- Home

- »

- Next Generation Technologies

- »

-

Ultrasonic Testing Market Size & Share Report, 2026-2033GVR Report cover

![Ultrasonic Testing Market Size, Share & Trends Report]()

Ultrasonic Testing Market (2026 - 2033) Size, Share & Trends Analysis Report By Type (Phased Array Ultrasonic Testing, Time-of-Flight Diffraction, Guided Wave Testing, Immersion Testing), By Equipment, By Services, By Application, By End Use Industry, By Region, And Segment Forecasts

Market Size, 2025

$3.6BMarket Estimate, 2026

$3.8BMarket Forecast, 2033

$6.4BCAGR, 2026–2033

7.7%Ultrasonic Testing Market Summary

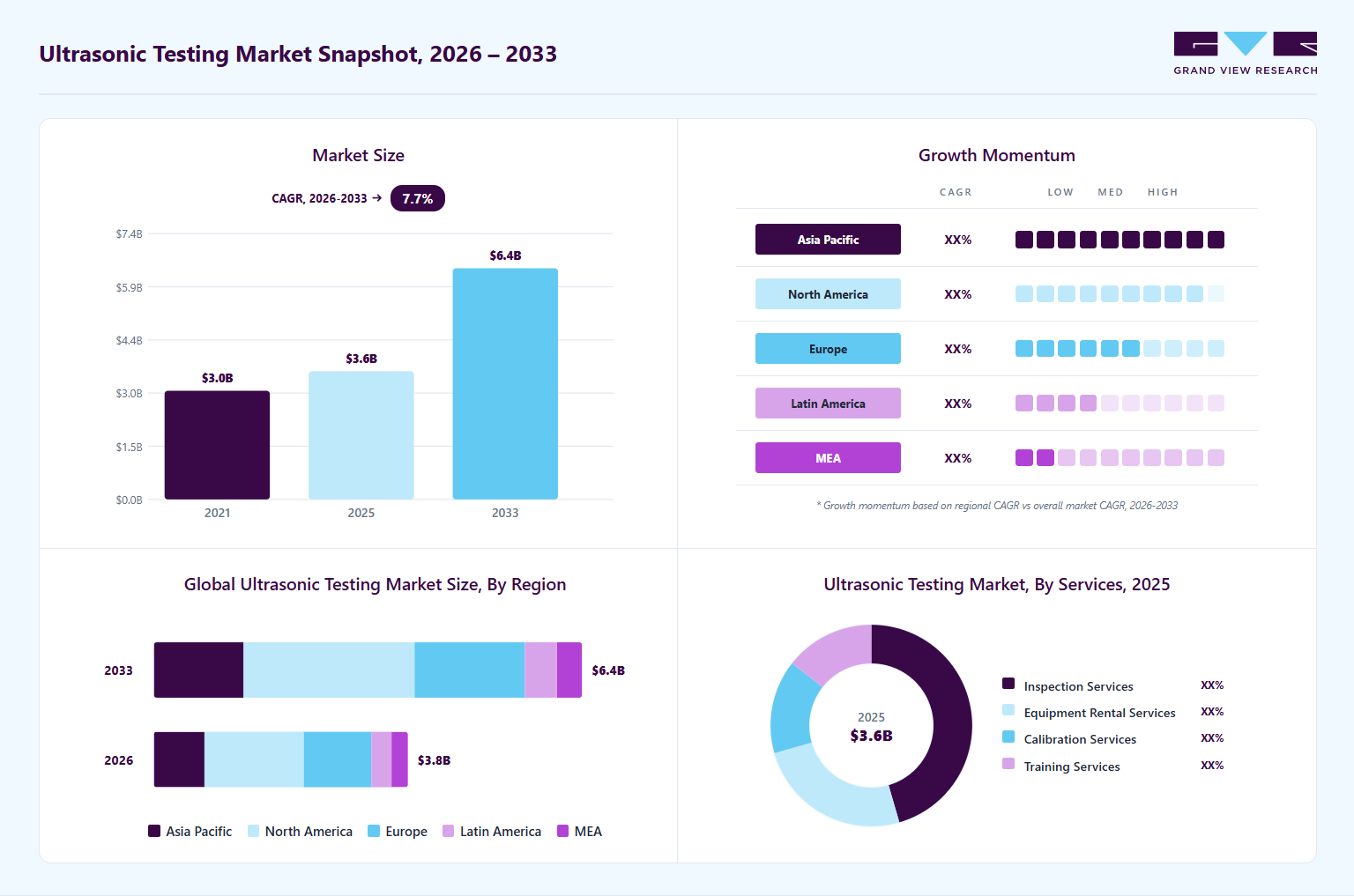

The global ultrasonic testing market size was valued at USD 3.6 billion in 2025 and is projected to grow from USD 3.8 billion in 2026 to USD 6.4 billion by 2033, at a CAGR of 7.7% from 2026 to 2033. The North America held the largest share of 39.0% of the global market in 2025. The growth of the market can be attributed to the government regulations mandating non-destructive testing (NDT), including ultrasonic testing (UT).

Key Market Trends & Insights

- By type: Phased array ultrasonic testing (PAUT) segment held the largest market share of 36.4% in 2025.

- By equipment: Flaw detectors segment accounted for the largest share in 2025.

- By services: Inspection services segment accounted for the largest share in 2025.

- By application: Weld inspection segment accounted for the largest share in 2025.

- By end use industry: Oil & gas segment accounted for the largest share in 2025.

Regional Highlights

- Largest regional market: North America (39.0% revenue share, 2025)

- By country: The U.S. held the dominant market position in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.6 Billion

- Estimated market size in 2026: USD 3.8 Billion

- Projected market size by 2033: USD 6.4 Billion

- CAGR (2026-2033): 7.7%

The U.S. Nuclear Regulatory Commission (NRC) enforces strict guidelines requiring regular ultrasonic testing inspections of reactor components to identify potential cracks or weaknesses that lead to catastrophic accidents. For instance, ultrasonic testing is used to inspect pressure vessels and piping systems in nuclear plants to prevent radioactive leaks. Similarly, in the oil and gas sector, regulations from agencies such as the U.S. Pipeline and Hazardous Materials Safety Administration (PHMSA) stipulate ultrasonic testing inspections during pipeline construction and maintenance to ensure integrity and prevent leaks or explosions. These regulatory requirements create a robust demand for ultrasonic testing equipment and qualified personnel, driving market expansion.")

