- Home

- »

- Petrochemicals

- »

-

Viscosity Index Improvers Market Report, 2025-2033GVR Report cover

![Viscosity Index Improvers Market Size, Share & Trends Report]()

Viscosity Index Improvers Market (2025 - 2033) Size, Share & Trends Analysis Report by Product (Polymethacrylate, Ethylene Propylene Copolymer, Polyisobutylene, Hydrostyrene Diene Copolymer), By Application (Engine Oils, Transmission Fluids, Gear Oils), By Region, And Segment Forecasts

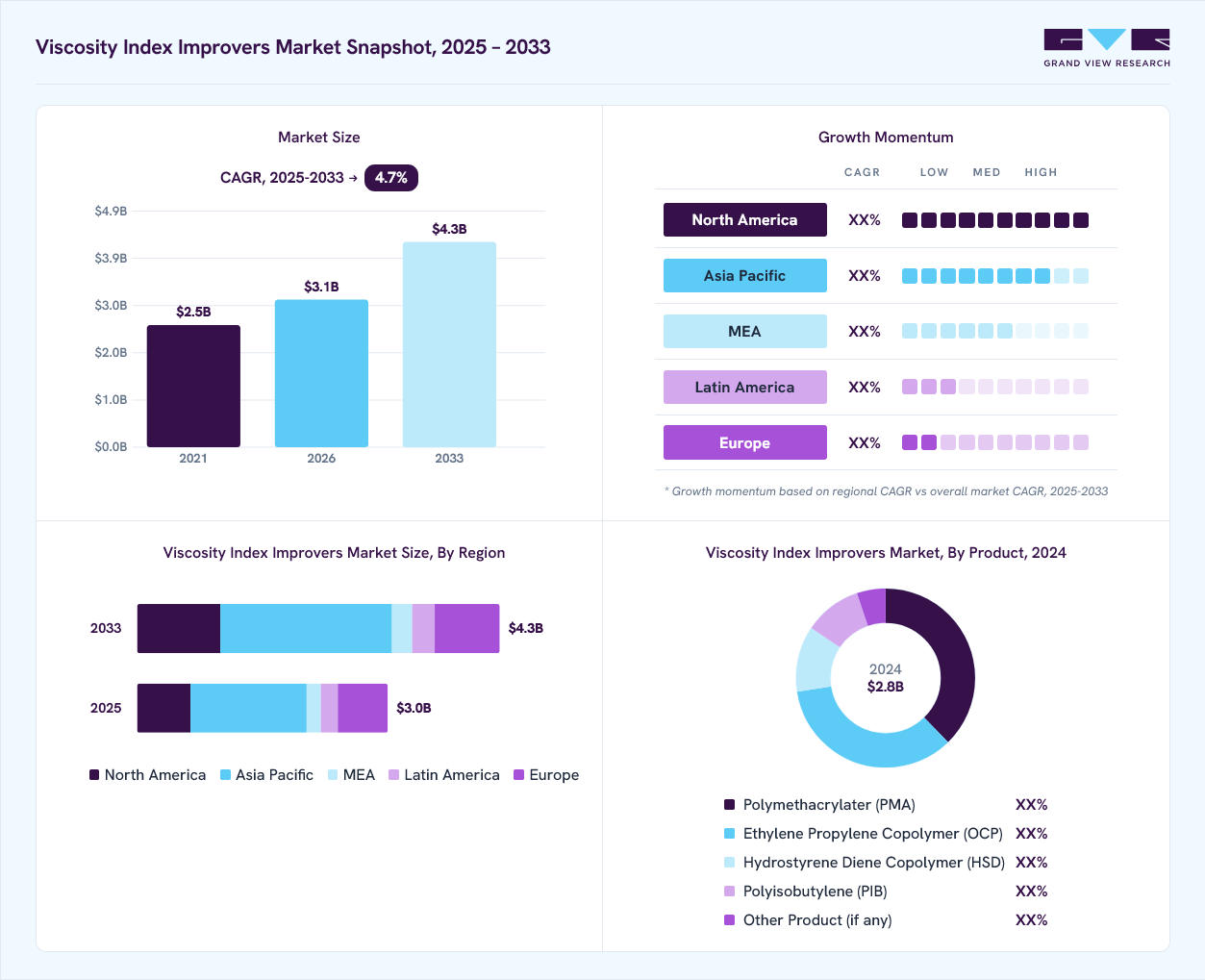

Market Size, 2024

$2.8BMarket Estimate, 2026

$3.1BMarket Forecast, 2033

$4.3BCAGR, 2025–2033

4.7%Viscosity Index Improvers Market Summary

The global viscosity index improvers market size was valued at USD 2.8 billion in 2024 and is projected to grow from USD 3.1 billion in 2026 to USD 4.3 billion by 2033, at a CAGR of 4.7% from 2025 to 2033. Asia Pacific dominated the market, accounting for a revenue share of 46.2% in 2024. The viscosity modifiers and viscosity index improvers are same.

