- Home

- »

- Next Generation Technologies

- »

-

5G Core Market Size, Share & Growth Report, 2023-2030GVR Report cover

![5G Core Market (2023 - 2030)Report]()

5G Core Market (2023 - 2030)

Size, Share & Trends Analysis Report By Component, By Deployment, By Network Function, By Architecture, By End-user, By Region, And Segment Forecasts

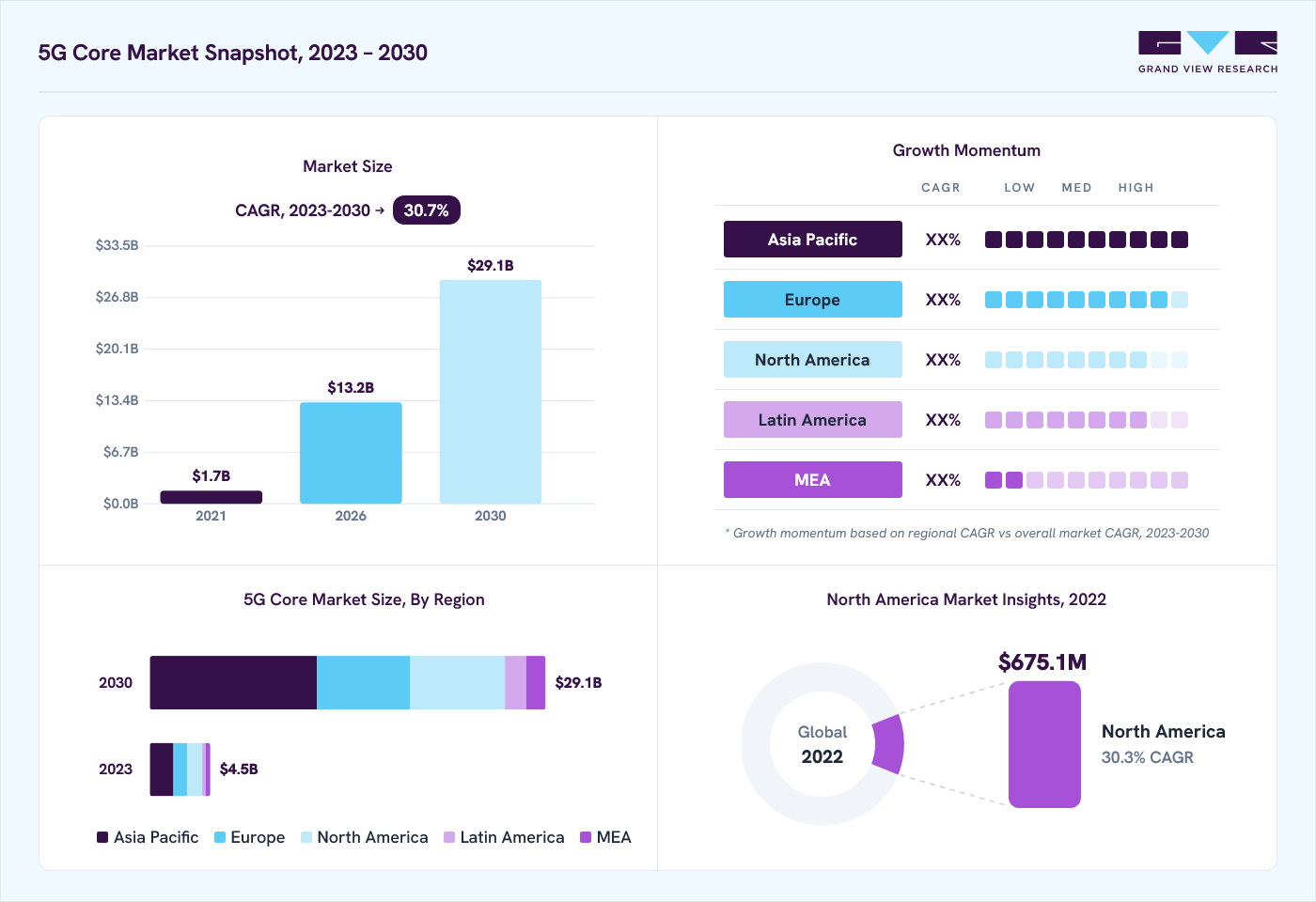

Market Size, 2022

$2.8BMarket Estimate, 2026

$13.2BMarket Forecast, 2030

$30.1BCAGR, 2023–2030

30.7%Report Overview

The global 5G core market size was valued at USD 2.8 billion in 2022 and is projected to grow from USD 13.2 billion in 2026 to USD 30.1 billion by 2030, at a CAGR of 30.7% from 2023 to 2030. Asia Pacific dominated the market, accounting for a revenue share of 38.0% in 2022. Growing adoption of 5G services is anticipated to fuel this growth as the core is the critical component of a 5G network. 5G core creates a dependable, secure connection to the end-user network and grants access to its services. The core network components of 5G are entirely software-based and built for cloud-based operations. Also, the core network is crucial for managing network traffic and storing customer data. To lower Total Cost of Ownership (TCO) and ensure lag-free connectivity, top network providers are moving toward installing cloud-based 5G core networks.

