- Home

- »

- Next Generation Technologies

- »

-

Artificial General Intelligence Market Size Report, 2026-2033GVR Report cover

![Artificial General Intelligence Market Size, Share & Trends Report]()

Artificial General Intelligence Market (2026 - 2033) Size, Share & Trends Analysis Report By Deployment (Cloud, On-Premises), By Type (Foundation Model-Based AGI, Autonomous Agent-Based), By End User, By Region, And Segment Forecasts

Market Size, 2025

$200.6MMarket Estimate, 2026

$257.2MMarket Forecast, 2033

$1,555.6MCAGR, 2026–2033

29.3%Artificial General Intelligence Market Summary

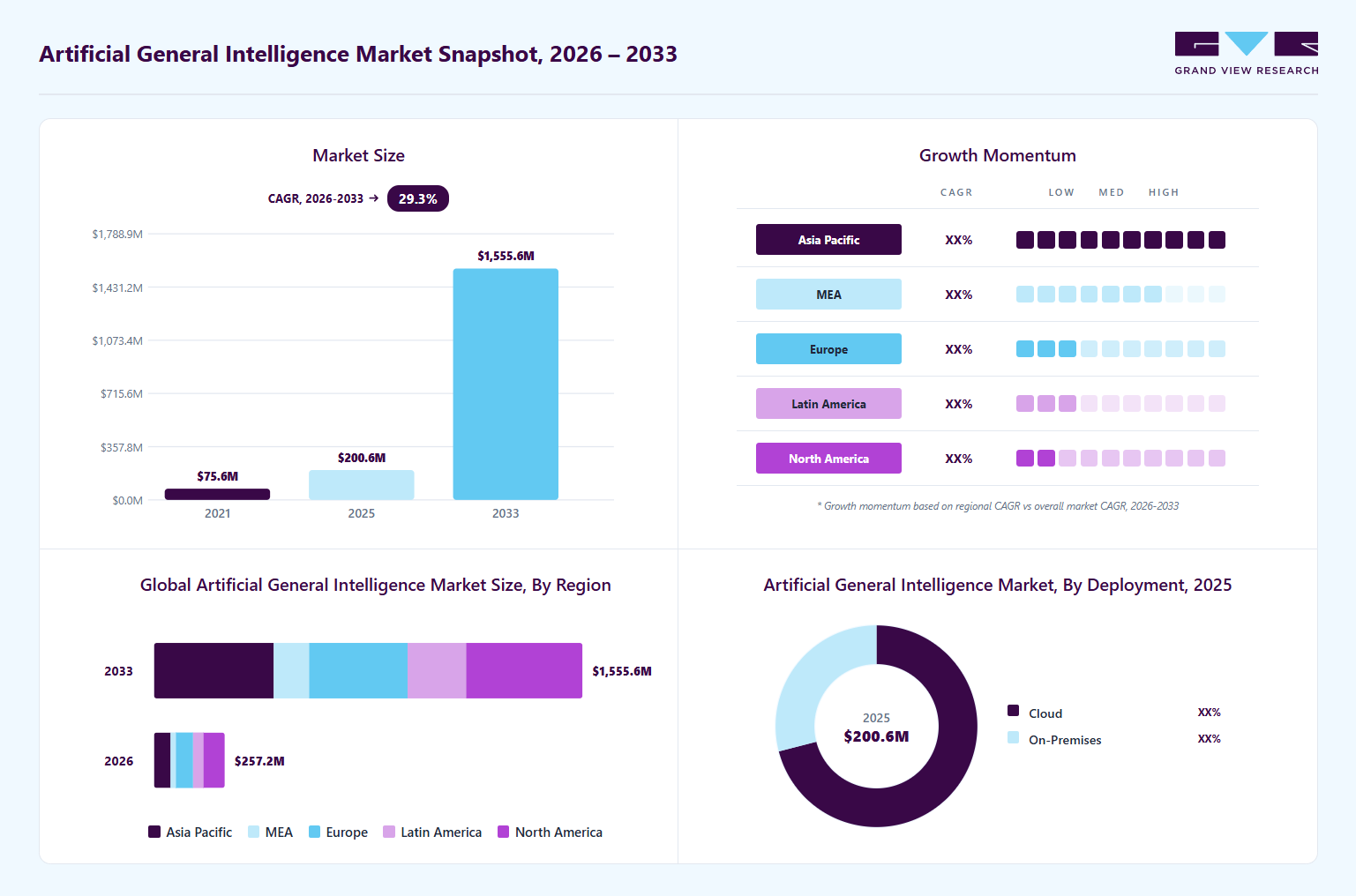

The global artificial general intelligence market size was valued at USD 200.6 million in 2025 and is projected to grow from USD 257.2 million in 2026 to USD 1,555.6 million by 2033, at a CAGR of 29.3% from 2026 to 2033. North America dominated the global industry with the largest revenue share of 30.7% in 2025. The increasing demand for artificial general intelligence is due to the expansion of multimodal AI systems capable of processing text, audio, image, and video data, which is contributing to the growth of the artificial general intelligence (AGI) market across healthcare, manufacturing, retail, and defense sectors.

Key Market Trends & Insights

- The artificial general intelligence market in the U.S. led the North American region and held the largest revenue share in 2025.

- By deployment, the cloud segment led the market and held the largest revenue share of 71.0% in 2025.

- By type, foundation model-based AGI held the dominant position in the market and accounted for the leading revenue share of 39.5% in 2025.

- By end user, the healthcare segment is expected to grow at the fastest CAGR of 32.4% from 2026 to 2033.

Market Size & Forecast

- 2025 Market Size: USD 200.6 Million

- 2033 Projected Market Size: USD 1,555.6 Million

- CAGR (2026-2033): 29.3%

- North America: Largest Market in 2025

Organizations are deploying autonomous AI agents for software development, workflow orchestration, cybersecurity monitoring, and intelligent process automation to improve productivity and reduce manual intervention. Advanced reasoning capabilities and multi-step task execution are increasing enterprise interest in autonomous AI platforms. The rapid growth of enterprise AI ecosystems and cloud-native AI platforms is supporting the deployment of scalable AGI solutions. In addition, increasing demand for real-time analytics and intelligent automation across data-intensive industries is strengthening the commercial adoption of AGI technologies.")

Furthermore, the major technology companies and governments are allocating substantial capital toward advanced AI research, high-performance computing infrastructure, and large-scale model development. The growing commercialization of AI copilots, intelligent agents, and multimodal assistants is expanding enterprise spending on AGI-related technologies. Cloud service providers are also increasing investments in AI accelerators, data centers, and AI orchestration platforms to support advanced cognitive workloads. In addition, collaborations between AI startups, hyperscalers, and research institutions are strengthening innovation across generalized intelligence systems.