Advancements in ultrasonic testing technology, such as phased array ultrasonic testing (PAUT) and time-of-flight diffraction (TOFD), are transforming the market by offering higher precision, faster inspection times, and improved defect detection capabilities. For instance, PAUT uses multiple ultrasonic probes to generate detailed images for precise flaw characterization. The National Institute of Standards and Technology (NIST) plays a pivotal role in developing standards and methodologies for these advanced ultrasonic testing techniques, ensuring their reliability and accuracy. The integration of automation and robotics in ultrasonic testing systems further enhances efficiency, reducing inspection times and operational costs. For example, automated ultrasonic testing systems are increasingly used in aerospace to inspect complex composite materials, thereby minimizing human error. These technological innovations make ultrasonic testing more attractive to industries, contributing to market growth. Ongoing research and development supported by government agencies such as NIST are expected to drive further advancements, sustaining this trend.

The adoption of continuous monitoring techniques using ultrasonic testing is a significant trend, particularly in industries such as manufacturing, energy, and transportation. Continuous ultrasonic testing monitoring enables real-time detection of developing fractures, voids, and other flaws, preventing unexpected equipment failures and reducing downtime for repairs. This approach enhances production efficiency and cost savings, making it highly desirable. The U.S. Department of Energy (DOE) emphasizes the importance of NDT methods, including ultrasonic testing, for ensuring the safety and reliability of energy infrastructure, such as pipelines and power generation equipment. For instance, ultrasonic testing is used to monitor pipelines for corrosion, preventing costly failures and environmental hazards. The regulatory push for regular inspections in power generation, driven by agencies such as the DOE, supports the growth of continuous ultrasonic testing monitoring systems, fueling market demand.

The integration of ultrasonic testing with digital technologies, such as artificial intelligence (AI) and data analytics, is creating new opportunities for market growth. AI-driven ultrasonic testing systems can analyze inspection data more accurately and quickly, improving defect detection and reducing human error. This trend is particularly evident in industries such as aerospace and defense, where precision and reliability are paramount. The Federal Aviation Administration (FAA) supports the development of advanced NDT technologies, including ultrasonic testing, to ensure the safety and performance of aircraft components. For instance, AI-enhanced ultrasonic testing is used to inspect composite materials in aircraft, detecting hidden defects with greater accuracy. Similarly, the U.S. Department of Defense (DOD) leverages advanced ultrasonic testing for defense applications, such as inspecting military equipment. The growing emphasis on predictive maintenance, supported by digital technologies, is expected to drive further adoption of ultrasonic testing, contributing to market expansion.