The rising proliferation of connected devices and the explosion of data traffic, there is a growing need for faster and more reliable connectivity. 5G networks promise to deliver faster speeds, lower latency, and higher bandwidth, which is driving demand for the 5G core. In addition, 5G technology is enabling new applications and use cases that were not possible with previous generations of mobile networks.

")

For example, 5G is expected to play a key role in enabling the Internet of Things (IoT), autonomous vehicles, smart cities, and other advanced applications that require high-speed, low-latency connectivity. Thus, the rising adoption of 5G technology is expected to aid the growth of the 5G core industry.

With the growing popularity of real-time applications such as gaming, virtual reality, and augmented reality, there is a significant demand for low-latency connectivity provided by 5G core. This driving need for advanced edge computing capabilities that can process data quickly and efficiently is anticipated to boost the growth of the market.

Moreover, cloud-native architecture is becoming increasingly important in the 5G core industry, as it allows service providers to create more scalable, flexible, and agile networks. By leveraging cloud-native technologies, service providers can reduce their infrastructure costs, improve network performance, and deploy new services more quickly which is driving the adoption of the 5G core technology.

The emergence of 5G core is facilitating new business models such as network-as-a-service (NaaS) and platform-as-a-service (PaaS) models that allow businesses to build their own applications on top of the 5G network. This is creating new revenue streams and driving innovation in a range of industries, including healthcare, transportation, and manufacturing, thereby driving the market growth. Moreover, increasing investments from the government of several countries in 5G technology is anticipated to support the market growth.

As 5G networks become more widespread, security is becoming a major concern for service providers and end-users. 5G cores are more vulnerable to cyberattacks than previous generations of mobile networks, due to the increased complexity and the use of virtualization technologies. However, service providers are investing in advanced security technologies, such as encryption, firewalls, and intrusion detection systems, to protect their networks from cyber threats.

COVID-19 Impact Analysis

The COVID-19 pandemic led to disruptions in the supply chain for 5G core components and equipment. As lockdowns and travel restrictions were put in place, manufacturers faced challenges in sourcing and transporting the necessary components and equipment for 5G core networks. This led to delays in the deployment of 5G networks in some areas. In addition, the pandemic caused a slowdown in investment in 5G infrastructure.

With many businesses facing financial challenges and uncertainty, some businesses delayed or scaled back their plans to invest in 5G networks, which led to a negative impact on the demand for 5G core solutions. However, the pandemic has highlighted the importance of 5G networks in enabling remote work and digital services. With more people working from home and relying on digital services for communication and entertainment, the need for reliable and high-speed connectivity has increased. This has led to increased demand for 5G networks and services, including 5G core solutions.

Component Insights

The software segment dominated the market in 2022 and accounted for a revenue share of more than 67.0%. The growing demand for cloud and virtualization technologies is anticipated to increase the demand for 5G core software. The software component of the 5G core is a critical part of the overall 5G ecosystem as it is based on cloud-native design. The network functions, management, and orchestration systems are completely software-based and are responsible for providing the core services of the network.

The services segment is anticipated to register significant growth over the forecast period. The segment is further bifurcated into professional and managed services. The managed services segment is expected to be the fastest-growing segment during the forecast period. The managed services include services such as deployment, integration, installation, and support & maintenance. The rising adoption of 5G non standalone and standalone core across the globe is predicted to increase the demand for managed services.

In addition, the professional services include consulting, network planning, project management, and others. The professional services segment is expected to grow substantially through the forecast period owing to the growing demand for deploying and optimizing the 5G networks by businesses.

Deployment Insights

The cloud segment accounted for a dominant revenue share of more than 59.0% in 2022. The segment is also anticipated to grow at the fastest CAGR during the forecast period. The cloud deployment model allows service providers to benefit from the scalability, flexibility, and cost efficiency of cloud core architecture while delivering ultra-low latency, high reliability, and enhanced network performance for 5G services which bodes well for the segment growth. Moreover, increasing demand for high-speed data services, low latency, and high network performance is anticipated to further augment the growth of the segment.