The expansion of advanced computing infrastructure and AI processing capabilities is driving the growth by increasing the deployment of AI accelerators, high-performance computing systems, and large-scale data processing environments is supporting the development and training of complex AGI models. The growing availability of distributed computing architectures is also improving the efficiency of large foundation-model operations across enterprise environments. In addition, advancements in semiconductor technologies and AI optimization frameworks are enhancing model scalability and processing speed. Organizations are increasingly adopting advanced AI infrastructure to support intelligent automation, real-time analytics, and cognitive decision-making applications.

Market Dynamics

The expansion of advanced computing infrastructure and multimodal AI capabilities is accelerating the growth of the AGI market. Increasing deployment of AI accelerators, high-performance computing systems, and large-scale data processing environments is improving the efficiency of complex AGI model training and inference operations. Enterprises are investing in scalable computing architectures to support autonomous reasoning systems, intelligent automation platforms, and multimodal cognitive applications across commercial environments.

Meanwhile, growing adoption of multimodal AI systems capable of processing text, image, audio, and video data is increasing the operational capabilities of AGI technologies across industries. Advancements in distributed computing, semiconductor technologies, and AI optimization frameworks are further supporting the commercialization of advanced AGI platforms for enterprise-scale deployment and real-time decision-making applications.

The development of artificial general intelligence systems requires access to large volumes of high-quality, diverse, and accurately labeled datasets to improve reasoning accuracy, contextual understanding, and multimodal learning capabilities. However, limitations associated with data availability, data privacy regulations, and biased or fragmented datasets create challenges in training advanced AGI models across enterprise environments. In addition, the increasing complexity of foundation models and autonomous AI systems is raising demand for specialized expertise in machine learning, reinforcement learning, multimodal AI, and cognitive computing architectures.

The shortage of highly skilled AI researchers, data scientists, and advanced computing specialists is limiting the scalability and commercialization of AGI technologies across industries. Enterprises and AI developers also face challenges related to high talent acquisition costs, intense competition for AI expertise, and limited availability of experienced professionals capable of managing large-scale AGI systems. These factors are slowing the development, deployment, and optimization of advanced autonomous intelligence platforms in the global AGI industry.