Market Dynamics

Rapid infrastructure development and modernization projects worldwide are driving the growth of the ultrasonic testing market. Investments in transportation infrastructure, such as railways, metros, bridges, airports, and energy pipelines, require regular inspection and maintenance to ensure operational safety and longevity. Ultrasonic testing plays a critical role in detecting cracks, corrosion, material fatigue, and structural flaws in these assets. Emerging economies, particularly in the Asia-Pacific, are witnessing strong industrialization and infrastructure spending, which is boosting demand for advanced inspection solutions. Government initiatives focused on manufacturing expansion, smart cities, and energy infrastructure development are further strengthening market growth prospects.

In addition, the rapid expansion of the renewable energy sector is driving the growth of the market. Wind turbines, solar infrastructure, hydrogen facilities, and offshore renewable installations require regular structural inspections to ensure operational safety and reliability. Ultrasonic testing is increasingly being used to inspect turbine blades, welded joints, pipelines, composite materials, and storage tanks used in renewable energy projects. Governments worldwide are heavily investing in clean energy infrastructure and energy transition initiatives, which are expected to generate substantial demand for advanced non-destructive testing solutions in the coming years.

The shortage of skilled and certified professionals capable of operating ultrasonic testing equipment is restraining the growth of the ultrasonic testing market. Ultrasonic inspection techniques require specialized expertise for accurate flaw detection, signal interpretation, equipment calibration, and compliance with strict industry standards. Incorrect handling or misinterpretation of inspection data can lead to false readings or undetected defects, posing operational and safety risks to industries that rely on non-destructive testing solutions.

Several emerging economies continue to face limited availability of trained non-destructive testing (NDT) personnel, reducing the adoption of advanced ultrasonic testing technologies across industrial applications. Ongoing training requirements, certification programs, and workforce development initiatives further increase operational costs for companies implementing sophisticated ultrasonic inspection systems.

The increasing adoption of predictive maintenance and condition-monitoring strategies across industrial sectors presents an opportunity for the ultrasonic testing market. Industries such as oil & gas, power generation, mining, and manufacturing are shifting from reactive maintenance toward predictive asset management to minimize downtime and reduce repair costs. Ultrasonic testing technologies enable continuous monitoring of equipment integrity, corrosion levels, weld quality, and structural health, making them essential for preventive maintenance programs. The growing industrial focus on extending asset life and improving operational efficiency is expected to create long-term opportunities for advanced ultrasonic inspection solutions.

Market Concentration & Characteristics

The ultrasonic testing market is moderately fragmented, with the presence of several global non-destructive testing (NDT) equipment manufacturers, inspection service providers, and specialized technology companies competing across industries such as oil & gas, aerospace, automotive, power generation, manufacturing, and infrastructure. The market includes established players offering advanced ultrasonic testing systems, phased-array technologies, automated inspection solutions, and digital monitoring platforms, alongside regional and niche companies that provide customized inspection services and portable testing equipment.

Competition is driven by technological innovation, product accuracy, automation capabilities, software integration, pricing strategies, and compliance with industry safety standards. Major companies focus on expanding their portfolios through research and development, partnerships, acquisitions, and geographic expansion to strengthen their market presence. The growing demand for automated ultrasonic testing, predictive maintenance solutions, and Industry 4.0-enabled inspection systems is further intensifying competition in the market.

Type Insights

The phased array ultrasonic testing market (PAUT) segment accounted for the largest share of 36.4% in 2025. PAUT is becoming widely adopted across industries due to its ability to scan large areas rapidly while delivering high-resolution images. It allows technicians to inspect complex geometries without physically moving the probe, which is especially valuable in aerospace and power generation sectors. As industrial safety regulations tighten globally, companies are shifting toward more precise and efficient testing methods such as PAUT for weld integrity checks and corrosion monitoring.

The time-of-flight diffraction (TOFD) segment is expected to grow at a significant CAGR during the forecast period. TOFD is gaining momentum for critical weld inspection, particularly in pipelines and pressure vessels. Its ability to size defects accurately and detect cracks with minimal operator influence makes it indispensable in industries where human safety and operational continuity are top priorities. Energy companies increasingly integrate TOFD into their quality assurance protocols due to its reliability and reproducibility.