Key Market Trends & Insights

- The China viscosity index improvers market is driven by massive automotive production, industrial manufacturing, and lubricant consumption.

- By product, the polymethacrylater (PMA) segment held the highest market share of 37.7% in 2024 in terms of revenue.

- By application, the engine oils segment led the viscosity index improvers industry with the largest revenue share of 50.0% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 2.8 billion

- 2033 Projected Market Size: USD 4.3 billion

- CAGR (2025-2033): 4.7%

- Asia Pacific: Largest Market in 2024

- North America: Fastest Growing Market

The viscosity modifiers (also known as viscosity index improvers) are key polymeric additives used to enhance the temperature-dependent behavior of lubricants and oils, ensuring consistent performance across varying thermal conditions. The market growth is primarily driven by the expanding automotive and industrial lubricant sectors, where the demand for high-performance, fuel-efficient, and low-viscosity lubricants continues to rise.Increasing production of passenger and commercial vehicles, coupled with stricter emission norms, has accelerated the adoption of viscosity index improvers in engine oils, transmission fluids, and hydraulic lubricants.

")

Another major growth driver is the increasing emphasis on fuel efficiency and emission reduction. Modern engine designs operate under higher temperatures and pressures, requiring lubricants that maintain optimal viscosity and film strength. Viscosity index improvers help achieve better energy efficiency by reducing frictional losses, improving cold-start performance, and extending oil drain intervals. The development of advanced hydrogenated styrene-diene and polymethacrylate-based VIIs is enabling the formulation of next-generation lubricants with superior shear stability and oxidation resistance. Additionally, the growing adoption of synthetic and semi-synthetic lubricants in both automotive and industrial sectors is further strengthening market demand for high-quality viscosity modifiers.

Furthermore, the rapid emergence of electric and hybrid vehicles presents new opportunities for viscosity index improver manufacturers. Electric vehicle (EV) drivetrains and e-transmissions require specialized lubricants with controlled thermal and rheological properties, creating demand for tailor-made VIIs compatible with low-viscosity fluids. The increasing industrial automation and expansion of heavy machinery, construction, and marine sectors also support lubricant consumption, reinforcing the market’s long-term growth outlook. Overall, ongoing product innovation, evolving engine technologies, and the global shift toward sustainability are expected to drive steady expansion in the viscosity index improvers market through 2033.

Market Concentration & Characteristics

The viscosity index improvers (VII) market is moderately consolidated, with a few global chemical and lubricant additive manufacturers dominating overall supply. Major players such as Lubrizol Corporation, Infineum International, Afton Chemical Corporation, and BASF SE hold significant market shares due to their strong product portfolios, global distribution networks, and long-standing relationships with lubricant formulators and OEMs. These companies invest heavily in R&D to develop advanced polymer chemistries, such as hydrogenated styrene-diene copolymers (HSDs) and polymethacrylates (PMAs), that offer superior shear stability and thermal performance for high-end lubricants. Entry barriers are relatively high, given the capital-intensive production process, the need for technical expertise in polymer synthesis, and stringent quality and performance validation standards required by end users.

At the same time, the market is witnessing a gradual shift toward regional diversification and strategic partnerships. Emerging Asian producers, particularly in China, India, and South Korea, are expanding capacity to cater to growing domestic lubricant demand, leading to increased competition at the regional level. However, the formulation of OEM-approved lubricant additives remains largely controlled by established multinational companies that possess proprietary technologies and testing capabilities. This dynamic results in a moderately concentrated but technologically differentiated market, where innovation, long-term supply contracts, and customized formulation capabilities are the key competitive advantages.

Products Insights

The polymethacrylater (PMA) segment led the market and accounted for the largest revenue share of 37.7% in 2024. This segment represents one of the most widely used viscosity index improvers due to its excellent thickening efficiency, thermal stability, and shear resistance across a wide temperature range. PMA-based VIIs are commonly used in engine oils, transmission fluids, and hydraulic lubricants, providing consistent viscosity performance under both high and low operating conditions. Their chemical versatility allows formulators to tailor molecular weight and structure for specific lubricant requirements, enabling optimal balance between viscosity control and fuel efficiency.

