identification of the fastest-growing RNA sequencing hubs (Asia-Pacific, China, India), evaluates precision medicine adoption curves, enables investment prioritization in genomics infrastructure, and helps align strategies with regional clinical- and research-driven transcriptomics demand.

Frequently Asked Questions About This Report

The global RNA analysis market size was valued at USD 9.2 billion in 2025 and is expected to reach USD 9.9 billion in 2026.

The global RNA analysis market is expected to grow at a compound annual growth rate of 13.3% from 2026 to 2033 to reach USD 23.6 billion by 2033.

Based on product, the kits & reagents segment led with a 59.5% revenue share in 2025.

Some key players operating in the RNA analysis market include Agilent Technologies; Bio-Rad Laboratories, Inc.; F. Hoffmann-La Roche AG; Illumina, Inc.; QIAGEN; Thermo Fisher Scientific, Inc.; Eurofins Scientific; Merck KGaA; Pacific Bioscience of California, Inc.; Affymetrix, Inc.; Danaher; Promega

Key factors that are driving the RNA analysis market growth include increasing interest of research entities in studying the transcriptomic profiles of humans and growing knowledge on the role of transcriptomics in disease diagnosis.

North America dominated with a 43.6% revenue share in 2025.

The real time-PCR (qPCR) segment held the largest revenue share of over 43.4% in 2025.

Based on application, the infectious diseases and pathogenesis segment held the largest revenue share of over 18.1% in 2025, and it is expected to grow with the fastest CAGR over the forecast period.

Based on end use, the government institutes & academic centers segment held the largest revenue share of over 32.0% in 2025.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.