Equipment Insights

The flaw detectors segment held the largest market share in 2025. Flaw Detectors are advancing with touchscreen interfaces and real-time imaging features, making them easier to use in field conditions. Modern handheld flaw detectors are compact and battery-efficient, ideal for technicians working on-site in sectors such as railways, aviation, and marine. These devices now support wireless data transfer and cloud connectivity, enabling faster reporting and remote collaboration. Moreover, integrating AI algorithms enables automated flaw detection, improving accuracy and reducing human error.

The thickness gauges segment is expected to grow at a significant CAGR from 2026 to 2033. Thickness gauges are evolving to offer dual-element probes and automatic data logging, enabling inspections even through paint or coatings. These instruments are vital in industries where wall thinning due to corrosion or erosion could lead to system failures, such as in chemical processing plants and ship hull inspections. Recent advancements also include Bluetooth connectivity and integration with mobile apps, streamlining data collection and analysis on-site. As regulatory standards tighten across industries, the demand for precise, efficient thickness measurement tools continues to rise.

Services Insights

The inspection services segment dominated the market in 2025, due to growing demand for third-party expertise for compliance and risk management. Hiring specialized service providers ensures inspections are conducted with the latest equipment and certified technicians, which is particularly crucial in regulated industries such as nuclear energy and aviation. Moreover, outsourcing inspection services reduces operational downtime and internal resource strain, allowing companies to focus on core functions. The rise of asset integrity management and predictive maintenance strategies further fuels the demand for professional inspection services.

The equipment rental services segment is projected to grow at the fastest CAGR over the forecast period. The segment is gaining traction among SMEs and project-based contractors who need access to advanced ultrasonic equipment without high upfront investments. Rental options are especially popular in the construction and civil engineering sectors for temporary bridge or structural inspections. This trend is supported by flexible rental models and bundled service offerings that include maintenance, calibration, and technical support and thereby driving growth of the ultrasonic testing equipment market. In addition, as technology evolves rapidly, renting allows users to access the latest equipment without concerns about asset depreciation.

Application Insights

The weld inspection segment dominated the market in 2025. Weld Inspection continues to be the primary application for ultrasonic testing, especially in infrastructure projects, shipbuilding, and pipeline networks. Non-destructive weld evaluation ensures the integrity of joints without halting production lines or dismantling structures. Advancements in phased array UT and time-of-flight diffraction (TOFD) are enhancing the precision and speed of weld inspections. With stricter quality standards and safety regulations worldwide, demand for reliable weld testing solutions is expected to remain strong across sectors.

The corrosion detection segment is projected to grow at the fastest CAGR over the forecast period. Corrosion detection is essential in sectors where metal degradation leads to environmental hazards or financial losses, such as in offshore oil rigs or chemical storage tanks. Ultrasonic testing detects early-stage corrosion, enabling proactive maintenance. Modern UT systems now offer high-resolution thickness mapping and automated scanning, improving detection accuracy in hard-to-reach areas. As infrastructure ages globally, the emphasis on corrosion monitoring is intensifying to extend asset life and ensure operational safety.

End Use Industry Insights

The oil & gas segment dominated the market in 2025. The oil & gas sector heavily relies on ultrasonic testing for pipeline inspection, tank bottom mapping, and corrosion under insulation. Strict regulations, such as PHMSA standards, drive ultrasonic testing adoption. Government investments in energy infrastructure, such as pipeline upgrades, further boost demand. In addition, the shift toward digital oilfields are accelerating the integration of advanced UT systems with real-time monitoring and data analytics. As exploration moves into harsher environments, the need for robust, accurate, and remote inspection tools continues to rise.

The aerospace segment is projected to grow at the fastest CAGR from 2026 to 2033. The increasing emphasis on aircraft safety, structural reliability, and regulatory compliance is driving the growth of ultrasonic testing in the aerospace industry. Aerospace manufacturers and maintenance providers are required to follow strict safety standards established by aviation authorities such as the FAA, EASA, and other international regulatory organizations. Ultrasonic testing plays a critical role in detecting internal defects, cracks, corrosion, delamination, and material fatigue in aircraft structures without causing damage to the components. The ability of ultrasonic testing to provide highly accurate and reliable inspection results makes it essential for maintaining airworthiness and ensuring passenger safety across commercial, military, and cargo aircraft fleets.