The on-premise segment is anticipated to witness significant growth through the forecast period. The on-premise deployment allows service providers to have more control over the network and the ability to customize the deployment to their specific needs, which is expected to fuel the segment growth. Several players are investing in the development of on-premise core solutions to fulfill the demand of their enterprise customers.

For instance, 5G core providers, such as China Mobile Limited and NTT DoCoMo, Inc. are investing in on-premise 5G core deployments to cater to use cases such as industrial automation, robotics, and smart cities. In addition, benefits offered by on-premise deployment such as increased security, lower latency, and high reliability are expected to support the growth of the segment.

Network Function Insights

The user plane function (UPF) segment dominated the market in 2022 and accounted for a revenue share of more than 15.0%. The dominance of the segment can be attributed to the increasing use of data-intensive applications and services, such as video streaming, cloud computing, and virtual reality. UPF is responsible for routing and forwarding user data packets between the user equipment (UE) and the application server, and it plays a critical role in delivering high-quality data services to the end-users.

As the number of connected devices and IoT applications continues to grow, the demand for User Plane Function is expected to increase even further. UPF is essential for providing reliable and efficient connectivity to a wide range of devices and applications, and it is a key component in the 5G network architecture.

The access and mobility management function (AMF) segment and session management function (AMF) segment are some of the important software components of the 5G core network. The segments are expected to witness significant growth during the forecast period owing to rising demand for 5G connectivity and the increasing need for advanced mobile network capabilities.

Architecture Insights

The service-based architecture (SBA) segment held the largest revenue share of more than 56.0% in 2022. The dominance of the segment is due to the increasing demand for 5G services and the need for flexible and scalable network infrastructure. Service-based architectures allow service providers to quickly develop and deploy new services and applications, as well as modify existing services to meet changing customer needs. Moreover, SBAs can enable service providers to more easily integrate new technologies and services into their existing networks, reducing the time and cost of deployment, which is expected to increase the demand for SBA.

The cloud-native architecture segment is predicted to grow at the fastest rate during the forecast period owing to the growing demand for the development of 5G core in cloud-native architecture. In a cloud-native architecture for the 5G core, network functions are designed as microservices that can be independently developed, deployed, and scaled.

Cloud native architectures offer several benefits over traditional architectures, such as better resource utilization, faster deployment, and easier maintenance which is driving the development of the architecture and fueling the growth of the segment. For instance, in February 2022, NEC Corporation announced the general accessibility of its Cloud-Native Converged Core which can be deployed in a traditional private core, on-premise, or the cloud via public cloud or hybrid scenarios.

End-user Insights

The telecom operators segment dominated the market in 2022 and accounted for a revenue share of more than 58.0%. Telecom operators use the 5G core to build application-specific 5G infrastructure to provide their subscribers with a tailored solution. Growing partnerships among 5G core providers and telecom operators to provide 5G services are anticipated to boost segment growth.

For instance, in January 2023, SFR, a French telecommunications company, signed a strategic partnership with Nokia Corporation to deploy its cloud-native 5G Standalone (SA) core network. This will enable SFR to provide its consumer and enterprise customers with advanced 5G services.

")

The enterprises segment is anticipated to register the highest CAGR over the forecast period. The growth of the segment can be attributed to the growing demand for private 5G networks from businesses to establish uninterrupted communication. In addition, the market players are developing creative ways to offer their 5G core networks to their enterprise customers.

For instance, in November 2022, Nokia Corporation added an alternative 5G core as a software-as-a-service (SaaS) for its enterprise customers that are seeking a simpler way to deploy the 5G standalone (SA) core network. The company offers 5G Core SaaS on-demand through a subscription service. This eliminates the upfront cost and the requirement to manage software maintenance and updates through an operator.

Regional Insights

Asia Pacific dominated the 5G core industry in 2022 and accounted for a revenue share of over 38.0%. The regional growth can be attributed to increasing demand for high-speed connectivity across various industries including healthcare, manufacturing, automotive, and entertainment. The market is expected to witness a significant increase in investments and partnerships between governments and private players to accelerate the deployment of 5G and infrastructure development.

For instance, in March 2022, the Chinese government planned to install over 600,000 5G base stations by the end of 2022. In addition, governments across countries such as China, Japan, and South Korea are focused on releasing multiple mmWave and sub-6GHz frequencies to fulfill the rising need for high-speed data connectivity among subscriber bases. Thus, the market in Asia Pacific is expected to witness strong growth throughout the projection period.