The hydrostyrene diene copolymer (HDO) segment is anticipated to grow at the fastest CAGR of 7.6% during the forecast period. This is driven by its superior shear stability, oxidation resistance, and long-term durability in severe operating environments. HSD-based VIIs are primarily used in synthetic and high-end lubricants, including heavy-duty diesel oils, transmission fluids, and industrial gear oils. Their unique molecular architecture allows for minimal viscosity loss under mechanical stress, making them ideal for modern engines that operate at higher pressures and temperatures.

Application Insights

The engine oils segment led the viscosity index improvers industry with the largest revenue share of 50.0% in 2024. This driven by the extensive use of multigrade lubricants in passenger and commercial vehicles. Viscosity index improvers are essential in engine oil formulations to maintain optimal viscosity over a wide temperature range, ensuring smooth cold starts, reduced friction, and enhanced fuel efficiency. With the automotive industry’s focus on reducing emissions and improving engine performance, advanced VIIs such as polymethacrylates (PMAs) and hydrogenated styrene-diene copolymers (HSDs) are increasingly used in synthetic and semi-synthetic oils.

The electrical vehicle (EV) fluids segment is expected to grow at the fastest CAGR with a CAGR of 18.3% from 2025 to 2033. The growth is supported by the rapid global shift toward electric mobility. Unlike traditional engine oils, EV fluids are engineered to provide thermal management, dielectric strength, and lubrication for e-transmissions, bearings, and cooling systems. Viscosity index improvers play a key role in maintaining stable viscosity under variable temperature and electrical conditions, ensuring system efficiency and component longevity.

Regional Insights

The Asia Pacific viscosity index improvers market accounted for the largest revenue share of 46.2% in 2024. The driven by its strong automotive manufacturing base and expanding industrial lubricant demand. Countries such as China, India, Japan, and South Korea are major consumers, supported by rising vehicle production, infrastructure development, and industrialization. The region also benefits from a well-established lubricant blending industry and increasing adoption of synthetic lubricants.

China Viscosity Index Improvers Market Trends

The China viscosity index improvers marketis driven by massive automotive production, industrial manufacturing, and lubricant consumption. Strong domestic production of additive chemicals and growing R&D in high-performance polymers are supporting market expansion. The shift toward synthetic and energy-efficient lubricants in response to emission norms is fueling demand for advanced PMA and HSD-based VIIs.

North America Viscosity Index Improvers Market Trends

The North America is expected to grow the fastest with a CAGR of 5.7% during the forecast period. This growth is supported by a strong presence of leading lubricant and additive manufacturers. The demand is largely driven by the U.S., where high-performance engine oils and industrial lubricants are widely used across automotive, energy, and manufacturing sectors. The region’s focus on low-viscosity, fuel-efficient, and extended-drain lubricants continues to boost consumption of advanced VII polymers such as PMA and HSD.

The U.S. viscosity index improvers market remains a technology leader, with major additive manufacturers such as Lubrizol, Afton, and Infineum driving innovation in viscosity modifier chemistry. High adoption of premium-grade engine oils and the growing trend toward electric vehicle lubricants are key growth factors. The country’s focus on improving fuel efficiency and meeting API and ILSAC lubricant standards continues to stimulate demand for performance-enhancing VIIs.

Europe Viscosity Index Improvers Market Trends

Europe’s market is driven by strict emission regulations and sustainability initiatives that promote the use of high-quality, low-viscosity lubricants. The region’s well-developed automotive industry, led by countries such as Germany, France, and the UK, emphasizes the use of synthetic and bio-based lubricants with superior thermal stability and shear resistance. The increasing adoption of electric vehicles and demand for extended drain interval oils are influencing the development of next-generation VIIs. European producers are also focusing on eco-friendly formulations aligned with EU regulatory standards.

The Germany viscosity index improvers market serves as Europe’s innovation hub for lubricant additives and polymer chemistry. As home to major automotive OEMs, the country places strong emphasis on high-performance and environmentally compliant lubricants. German formulators are actively developing low-viscosity, high-shear-stability VIIs for both internal combustion and electric vehicle applications. Moreover, the nation’s commitment to sustainability and R&D-driven manufacturing reinforces its leadership in the European viscosity index improvers market

Latin America Viscosity Index Improvers Market Trends

Latin America growth is supported by economic recovery, industrial growth, and rising vehicle ownership. Countries like Brazil and Mexico are key markets, with growing lubricant demand from the automotive, mining, and agricultural sectors. Increasing infrastructure development and foreign investments in lubricant blending plants are driving regional growth.