Regional Insights

The North America ultrasonic testing market accounted for the largest revenue share of 39.0% in 2025, driven by advanced industrial sectors, robust regulatory frameworks, and significant infrastructure investments. The region’s focus on safety and quality assurance in aerospace, oil & gas, and transportation fuels ultrasonic testing adoption. Widespread adoption of digital inspection technologies and skilled workforce availability further strengthen the region’s market position. Ongoing upgrades to aging infrastructure, such as bridges and pipelines, continue to create sustained demand for UT solutions.

U.S. Ultrasonic Testing Market Trends

The U.S. ultrasonic testing industry held a dominant position in 2025 in North America, propelled by widespread adoption in aerospace, oil & gas, and railway infrastructure inspections. The integration of advanced ultrasonic testing technologies, such as phased array ultrasonic testing (PAUT), enhances inspection accuracy. The U.S. Bipartisan Infrastructure Law (2021), allocating USD 1.2 trillion for transportation and energy projects, drives ultrasonic testing use for weld and corrosion inspections in bridges and pipelines.

Europe Ultrasonic Testing Market Trends

The Europe ultrasonic testing industry was identified as a lucrative region in 2025, driven by strong automotive, aerospace, and manufacturing sectors. The region’s commitment to quality standards and technological advancements supports ultrasonic testing growth. Ultrasonic testing market in Germany thrives due to its robust automotive and manufacturing industries, with a focus on automated ultrasonic testing (AUT) for quality control. The UK ultrasonic testing market is a hub for ultrasonic testing innovation, particularly in aerospace and defense, with increasing adoption of continuous monitoring techniques.

Asia Pacific Ultrasonic Testing Market Trends

The Asia-Pacific region is experiencing rapid growth in the ultrasonic testing market, fueled by industrialization and infrastructure development in countries such as China, India, and Japan. The increasing focus on quality assurance and safety standards in industries such as oil & gas, manufacturing, and construction drives the demand for ultrasonic testing solutions. Government initiatives to promote technology adoption and ensure regulatory compliance further boost market growth.

Ultrasonic testing market in China is expanding due to its robust manufacturing sector and extensive infrastructure projects. The country's emphasis on safety in industries such as oil & gas, construction, and transportation leads to increased adoption of ultrasonic testing solutions. In addition, China's investments in renewable energy and high-speed rail projects necessitate regular inspection and maintenance, further driving the demand for ultrasonic testing technologies.

India's ultrasonic testing market is growing rapidly, supported by government initiatives such as “Make in India” and increased investments in infrastructure and manufacturing. The country’s emphasis on safety and quality standards across industries such as aerospace, oil & gas, and construction drives the demand for ultrasonic testing solutions. Additionally, India’s push for defense indigenization and the development of smart cities further propels the adoption of ultrasonic testing technologies to ensure safe and reliable infrastructure.

Key Ultrasonic Testing Company Insights

Some of the major players in the ultrasonic testing market include Baker Hughes Company, MISTRAS Group, Eddyfi Technologies, Sonatest, Intertek Group plc, among others, due to their comprehensive technological capabilities, consistent innovation in non-destructive testing (NDT) solutions, and their ability to serve a wide range of end-use industries including oil & gas, aerospace, automotive, manufacturing, and power generation. These companies lead the market by offering advanced ultrasonic testing systems such as phased array, time-of-flight diffraction, and high-resolution imaging technologies, often integrated with artificial intelligence and digital data platforms.

-

Baker Hughes Company, through its Waygate Technologies business, provides industrial inspection, offering a full spectrum of ultrasonic testing (UT) equipment, from precision thickness gauges to advanced phased‑array systems. Its heritage (over 75 years of NDT innovation) and global service network enable it to support critical sectors (aerospace, oil & gas, power generation) with turnkey solutions and 24/7 field support. Waygate’s ability to integrate hardware, software, and data‑analytics platforms positions Baker Hughes as a one‑stop provider for customers seeking reliability, traceability, and lifecycle asset management in ultrasonic testing.

-

MISTRAS Group is a NDT services and equipment provider with deep domain expertise in ultrasonic inspection. Its provides in‑lab testing, field inspection services, and data analytics, enabling turnkey delivery of inspection programs for energy, aerospace, and manufacturing clients. The company’s global footprint of accredited labs and its emphasis on digital data solutions equip customers with actionable insights for predictive maintenance and risk management.