Healthcare organizations are integrating advanced cognitive AI systems into medical imaging, clinical decision support, molecular analysis, and patient monitoring applications to improve diagnostic accuracy and operational efficiency. The growing availability of healthcare data and advancements in multimodal AI models are supporting the development of intelligent systems capable of processing complex clinical information across multiple formats. In addition, rising demand for precision medicine and personalized treatment approaches is accelerating the deployment of AGI-enabled analytical platforms across hospitals and research institutions. Autonomous reasoning systems and AI-driven research platforms are improving the analysis of large-scale biomedical datasets and reducing the complexity associated with therapeutic development. The integration of AGI into healthcare research environments is also supporting faster identification of disease patterns, treatment responses, and biomarker analysis. Furthermore, increasing investments in AI-assisted healthcare infrastructure and intelligent automation technologies are contributing to the expansion of AGI applications across life sciences and clinical research operations.

Market Concentration & Characteristics

The impact of regulations on the industry remains medium due to increasing focus on AI governance, transparency, data privacy, and responsible AI deployment practices. Regulatory authorities and standards organizations are introducing frameworks related to AI safety, cybersecurity, model accountability, and ethical AI development across enterprise environments. Compliance requirements associated with sensitive data handling and autonomous decision-making systems are influencing enterprise deployment strategies. In addition, organizations are increasingly investing in explainable AI, secure AI infrastructure, and governance frameworks to align with evolving regulatory expectations.

End-user concentration is significant, with demand primarily concentrated across IT & telecommunications, healthcare, BFSI, government, and advanced manufacturing sectors. These industries generate significant demand for autonomous AI systems, intelligent automation platforms, and advanced analytical capabilities due to their high data intensity and operational complexity. Enterprise adoption is increasing across organizations requiring real-time decision-making, workflow optimization, and multimodal intelligence applications. In addition, rising investments in AI infrastructure and cognitive automation technologies across these sectors are contributing to sustained AGI commercialization activities.

Type Insights

The foundation model-based AGI segment led the industry and accounted for 39.5% of the global revenue in 2025. The growth of foundation model-based AGI systems is driven by increasing enterprise demand for advanced reasoning, contextual understanding, and multimodal intelligence capabilities. Organizations are integrating large-scale foundation models into workflow automation, content generation, customer interaction, and enterprise knowledge management applications to improve operational efficiency. Moreover, the expansion of cloud-based AI ecosystems and API-driven deployment models is increasing accessibility to advanced cognitive AI technologies across industries.

The autonomous agent-based AGI segment is predicted to foresee significant growth in the forecast period, due to rising demand for intelligent task execution, autonomous decision-making, and workflow orchestration across enterprise environments. Advancements in reasoning models, memory architectures, and multi-step execution capabilities are enhancing the operational efficiency of autonomous AI systems. Furthermore, the growing integration of agentic AI into enterprise platforms and digital ecosystems is supporting the expansion of autonomous agent-based AGI technologies across multiple industry verticals.

Deployment Insights

The cloud segment accounted for the largest market revenue share of 71.0% in 2025, driven by the increasing adoption of cloud-based AGI platforms by organizations to access advanced foundation models, autonomous AI agents, and multimodal intelligence systems without investments. The expansion of hyperscale data centers and AI cloud ecosystems is further improving accessibility to high-performance AI workloads and real-time processing capabilities. It supports faster integration, continuous model updates, and flexible enterprise scalability, contributing to the increasing commercialization of AGI technologies.

The on-premises segment is predicted to foresee significant growth in the forecast period, anticipated due to the rising concerns related to data privacy, cybersecurity, and regulatory compliance across enterprises and government organizations. Industries such as BFSI, healthcare, and defense are deploying private AGI infrastructure to maintain greater control over sensitive operational and customer data. Increasing demand for secure AI environments and localized processing capabilities is further supporting the deployment of on-premises AGI systems.

End User Insights

The IT & telecommunications segment held the highest market share of 25.3% in 2025. The adoption of this market in this sector is increasing due to rising demand for intelligent automation, autonomous network management, and advanced software engineering capabilities. The growing use of autonomous AI agents and coding intelligence platforms is further supporting enterprise adoption across digital infrastructure environments. In addition, increasing investments in cloud computing, AI-native applications, and hyperscale data centers are strengthening the deployment of AGI systems across the IT & telecommunications industry.