Middle East and Africa Viscosity Index Improvers Market Trends

The Middle East & Africa market is emerging as a promising growth region due to industrial expansion and the strengthening of automotive aftermarket activities. The Gulf countries, in particular, are witnessing rising lubricant consumption linked to construction, transportation, and oil & gas operations. Increasing investments in lubricant blending and packaging facilities are helping regional players localize production. Additionally, rising awareness about lubricant quality and performance standards is gradually boosting the adoption of premium VIIs.

Key Viscosity Index Improvers Company Insights

Some of the key players operating in the market include BASF SE, Afton Chemical Corporation, Evonik Industries AG, and The Lubrizol Corporation.

-

BASF SE is a chemical manufacturing company with a presence across Asia Pacific, North America, Central & South America, Europe, and the Middle East & Africa. The company operates through six business segments, namely chemical, material, transmission fluids solutions, surface technologies, agricultural solutions, and nutrition & care. The chemical segment includes petrochemicals and intermediaries. The material segment comprises performance polymers and monomers. The Transmission Fluids solutions segment includes performance chemicals and dispersions & pigments. The agricultural solution segment includes products for farming, landscape management, and pest control. The nutrition & care segment is further sub-segmented into nutrition & health and care. The company provides a wide range of surfactants for textile, paint & coatings, homecare, and food processing industries.

Key Viscosity Index Improvers Companies:

The following are the leading companies in the viscosity index improvers market. These companies collectively hold the largest market share and dictate industry trends.

- BASF SE

- Chevron Oronite Company LLC

- Evonik Industries AG

- Afton Chemical Corporation

- The Lubrizol Corporation

- Sanyo Chemical Industries

- Akzo Nobel N.V.

- Mitsui Chemicals, Inc.

- Petronas

- Para Lubricants Ltd.

- Sika AG

Recent Developments

- In July 2025, Chevron Phillips Chemical announced an expansion of its VII production capacity to meet the growing demand for VIIs in the automotive and industrial sectors.

Viscosity Index Improvers Market Report Scope

Report Attribute

Details

Market size value in 2024

USD 2.8 billion

Market size value in 2026

USD 3.1 billion

Revenue forecast in 2033

USD 4.3 billion

Growth rate

CAGR of 4.7% from 2025 to 2033

Base year for estimation

2024

Historical data

2018 - 2023

Forecast period

2025 - 2033

Quantitative units

Volume in kilotons, revenue in USD million, and CAGR from 2025 to 2033

Report coverage

Revenue forecast, volume forecast, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Japan; South Korea; Brazil; Argentina; Saudi Arabia; South Africa

Key companies profiled

BASF SE; Chevron Oronite Company LLC; Evonik Industries AG; Afton Chemical Corporation; The Lubrizol Corporation; Sanyo Chemical Industries; Akzo Nobel N.V.; LANXESS AG; Mitsui Chemicals, Inc.; Petronas; Para Lubricants Ltd.; Sika AG

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional, and segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Viscosity Index Improvers Market Report Segmentation

This report forecasts volume & revenue growth at the global level and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global viscosity index improvers market report based on product, application, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Polymethacrylater (PMA)

-

Ethylene Propylene Copolymer (OCP)

-

Hydrostyrene Diene Copolymer (HSD)

-

Polyisobutylene (PIB)

-

Other Product (if any)

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Engine Oils

-

Transmission Fluids

-

Hydraulic Fluids

-

Gear Oils

-

Electric Vehicle (EV) Fluids

-

Other Application

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global viscosity index improvers market size was valued at USD 2.8 billion in 2024 and is estimated at USD 3.1 billion for 2026.

The global viscosity index improvers market is expected to grow at a CAGR of 4.7% from 2025 to 2033, reaching USD 4.3 billion by 2033.

The Asia Pacific viscosity index improvers market accounted for the largest revenue share of 46.2% in 2024. The driven by its strong automotive manufacturing base and expanding industrial lubricant demand.

Some key players operating in the viscosity index improvers market include BASF SE; Chevron Oronite Company LLC; Evonik Industries AG; Afton Chemical Corporation; The Lubrizol Corporation; Sanyo Chemical Industries; Akzo Nobel N.V.; LANXESS AG; Mitsui Chemicals, Inc.; Petronas; Para Lubricants Ltd.; Akzo Nobel N.V.; Sika AG

The market growth is primarily driven by the expanding automotive and industrial lubricant sectors, where the demand for high-performance, fuel-efficient, and low- viscosity lubricants continues to rise.

About the Author(s)

Petrochemicals Research Team

Bulk Chemicals · PetrochemicalsThis report was authored by the petrochemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the petrochemicals segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.