Key Ultrasonic Testing Companies

The following key companies have been profiled for this study on the ultrasonic testing market.

-

Baker Hughes Company

-

MISTRAS Group

-

Eddyfi Technologies

-

Sonatest

-

Intertek Group plc

-

Olympus Corporation

-

TÜV Rheinland

-

NDT Systems Inc

-

Sonotron NDT

-

Cygnus Instruments Ltd

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Baker Hughes Company; MISTRAS Group; TÜV Rheinland; Eddyfi Technologies

- Mature players in the ultrasonic testing market are focusing on expanding their advanced non-destructive testing (NDT) portfolios through automation, phased-array ultrasonic testing (PAUT), digital inspection platforms, and predictive maintenance solutions. Their strategies emphasize long-term service contracts with industries such as oil & gas, aerospace, power generation, automotive, and manufacturing.

- Mature players gain a competitive advantage through strong global inspection networks, extensive certification expertise, advanced ultrasonic testing technologies, and comprehensive service capabilities. Their ability to deliver highly accurate flaw detection, automated inspection systems, regulatory compliance support, and integrated asset integrity solutions strengthens their leadership across safety-critical industries.

- These companies often face challenges related to high operational costs, complex organizational structures, and slower adaptation to niche industrial requirements. Large-scale operations can delay rapid innovation and customization for emerging applications such as compact portable testing systems and AI-driven inspection analytics.

Emerging Players: Hi-Target; VI Instruments

- Emerging players in the ultrasonic testing market focus on developing portable, lightweight, and application-specific inspection solutions for industries including marine, infrastructure, manufacturing, and field services. Their strategies center on product customization, faster innovation cycles, user-friendly interfaces, and affordable inspection technologies.

- Emerging players gain market traction through flexibility, faster product development, and specialized ultrasonic inspection expertise. Their compact and cost-efficient systems are ideal for field inspections, remote operations, and small-scale industrial applications.

- Emerging players face limitations related to smaller global distribution networks, lower brand recognition, and restricted financial resources compared to multinational competitors. Limited large-scale service infrastructure and lower investment capacity in advanced automation or AI-driven inspection technologies can restrict expansion opportunities.

Recent Developments

-

In January 2026, NDT Global introduced CIGMA‑x, a next‑generation inline inspection tool that brings ultrasonic Lamb‑wave crack detection to live gas pipelines without needing liquid coupling, delivering high-confidence identification and accurate depth sizing for stress‑corrosion cracking (SCC) and linear cracks. Developed with operator partners and validated in full‑scale gas loops, CIGMA‑x demonstrated ~98% probability of detection for in‑scope linear features, ±1.4 mm depth accuracy, and combined pulse‑echo and pitch‑and‑catch modes plus ML‑enhanced signal processing to reduce false calls and unnecessary excavations.

-

In June 2025, Eddyfi Technologies introduced Cypher, a next‑generation portable phased‑array ultrasonic testing (PAUT) platform designed to make high‑end ultrasonic inspection faster, clearer, and more accessible to inspectors in demanding industrial environments. Built around the Total Focusing Method (TFM), Cypher delivers the fastest TFM inspection speeds on the market, with a 12.1‑inch, sunlight‑readable touchscreen that simplifies setup, automatic probe and scanner detection, and support for multiple techniques such as time‑of‑flight diffraction (TOFD), phase‑coherence imaging, and plane‑wave imaging. The platform is ruggedized with IP65 protection and MIL‑STD‑810G drop resistance, features hot‑swappable batteries for continuous operation, and includes cloud‑enabled data sync, enabling teams to generate real‑time reports, collaborate remotely, and analyze results from harsh sites such as offshore facilities, refineries, and aerospace plants.

-

In April 2025, MISTRAS Group launched MISTRAS Data Solutions, a unified platform integrating its inspection data services, digital twins, IoT-enabled sensors, and predictive analytics capabilities. This strategic move aims to provide customers across the energy, aerospace, and infrastructure sectors with centralized, real-time integrity data to improve maintenance efficiency. Furthermore, in May 2025, MISTRAS announced strong Q1 2025 earnings, attributing growth to the increased demand for ultrasonic inspection services and rising adoption of its new digital solutions suite, reinforcing its position as a data-driven leader in the ultrasonic testing market.