North America is anticipated to register significant growth over the forecast period. The growth of the market can be attributed to the presence of prominent players in the region such as AT&T Inc.; Verizon Communications, Inc.; T-Mobile USA, Inc.; and others. The key players are increasing the adoption of advanced technologies, including high-speed connectivity, virtualization, and cloud computing, to deliver innovative and efficient services to businesses and consumers. Moreover, rising government initiatives to support the development of 5G are anticipated to aid the market growth.

Key Companies & Market Share Insights

The market is fragmented with the presence of several small players. The companies are mainly adopting product development strategies, geographical expansion, and partnerships to enhance their product offerings. For instance, in April 2020, British Telecommunication PLC and Telefonaktiebolaget LM Ericsson together signed an agreement to deploy 5G core-based cloud-native mobile packet core for non-standalone and standalone networks to satisfy the high-speed bandwidth demand of enterprises and individual consumers.

Key players are introducing cloud-native core network solutions to offer their customers advanced technology. For instance, in December 2022, Cisco Systems, Inc., and T-Mobile US, Inc., collaborated to launch a cloud-native 5G core gateway. With this launch, the companies aim to take the 5G standalone core network to the next level. T-Mobile US, Inc., moved all of its 4G and 5G traffic to the new cloud native 5G convergent core, boosting network performance for all its customers. Such initiatives are fueling the market’s growth. Some prominent players in the global 5G core market include:

-

Telefonaktiebolaget LM Ericsson

-

Nokia Corporation

-

Huawei Technologies Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

Cisco Systems, Inc.

-

Hewlett Packard Enterprise Company

-

Oracle Corporation

-

Athonet

-

Mavenir

-

Affirmed Networks

5G Core Market Report Scope

Report Attribute

Details

Market size in 2022

USD 2.8 billion

Estimated Market size in 2026

USD 13.2 billion

Projected Market size by 2030

USD 30.1 billion

Growth rate

CAGR of 30.7% from 2023 to 2030

Base year of estimation

2022

Historical data

2018 - 2021

Forecast period

2023 - 2030

Quantitative units

Revenue in USD million and CAGR from 2023 to 2030

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, network function, architecture, end-user, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; U.K.; Germany; France; China; India; Japan; Australia; South Korea; Brazil; Mexico; Kingdom of Saudi Arabia; UAE; South Africa

Key companies profiled

Telefonaktiebolaget LM Ericsson; Nokia Corporation; Huawei Technologies Co., Ltd.; Samsung Electronics Co., Ltd.; Cisco Systems, Inc.; Hewlett Packard Enterprise Company; Athonet; Casa Systems, Inc.; Mavenir; Affirmed Networks; Oracle Corporation

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global 5G Core Market Segmentation

The report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global 5G core market report based on component, deployment, network functions, architecture, end-user, and region:

-

Component Outlook (Revenue, USD Million, 2018 - 2030)

-

Software

-

Services

-

-

Deployment Outlook (Revenue, USD Million, 2018 - 2030)

-

On-premise

-

Cloud

-

-

Network Function Outlook (Revenue, USD Million, 2018 - 2030)

-

Access and Mobility Management Function

-

Session Management Function

-

Policy Control Function

-

Network Exposure Function

-

NF Repository function

-

Unified Data Management

-

Authentication Server Function

-

User Plane Function

-

Application Function

-

Network Slice Selection Function

-

-

Architecture Outlook (Revenue, USD Million, 2018 - 2030)

-

Service-based Architecture

-

Cloud Native Architecture

-

-

End-user Outlook (Revenue, USD Million, 2018 - 2030)

-

Telecom Operators

-

Enterprises

-

-

Regional Outlook (Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

U.K.

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

Kingdom of Saudi Arabia (KSA)

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global 5G core market is expected to grow at a CAGR of 30.7% from 2023 to 2030, reaching USD 30.1 billion by 2030.

The global 5G core market size was valued at USD 2.8 billion in 2022 and is estimated at USD 13.2 billion for 2026.

Asia Pacific dominated with a revenue share of 38.0% in 2022.

Some key players operating in the 5G core market include Telefonaktiebolaget LM Ericsson, Nokia Corporation, Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Cisco Systems, Inc., Hewlett Packard Enterprise Company, Athonet, Casa Systems, Inc., Mavenir, Affirmed Networks, Oracle Corporation.

Key factors that are driving the 5G core market growth include growing demand for low latency enhanced bandwidth connectivity for several mission-critical applications such as V2X and drone connectivity, and the growing demand for high-speed internet to provide seamless connectivity to millions of IIoT devices.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst -

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.