The healthcare segment is predicted to foresee significant growth in the forecast period. The growth is driven by increasing demand for advanced diagnostics, clinical decision support, and intelligent patient management systems. Healthcare organizations are integrating multimodal AI and autonomous reasoning platforms into medical imaging, drug discovery, and personalized treatment applications to improve diagnostic accuracy and operational efficiency. Furthermore, increasing adoption of AI-assisted automation in administrative workflows and patient engagement systems is contributing to the expansion of AGI applications in healthcare environments.

Regional Insights

North America dominated the market with a 30.7% revenue share in 2025, due to the strong presence of hyperscale AI companies, advanced semiconductor ecosystems, and large-scale AI research initiatives. Enterprises across the region are increasing investments in autonomous AI systems, multimodal intelligence platforms, and foundation-model integration to improve operational efficiency and digital transformation capabilities. The region also benefits from high adoption of cloud-native AI environments and enterprise automation technologies across multiple industries

U.S. Artificial General Intelligence Market Trends

The artificial general intelligence market in the U.S. is driven by extensive investments in foundation-model development, autonomous AI agents, and advanced AI computing infrastructure. The country hosts major AGI ecosystem participants involved in multimodal AI, intelligent automation, and cognitive reasoning platform development across enterprise and commercial applications. Additionally, strong venture capital activity and continuous innovation in AI accelerators, large language models, and agentic AI systems are contributing to the expansion of the AGI market in the U.S.

Europe Artificial General Intelligence Market Trends

The artificial general intelligence market in Europe is driven by increasing focus on ethical AI development, regulatory standardization, and enterprise adoption of secure cognitive AI systems. Rising investments in autonomous AI infrastructure and trusted AI frameworks are further supporting the deployment of advanced AGI systems across enterprise environments. Additionally, the growing focus on explainable AI and compliant AI governance models is contributing to the expansion of AGI adoption across European industries.

Asia Pacific Artificial General Intelligence Market Trends

The artificial general intelligence market in Asia Pacific is supported by rapid digital transformation, expanding AI startup ecosystems, and increasing deployment of intelligent automation technologies across enterprises. Organizations in the region are adopting AGI systems for smart manufacturing, robotics, digital commerce, and AI-enabled public services to improve operational productivity and analytical capabilities. Furthermore, the rising adoption of multimodal AI platforms and intelligent robotics applications is contributing to the commercialization of AGI technologies across Asia Pacific.

Key Artificial General Intelligence Company Insights

Some key companies in the artificial general intelligence industry are OpenAI, Microsoft, Google LLC, and Amazon Inc.

-

OpenAI develops advanced artificial intelligence systems focused on reasoning, multimodal intelligence, autonomous agents, and large-scale foundation models. The company provides AI platforms and models used across enterprise productivity, software engineering, research, education, and content generation applications. Its product ecosystem includes conversational AI systems, coding intelligence platforms, and multimodal AI technologies designed for commercial and enterprise deployment. OpenAI also focuses on AI safety, model alignment, and scalable AI infrastructure to support advanced cognitive computing applications.

-

Microsoft integrates AI technologies into cloud infrastructure, productivity applications, cybersecurity platforms, and enterprise workflow systems to improve operational efficiency and digital transformation capabilities. Its AI portfolio includes intelligent copilots, autonomous AI agents, developer tools, and advanced cloud-based AI services designed for enterprise-scale deployment. Microsoft also focuses on expanding AI infrastructure through hyperscale cloud environments, AI accelerators, and data center investments to support advanced computing workloads. Its expanding AI ecosystem supports the commercialization of advanced artificial intelligence and agentic AI applications across multiple industries.

Key Artificial General Intelligence Companies

The following key companies have been profiled for this study on the artificial general intelligence market.

-

OpenAI

-

Google LLC

-

Anthropic

-

Meta

-

xAI

-

NVIDIA

-

DeepSeek

-

Microsoft

-

Amazon Inc.

-

Mistral Solutions Pvt. Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: OpenAI; Anthropic; Google LLC; NVIDIA

- Focus on foundation model development and enterprise AI integration across cloud ecosystems.

- Increase investments in AI accelerators, reasoning models, and multimodal AI platforms to improve enterprise-scale deployment capabilities.

- Strong semiconductor capabilities and enterprise AI ecosystems support large-scale AGI deployment and commercialization.

- Extensive AI research capabilities, proprietary datasets, and high capital investments support faster development.

- High operational costs of model training and infrastructure maintenance impact scalability.