-

In April 2024, Baker Hughes Companys’ Waygate Technologies introduced the Krautkrämer CL Go+, a next-generation ultrasonic precision thickness gauge offering ±0.001 mm accuracy and a user-friendly interface. The portable device is designed for fast, non-destructive wall-thickness measurement across industries like aerospace and energy. In addition, in April 2025, Baker Hughes showcased its RotoArray comPAct phased-array probe and Krautkrämer USM 100 flaw detector at Control 2025 in Stuttgart, Germany. These innovations feature AI-assisted imaging and miniaturized electronics, underlining Baker Hughes’ commitment to precision, portability, and digital transformation in ultrasonic testing.

Ultrasonic Testing Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 3.6 billion

Estimated market size in 2026

USD 3.8 billion

Projected market size by 2033

USD 6.4 billion

Growth rate

CAGR of 7.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, equipment, services, application, end use industry, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Baker Hughes Company; MISTRAS Group; Eddyfi Technologies; Sonatest; Intertek Group plc; Olympus Corporation; TÜV Rheinland; NDT Systems Inc; Sonotron NDT; Cygnus Instruments Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Ultrasonic Testing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global ultrasonic testing market report based on type, equipment, services, application,end use industry, and region:

-

Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Phased Array Ultrasonic Testing (PAUT)

-

Time-of-Flight Diffraction (TOFD)

-

Guided Wave Testing

-

Immersion Testing

-

Others

-

-

Equipment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Flaw Detectors

-

Thickness Gauges

-

Transducers & Probes

-

Imaging Systems

-

Tube Inspection Systems

-

Others

-

-

Services Outlook (Revenue, USD Billion, 2021 - 2033)

-

Inspection Services

-

Equipment Rental Services

-

Calibration Services

-

Training Services

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Weld Inspection

-

Corrosion Detection

-

Thickness Measurement

-

Material Characterization

-

Others

-

-

End Use Industry Outlook (Revenue, USD Billion, 2021 - 2033)

-

Oil & Gas

-

Manufacturing

-

Aerospace

-

Power Generation

-

Automotive

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Ultrasonic Testing Market Opportunity Assessment

Country/region-wise market sizing and forecasts for conventional ultrasonic testing, phased array ultrasonic testing (PAUT), and automated ultrasonic testing (AUT) systems

Analysis of industrial infrastructure development across oil & gas, aerospace, power generation, manufacturing, and transportation sectors

Identification of high-growth regional markets and industrial investment hotspots

Identified region-specific growth opportunities

Supported expansion and market entry strategies

Enabled informed regional investment decisions

Technology and Innovation Assessment

Evaluation of emerging ultrasonic testing technologies, including PAUT, TOFD, digital ultrasonic testing, and robotic inspection systems

Analysis of AI integration, predictive maintenance capabilities, and Industry 4.0 trends in ultrasonic inspection

Supported technology roadmap planning

Identified innovation and investment opportunities

Enabled strategic R&D decision-making

Competitive Benchmarking and Strategic Positioning

Benchmarking of key competitors based on product portfolios, ultrasonic testing technologies, geographic presence, and end-use industry focus

Comparative assessment of portable ultrasonic devices, automated inspection systems, and digital NDT solutions

Analysis of partnerships, acquisitions, certifications, and innovation strategies

Identified competitive white spaces and market gaps

Supported differentiation and strategic positioning

Enabled data-driven competitive intelligence

Frequently Asked Questions About This Report

Some of the key players in the ultrasonic testing market include Baker Hughes Company, MISTRAS Group, Eddyfi Technologies, Sonatest, Intertek Group plc, Olympus Corporation, TÜV Rheinland, NDT Systems Inc, Sonotron NDT, Cygnus Instruments Ltd.

Rising demand for non-destructive testing in aging infrastructure and advanced manufacturing is driving growth in the ultrasonic testing market.

The global ultrasonic testing market size was valued at USD 3.6 billion in 2025 and is estimated at USD 3.8 billion for 2026.

The global ultrasonic testing market is expected to grow at a CAGR of 7.7% from 2026 to 2033, reaching USD 6.4 billion by 2033.

The phased array ultrasonic testing (PAUT) segment led the market with a 36.4% revenue share in 2025.

The flaw detectors segment held the largest market share in 2025.

The inspection services segment dominated the market in 2025, while equipment rental services are projected to grow at the fastest CAGR.

The weld inspection segment dominated the market in 2025, while corrosion detection is projected to grow at the fastest CAGR.

The oil & gas segment dominated the market in 2025.

North America dominated the market with a 39.0% revenue share in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.