- Regulatory compliance, cybersecurity risks, and AI reliability concerns create operational and governance challenges.

Emerging Players: xAI; DeepSeek; Mistral Solutions Pvt. Ltd.

- Focus on lightweight AI architectures, specialized foundation models, and open-source AGI development approaches.

- Collaborate with cloud providers and enterprises to expand autonomous AI and multimodal intelligence applications.

- Faster innovation cycles and flexible model customization support niche AGI application development.

- Focus on computational efficiency and open-source ecosystems to improve accessibility and lower-cost AI deployment.

- Limited access to advanced computing infrastructure and large-scale training datasets restricts commercialization scale.

- Lower enterprise penetration and competition from hyperscalers create challenges.

Recent Developments

-

In May 2025, Anthropic announced the launch of Claude Opus 4 and Claude Sonnet 4, its next-generation AI models designed to advance coding, reasoning, and autonomous task execution capabilities. The company stated that Claude Opus 4 is its most powerful model to date, capable of handling complex, long-duration workflows and agentic tasks with improved accuracy and reliability. The release also introduces enhanced memory, tool-use functionality, and developer integrations, strengthening Anthropic's position in the race toward more capable and general-purpose AI systems.

-

In May 2025, Google DeepMind announced significant enhancements to its Gemini AI platform at Google I/O 2025, including the introduction of Gemini 2.5 Pro with Deep Think, an advanced reasoning mode designed to tackle complex problems. The update also expands agentic AI capabilities, enabling Gemini to perform more sophisticated multi-step tasks across applications and workflows. These developments reinforce Google's efforts to advance frontier AI systems and accelerate progress toward more capable general-purpose intelligence.

Artificial General Intelligence Market Report Scope

Report Attribute

Details

Market size in 2025

USD 200.6 million

Market size in 2026

USD 257.2 million

Revenue forecast in 2033

USD 1,555.6 million

Growth rate

CAGR of 29.3% from 2026 to 2033

Base year for estimation

2025

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Deployment, type, end user, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Europe; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

OpenAI; Google LLC; Anthropic; Meta; xAI; NVIDIA; DeepSeek; Microsoft; Amazon Inc.; Mistral Solutions Pvt. Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Artificial General Intelligence Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global artificial general intelligence market report based on deployment, type, end user, and region.

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-Premises

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Foundation Model-Based AGI

-

Autonomous Agent-Based AGI

-

Multi-Modal AGI Systems

-

Hybrid Cognitive AGI

-

-

End User Outlook (Revenue, USD Million, 2021 - 2033)

-

Healthcare

-

BFSI

-

IT & Telecommunications

-

Manufacturing

-

Government

-

Aerospace & Defense

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Custom Research Modules Delivered

Strategic Value / Business Impact

Market Entry & Expansion Assessment

Regional demand sizing and forecasting

Customer segmentation and buying behavior analysis

Competitive landscape benchmarking

Regulatory and distribution channel assessment

Identified high-growth market opportunities Supported go-to-market strategy development

Highlighted investment priorities and risks

Enabled data-driven expansion planning

Product Positioning & Competitive Intelligence

Product benchmarking and feature comparison

Pricing and value proposition analysis

Brand perception and customer preference study

Competitor strategy evaluation

Improved product differentiation strategy

Supported pricing optimization

Identified unmet customer needs

Enhanced competitive positioning

Technology & Innovation Assessment

Emerging technology trend analysis

Innovation pipeline

Technology adoption readiness assessment

Ecosystem and partnership mapping

Identified future growth areas

Supported innovation roadmap planning

Evaluated commercialization potential

Strengthened strategic partnership decisions

Frequently Asked Questions About This Report

The global artificial general intelligence market size was estimated at USD 200.6 million in 2025 and is expected to reach USD 257.2 million in 2026.

The global artificial general intelligence market is expected to grow at a compound annual growth rate of 29.3% from 2026 to 2033 to reach USD 1,555.6 million by 2033.

North America dominated the artificial general intelligence market with a share of 30.7% in 2025. Enterprises across the region are increasing investments in autonomous AI systems, multimodal intelligence platforms, and foundation-model integration to improve operational efficiency and digital transformation capabilities.

Some key players operating in the artificial general intelligence market include OpenAI, Google LLC, Anthropic, Meta, xAI, NVIDIA, DeepSeek, Microsoft, Amazon Inc., Mistral Solutions Pvt. Ltd.

Key factors that are driving the market growth include the expansion of multimodal AI systems capable of processing text, audio, image, and video data.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.